ID : MRU_ 435483 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

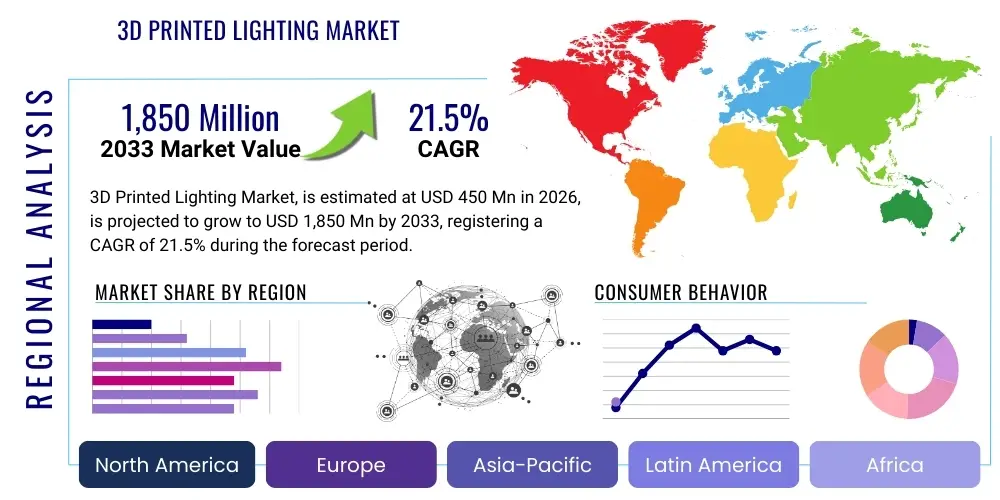

The 3D Printed Lighting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2026 and 2033. The market is estimated at $450 Million USD in 2026 and is projected to reach $1,850 Million USD by the end of the forecast period in 2033.

The 3D Printed Lighting Market encompasses the design, manufacture, and distribution of illumination fixtures, components, and complete systems utilizing additive manufacturing (AM) technologies. This market is fundamentally shifting traditional lighting production paradigms by enabling rapid prototyping, complex geometrical designs previously unattainable with conventional methods like injection molding or casting, and highly customized end-use products. The technology leverages various processes, including Selective Laser Sintering (SLS), Fused Deposition Modeling (FDM), and Stereolithography (SLA), using materials such as polymers, resins, and increasingly, specialized metals and ceramics, tailored for optimal light transmission, diffusion, and heat dissipation requirements.

Major applications span architectural, decorative, industrial, and automotive sectors, driven by the demand for bespoke aesthetics and functional efficiency. In architectural lighting, 3D printing allows for seamless integration of fixtures into building structures, optimizing light distribution and minimizing material waste. Decorative lighting benefits significantly from the design freedom offered by AM, facilitating intricate lattice structures and organic forms that define modern interior design. Furthermore, the ability to produce on-demand spare parts and limited-edition runs reduces inventory holding costs and addresses obsolescence challenges prevalent in the fast-paced lighting industry.

The primary benefits driving market adoption include unprecedented design complexity, reduced manufacturing lead times, enhanced material utilization leading to sustainability advantages, and the capacity for mass customization—a critical factor in high-end commercial and hospitality projects. Driving factors are rooted in the continual advancements in AM material science, the decreasing cost of high-resolution 3D printers, and the growing focus on energy-efficient LED integration, where custom-designed heat sinks and optical elements are crucial for performance and longevity. The convergence of lighting design software with AM workflows further accelerates innovation and market penetration.

The 3D Printed Lighting Market is poised for exponential growth, largely catalyzed by increasing demand for personalized and aesthetically unique lighting solutions across commercial and residential sectors. Key business trends indicate a strong shift towards localized manufacturing and 'digital inventories,' reducing reliance on complex global supply chains. Furthermore, strategic partnerships between large lighting manufacturers and dedicated additive manufacturing service bureaus are becoming commonplace, focusing on integrating complex optical components and lightweight fixture designs. Technology advancements, particularly in high-speed sintering processes and the qualification of fire-resistant and UV-stable polymers, are enhancing product viability and durability, addressing previous constraints related to material limitations and volume production scalability.

Regionally, North America and Europe currently dominate the market due to the early adoption of advanced manufacturing technologies, robust architectural design communities, and significant investments in smart city infrastructure requiring customized, IoT-integrated fixtures. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth, fueled by rapid urbanization, substantial investments in commercial infrastructure (hotels, retail, offices), and the rising establishment of regional AM hubs in countries like China, Japan, and South Korea, which are increasingly using 3D printing to bypass traditional prototyping cycles and accelerate time-to-market for consumer and industrial lighting products.

Segment trends reveal that Selective Laser Sintering (SLS) technology maintains a leading share due to its capability to produce strong, durable, complex parts without support structures, ideal for fixture bodies and diffusers. The Decorative Lighting application segment, encompassing customized chandeliers, pendants, and sconces, is the largest revenue generator, leveraging the unique aesthetic possibilities of AM. Material-wise, high-performance plastics (like Nylon 12) remain central, but there is an accelerating trend towards utilizing specialized opaque and translucent resins and advanced metal alloys for superior thermal management in high-power LED installations, reflecting a growing maturity and diversification within the material ecosystem.

User queries regarding the impact of Artificial Intelligence (AI) on the 3D Printed Lighting Market typically center on three core areas: the automation of complex design workflows, the optimization of print parameters for structural and thermal performance, and the creation of generative designs tailored precisely to specific environmental lighting needs. Users are concerned with how AI can democratize sophisticated design processes, enabling faster iteration cycles and reducing the dependency on highly specialized engineering expertise. Key expectations revolve around AI’s ability to predict material behavior during printing, minimize failure rates, and instantaneously generate optimal lattice structures that maximize light diffusion while minimizing material consumption, thus driving down overall production costs and improving sustainability metrics within the lighting industry supply chain.

The 3D Printed Lighting Market is significantly influenced by powerful market forces that both accelerate and constrain its growth trajectory. Key drivers include the overwhelming need for product customization and the efficiency gains derived from localized, decentralized manufacturing models, which are particularly appealing to architects and interior designers seeking bespoke fixtures. Opportunities are vast, especially in the development of multi-material printing capabilities—such as integrating conductive traces or light guides during the printing process—which promise true functional integration rather than just aesthetic component creation. However, the market faces strong restraints, primarily concerning the initial high capital expenditure required for industrial-grade AM systems and, crucially, the perceived limitations in achieving the ultra-smooth surfaces and optical clarity required for high-end optical components using current polymer printing technologies, often necessitating post-processing steps that negate some of the speed benefits of AM.

Impact forces are predominantly driven by technological evolution and standardization efforts. As industrial 3D printing systems become faster and more reliable, scaling up production volumes becomes feasible, moving the technology beyond exclusive use in prototyping or low-volume customization toward mid-volume manufacturing. Standardization of materials and rigorous testing protocols for heat management and fire safety (especially for large architectural installations) are critical impact forces determining insurance coverage and regulatory acceptance. The shift towards sustainable design also exerts major pressure, compelling manufacturers to utilize AM's low-waste capabilities and bio-based materials, further embedding 3D printing into core corporate social responsibility (CSR) initiatives.

The transition from traditional subtractive and formative manufacturing methods is not seamless; the high volume of legacy tooling and entrenched expertise in conventional methods represents a structural hurdle. However, the rapidly expanding ecosystem of specialized software—from topology optimization to print preparation—acts as a continuous force multiplier, lowering the barrier to entry for design engineers. The ability to iterate designs rapidly for LED cooling solutions, a constant challenge in high-intensity lighting, provides a compelling economic incentive that continuously pushes the market forward, mitigating some of the restraints related to material certification and initial investment costs.

The 3D Printed Lighting Market is segmented based on the core technologies used for manufacturing, the types of materials employed, the specific applications where the fixtures are deployed, and the end-user demographics. This segmentation is crucial for understanding the varied adoption rates and market dynamics across different industrial verticals. Technology differentiation, particularly between powder-bed fusion methods like SLS, which excels in complex geometries and structural components, and vat photopolymerization methods like SLA, which offers higher surface finish and optical precision, defines capability boundaries and cost structures within the market. Material choice dictates performance characteristics, such as light diffusion (polymers/resins) versus thermal management (metals/ceramics), fundamentally impacting where the 3D-printed products can be used.

The value chain of the 3D Printed Lighting Market is distinct from traditional lighting manufacturing, characterized by a tight integration between design, material supply, and digital fabrication processes. The upstream segment is dominated by material suppliers, including chemical companies developing specialized photo-polymers and engineering-grade thermoplastics (like flame-retardant Nylon 12 and translucent resins), and hardware manufacturers providing advanced 3D printing platforms. Key activities here involve rigorous material qualification for optical properties, thermal stability, and fire safety standards. The competitive advantage upstream rests on developing materials that minimize post-processing requirements and enable multi-color or multi-material printing capabilities.

The midstream involves software providers (CAD, topology optimization, build preparation software), 3D printing service bureaus, and dedicated lighting OEMs that have integrated AM capabilities in-house. Service bureaus, which often possess a diverse range of high-end industrial printers, play a crucial role in enabling small and medium-sized design firms to access the technology without massive capital investment. Fabrication efficiency, quality control, and the management of large digital design libraries are central to the value capture in this stage. Post-processing activities, such as smoothing, polishing, coloring, and assembly with electronic components (LEDs, drivers), are also critical midstream steps ensuring the functional readiness of the final fixture.

The downstream segment focuses on distribution and installation. Distribution channels are shifting; while traditional lighting wholesalers and distributors still hold relevance for standard product lines, customized 3D-printed fixtures are increasingly distributed directly to architects, interior designers, and specialized lighting consultants (direct channel). Indirect channels, such as e-commerce platforms specializing in customizable goods, also contribute significantly. Direct involvement allows manufacturers to maintain tight control over the customization process and ensure the integrity of complex bespoke installations, offering specialized technical support directly to the end-user or installer, thereby completing a highly collaborative value loop.

Potential customers for 3D Printed Lighting solutions are primarily clustered in sectors demanding high aesthetic customization, rapid iteration, and superior functional integration, often requiring low-volume, high-value components. The architectural and interior design communities represent the largest demographic of buyers, specifically for large commercial projects, luxury residential developments, and specialized public spaces like museums or galleries. These buyers seek light fixtures that are seamlessly integrated into the building’s design language, often requiring unique shapes, specific color temperatures, and precise light throw angles that conventional mass-produced products cannot achieve. The allure is the ability to create truly signature lighting installations that serve as defining features of a space.

Another major segment comprises the hospitality industry, particularly upscale hotel chains and bespoke restaurant groups. These establishments prioritize unique ambiance and branding through custom lighting. They leverage 3D printing to create differentiated fixtures that can be rapidly iterated and deployed across new property openings globally, ensuring brand consistency while offering localized design variations. The rapid replacement capability offered by digital inventories is highly attractive here, allowing hotels to quickly reprint damaged fixtures, even years after the initial installation, avoiding the long lead times associated with custom traditional manufacturing.

Furthermore, specialized industrial buyers, including automotive manufacturers and aerospace firms, utilize 3D printing for functional lighting, focusing on lightweight, high-performance components such as custom heat sinks for LED arrays or complex internal reflectors and diffusers. These customers prioritize performance metrics, such as weight reduction and specific thermal management capabilities, over pure aesthetics. The ability to produce small batches of specialized replacement parts for niche machinery or vintage vehicles also makes AM highly valuable to industrial maintenance and restoration teams.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $450 Million USD |

| Market Forecast in 2033 | $1,850 Million USD |

| Growth Rate | 21.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Signify, OSRAM, GigaForce, Stratasys, Materialise, HP, EOS GmbH, SLM Solutions, 3D Systems, Luxion, KUKA, Formlabs, TRILUX, Kreon, Delta Light, RZB Lighting, Voxeljet, Carbon, GE Additive, Coherent |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for 3D Printed Lighting is dominated by advancements in four main categories of additive manufacturing that cater to different requirements of the fixture: structural strength, thermal performance, light diffusion, and surface finish. Selective Laser Sintering (SLS) is favored for producing complex, structural housing components because it offers isotropic properties and does not require support structures, leading to faster, cleaner parts suitable for load-bearing applications. The material flexibility of SLS, particularly engineering-grade Nylon 12, allows for good heat resistance and durability, which are paramount for ensuring the longevity of integrated LED electronics. However, SLS parts typically have a slightly rough surface finish, often requiring secondary surface treatments like vapor smoothing or painting for high-end decorative or architectural applications.

Stereolithography (SLA) and Digital Light Processing (DLP) are pivotal for the production of transparent or highly translucent components, such as lenses, diffusers, and light guides, where optical clarity and smooth surfaces are non-negotiable. Recent breakthroughs in high-temperature, optically clear resins allow these methods to produce components that can withstand the operational heat generated by high-power LEDs without yellowing or warping. The challenge remains scaling these vat polymerization technologies to produce larger fixture components economically while maintaining strict quality control over clarity and refractive index uniformity across the entire part geometry.

FDM technology, while lower in resolution, remains relevant for rapid prototyping and the production of large, non-critical components or customized mounting hardware, benefiting from the cost-effectiveness and accessibility of materials like ABS and PLA. Furthermore, the integration of advanced materials, particularly metal printing (e.g., using Selective Laser Melting or Binder Jetting of aluminum alloys), is rapidly expanding for producing high-efficiency, geometrically optimized heat sinks. These advanced thermal management components are crucial for high-performance architectural and industrial lighting systems, allowing LEDs to operate at optimal temperatures and brightness levels, thereby significantly extending their lifespan.

The primary cost savings stem from reduced tooling expenses, minimized material waste (especially in complex designs), and significantly shorter lead times for design iteration and low-volume production. Digital inventory management also eliminates costs associated with warehousing and obsolescence of physical stock.

Stereolithography (SLA) and Digital Light Processing (DLP) technologies are most suitable for transparent components due to their high resolution and ability to use optically clear resins, providing the surface finish and clarity required for light transmission and precise optical function.

3D printing inherently reduces waste through optimized topology design and direct material use. It also enables localized production (reducing transport emissions) and facilitates the creation of durable, modular designs that simplify repair and component replacement, extending product life cycles.

Key limitations include achieving regulatory compliance for fire safety in large installations with certain polymers, ensuring long-term UV and heat stability without degradation, and economically achieving the ultra-smooth, high-clarity surfaces needed for precision optical elements without extensive post-processing.

The Decorative Lighting and Hospitality segments are expected to experience the fastest growth, driven by the strong consumer and commercial demand for bespoke, high-aesthetic fixtures and the technological capability of AM to deliver complex, signature designs rapidly.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.