ID : MRU_ 438317 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

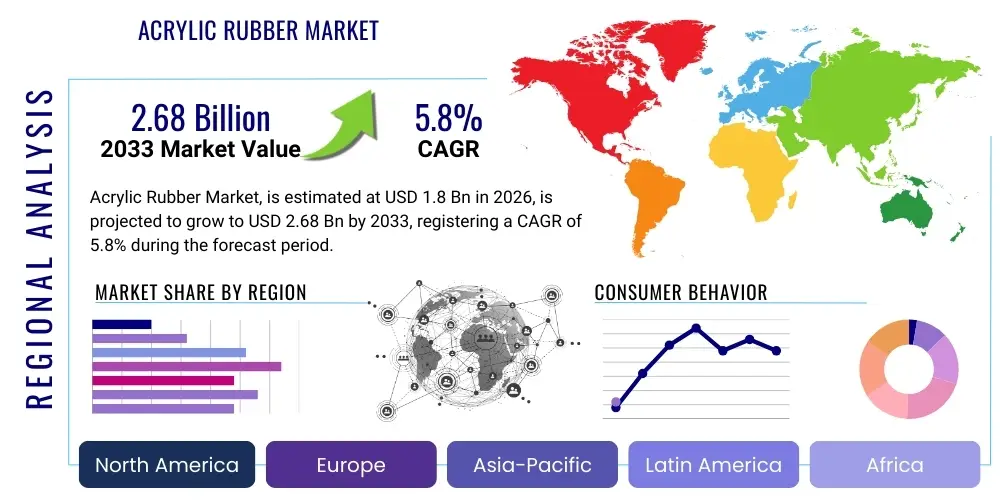

The Acrylic Rubber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $1.8 Billion in 2026 and is projected to reach $2.68 Billion by the end of the forecast period in 2033.

Acrylic rubber, primarily encompassing Acrylate Copolymer Rubber (ACM) and Ethylene Acrylate Rubber (AEM), represents a critical segment within the specialty elastomers industry, valued particularly for its superior thermal resistance and oil compatibility. These synthetic rubbers are derived from acrylic ester monomers, such as ethyl acrylate and butyl acrylate, offering a unique blend of high-temperature resilience, often maintaining performance integrity up to 150°C to 170°C, and excellent resistance to hot oils, transmission fluids, and ozone degradation. Unlike standard natural or commodity synthetic rubbers, acrylic elastomers are specifically engineered for highly demanding environments where heat aging and fluid immersion are constant challenges. This makes them indispensable in modern engineering applications, particularly within the automotive and industrial sectors where component reliability under harsh conditions is paramount for operational safety and longevity. The introduction of improved curing systems, such as amine and metal soap methods, has further enhanced their mechanical properties, including tensile strength and compression set characteristics, cementing their role as a high-performance material choice.

The product portfolio within the acrylic rubber market is diverse, catering to specific performance requirements. ACM is widely utilized for general sealing applications requiring resistance to hot air and mineral oils, making it a mainstay in automotive transmissions and engine compartments. AEM, often marketed under proprietary names, exhibits enhanced low-temperature flexibility and improved chemical resistance due to the inclusion of ethylene units in its polymer backbone, thereby expanding its usage into demanding applications like vibration damping and critical hose linings. The inherent benefits of these materials, including vibration dampening capabilities, excellent color stability, and ease of processing compared to fluoroelastomers (FKM), contribute significantly to their steady market adoption. Furthermore, the push towards vehicle lightweighting and the increasing complexity of engine designs, which necessitate materials capable of operating closer to heat sources, are foundational driving forces behind the sustained demand for acrylic rubber grades.

Major applications of acrylic rubber are concentrated in the automotive sector, accounting for the largest share of consumption, where they are essential components for gaskets, seals, O-rings, shaft seals, and hydraulic system hoses. Beyond vehicles, industrial machinery, specifically in applications requiring resilience against lubricating oils and high operating temperatures such as manufacturing equipment and heavy-duty compressors, rely heavily on acrylic elastomers. Key market driving factors include the rapid growth of electric vehicles (EVs), which utilize specialized sealing materials for battery cooling systems and thermal management, and increasingly stringent emission regulations globally, which demand more durable and reliable engine components to ensure long-term performance and minimize environmental impact. The ongoing research into developing ultra-high temperature resistant grades and bio-based alternatives also shapes the competitive landscape and future trajectory of this highly specialized market segment.

The Acrylic Rubber Market demonstrates robust expansion, driven primarily by technological advancements in the global automotive industry and the growing penetration of specialty elastomers in high-performance sealing solutions. Business trends indicate a strategic focus by major manufacturers on diversifying product portfolios, particularly through the development of high-performance Ethylene Acrylate Rubber (AEM) grades, which offer superior low-temperature performance compared to traditional Acrylate Copolymer Rubber (ACM). This innovation addresses a key historical limitation of ACM and opens avenues in colder climate applications and complex EV thermal management systems. Furthermore, manufacturers are investing heavily in optimizing compounding techniques to improve resistance to modern synthetic lubricants and biodiesel fuels, a necessity arising from evolving engine oil formulations and environmental mandates. Consolidation through strategic mergers and acquisitions remains a persistent theme, aimed at securing raw material supply chains and expanding geographic reach, ensuring cost competitiveness against substitute elastomers like HNBR and FKM.

Regionally, the Asia Pacific (APAC) market maintains its dominance, largely fueled by the massive automotive manufacturing bases in China, India, and Japan. This region is not only a major consumer but also an increasingly significant production hub, benefiting from lower operating costs and burgeoning local demand for durable components in both passenger and commercial vehicles. North America and Europe, while characterized by slower overall vehicle production growth compared to APAC, exhibit a disproportionately high demand for premium, high-specification acrylic rubber components, particularly those certified for strict aerospace and advanced industrial applications. These mature markets are leading the adoption curve for next-generation acrylic elastomers specifically designed for Electric Vehicle (EV) battery sealing and thermal runaway prevention, reflecting a quality-over-volume market structure driven by stringent regulatory frameworks focusing on vehicle safety and environmental compliance.

Segment trends highlight the automotive application segment as the definitive market leader, projected to experience accelerated growth due to the shift towards electrification. Within the application types, Gaskets and Seals continue to hold the largest market share, but the Hoses segment, crucial for engine cooling and turbocharger systems, is forecasted to exhibit the highest CAGR as engine compartments become increasingly confined and subject to intense thermal stress. From a product perspective, while ACM remains the workhorse of the market, the adoption rate of AEM is increasing substantially. This shift is driven by AEM's unique ability to bridge the performance gap between ACM (high heat resistance) and general-purpose rubbers (better low-temperature flexibility), making it highly suitable for demanding modern powertrain systems and critical EV components where performance across a wide temperature spectrum is non-negotiable. Overall, the market's trajectory is firmly linked to innovation in mobility and industrial reliability standards.

User queries regarding AI's influence in the acrylic rubber domain predominantly center on optimizing polymerization processes, predicting material performance under extreme conditions, and automating quality control in compounding and fabrication. Users are keenly interested in how Artificial Intelligence and Machine Learning (ML) can accelerate the notoriously slow material discovery process, specifically focusing on synthesizing novel acrylic monomers or optimizing co-polymer ratios to achieve desired properties like reduced compression set or enhanced chemical resistance without extensive traditional trial-and-error. Furthermore, there is significant concern regarding supply chain volatility, prompting questions about AI-driven predictive analytics for managing raw material inventory (acrylate esters, curing agents) and forecasting demand fluctuations in the automotive OEM sector. The key themes summarized revolve around leveraging AI for operational efficiency, accelerating R&D cycles, and establishing digital twins of component performance to minimize physical testing costs and time-to-market for specialized sealing solutions required by emerging technologies like hydrogen fuel cells and advanced EVs.

The Acrylic Rubber Market is fundamentally shaped by powerful synergistic forces encompassing technological drivers, cost-related restraints, and expanding application opportunities, collectively influencing its growth trajectory. Key drivers include the global automotive industry's relentless pursuit of lightweighting objectives to improve fuel efficiency and extend the range of electric vehicles. Acrylic rubber, offering high thermal stability without the high density associated with alternatives like FKM, is ideal for seals in engine bays, transmission systems, and increasingly, battery packs, where heat management is critical. The rapid adoption of new powertrain technologies, including turbocharged engines operating at higher temperatures and specialized cooling circuits in EVs, mandates the use of materials capable of handling sustained heat exposure and aggressive synthetic fluids, directly bolstering demand for high-performance ACM and AEM grades. Furthermore, global regulatory pressures enforcing stricter emissions standards require more robust and durable sealing components to prevent fluid leaks and maintain engine efficiency over extended periods, making acrylic elastomers a preferred choice for manufacturers aiming for compliance.

However, the market faces significant restraints, primarily stemming from the relatively high cost of acrylic rubber compared to general-purpose elastomers like EPDM or NBR. The synthesis of specialized acrylate monomers and the complex curing mechanisms required for optimal performance contribute to higher production costs, sometimes limiting their adoption in cost-sensitive, large-volume industrial applications. Competition from alternative high-performance elastomers, notably Highly Saturated Nitrile Rubber (HNBR) and Fluoroelastomers (FKM), poses a persistent challenge. While FKM offers superior temperature limits, and HNBR offers better low-temperature performance in many cases, manufacturers must continuously innovate in the acrylic rubber space to justify the cost premium through improved performance parameters, such as lower compression set and better chemical inertia. Supply chain volatility and the fluctuation in prices of crude oil derivatives, which serve as foundational feedstocks for acrylate monomers, introduce economic instability that can restrain market expansion and complicate long-term pricing strategies for compounders.

The market opportunities are substantial and focused heavily on emerging industrial sectors and geographical expansion. A significant opportunity lies in the burgeoning electric vehicle market, where acrylic rubber is critical for sealing battery pack components, charging ports, and specialized thermal coolant circuits due to its excellent dielectric properties and resistance to polar fluids. Beyond automotive, the aerospace and defense sectors offer high-margin opportunities for specialized, certified acrylic elastomers used in fuel systems and hydraulic seals, driven by demand for lightweight, high-reliability materials in high-altitude environments. Moreover, the increasing focus on sustainable practices presents an avenue for growth. Development and commercialization of bio-based or recycled content acrylic elastomers, currently an intensive area of research, would not only differentiate products but also meet the growing corporate demand for sustainable raw materials, providing a crucial competitive edge in the evolving global market landscape.

The segmentation of the Acrylic Rubber Market provides a structured view of consumption patterns, technological preferences, and end-user requirements, essential for strategic market positioning. The market is primarily divided based on Type (ACM, AEM), Application (Gaskets and Seals, Hoses, O-rings), and End-Use Industry (Automotive, Industrial Machinery, Aerospace). The Type segmentation reveals a clear distinction in performance capabilities and market niches; ACM holds the larger volume share, being the traditional choice for high-temperature resistance in standard powertrain applications. Conversely, AEM, offering superior low-temperature performance and improved oil resistance, captures the high-growth, high-specification segment, particularly within modern engine turbo systems and the advanced thermal management systems of electric vehicles, driving its disproportionate value growth within the forecast period. Understanding these nuances allows suppliers to tailor their product offerings, focusing on compounding additives that enhance AEM's properties for specific battery electric vehicle (BEV) requirements, or optimizing ACM processing for cost-effective high-volume sealing solutions.

Application analysis highlights the dominance of Gaskets and Seals, which are universally required across all end-use industries to prevent fluid leakage and maintain pressure integrity. Within automotive applications, the demand for transmission shaft seals and valve cover gaskets represents a core market driver due to the material's specific resistance to hot transmission fluids and engine oils. However, the Hoses segment, encompassing critical air management hoses (like turbocharger hoses) and specialized coolant hoses, is experiencing accelerated growth. As engine operating temperatures climb and hybrid systems become more complex, the material requirements for hoses become more stringent, necessitating high-performance acrylic rubbers that can withstand continuous exposure to heat, aggressive coolants, and oxidative stress without compromising flexibility or structural integrity. This segment is characterized by strong customization requirements, involving intricate designs and specialized compounding to ensure compliance with OEM performance specifications and longevity requirements.

The End-Use Industry segmentation confirms the Automotive sector as the indisputable largest consumer, dictating both volume and innovation direction. The industry's shift towards electric mobility is fundamentally reshaping material demand, requiring specialized acrylic rubbers for unique applications such as battery pack seals designed for fire safety and superior environmental sealing. The Industrial Machinery sector provides a stable, though slower-growing, revenue stream, focusing on seals and vibration dampeners in heavy equipment, compressors, and hydraulic systems where reliability in oily, high-heat environments is paramount. The Aerospace and Defense segment, while representing a smaller volume, is crucial for high-value revenue due to the extremely stringent material qualification processes and the resulting high pricing power for certified acrylic elastomer grades used in aircraft engine seals and fluid conveyance systems, demanding minimal compression set and maximum thermal resistance across extreme operational temperatures, thereby representing the pinnacle of performance requirements in this market.

The value chain for the Acrylic Rubber Market is complex, beginning with the upstream sourcing of foundational petrochemical derivatives and extending through polymerization, compounding, component fabrication, and finally, distribution to the end-user OEMs. Upstream analysis focuses heavily on the supply of acrylate monomers, primarily ethyl acrylate and butyl acrylate, which are derived from petrochemical feedstocks such as ethylene and propylene. Key chemical producers specialize in synthesizing these monomers, and their production capacity and pricing volatility significantly impact the cost structure of the entire chain. Fluctuations in crude oil prices and the global supply-demand dynamics of precursor chemicals directly influence the profitability of acrylic rubber manufacturers. The competitive landscape at this stage is highly specialized, often involving large chemical conglomerates who secure long-term supply contracts with polymerization specialists.

The midstream phase involves the core polymerization process, where specialized rubber manufacturers convert monomers into crude acrylic rubber (ACM or AEM) bales, and the subsequent compounding process. Compounding is a critical step, involving the incorporation of various additives—such as fillers (carbon black, silica), plasticizers, antioxidants, and most crucially, specialized curing agents (amines or metallic soaps)—to achieve the final desired performance characteristics like high tensile strength, low compression set, and improved processing stability. Manufacturers who possess proprietary compounding expertise and advanced polymerization technologies, particularly those capable of controlling co-monomer inclusion to optimize low-temperature flexibility, gain substantial competitive advantage. Following compounding, the product moves to component fabricators who utilize injection molding, extrusion, or compression molding techniques to produce finished parts like gaskets and hoses according to precise OEM specifications.

The downstream segment involves the distribution of these fabricated components to original equipment manufacturers (OEMs), primarily within the automotive sector (Tier 1 suppliers) and large industrial machinery producers. Distribution channels can be broadly categorized into direct and indirect routes. Direct sales are common for highly customized and high-volume automotive parts, where close technical collaboration between the rubber manufacturer/fabricator and the OEM is required for design and quality control. Indirect channels involve authorized distributors and specialized industrial material suppliers who maintain inventory and provide smaller volume, generalized products to the maintenance, repair, and operations (MRO) sector or smaller industrial buyers. The overall efficiency and profitability of the value chain rely heavily on maintaining high quality standards, as failure of a single sealing component in a high-temperature engine environment can lead to significant warranty claims, emphasizing the importance of stringent quality control at every stage from monomer purity to final component inspection.

Potential customers for acrylic rubber are concentrated within industries demanding sealing and dampening solutions that must withstand elevated temperatures, prolonged exposure to aggressive oils, and high levels of operational vibration. The primary consumer base resides within the global automotive manufacturing ecosystem, spanning Original Equipment Manufacturers (OEMs) such as BMW, General Motors, and Toyota, as well as their vast network of Tier 1 and Tier 2 suppliers like Continental, Bosch, and ZF. These automotive entities purchase acrylic rubber components, including shaft seals, O-rings, and specialized hoses, for deployment across critical vehicle systems, specifically engine transmission systems, valve covers, oil pan gaskets, and, increasingly, battery pack thermal management seals in electric vehicles. The procurement decisions in this sector are driven by stringent component life cycle demands, compliance with global environmental regulations, and the need for materials that contribute to enhanced vehicle reliability and reduced maintenance frequency.

Beyond the core automotive sector, key potential customers are found in the heavy industrial and machinery manufacturing domain. This includes companies specializing in hydraulic systems, compressors, pumps, and heavy construction equipment. Manufacturers such as Caterpillar, Komatsu, and various industrial pump producers require acrylic rubber for robust seals and gaskets capable of resisting lubricating and hydraulic fluids across wide temperature fluctuations often encountered in heavy-duty operations. These end-users prioritize materials with low compression set characteristics to ensure long-term sealing effectiveness under constant load and heat. The MRO (Maintenance, Repair, and Overhaul) market also constitutes a steady consumer segment, requiring replacement seals and components for aging industrial infrastructure, often preferring acrylic rubber due to its dependable service history and recognized specifications in legacy equipment.

A high-value, albeit smaller volume, customer segment exists within the aerospace and defense industries. Aircraft manufacturers and specialized component suppliers, including companies like Boeing, Airbus, and their supply chain partners, utilize high-specification acrylic elastomers in areas such as aircraft engine seals, fluid conveyance systems, and vibration isolators. Procurement in this sector is dictated by mandatory certifications, often military or civil aviation standards (e.g., specific AMS standards), requiring materials with exceptional fire resistance, extreme thermal stability, and proven performance reliability under vacuum and high-altitude conditions. These customers are willing to pay a premium for certified, traceable materials, making this segment crucial for manufacturers specializing in advanced, regulatory-compliant acrylic rubber formulations. The diversity of these end-user segments underscores the material's versatility in high-stress thermal and chemical environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.8 Billion |

| Market Forecast in 2033 | $2.68 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Zeon Corporation, DuPont, BASF SE, Wacker Chemie AG, Asahi Kasei Corporation, Shin-Etsu Chemical Co., Ltd., ExxonMobil Corporation, Lanxess AG, Dow Inc., Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd., Kuraray Co., Ltd., Denka Company Limited, Solvay S.A., 3M Company, Hangzhou Zhongce Rubber Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Acrylic Rubber Market is characterized by continuous refinement aimed at addressing the persistent trade-off between high-temperature performance, low-temperature flexibility, and compression set. A key technological focus is the advancement in polymerization techniques, specifically moving towards emulsion and suspension polymerization methods that allow for better control over polymer chain architecture and molecular weight distribution. This control is vital for reducing the material’s glass transition temperature (Tg), thereby improving the low-temperature flexibility of ACM grades, which historically lagged behind competitors like HNBR. The development of advanced co-monomers, such as alkoxy acrylates, is central to improving the thermal stability and oil resistance further, enabling acrylic rubber to withstand the increasingly aggressive synthetic fluids and high operational temperatures found in modern engines and transmissions. Furthermore, the integration of nanocarbons and other high-aspect-ratio fillers through sophisticated mixing technologies is being explored to enhance mechanical strength and reduce abrasion without compromising the elastomer's elasticity.

Another crucial technological frontier involves the optimization of curing systems. Acrylic rubber traditionally relies on amine or metal soap curative systems. However, ongoing research focuses on developing non-staining, faster-curing systems that also yield superior physical properties, particularly low compression set—a critical performance indicator for static seals and gaskets designed for long service life. Ultra-low compression set grades are essential for high-reliability applications, and technological breakthroughs in cross-linking density control are key to achieving this. Suppliers are actively researching novel peroxide cure systems tailored for AEM, offering a robust alternative to standard amine cures, which can sometimes be susceptible to moisture and may cause staining. The goal is to provide fabricators with materials that offer high green strength (uncured strength) for easier processing while delivering exceptional sealing force retention when exposed to continuous heat and stress over thousands of operating hours, a requirement critical for minimizing warranty risk in automotive applications.

In response to the automotive electrification trend, the technology landscape is rapidly evolving to encompass specialized compounds for EV applications. This includes the development of acrylic elastomers with enhanced dielectric strength and flame-retardant properties suitable for battery housing seals and electrical connectors. Focus areas include optimizing formulations to resist volatile organic compounds (VOCs) emitted by adjacent battery components and improving resistance to aggressive coolants used in thermal management systems, which often differ significantly from traditional engine oils. Furthermore, processing technology advancements, particularly in highly automated injection molding and liquid injection molding (LIM) of specialized high-viscosity acrylic rubber compounds, are crucial for producing geometrically complex seals and integrated gaskets with high precision and minimal flash, ensuring zero-defect rates required by safety-critical EV components. This combination of material science and processing technology innovation is instrumental in maintaining acrylic rubber’s competitive position against silicone and FKM in the rapidly evolving high-tech mobility market.

The global Acrylic Rubber Market exhibits highly variable regional dynamics, heavily influenced by local automotive production volume, regulatory standards, and industrial maturity. Asia Pacific (APAC) currently dominates the market in terms of volume consumption, driven by its status as the world's largest manufacturing hub for automobiles and industrial machinery, particularly concentrated in China, Japan, and South Korea. Rapid urbanization, increasing disposable income, and subsequent growth in vehicle ownership in emerging economies like India and Southeast Asia fuel the demand for both standard and high-performance acrylic rubber components in new vehicle manufacturing. Furthermore, substantial foreign direct investment into the region's manufacturing infrastructure means that APAC is not just a consumer but also a critical global supplier of acrylic rubber compounds and finished parts, capitalizing on lower labor and energy costs while gradually improving technological capabilities to meet global quality benchmarks.

North America and Europe represent mature markets characterized by stringent regulatory environments and a strong emphasis on high-specification, premium materials. European demand is intensely focused on high-performance acrylic elastomers (AEM and specialty ACM grades) required to comply with Euro 6 and upcoming Euro 7 emission standards, which mandate exceptional durability and minimal component failure in engine and exhaust systems operating at elevated temperatures. The region is a leader in adopting specialized acrylic rubber for high-value industrial applications, including aerospace components and advanced hydraulic systems, where quality assurance and material traceability are paramount. North America is experiencing a significant pivot in demand driven by the robust growth in electric vehicle production and associated infrastructure. This has created specialized requirements for thermal management seals and vibration dampeners in battery architectures, where acrylic rubber's combination of heat resistance and dielectric properties offers a crucial advantage over many competing elastomers.

Latin America and the Middle East & Africa (MEA) currently hold smaller market shares but offer long-term growth potential. Latin America's market growth is intrinsically linked to the performance of its domestic automotive manufacturing industries, particularly in Brazil and Mexico, which serve as regional production hubs. While cost-sensitivity remains a factor, the adoption of globally standardized engine technologies drives a steady demand for quality acrylic seals. The MEA region, particularly the Gulf Cooperation Council (GCC) countries, is witnessing growth in industrial applications related to petrochemicals and heavy machinery maintenance. Acrylic rubber is valued here for its resistance to petroleum-based fluids and resilience in extremely high ambient temperatures. However, geopolitical instability and reliance on imported finished products often limit the scale and pace of market penetration compared to the technologically advanced markets of North America and Europe, necessitating a localized strategy focused on industrial MRO requirements.

The primary difference lies in their chemical structure and corresponding performance at low temperatures. Acrylate Copolymer Rubber (ACM) offers excellent resistance to high heat and hot oil but has limited low-temperature flexibility. Ethylene Acrylate Rubber (AEM) incorporates ethylene units, significantly improving its low-temperature performance while maintaining superior heat and oil resistance, making AEM suitable for applications requiring a broader operating temperature range, such as modern electric vehicle components.

Acrylic rubber is most commonly used in demanding automotive sealing applications, including transmission seals and gaskets, crankshaft and camshaft seals, valve cover gaskets, and oil pan seals. Its strength is its ability to withstand continuous exposure to hot engine oil, transmission fluids, and high temperatures within confined engine and transmission compartments without hardening or cracking.

EV growth drives specialized demand for acrylic rubber, particularly AEM grades. While traditional engine applications decrease, demand shifts to critical EV components such as seals for battery thermal management systems, coolant circuits, and charging port gaskets, where resistance to specialized coolants, thermal cycling, and superior dielectric properties are required for safety and longevity.

Acrylic rubber offers a significant performance advantage over standard NBR (Nitrile Butadiene Rubber) and EPDM (Ethylene Propylene Diene Monomer) primarily in terms of high-temperature resistance and resistance to hot oil and transmission fluids. While EPDM is excellent for ozone and weather resistance and NBR for general oil resistance, ACM and AEM maintain functional integrity at continuously higher operating temperatures, often exceeding 150°C, a threshold where NBR rapidly degrades.

Key restraints include the relatively higher cost of production compared to commodity elastomers, mainly driven by specialized monomer synthesis and curing agent requirements. Additionally, strong competition from substitute high-performance materials like FKM (Fluoroelastomer), which offers higher maximum service temperatures, and HNBR (Hydrogenated Nitrile Butadiene Rubber), which excels in low-temperature flexibility, challenges market penetration in cost-sensitive segments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.