ID : MRU_ 433017 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

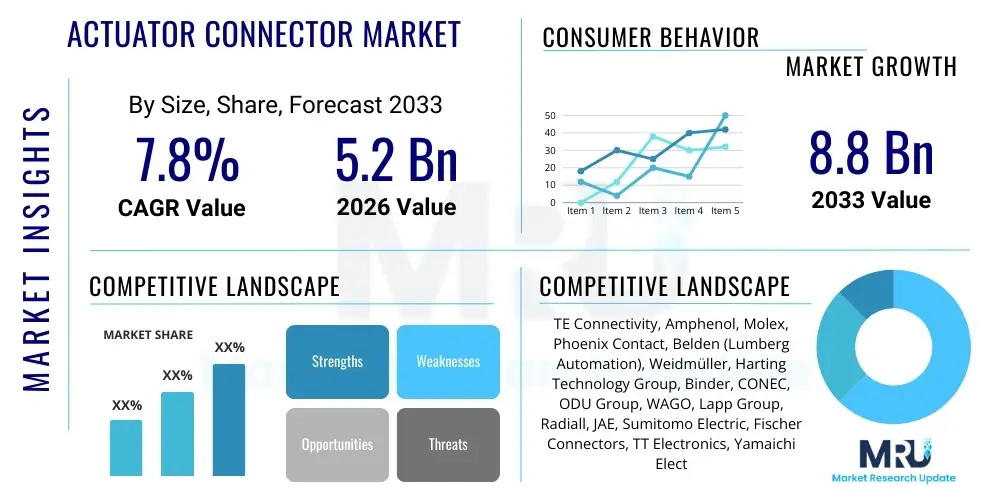

The Actuator Connector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $5.2 Billion in 2026 and is projected to reach $8.8 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by the accelerating global trend of industrial automation, the proliferation of smart factory initiatives (Industry 4.0), and the increasing demand for high-reliability components that can withstand harsh operating environments. Actuator connectors are critical interface elements, enabling seamless communication and power delivery between control systems and field devices, making their adoption intrinsic to modern manufacturing efficiency.

The Actuator Connector Market encompasses specialized electrical and electronic components designed to interface control signals and power supply lines with industrial actuators, such as valves, motor drives, solenoids, and pneumatic systems. These connectors, frequently standardized (e.g., M8, M12, M18 series), provide rugged, secure, and reliable connections necessary for continuous operation in demanding factory automation and process control environments. The core purpose of these products is to minimize downtime, simplify installation, and ensure data integrity across complex industrial networks, often supporting high-speed protocols like IO-Link.

Major applications of actuator connectors span across key industrial sectors, including discrete manufacturing, automotive assembly lines, food and beverage processing, and heavy machinery. Their ability to deliver superior ingress protection (IP ratings), resistance to vibration, and chemical stability makes them indispensable for linking field devices to programmable logic controllers (PLCs) or distributed control systems (DCS). Key benefits derived from their usage include reduced maintenance costs due to enhanced reliability, faster setup times through pre-assembled solutions, and improved system diagnostics enabled by standardized, robust interfaces. The foundational driving factors for this market involve the sustained global push toward efficiency improvements in manufacturing, the increasing density of installed sensors and actuators per machine, and the mandated requirement for safety and performance compliance in automated systems.

The Actuator Connector Market is experiencing dynamic growth driven by pervasive digitalization in the industrial sector. Key business trends include a significant shift towards smart connectors integrated with diagnostic capabilities (enabling predictive maintenance), and the rapid adoption of compact, high-density M12 and M8 connectors tailored for miniature robotics and space-constrained applications. Geographically, Asia Pacific (APAC) dominates the market, propelled by massive investments in manufacturing infrastructure and government mandates promoting automation in economies like China, India, and Southeast Asia. North America and Europe maintain strong growth, characterized by high adoption rates of advanced, highly customized connector solutions required for complex, high-mix manufacturing environments.

Segment trends highlight the dominance of M12 connectors due to their versatility and suitability across various harsh environments. However, M8 connectors are gaining traction, especially in sensor integration and compact actuator applications, reflecting the trend towards miniaturization. From an application standpoint, factory automation remains the largest consumer segment, benefiting from continuous technology upgrades and the shift from traditional hard-wired connections to modular, field-attachable connector systems. Furthermore, the market is characterized by intense competition focused on product innovation, particularly the development of hybrid connectors capable of transmitting both power and data over a single cable, addressing the critical industry need for simplified cabling and reduced system complexity.

User inquiries regarding AI's influence on the Actuator Connector Market frequently revolve around three core themes: whether AI-driven predictive maintenance will necessitate new diagnostic features in connectors, how AI optimization of assembly lines impacts connector form factors, and the role of enhanced data transmission standards required by AI workloads. The primary concern is reliability; as AI systems take over operational control, the integrity of the data stream connecting the actuator (via the connector) to the control system becomes paramount. Users anticipate that AI integration will shift demand away from simple pass-through connectors towards smart, edge-enabled connectors that can monitor their own performance metrics (such as temperature, vibration, and insertion loss) and feed this real-time health data back to centralized AI analytics platforms. This transition mandates superior manufacturing quality and embedded intelligence within the connector system itself, moving the component from a passive interface to an active data source, thereby significantly expanding the market's value proposition and complexity.

The Actuator Connector Market growth is robustly driven by the widespread implementation of Industry 4.0 initiatives across global manufacturing sectors, necessitating seamless connectivity for smart devices and complex machinery. Complementary to this is the continuous technological evolution in automation, including the increasing sophistication and density of industrial robotics, which inherently requires high-reliability, compact actuator interfaces. Conversely, the market faces significant restraints, primarily stemming from the lack of universal global standardization beyond established M-series specifications, leading to complexities in cross-platform integration and inventory management for end-users. Furthermore, the high initial investment required for switching from legacy wiring systems to modern modular connector architectures presents a financial barrier, particularly for small and medium enterprises (SMEs).

Opportunities in this market are vast, centered on the development of hybrid connectors that consolidate power, data, and even pneumatics into a single interface, dramatically reducing cable clutter and simplifying installations. Another critical opportunity lies in leveraging emerging technologies like Single Pair Ethernet (SPE) to create ultra-lightweight, standardized connectors for field-level devices, specifically sensors and lower-power actuators, enabling simpler field wiring harnesses. The primary impact forces shaping the market include competitive pricing pressures from Asian manufacturers, demanding constant innovation from Western suppliers in terms of material science (for better chemical resistance) and design for faster field assembly. The market is also heavily impacted by strict safety regulations and requirements for electromagnetic compatibility (EMC), compelling manufacturers to continuously upgrade insulation materials and shielding effectiveness to maintain market relevance.

The Actuator Connector Market is extensively segmented based on connector type, application, and end-use industry, reflecting the diverse requirements of industrial automation globally. Segmentation by type differentiates between established standards like M8 and M12, which dominate the market due to their ruggedness and wide acceptance, and larger formats like M18 or custom rectangular connectors used for high-power or high-pin-count applications. The rapid advancement of robotics and miniaturization is specifically fueling demand within the M8 segment. Application segmentation highlights factory and process automation as central pillars, where connectivity reliability is critical to operational continuity and efficiency metrics. End-use segmentation clearly divides demand between discrete manufacturing (e.g., automotive, electronics assembly) which relies heavily on high-speed data transfer, and process manufacturing (e.g., oil and gas, pharmaceuticals) which prioritizes resistance to extreme temperatures, corrosion, and pressure.

The value chain for the Actuator Connector Market begins with upstream activities involving raw material suppliers, primarily providing high-grade plastics (for insulation and housing), copper alloys (for contacts), and specialized sealing materials (for environmental protection). Manufacturers rely heavily on consistent sourcing of these materials to ensure connectors meet rigorous industrial standards concerning durability and ingress protection (IP ratings). Key upstream challenges involve managing fluctuating commodity prices and sourcing specialized components that meet stringent flammability and chemical resistance standards required by UL and CE certifications. Material innovation at this stage, particularly in developing lighter, stronger, and more resilient polymer compounds, is crucial for market competitiveness and meeting evolving customer specifications in harsh environments.

Midstream involves the core activities of design, precision molding, automated assembly, and stringent quality control (QC). Connector manufacturers invest heavily in automated assembly lines to manage the high volumes and precision required for producing reliable M8 and M12 components. Direct distribution channels involve large manufacturers selling directly to major OEMs (Original Equipment Manufacturers) in the automation sector, allowing for deep technical collaboration and custom design integration early in the product lifecycle. Indirect distribution relies on a network of specialized industrial distributors and component resellers who provide logistical support, local inventory, and technical expertise to smaller end-users, system integrators, and maintenance professionals. This dual channel approach ensures broad market reach and prompt delivery of standard products.

Downstream activities center on the installation, maintenance, and eventual replacement of connectors within industrial systems. End-users, including plant operators, maintenance engineers, and system integrators, constitute the final point of consumption. The downstream feedback loop is critical, informing manufacturers about failure modes, environmental performance gaps, and demands for new features, such as push-pull locking mechanisms or integrated LED diagnostics. The increasing complexity of industrial networks has empowered system integrators, who act as significant influencers and purchasers, determining which connector brands and technologies are incorporated into large-scale automation projects, thus making them key strategic targets within the value chain.

The primary consumers and end-users of actuator connectors span the entire spectrum of industrial infrastructure where automated movement and control are prerequisites for operation. Key potential customers include large-scale Original Equipment Manufacturers (OEMs) specializing in industrial machinery, such as robot manufacturers, machine tool builders, packaging equipment providers, and textile machinery producers. These customers purchase connectors in high volumes for integration directly into their newly built machines, demanding custom-designed, highly reliable, and standardized solutions that align with their overall equipment design and performance guarantees. The specification of connectors often occurs early in the machine design phase, making early engagement with these OEMs crucial for market leaders.

Another major customer segment consists of system integrators and engineering firms who manage large automation upgrade projects and plant expansions. These professionals require a broad portfolio of standardized, field-attachable connectors and cabling solutions that offer flexibility and ease of installation when retrofitting existing factory infrastructure or deploying new automation cells. Their purchasing decisions are heavily influenced by the availability of connectors supporting multiple protocols (e.g., IO-Link, Industrial Ethernet) and the overall ease of maintenance. Finally, maintenance, repair, and overhaul (MRO) departments in end-user facilities (e.g., automotive plants, food processing facilities, chemical refineries) represent a consistent customer base, purchasing replacement connectors and components to ensure minimal operational downtime, often prioritizing quick availability and interchangeability with existing installed bases.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $5.2 Billion |

| Market Forecast in 2033 | $8.8 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity, Amphenol, Molex, Phoenix Contact, Belden (Lumberg Automation), Weidmüller, Harting Technology Group, Binder, CONEC, ODU Group, WAGO, Lapp Group, Radiall, JAE, Sumitomo Electric, Fischer Connectors, TT Electronics, Yamaichi Electronics, HIROSE Electric, Mencom Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution within the Actuator Connector Market is focused primarily on enhancing performance in three critical areas: data speed, power density, and environmental resilience. A major trend is the widespread adoption of technologies supporting Industrial Ethernet protocols, necessitating connectors that can reliably handle Gigabit speeds while maintaining superior electromagnetic compatibility (EMC) shielding. This push requires manufacturers to utilize advanced contact materials and specialized internal shielding mechanisms to prevent signal degradation in noisy factory environments. The move toward IO-Link capabilities is also a crucial technological advancement, as it transforms simple M12 connectors into intelligent communication hubs capable of bidirectional data transfer and diagnostic functionality, facilitating easier integration into centralized control systems and supporting advanced machine learning applications.

Furthermore, material science plays a pivotal role in the competitive landscape. Connector manufacturers are continually developing advanced housing materials, focusing on polymers and metals that offer exceptional resistance to caustic chemicals, extreme temperatures, UV radiation, and mechanical stress, thereby achieving higher IP ratings (up to IP69K for wash-down environments). Another defining technological advancement is the rise of hybrid connectivity solutions. These innovative designs integrate multiple functionalities—such as high-current power lines, high-speed data pairs, and fiber optic elements—into a single connector housing. This technology significantly reduces the required installation footprint and cabling complexity, proving particularly valuable in modular robotic applications and space-constrained industrial machinery, offering streamlined deployment and maintenance efficiencies that drive down total cost of ownership (TCO).

Beyond physical design, the integration of quick-connect and push-pull locking mechanisms is becoming standard. These technologies eliminate the need for time-consuming screw-locking procedures, drastically reducing installation and maintenance labor time, a critical factor given the ongoing scarcity of skilled labor in industrial maintenance. The long-term technological trajectory points toward smart, self-monitoring connectors capable of reporting wear and tear before failure occurs. This edge intelligence, combined with emerging Single Pair Ethernet (SPE) standards for lower-power field devices, promises to further simplify and standardize industrial wiring architectures, enabling fully interconnected, future-proof automation systems that are easier to manage and scale across varied geographic locations and industrial processes.

The global Actuator Connector Market exhibits distinct growth patterns influenced by regional economic development, automation maturity, and regulatory frameworks. Asia Pacific (APAC) stands out as the most dominant and rapidly growing region, driven by massive public and private investment into manufacturing capacity expansion and digital transformation programs, particularly in China, South Korea, and Japan. North America and Europe, while growing at a slightly slower pace, focus intensely on quality, customization, and high-end technological integration, representing key markets for advanced hybrid and smart connector solutions. Latin America and MEA are emerging markets, primarily driven by investments in resource extraction (Oil & Gas, Mining) and infrastructure projects, demanding extremely rugged and explosion-proof connector types.

The primary function of an actuator connector is to reliably transmit power and control signals between the central control system, such as a PLC or IO-Link master, and the physical actuator device, ensuring seamless operational execution in automated systems. They are designed for high durability and ingress protection (IP) in harsh industrial environments.

The M12 connector standard is the most prevalent in the current market due to its robust design, versatility, ability to support both power and high-speed data transmission (including Industrial Ethernet), and its wide acceptance across various automation applications globally.

Industry 4.0 demands intelligent, network-enabled components. This is driving the demand for smart actuator connectors featuring integrated diagnostics, support for IO-Link protocol, and hybrid designs that simplify field wiring while accommodating higher data throughput required for real-time monitoring and AI applications.

The Asia Pacific (APAC) region, specifically countries like China and India, is currently exhibiting the fastest growth rate in actuator connector adoption, fueled by massive government and private sector investments in factory automation, robotics, and expanded manufacturing capabilities.

Hybrid actuator connectors consolidate multiple functions, such as power, signal, and data (or even pneumatic lines), into a single interface. They offer significant benefits by reducing cable clutter, decreasing installation time and complexity, and lowering the overall material and maintenance costs of automation systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.