ID : MRU_ 439431 | Date : Jan, 2026 | Pages : 248 | Region : Global | Publisher : MRU

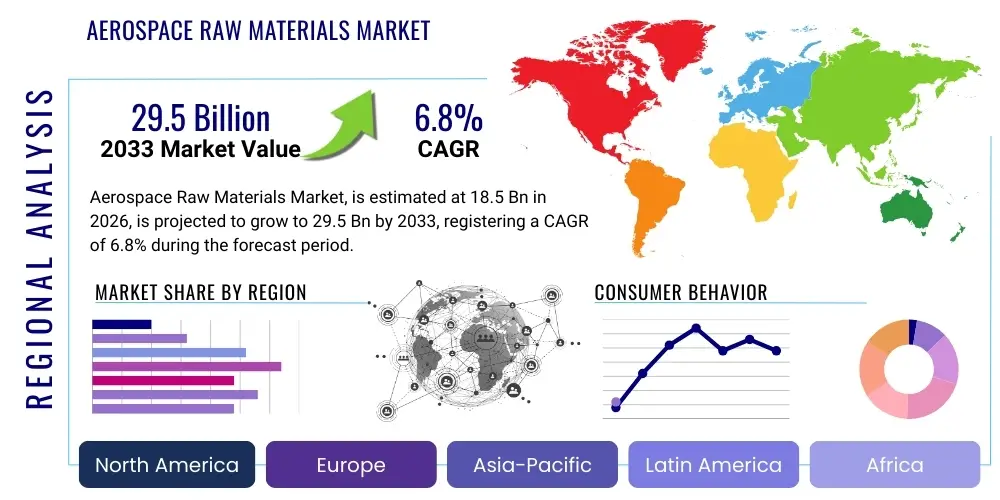

The Aerospace Raw Materials Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 29.5 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by sustained demand from global aircraft manufacturing, driven by commercial fleet expansion and military modernization programs. The increasing adoption of advanced materials like composites and specialized alloys to enhance fuel efficiency and operational performance further contributes to this significant market expansion. Geopolitical considerations and the continuous innovation in material science are also pivotal factors influencing market dynamics and future revenue streams.

The Aerospace Raw Materials Market encompasses a diverse range of high-performance materials essential for the construction, maintenance, and repair of aircraft, spacecraft, and missiles. These materials include, but are not limited to, advanced composites, aluminum alloys, titanium alloys, superalloys, and specialized steels, each selected for their unique properties such as high strength-to-weight ratio, temperature resistance, corrosion resistance, and durability. The market's primary applications span across commercial aviation, military aircraft, space exploration, and maintenance, repair, and overhaul (MRO) activities, supporting a global industry reliant on stringent performance and safety standards.

The benefits derived from these sophisticated raw materials are manifold, including significant reductions in aircraft weight, which directly translates to improved fuel efficiency and lower operating costs for airlines. Furthermore, their enhanced structural integrity and fatigue resistance contribute to longer operational lifespans for aerospace platforms, reducing maintenance requirements and ensuring greater safety. Innovations in material science are continuously pushing boundaries, enabling the development of next-generation aircraft capable of higher speeds, greater payloads, and extended ranges, while also contributing to environmental sustainability through lighter designs and advanced manufacturing processes.

Several critical factors are driving the robust growth of the Aerospace Raw Materials Market. The escalating demand for new commercial aircraft, particularly in emerging economies and for fleet renewals, serves as a primary driver. Concurrent with this is the ongoing modernization of military fleets worldwide, necessitating high-performance materials for advanced combat and transport aircraft. The burgeoning space exploration sector, including both government-led initiatives and private commercial ventures, also represents a significant demand pool. Furthermore, continuous technological advancements in material engineering, focusing on lightweighting, increased resilience, and cost-effectiveness, are pivotal in sustaining market momentum and fostering new applications.

The Aerospace Raw Materials Market is experiencing dynamic business trends characterized by a strong emphasis on supply chain resilience, sustainability, and technological innovation. Key industry players are increasingly investing in research and development to create lighter, stronger, and more environmentally friendly materials, such as advanced thermoplastic composites and additive manufacturing-compatible alloys, to meet the evolving demands of aerospace OEMs. Strategic collaborations, mergers, and acquisitions are prevalent as companies seek to consolidate market share, enhance their material portfolios, and optimize production efficiencies. The market is also navigating challenges related to raw material price volatility, stringent regulatory requirements, and the need for qualified skilled labor in specialized manufacturing processes.

From a regional perspective, North America continues to dominate the aerospace raw materials market, primarily due to the presence of major aircraft manufacturers like Boeing and Lockheed Martin, coupled with substantial defense spending and robust research infrastructure. Europe, home to Airbus and various defense contractors, also holds a significant market share, driven by innovation and strong export markets. However, the Asia Pacific region is rapidly emerging as a high-growth market, propelled by increasing passenger traffic, expanding domestic aircraft production capabilities in countries like China and India, and significant investments in both commercial and military aviation infrastructure. Latin America, the Middle East, and Africa are showing steady growth, supported by fleet expansion and upgrades, though at a comparatively slower pace.

Segment trends within the Aerospace Raw Materials Market reveal a notable shift towards advanced composites due to their superior strength-to-weight characteristics, which are crucial for enhancing fuel efficiency in modern aircraft. While traditional materials like aluminum and titanium alloys remain foundational, their demand is increasingly focused on specialized applications where their specific properties are indispensable. The propulsion systems segment demands high-temperature superalloys, whereas airframe structures are increasingly incorporating hybrid materials. The MRO sector exhibits stable demand for replacement parts and refurbishment materials, ensuring ongoing market stability. Furthermore, additive manufacturing (3D printing) is gaining traction across various segments, enabling complex geometries, reduced waste, and faster prototyping and production of aerospace components.

User inquiries concerning AI's influence on the Aerospace Raw Materials Market frequently revolve around its potential to revolutionize material discovery, optimize manufacturing processes, and enhance supply chain management. Common themes include curiosity about how AI can accelerate the development of novel alloys and composites, concerns regarding the integration challenges and data security, and expectations for increased efficiency, cost reduction, and predictive capabilities in production and maintenance. Users also inquire about AI's role in quality control, defect detection, and ensuring material consistency, recognizing its potential to elevate performance standards and mitigate risks inherent in high-stakes aerospace applications. The overarching sentiment points towards an anticipation of AI as a transformative force, albeit with a recognition of the complexities involved in its widespread adoption.

The Aerospace Raw Materials Market is influenced by a complex interplay of Drivers, Restraints, and Opportunities, collectively forming the impact forces shaping its trajectory. Key drivers include the ever-increasing global demand for new commercial aircraft, propelled by rising air passenger traffic and fleet modernization efforts by major airlines, especially in emerging economies. Additionally, significant defense spending by nations worldwide to upgrade military aircraft and enhance strategic capabilities fuels demand for high-performance materials. Technological advancements in material science, focusing on lightweighting, improved fuel efficiency, and enhanced structural integrity, serve as a continuous impetus for market growth. The burgeoning space industry, encompassing both government and private initiatives for satellite launches and exploration missions, also represents a growing demand segment for specialized raw materials.

Despite robust growth drivers, the market faces several significant restraints. The high research and development costs associated with developing new aerospace-grade materials, coupled with stringent certification processes and regulatory compliance, can be prohibitive for new entrants and slow down innovation cycles. Volatility in raw material prices, particularly for critical metals like titanium and rare earth elements, along with disruptions in global supply chains, poses considerable economic challenges and can impact production schedules. Furthermore, the specialized nature of aerospace manufacturing demands highly skilled labor and advanced infrastructure, which can be a limiting factor in certain regions. Geopolitical instability and trade protectionism can also introduce uncertainties, affecting material sourcing and market access.

Opportunities for growth are abundant within the Aerospace Raw Materials Market. The increasing adoption of advanced manufacturing techniques such as additive manufacturing (3D printing) presents a transformative opportunity, allowing for the production of complex, lightweight components with reduced material waste and shorter lead times. The rising focus on sustainable aviation and environmental concerns is driving demand for eco-friendly and recyclable materials, creating a niche for bio-composites and advanced recyclable alloys. Furthermore, the expansion of the Urban Air Mobility (UAM) and drone sectors is opening new avenues for lightweight, cost-effective, and high-performance materials. Strategic collaborations between material suppliers, component manufacturers, and aerospace OEMs to co-develop next-generation materials and streamline supply chains will also unlock significant market potential. The ongoing quest for enhanced aircraft performance, including higher speeds and greater ranges, continually pushes the boundaries for material innovation.

The Aerospace Raw Materials Market is comprehensively segmented by material type, application, and end-user, offering a granular view of its diverse landscape. This segmentation allows for a detailed analysis of market dynamics, identifying specific growth drivers, challenges, and opportunities within each category. Understanding these segments is crucial for stakeholders to tailor their strategies, product development, and market penetration efforts effectively. The intricate interplay between these segments defines the market's structure and future growth trajectory, reflecting the varied demands across the global aerospace industry.

The value chain for the Aerospace Raw Materials Market is highly intricate, beginning with the extraction and processing of basic raw minerals and extending through various stages of material refinement, component manufacturing, and final integration into aerospace platforms. The upstream segment involves mining, smelting, and initial material processing, where companies extract bauxite for aluminum, iron ore for steel, or specialized ores for titanium and superalloys. This stage is capital-intensive and subject to commodity price fluctuations and geopolitical influences. Specialized chemical companies also play a crucial role in producing resins and fibers necessary for composite materials, requiring advanced chemical engineering expertise.

Midstream activities encompass the transformation of basic raw materials into aerospace-grade forms, such as high-strength aluminum sheets, titanium forgings, superalloy castings, and prepregs for composites. This involves specialized manufacturing processes like rolling, extrusion, forging, heat treatment, and advanced material synthesis, often requiring significant investments in R&D and strict quality control to meet stringent aerospace specifications. Component manufacturers then further process these materials into specific parts, such as airframe structures, engine components, or interior elements. Downstream in the value chain, direct and indirect distribution channels play a pivotal role. Direct channels involve long-term supply agreements between major material producers and aerospace OEMs (e.g., Boeing, Airbus, Lockheed Martin), ensuring a stable supply of critical materials for large-scale production programs.

Indirect channels primarily serve smaller component manufacturers, MRO providers, and specialized niche markets, often through authorized distributors and aggregators who manage inventory and provide logistics support. These distributors are crucial for offering flexibility and responsiveness, particularly for spare parts and specialized orders. The strong emphasis on quality assurance, traceability, and regulatory compliance (such as AS9100 certification) permeates every stage of the value chain, from raw material sourcing to final product delivery. The high-value nature of aerospace components means that even minor disruptions or quality issues at any point can have significant consequences, necessitating robust quality management systems and close collaboration across all tiers of suppliers. This integrated and highly regulated structure ensures the reliability and safety paramount to the aerospace industry.

The primary potential customers and end-users of the Aerospace Raw Materials Market are diverse, yet all operate within the demanding confines of the global aerospace and defense industries. Leading the demand are the major Original Equipment Manufacturers (OEMs) of commercial aircraft, such as Boeing and Airbus, who require vast quantities of high-performance materials for their new aircraft production lines. Similarly, military aircraft manufacturers like Lockheed Martin, Northrop Grumman, and BAE Systems are significant consumers, driving demand for specialized alloys and composites for advanced fighter jets, transport aircraft, and surveillance platforms. These OEMs procure materials directly from producers through established supply agreements, often for multi-year programs, ensuring consistent quality and supply.

Beyond the prime OEMs, the market also serves a broad ecosystem of Tier 1, Tier 2, and Tier 3 suppliers who manufacture specific components and sub-assemblies for aircraft. These suppliers specialize in producing everything from landing gear and engine components to interior elements and avionics structures, each requiring specific material types adapted to their functional demands. For example, engine manufacturers like GE Aviation, Rolls-Royce, and Pratt & Whitney are major consumers of superalloys and advanced ceramics due to the extreme operating temperatures within jet engines. The increasingly complex nature of modern aircraft means that even small component manufacturers contribute significantly to the overall material demand, often sourcing through indirect distribution channels or specialized material processors.

Furthermore, the Maintenance, Repair, and Overhaul (MRO) sector represents a crucial and continuously active customer segment. MRO providers require a steady supply of aerospace raw materials for routine maintenance, structural repairs, and component overhauls throughout the operational lifespan of aircraft fleets. This includes materials for patching, reinforcement, and replacement of fatigued or damaged parts, ensuring continued airworthiness. The burgeoning space exploration and satellite manufacturing industry, including companies like SpaceX, Blue Origin, and various national space agencies, also constitute a growing customer base, demanding ultra-lightweight and radiation-resistant materials for rockets, spacecraft, and satellite components. Lastly, manufacturers of Business Jets and Unmanned Aerial Vehicles (UAVs) contribute to market demand, seeking lightweight and durable materials for their specialized applications, often with a focus on fuel efficiency and extended flight capabilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 29.5 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Toray Industries, Inc., Hexcel Corporation, Solvay S.A., DuPont de Nemours, Inc., Teijin Limited, Alcoa Corporation, Arconic Corporation, VSMPO-AVISMA Corporation, ATI Inc., Carpenter Technology Corporation, RTI International Metals (a subsidiary of Alcoa), Allegheny Technologies Incorporated, Kaiser Aluminum, Constellium SE, NLMK Aerospace, Hitachi Metals, Ltd., Mitsubishi Chemical Corporation, SGL Carbon SE, BASF SE, Cytec Industries (now part of Solvay) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Aerospace Raw Materials Market is characterized by continuous innovation aimed at developing materials that offer superior performance, lighter weight, and improved cost-effectiveness. A prominent technological thrust involves advanced composite manufacturing techniques, including automated fiber placement (AFP) and automated tape laying (ATL), which allow for precise and efficient production of complex composite structures with reduced waste. The development of new resin systems, such as high-temperature thermoplastics and thermosets, is enabling composites to withstand more extreme operational environments and offering greater recyclability. Furthermore, hybrid material technologies, combining the benefits of different material classes (e.g., metal-matrix composites or GLARE), are gaining traction for specific applications requiring a balance of strength, stiffness, and damage tolerance.

Additive manufacturing, commonly known as 3D printing, represents another pivotal technological advancement, revolutionizing the way aerospace components are designed and produced. Techniques like Selective Laser Melting (SLM), Electron Beam Melting (EBM), and Fused Deposition Modeling (FDM) are being increasingly utilized to create complex geometries, optimize part consolidation, and produce near-net-shape components from advanced alloys (e.g., titanium, nickel superalloys) and high-performance polymers. This technology not only reduces material waste and lead times but also enables the fabrication of parts that are structurally lighter and functionally superior. Moreover, advanced surface treatment technologies, such as cold spray, laser peening, and specialized coatings, are critical for enhancing the corrosion resistance, fatigue life, and wear resistance of aerospace raw materials, significantly contributing to the longevity and reliability of aircraft components.

Beyond manufacturing, the integration of digital technologies such as material informatics, computational materials science, and AI-driven predictive modeling is transforming material discovery and qualification processes. These technologies leverage big data and machine learning algorithms to accelerate the identification of new material formulations, predict their performance characteristics, and optimize processing parameters, significantly reducing the traditional trial-and-error approach. Non-destructive testing (NDT) methods, including advanced ultrasonic, eddy current, and X-ray techniques, are continuously evolving to ensure the integrity and quality of raw materials and finished components, which is paramount in the safety-critical aerospace industry. The overarching goal of these technological advancements is to provide materials that meet increasingly stringent performance requirements, support sustainable aviation goals, and enable the next generation of aerospace platforms.

The Aerospace Raw Materials Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033, driven by increasing aircraft demand and technological advancements.

Advanced composites, particularly carbon fiber composites, are rapidly gaining market share due to their superior strength-to-weight ratio and fuel efficiency benefits, though aluminum and titanium alloys remain foundational.

AI significantly impacts material discovery, design optimization, predictive maintenance in manufacturing, enhanced quality control, and supply chain efficiency, accelerating innovation and reducing costs.

Key drivers include rising global demand for commercial and military aircraft, continuous technological advancements in material science, and the expanding space exploration sector.

North America is anticipated to maintain its dominance due to the presence of major aircraft OEMs and significant defense spending, while the Asia Pacific region is expected to exhibit the fastest growth.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.