ID : MRU_ 434853 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

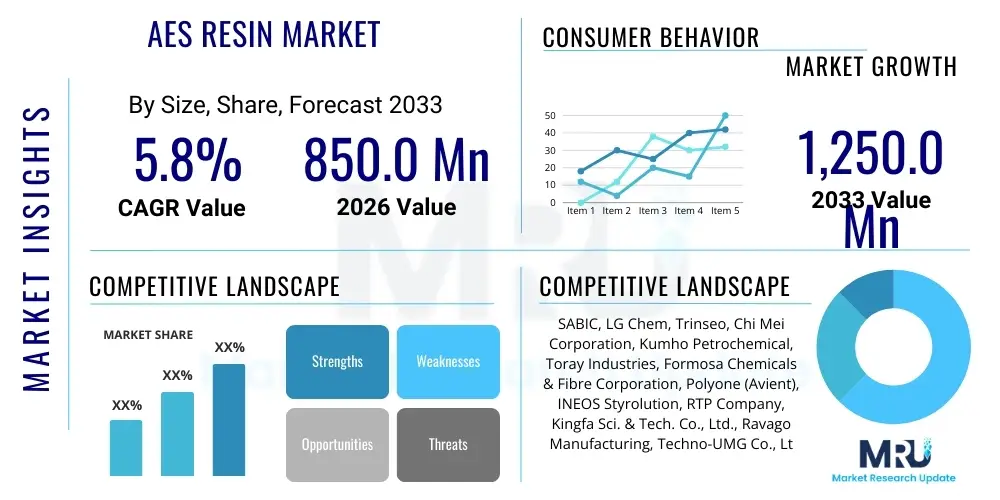

The AES Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 850.0 million in 2026 and is projected to reach USD 1,250.0 million by the end of the forecast period in 2033.

The AES (Acrylonitrile Ethylene Styrene) resin market encompasses the production, distribution, and consumption of high-performance thermoplastic copolymers known for their excellent weatherability, impact resistance, and aesthetic appeal. AES resin is a sophisticated engineering plastic created through the polymerization of styrene and acrylonitrile, enhanced by the incorporation of an ethylene-propylene rubber component. This unique composition grants AES superior ultraviolet (UV) stability compared to conventional plastics like ABS (Acrylonitrile Butadiene Styrene), making it highly suitable for outdoor and high-exposure applications where color stability and structural integrity under sunlight are critical requirements.

The primary applications driving the demand for AES resin include the automotive sector, particularly for exterior components such as grilles, mirror housings, and spoilers, where resistance to environmental degradation is essential. Furthermore, the construction industry utilizes AES in window profiles, siding, and roofing materials. The electrical and electronics sector also employs AES for components requiring durability and good finish, such as external casings and outdoor signage. Its inherent resistance to heat and chemicals, coupled with ease of processing via injection molding and extrusion, positions AES resin as a premium material choice, offering a balanced combination of performance characteristics that justify its higher cost compared to commodity polymers.

Key benefits of utilizing AES resin include long-term color retention, superior resistance to yellowing or chalking when exposed to harsh sunlight, and robust mechanical properties, even at low temperatures. These features are strong driving factors, particularly in geographical regions experiencing high UV radiation levels. The market growth is further propelled by stringent regulatory demands in the automotive industry favoring lightweight materials that contribute to fuel efficiency, alongside increasing consumer expectations for durable, long-lasting exterior products across various consumer goods and infrastructure applications. The shift towards aesthetic longevity and reduced maintenance costs across industrial sectors significantly bolates the adoption rate of AES resin globally.

The AES Resin Market is undergoing consistent expansion, primarily fueled by robust demand from the global automotive manufacturing sector and the rapidly evolving construction industry seeking materials offering both aesthetic durability and performance longevity. Business trends indicate a focus on strategic capacity expansion among major resin producers, particularly those integrated into the supply chains of multinational automotive original equipment manufacturers (OEMs). Furthermore, there is a clear push towards developing specialized grades of AES, including those enhanced for flame retardancy or specific color matching, to cater to niche industrial requirements. Competitive intensity is characterized by differentiation based on product consistency and technical support provided to processors, as supply security and quality assurance are paramount concerns for high-volume end-users.

Regional trends highlight the Asia Pacific (APAC) region as the dominant market driver, attributed to massive infrastructure development projects, burgeoning automotive production bases, and the expansion of the electronics manufacturing hub in countries like China, India, and South Korea. North America and Europe maintain a mature but steadily growing market, driven by replacement cycles in the construction sector and the continued stringent quality standards mandated for premium automotive components. Emerging markets in Latin America and the Middle East and Africa (MEA) are showing increasing adoption, particularly in building materials and consumer durables, as urbanization rates accelerate and disposable incomes rise, leading to higher quality product expectations.

In terms of segment trends, the Injection Molding Grade of AES resin holds the largest market share due to its extensive use in producing complex, high-precision components required by automotive and electronics industries. Concurrently, the Extrusion Grade segment is experiencing rapid growth, driven by its applicability in large profile applications such as outdoor decking, window frames, and specialized piping in the construction domain. The automotive application segment remains the primary revenue generator, but the Electrical & Electronics segment is projected to register the highest growth rate over the forecast period, reflecting the global trend towards durable, weather-resistant outdoor electronic enclosures and smart infrastructure components requiring advanced polymer protection.

User inquiries regarding the impact of Artificial Intelligence (AI) on the AES Resin Market primarily revolve around themes of predictive maintenance in polymerization reactors, optimization of compound formulations, and efficiency improvements in supply chain logistics. Common questions assess how AI-driven simulation tools can accelerate the development cycle for new AES grades, especially concerning UV stability and impact modification. Users express interest in the potential of AI to minimize material wastage during complex manufacturing processes (like injection molding parameters optimization) and to enhance quality control by detecting microscopic defects in finished resin pellets or final parts. The core expectation is that AI will lead to cost reduction, higher material consistency, and faster innovation cycles, addressing the inherent challenges of high production costs and the need for continuous material performance improvement specific to AES resin properties.

The integration of AI and machine learning (ML) models into polymer science is poised to revolutionize the traditionally slow and iterative process of material discovery and optimization. For AES resins, AI algorithms can analyze vast datasets concerning raw material inputs, reactor conditions, and resulting polymer characteristics (such as melt flow index, Izod impact strength, and weathering test results). This data-driven approach allows manufacturers to predict the outcome of various formulation adjustments before expensive pilot plant trials, significantly shortening the time-to-market for specialized or customized AES compounds. This predictive capability directly impacts the competitiveness of manufacturers by ensuring optimal material properties tailored exactly to end-user specifications, particularly critical in sensitive automotive applications.

Furthermore, AI significantly enhances operational efficiency across the AES value chain. In manufacturing, AI-powered systems monitor critical process variables in real-time, enabling immediate adjustments to maintain optimal reaction kinetics, thereby maximizing yield and minimizing off-spec production. In logistics, ML algorithms can forecast demand patterns with greater accuracy, optimizing inventory levels and reducing warehousing costs for raw materials (acrylonitrile, styrene, and rubber). The ability to foresee potential bottlenecks or material shortages through AI analytics ensures a more resilient and responsive supply chain, crucial for industries reliant on consistent material flow, such as large-scale automotive assembly lines.

The AES Resin Market dynamics are shaped by a complex interplay of strong market drivers, inherent industry restraints, and emerging growth opportunities, collectively known as DRO (Drivers, Restraints, Opportunities). The primary driver is the accelerating demand for high-performance, weather-resistant exterior materials, particularly within the automotive sector's push for lightweighting and the increasing longevity requirements for vehicles. Simultaneously, the market faces significant restraints, chiefly high raw material costs stemming from volatile petrochemical prices (styrene and acrylonitrile), which elevates the final cost of AES resin compared to commodity plastics, limiting its adoption in non-premium applications. Opportunities are plentiful, particularly in developing flame-retardant and bio-based AES variants, addressing evolving regulatory landscapes and sustainability mandates globally. These forces are constantly shifting market equilibrium and dictating strategic investment decisions by key players.

Key impact forces further influencing the market include intense competition from alternative, lower-cost polymers like specialized ABS grades or weather-resistant polycarbonate blends, which constantly pressure AES pricing margins. Regulatory requirements, especially those pertaining to material recycling and the presence of certain chemical additives, necessitate continuous R&D investment to ensure compliance. Moreover, the technological complexity involved in maintaining the precise grafting efficiency during the polymerization process acts as a barrier to entry for new manufacturers, concentrating production capabilities among established global chemical conglomerates. The sustained growth of the housing and infrastructure sectors in emerging economies provides a substantial long-term tailwind, particularly for extrusion-grade AES used in durable outdoor building materials.

The balance between high performance (driver) and high cost (restraint) is the central tension defining the AES market. Success hinges on maximizing the perceived value proposition of AES through superior durability and reduced life-cycle maintenance costs for end-users, thereby justifying the initial premium. Market participants must leverage process innovations to mitigate raw material price volatility while strategically positioning their products to capitalize on sustainability trends, such as developing compounds that are easier to recycle or incorporate recycled content. The increasing global focus on climate resilience and protection against harsh environmental factors ensures that the core value proposition of AES—superior weatherability—remains a powerful and enduring driver for market penetration in premium, long-life applications.

The AES Resin Market is comprehensively segmented based on various technical and commercial parameters, allowing for detailed market analysis and strategic planning. The primary segmentation revolves around the physical characteristics or grades of the resin, specifically distinguishing between injection molding and extrusion materials, reflecting their primary processing techniques and end-use applications. Further segmentation based on application highlights the major consuming industries, with Automotive, Electrical & Electronics, and Construction being the most dominant categories, each possessing distinct material requirements regarding impact strength, heat distortion temperature, and UV stability. Geographic segmentation provides critical insights into regional demand disparities, regulatory influences, and local manufacturing trends driving consumption patterns across major global territories, ensuring a granular understanding of the market landscape.

The segmentation by grade is crucial as injection molding grades typically offer higher flow rates and dimensional stability required for intricate parts like automotive interior components and small electronic housings, while extrusion grades emphasize melt strength and processability for continuous profile manufacturing such as pipes, sheets, and siding. Analyzing the market through the lens of end-user application reveals specific growth pockets; for instance, the rapid transition to electric vehicles (EVs) is generating new demand for AES in durable external battery covers and charging station infrastructure. Understanding these segment dynamics is vital for producers to align their production capacity and R&D efforts towards high-growth areas, maintaining a competitive edge through specialization and meeting specific industry standards, particularly in highly regulated sectors like automotive.

The value chain for the AES Resin Market begins with upstream activities involving the procurement and processing of fundamental petrochemical feedstocks: styrene monomer (SM), acrylonitrile monomer (AN), and various rubber components, typically based on ethylene-propylene diene monomer (EPDM) or similar elastomeric materials. The successful production relies heavily on the quality and price stability of these raw materials, which are often subject to global oil and gas price fluctuations. Key upstream players include major integrated oil and chemical companies responsible for cracking and synthesis. The manufacturing step, which involves the complex graft copolymerization process to achieve the necessary UV resistance and mechanical blending, forms the core transformative phase of the value chain, where technological expertise and proprietary process control are paramount.

Moving downstream, the distribution channel for AES resin typically bifurcates into direct sales to large volume industrial consumers, such as Tier 1 automotive suppliers or major construction material manufacturers, and indirect sales facilitated through a network of specialized compounders, distributors, and regional agents. Distributors play a crucial role in providing logistical support, smaller batch sizes, and technical service to mid-sized processors who cannot procure directly from the large global producers. The final stage involves the conversion of AES pellets into finished components by processors via injection molding, extrusion, or thermoforming, serving the ultimate end-users across diverse applications.

Effective value chain management in the AES market requires deep integration between resin manufacturers and downstream compounders to ensure custom formulations meet precise application specifications. Given the premium nature of AES, technical support is a vital component of the value proposition, extending beyond material supply to assist processors in optimizing mold design and processing parameters. The high costs associated with raw material sourcing necessitate sophisticated hedging strategies and long-term contracts upstream, while downstream effectiveness is measured by reliable, timely delivery and the ability to respond rapidly to changing demand from key sectors like automotive and construction, maintaining a resilient and customer-centric distribution network.

The potential customers for AES resin are primarily large-scale industrial buyers and manufacturers who require durable, high-performance thermoplastic materials specifically resistant to weathering, impact, and heat distortion for external components. These customers typically fall within regulated industries where material failure due to environmental exposure is unacceptable, thus prioritizing material quality and longevity over marginal cost savings. The largest cohort of buyers resides in the automotive sector, including Tier 1 suppliers specializing in exterior trim and specialized functional parts, who demand materials certified to withstand harsh road conditions and prolonged UV exposure without significant degradation or color shift, ensuring compliance with strict OEM warranties and aesthetic standards.

A secondary, rapidly growing customer base is found within the construction and infrastructure industry, specifically manufacturers of residential and commercial building components. These buyers utilize AES resin for durable outdoor products such as window lineals, exterior siding, gutters, and various composite decking elements, where the material’s superior color stability prevents the need for frequent painting or maintenance. Furthermore, the electrical and electronics sector represents a significant growth area, with customers seeking AES for robust outdoor electronics enclosures, telecommunication cabinets, and components used in solar energy installations and smart city infrastructure, all of which require reliable protection against environmental elements and vandalism, broadening the resin’s market scope beyond traditional applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850.0 million |

| Market Forecast in 2033 | USD 1,250.0 million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SABIC, LG Chem, Trinseo, Chi Mei Corporation, Kumho Petrochemical, Toray Industries, Formosa Chemicals & Fibre Corporation, Polyone (Avient), INEOS Styrolution, RTP Company, Kingfa Sci. & Tech. Co., Ltd., Ravago Manufacturing, Techno-UMG Co., Ltd., Versalis S.p.A., Entec Polymers, JSR Corporation, Mitsubishi Chemical Corporation, Nippon A&L Inc., Idemitsu Kosan Co., Ltd., Sumitomo Chemical Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology underpinning the AES Resin Market involves advanced polymerization techniques, specifically focusing on graft copolymerization where the styrene-acrylonitrile (SAN) matrix is chemically bonded (grafted) onto an elastomeric backbone, typically an ethylene-propylene rubber (EPR or EPDM). The technological challenge lies in maximizing the grafting efficiency and controlling the particle size and morphology of the rubber phase, as these factors directly dictate the final material properties, including impact strength and, crucially, long-term UV resistance. Manufacturers continually invest in optimizing reactor design and process control systems, such as advanced spectroscopic monitoring and statistical process control, to ensure consistent and high-quality production runs, minimizing batch variation which is critical for demanding applications like exterior automotive finishes.

Recent advancements in the technology landscape focus heavily on compounding and modification technologies aimed at enhancing the inherent benefits of AES while addressing its limitations, primarily cost and processability. This includes the development of highly efficient UV stabilizers and antioxidant packages tailored specifically for AES to further extend its lifespan in extremely harsh climates. Furthermore, specialized compounding techniques are utilized to create flame-retardant (FR) grades necessary for certain electrical and construction applications, often involving the incorporation of non-halogenated flame retardants to meet stringent environmental and safety regulations. The use of twin-screw extruders with specialized screw configurations allows for excellent dispersion of additives and fillers, leading to superior final product homogeneity and performance reliability, a key differentiator in the premium resin market.

The application of digital twin technology and advanced simulation tools is rapidly becoming a standard technological component within leading AES manufacturing facilities. These tools allow producers to model the entire polymerization process, from monomer feed rates to final pellet properties, enabling virtual experimentation and rapid optimization without costly physical trials. This predictive capability extends to modeling the material’s long-term behavior under various environmental stresses, such as accelerated weathering tests, offering precise performance guarantees to end-users. The continuous refinement of processing aids and mold release agents also contributes to the technological maturity, facilitating easier handling and faster cycle times during the injection molding and extrusion processes, ultimately improving the cost-efficiency of using AES resin in high-volume manufacturing settings globally.

The AES Resin Market exhibits diverse growth trajectories across major global regions, heavily influenced by localized manufacturing capacities, regulatory standards, and end-user demands, creating specific opportunities and challenges in each territory.

The primary advantage of AES resin over standard ABS (Acrylonitrile Butadiene Styrene) is its vastly superior weatherability and UV resistance. Unlike ABS, which degrades and yellows quickly when exposed to sunlight due to the presence of butadiene, AES utilizes a saturated rubber component (like EPDM) in its backbone, ensuring excellent long-term color stability and mechanical integrity in outdoor applications without needing protective coatings.

The Automotive industry accounts for the largest share of AES resin consumption globally. AES is extensively used in exterior components such as grilles, mirror housings, spoilers, and decorative trims where high impact resistance, chemical stability, and exceptional resistance to environmental exposure are mandatory for vehicle longevity and aesthetic retention.

The main factors restraining market growth include the high production cost of AES resin, primarily driven by the volatility and elevated pricing of key petrochemical feedstocks like styrene and acrylonitrile. This premium pricing structure limits its adoption in highly cost-sensitive, non-premium applications where cheaper commodity plastics or alternative engineered polymers might be utilized.

Yes, the AES resin market is showing significant growth potential in the construction sector. Its use is expanding in durable outdoor building materials like window profiles, exterior siding, and roofing components, driven by the need for materials that offer excellent aesthetic appeal, weather resistance, and reduced maintenance costs over the structure's lifetime, particularly in regions with harsh climates.

Injection molding grade AES is formulated for higher flow rates (lower viscosity) to facilitate the rapid filling of complex molds for intricate parts, emphasizing dimensional stability. Extrusion grade AES is formulated with higher melt strength and viscosity to maintain profile shape during continuous processing for items like sheets, pipes, and siding, emphasizing processability under continuous shear conditions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.