ID : MRU_ 434607 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

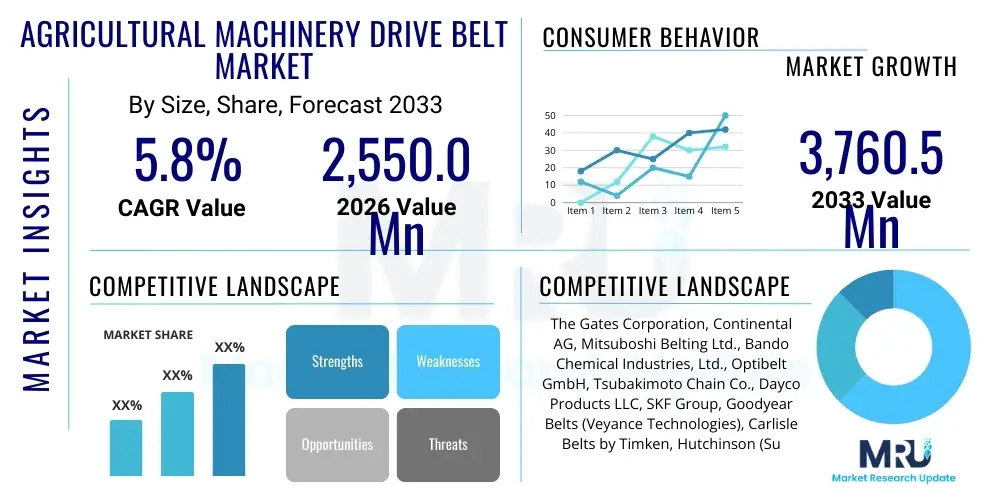

The Agricultural Machinery Drive Belt Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $2,550.0 million in 2026 and is projected to reach $3,760.5 million by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the increasing global demand for high-efficiency farming techniques, necessitating the adoption of advanced, reliable agricultural machinery across both developed and rapidly mechanizing emerging economies. The performance and longevity of these critical machines, which are vital for timely planting, maintenance, and harvesting cycles, rely heavily on robust drive belt systems. These belts must be specifically engineered to withstand profoundly harsh operational environments, characterized by exposure to abrasive dust, corrosive chemical residue, extreme temperature fluctuations (from sub-zero during planting to intense heat during summer harvests), and continuous, heavy shock loads intrinsic to field operations like baling and threshing. Consequently, manufacturers are intensely focusing on developing high-performance belts utilizing advanced materials like specialty EPDM (Ethylene Propylene Diene Monomer) and high-strength aramid fiber reinforcement. These materials are strategically employed in belt construction to minimize slippage under peak torque, maximize power transmission efficiency across complex multi-pulley systems, and significantly reduce overall maintenance downtime, thereby directly supporting the agricultural sector's sustained drive towards greater output per acre and ensuring a predictable, high-growth trajectory for the specialized drive belt industry over the forthcoming decade.

The Agricultural Machinery Drive Belt Market encompasses the entire lifecycle, from the highly specialized manufacturing to the global distribution and ultimate utilization of power transmission components specifically engineered for modern, high-capacity agricultural equipment. This equipment includes, but is not limited to, large four-wheel-drive tractors, technologically advanced self-propelled combine harvesters, precision seed drills, high-density square and round balers, and sophisticated variable-rate sprayers. These specialized agricultural belts, which must operate reliably where standard industrial belts often fail, are critical for efficiently transferring the substantial mechanical power generated by high-horsepower engines. This power must be accurately delivered to various functional units throughout the machine, such as the large rotary mechanisms in threshing systems, the cutting platforms (headers), internal cooling fans, hydraulic pumps, and the complex feed rolls of baling equipment. The core product offering spans traditional V-belts (classical and narrow profiles), high-performance synchronous (timing) belts required for synchronized seeding, flat belts used in specialized conveying applications, and specialized variable speed belts essential for managing dynamic load changes in continuous processing machinery.

The distinctive requirements of the agricultural sector impose stringent demands on belt manufacturers, necessitating products that demonstrate exceptional reliability and resilience far beyond typical industrial benchmarks. Key performance characteristics are non-negotiable and include extremely high tensile strength, necessary to prevent stretching and subsequent slippage under momentary overload; superior resistance to chemical attack from fertilizers, pesticides, and lubricating oils; exceptional flexibility to handle serpentine drives and smaller pulley diameters common in compact, high-efficiency machine designs; and, critically, high resistance to ozone and abrasion caused by airborne particulate matter. The high-quality agricultural drive belt offers intrinsic, quantifiable benefits, including significantly enhanced operational reliability during crucial peak seasons where even minor delays are costly, a substantial reduction in energy consumption achieved through minimized power loss during transmission, and demonstrably extended service intervals, which collectively lower the total cost of machine ownership (TCO) for large-scale farming enterprises. The continuous push for greater machine autonomy and the integration of highly sensitive sensors and precision controls in farming mandate even tighter tolerance requirements and higher reliability standards from all associated mechanical drive components, compelling innovation in belt materials and profile optimization.

Market expansion is structurally supported by several overarching macro-economic factors. Firstly, the escalating need to feed a growing global population drives sustained investment in agricultural productivity enhancement globally, rapidly accelerating mechanization rates across emerging economies in Asia Pacific and Africa. Secondly, substantial governmental subsidies and fiscal policies across North America and Europe, aimed at promoting farm modernization and increasing farming efficiency, directly incentivize the replacement of older equipment with new, belt-intensive advanced machines. Thirdly, the persistent global increase in the cost and scarcity of skilled agricultural labor makes automation and high-capacity mechanization economically imperative, further boosting demand for the reliable components that sustain these systems. Continuous technological improvements in belt manufacturing, such as the utilization of advanced compounding materials that significantly improve heat dissipation and the integration of robust, patented textile reinforcements, further fuel this market expansion by offering verifiable improvements in component longevity and field performance, outweighing the constraints imposed by cyclical agricultural spending and price sensitivity in the smaller farm segments.

The contemporary Agricultural Machinery Drive Belt Market is underpinned by robust business trends focusing heavily on product durability, energy transmission efficiency, and the development of specialized materials capable of enduring the most punishing operational profiles typical of modern agriculture. Leading multinational manufacturers are actively pursuing sophisticated business strategies centered on deepening vertical integration, securing intellectual property around proprietary belt profiles, and forging powerful, long-term supply agreements with Original Equipment Manufacturers (OEMs) of global agricultural machinery. Securing these specifications during the initial design phase of new machinery models is paramount, effectively locking in years of assured supply and establishing barriers to entry for competitors. A key technological trend observed across the industry is the relentless pursuit of ‘maintenance-free’ or significantly extended-life belts, achieved through the development of synthetic rubber compounds (such as high-grade EPDM) paired with advanced high-tensile cords, which successfully extend planned replacement cycles. Although this trend might slightly dampen replacement volume in the immediate aftermarket, it commands substantially higher unit prices and enhances the overall brand reputation for reliability, a critical factor for farmers.

From a geographical perspective, the market exhibits sharp regional divergence in terms of demand characteristics and growth trajectories. The established markets of North America and Western Europe are defined by their mature industrial infrastructure, high regulatory compliance, and high adoption rates of colossal, high-horsepower machinery fleets. Demand here is characterized by a premium focus on specialized, top-tier belt types (often incorporating sensor-ready features) primarily driven by the consistent and necessary replacement cycles for an already substantial and aging equipment installed base. In stark contrast, the Asia Pacific region, specifically encompassing the rapidly modernizing agricultural sectors of India, China, and Southeast Asia, represents the unparalleled epicenter of future growth. This expansion is catalyzed by government mandates promoting mechanization of smaller landholdings and extensive government support for technology upgrades. While this region currently exhibits a substantial demand for cost-effective, generalized belt types for entry-level and mid-range equipment, it simultaneously demonstrates rapidly accelerating, nascent demand for the same high-performance belts required by new combine harvesters and precision planters imported or manufactured locally, indicating a shift in quality requirements.

Segmental dynamics confirm the continued volume leadership of classical V-belts and banded belt systems, due to their universally proven efficacy, cost-effectiveness, and adaptability across a massive range of general-purpose and high-load agricultural applications. However, the synchronous (timing) belt segment is currently registering the fastest revenue growth, directly correlating with the market’s pivot towards sophisticated, computer-integrated planting and harvesting systems where absolute, slip-free timing is non-negotiable for achieving high yield accuracy. Material trends show a definitive preference for EPDM synthetic rubber over traditional materials due to its vastly superior performance metrics related to heat and ozone exposure, thus providing much longer operational lifetimes. The Original Equipment Manufacturer (OEM) channel captures the dominant share of total market revenue, reflecting the high volume of new equipment sales globally and the critical reliance of these manufacturers on proprietary belt designs tailored for peak system performance. Nevertheless, the robust Aftermarket segment, characterized by high replacement rates due to operational wear and tear, remains a highly resilient and strategically critical source of stable, high-margin revenue for global belt manufacturers and specialized independent component suppliers, especially vital in regions where OEM service networks are less ubiquitous or parts logistics are more challenging.

The convergence of Artificial Intelligence (AI) and the Industrial Internet of Things (IIoT) is rapidly transforming user expectations regarding drive belt lifecycle management, moving away from time-based maintenance to highly accurate, condition-based monitoring (CBM). Common user questions center on the tangible application of predictive maintenance analytics: specifically, how advanced machine learning algorithms can ingest and interpret multivariate data streams (e.g., vibration analysis, thermal imaging, acoustic signatures) captured by IoT sensors strategically placed on or near the drive belt system. Users are keenly interested in the methodologies AI employs to establish a robust baseline of 'healthy' operation, how deviations from this baseline translate into accurate forecasts of remaining useful life (RUL), and, fundamentally, the measurable return on investment (ROI) derived from the implementation of these high-tech monitoring solutions in real-world agricultural settings. Furthermore, widespread concern exists regarding the seamless integration of these complex smart belt technologies with the diverse, often legacy, machinery fleets currently operating globally, alongside concerns about the cybersecurity and proprietary nature of the highly valuable operational data generated.

The most immediate and profound impact of AI is evidenced in the revolutionizing of fleet maintenance strategies, particularly for high-capital, high-utilization equipment like powerful combine harvesters and self-propelled forage harvesters. AI algorithms facilitate the sophisticated analysis of voluminous sensor data, enabling the construction of dynamic, predictive digital twins representing the belt's operating environment and instantaneous stress profile. This rigorous, continuous analysis allows fleet managers to receive highly accurate alerts identifying nascent belt degradation, potential tension loss, or impending material failure hours or days ahead of actual catastrophic failure. This capability is invaluable in agricultural contexts where machinery downtime during short, critical periods (like a dry harvest window) translates directly into substantial economic loss due to reduced yield or spoiled crops. By maximizing operational uptime through precise, preemptive component replacement, AI significantly elevates the functional value of the drive belt, repositioning it as a critical data-generating asset within the farm's overall telematics and operational ecosystem, driving demand for technologically integrated components.

Beyond operational maintenance, AI is intrinsically affecting the foundational research and development (R&D) processes utilized by major belt manufacturers. Machine Learning models are now routinely deployed to simulate highly complex stress profiles, thermal load dissipation, and long-term fatigue performance of novel material combinations—including new rubber compounds, different cord materials, and specialized fabric reinforcements—under thousands of simulated, extreme operating cycles, far exceeding the speed and efficiency of traditional physical testing protocols. By rapidly simulating the real-world effects of abrasion, chemical exposure, and varying tension levels, manufacturers can swiftly optimize material selection and geometric design, leading to the creation of inherently more durable and finely tuned drive belts. This data-driven, iterative design loop ensures that the components are not merely optimized for peak power transfer, but also specifically engineered for superior longevity and heightened resistance to the localized, complex environmental challenges faced across diverse farming regions, such as extreme dust generation or high humidity, offering a crucial competitive advantage.

The Agricultural Machinery Drive Belt Market is governed by a dynamic interplay of powerful drivers, significant structural restraints, and clear future opportunities that collectively define its trajectory. The market’s primary momentum is supplied by the pervasive global necessity to increase agricultural output, which mandates sustained investment in increasingly sophisticated and powerful farm mechanization. This is coupled with the critical role of drive belt technology in ensuring the high efficiency and reliability of these expensive assets. However, this growth is structurally constrained by the inherent vulnerability of the agricultural sector to macro-economic volatility, including unpredictable climate patterns that severely impact crop yields and farmer profitability, alongside the acute challenges posed by rapidly fluctuating raw material prices, notably petroleum-derived synthetic polymers, which directly affect manufacturing costs and pricing stability. Opportunities are strongly concentrated in the rapidly developing niche markets for highly specialized belts designed for precision agriculture systems and the perpetually expanding aftermarket sector, particularly for high-durability, extended-life replacement parts needed by the massive and globally dispersed installed machinery base, making technological resilience and proactive risk management essential for market participants.

The primary drivers bolstering market growth are multifaceted and linked to global demographic and technological shifts. Firstly, the continuous advancement in agricultural equipment technology means tractors and harvesters are consistently being equipped with higher horsepower engines, requiring more complex and robust power transmission systems. These systems necessitate superior, modern belts capable of handling exceptionally increased torque loads and operational speeds without premature material degradation. Secondly, the accelerating global trend towards consolidated, large-scale commercial farming operations—particularly dominant in North America, South America, and large parts of Australia—demands components with maximum reliability to ensure non-stop operations during time-sensitive planting and harvesting windows. Any machine failure during these periods carries substantial financial penalties, driving demand for premium, high-specification belts. Furthermore, growing regulatory pressure worldwide focused on enhancing environmental sustainability and fuel efficiency in farming favors the adoption of advanced, low-friction belt designs that minimize parasitic power loss, directly contributing to reduced energy consumption and operational costs for the end-user.

Despite these growth drivers, the market faces significant and persistent restraints. Paramount among these is the fierce, often margin-compressing, competition originating from large-volume, low-cost manufacturers, predominantly those based in certain Asian economies. These companies frequently offer price-competitive products that appeal strongly to small and medium-sized farmers and certain segments of the independent aftermarket, often undercutting the specialized products offered by multinational market leaders, even if at the expense of long-term durability. Moreover, the inherent volatility and price unpredictability of key raw materials—including specialized rubber polymers, petrochemical-based inputs, and high-tenacity textile cords—pose a continuous challenge, forcing manufacturers to deploy sophisticated, resource-intensive procurement and hedging strategies to maintain stable pricing structures. A further restraint is the cyclical nature of agricultural machinery investment, which is profoundly influenced by global commodity markets, farmer income levels, and the availability of agricultural credit and government support, introducing inherent unpredictability into forecasting new equipment sales and associated OEM belt demand. The high quality and extended lifespan of modern belts, while a benefit to the farmer, ironically acts as a restraint on replacement volume in the immediate aftermarket, necessitating continuous product innovation to command higher unit pricing.

The comprehensive segmentation analysis of the Agricultural Machinery Drive Belt Market offers manufacturers and strategists a detailed, granular roadmap of demand distribution across critical product characteristics, material science, specific machine applications, and channel structures, enabling the precise calibration of production and commercial strategies. Product segmentation clearly indicates the foundational role of traditional V-belts, particularly in their banded configuration, which still commands the dominant volume share. This segment serves as the indispensable workhorse across the spectrum of agricultural applications due to its cost efficiency, robust reliability, and proven traction capabilities. However, strategic focus and higher revenue growth rates are increasingly directed towards the synchronous (timing) belt segment. This growth is a direct consequence of the agricultural industry’s pivot towards high-precision operations, where synchronous belts are essential for ensuring the non-slip, perfectly timed transfer of motion required by sophisticated computer-controlled planting mechanisms, fertilizer dispensers, and variable-rate spreading equipment, critical for optimizing farm inputs and maximizing yield per unit area with sub-centimeter accuracy.

A deep dive into material analysis reveals a decisive, secular trend favoring high-performance synthetic elastomers and specialized reinforcement materials. Ethylene Propylene Diene Monomer (EPDM) rubber has emerged as the industry standard-bearer, rapidly displacing older formulations like neoprene and natural rubber due to its vastly superior inherent resistance to extreme thermal cycling, ozone exposure, corrosive agents (such as liquid ammonia fertilizer residues), and UV degradation. This superior resilience is a crucial performance differentiator given that modern farm machinery operates continuously under intense solar radiation and high ambient temperatures. Furthermore, the selection of the tensile cord is paramount: the utilization of advanced cordage materials, including para-aramid (such as Kevlar) and high-strength fiberglass, is growing significantly, as these materials drastically enhance the belt's ability to resist dynamic stretch, significantly increasing its load-carrying capacity and thus ensuring minimal slack and maximum stability for sustained power transmission required by today’s 600+ horsepower tractors and mega-sized combine harvesters.

Application segmentation confirms that tractors, owing to their universal presence and use in primary power take-off (PTO) functions, continue to generate the largest total volume demand for drive belts across all profiles. This is followed closely by the highly complex machinery of combine harvesters, which utilize a dense array of specialized, often custom-profiled, drive belts for powering the header, feeding, threshing, separation, and cleaning mechanisms, where belt failure can halt a high-value, time-critical operation. The third major application cluster involves ancillary and implement machinery, including massive square balers, sophisticated mowers, and precision tillage equipment, all showing robust growth correlated with farm modernization investments. Finally, the distribution channel analysis emphatically highlights the commercial dominance of the Original Equipment Manufacturer (OEM) channel in terms of revenue value, achieved through exclusive, high-volume, multi-year supply contracts. Yet, the Aftermarket channel remains indispensable: it is characterized by stable, resilient replacement demand, providing essential access to parts through a global network of independent distributors, OEM dealerships, and local service providers, ensuring that agricultural operations can swiftly return to productivity following inevitable component wear and failure.

The operational efficiency of the Agricultural Machinery Drive Belt Market value chain is critically dependent on seamless coordination across highly specialized stages, beginning with the highly concentrated upstream supplier base. This foundational segment is responsible for the meticulous sourcing and processing of crucial raw materials, which include specialized synthetic elastomers (such as high-grade EPDM and HNBR, High-Nitril Butadiene Rubber), various high-performance processing chemicals, and, most importantly, the high-tenacity tensile cords, often made of aramid, polyester, or fiberglass. Due to the requirement for specific performance characteristics, the supply of these specialized polymers and reinforcing textiles is typically controlled by a limited number of global chemical and textile giants, granting them considerable leverage in both pricing and supply allocation. Belt manufacturers at the core of the chain then engage in capital-intensive processes: sophisticated compound formulation, precise extrusion of the rubber base, specialized molding (often utilizing heat and high pressure), and the complex vulcanization process, which locks in the belt’s final geometry and mechanical properties. Rigorous quality assurance is integrated at this stage, as any deviation in material mixture or profile geometry directly translates into measurable performance loss or premature component failure in the field, making technological precision a core competitive differentiator.

The midstream stage is dominated by the core belt manufacturing firms, which are segmented into large diversified power transmission conglomerates and highly specialized, niche belt producers. The paramount focus at this stage is on design optimization and customization, requiring close engineering collaboration with major OEMs to meet specific, often proprietary, machinery requirements regarding belt length, profile geometry, and load tolerance specifications. Value addition here is heavily reliant on intellectual property, with companies investing substantially in patented belt profiles (e.g., specialized cog designs) and proprietary material compounds that offer verifiable performance enhancements, such as superior heat aging resistance or increased resistance to environmental contaminants. The final products from the midstream are then strategically channeled through two distinct supply pathways: direct shipment to major OEM assembly lines globally, a process demanding rigorous adherence to just-in-time (JIT) delivery schedules and exceptional logistical precision, and indirect shipment to the vast global aftermarket for replacement purposes, which requires a flexible and comprehensive inventory management system to cover thousands of SKUs (Stock Keeping Units).

The downstream sector is defined by the complex, multi-tiered distribution network responsible for ensuring that replacement parts reach the end-user (the farmer) quickly and reliably, thereby minimizing costly machine downtime. The indirect distribution channel is the most expansive, leveraging a dense network comprising large national and international wholesale distributors, regional warehousing facilities, and thousands of local authorized equipment dealerships, alongside independent industrial parts retailers. This extensive localized footprint is essential for providing rapid access to replacement belts across remote farming regions globally. Direct distribution, conversely, primarily serves high-volume transactions, such as supplying belts directly to large corporate farming operations managing massive fleets or servicing specialized government agricultural procurement programs. The ultimate consumers—the farmers and large farm corporations—judge the entire chain based on component longevity, ease of replacement, and the speed of part availability. The increasing efficiency and reliability of both the direct and indirect channels are crucial for maintaining end-user confidence and securing repeat replacement business, ensuring the high-margin aftermarket segment continues to flourish and remain structurally relevant within the overall market ecosystem.

The primary potential customers and buyers in the Agricultural Machinery Drive Belt Market are categorized into two main groups: the Original Equipment Manufacturers (OEMs) and the expansive Aftermarket segment, consisting predominantly of professional farming operations and service providers. OEMs, such as John Deere, CNH Industrial, AGCO Corporation, and Kubota, represent the highest volume buyers in terms of initial procurement, as they require customized, high-specification belts integrated into every piece of new machinery they produce. These customers prioritize technical excellence, supply chain reliability, and long-term partnership agreements that ensure stable component availability and competitive unit pricing over multi-year cycles, often demanding belts that are optimized specifically for their proprietary transmission systems. OEM purchasing priorities are centered on technical excellence, robust quality control systems (including zero-defect tolerance), competitive bulk pricing, and demonstrable supply chain resilience to ensure that production assembly lines never face component shortages, thereby fostering deep, strategic, and often exclusive partnership arrangements with selected belt manufacturers.

The second major group, the end-users, comprises large-scale commercial farming operations (corporate farms, farming cooperatives), independent small and medium-sized farmers, and agricultural service contractors who own and operate vast fleets of machinery. These customers drive the stable, high-margin aftermarket demand for replacement belts. Their purchasing decisions are primarily influenced by product durability, immediate availability of parts (especially during planting/harvesting seasons), and overall value (cost vs. expected lifespan). Due to the economic penalties associated with machinery downtime, these end-users increasingly prefer high-quality, branded replacement belts that promise reduced failure rates, often sourced through their local authorized equipment dealer or specialized industrial suppliers, emphasizing quick fulfillment and trusted reliability over the lowest possible cost. These consumers consistently favor premium, well-known brand names that guarantee reduced failure rates, typically sourcing components through their local authorized equipment dealer networks or specialized agricultural parts wholesalers, emphasizing swift fulfillment and reliable product guarantees.

Additionally, independent repair workshops and parts distributors constitute an important intermediary customer base within the aftermarket segment. These entities act as key purchasing agents, servicing numerous small farmers who may not maintain direct relationships with OEM dealers. They require a broad inventory of standard and sp

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $2,550.0 million |

| Market Forecast in 2033 | $3,760.5 million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | The Gates Corporation, Continental AG, Mitsuboshi Belting Ltd., Bando Chemical Industries, Ltd., Optibelt GmbH, Tsubakimoto Chain Co., Dayco Products LLC, SKF Group, Goodyear Belts (Veyance Technologies), Carlisle Belts by Timken, Hutchinson (Subsidiary of Total), Colmant Coated Fabrics, Rubena a.s., Fenner Precision Polymers, PIX Transmissions Ltd., Forbo Siegling, Lovejoy Inc., Sanlux Group, Zhejiang Powerbelt Co., Ltd., Wuxi Riyi Electrical Appliance Co., Ltd., Dongil Rubber Belt (DRB), Megadyne Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology landscape driving innovation in the agricultural machinery drive belt sector is rigorously focused on advanced material science, precision engineering for complex geometries, and the burgeoning integration of digital monitoring capabilities, all aimed at achieving maximized durability and minimized power loss. A principal technological leap involves the continuous refinement and widespread commercial deployment of Ethylene Propylene Diene Monomer (EPDM) compounds, which offer transformative resistance to the harsh chemical, thermal, and ozone exposure inherent in farming environments compared to legacy materials like neoprene. EPDM formulations now incorporate specialized additives and curing agents to further enhance their anti-cracking and heat-aging properties, substantially extending the reliable operational life of the belt, a crucial factor when machinery often runs for hundreds of continuous hours during harvesting. Furthermore, strategic material choice for the tensile member is critical: the adoption of ultra-high-modulus tensile cords, particularly those utilizing aramid fibers (known for their exceptional strength-to-weight ratio and minimal stretch characteristics), ensures precise pitch control and minimizes slippage under high-torque dynamic loads, directly supporting the rigorous demands of contemporary, high-horsepower agricultural equipment.

Structural technology enhancements center on perfecting belt geometry and profile design to boost efficiency and reliability across varied operational speeds and pulley configurations. For V-belts, the key innovation is the precision-molded cog profile. Cogs significantly increase the belt’s flexibility, allowing it to efficiently traverse small-diameter pulleys without generating excessive internal heat or compromising tensile strength, thereby improving energy efficiency and extending service life, especially vital in serpentine drive systems common in high-capacity equipment. In the synchronous belt category, technological advancements focus on the development of specialized curvilinear and parabolic tooth profiles. These advanced profiles are meticulously engineered to minimize backlash and ensure absolute, positive engagement with the pulley grooves, which is essential for maintaining the sub-millisecond synchronization required by advanced precision planting and harvesting control systems. These intricate design specifications demand sophisticated, highly automated manufacturing processes that maintain micron-level dimensional stability, guaranteeing superior dynamic balance and high-speed operational stability.

The most forward-looking technology trend is the integration of Industrial Internet of Things (IIoT) principles, leading to the emergence of 'Smart Belts' and condition-based monitoring (CBM) systems. Although still in the early adoption phase, this technology involves embedding miniature, non-intrusive sensors (such as passive RFID tags for identification, or active micro-acoustic emission monitors and thermal sensors) directly within the belt structure or mounting them adjacent to the pulley system. These sensors generate continuous, real-time data streams concerning the belt’s actual operational condition—including temperature, vibration spectral analysis, and instantaneous tension loss—transmitting this data wirelessly to the machine’s telematics unit for AI-driven analysis. This technological convergence shifts the entire maintenance paradigm from relying on scheduled replacement to executing precise, predictive intervention, drastically reducing the risk of catastrophic field failure. This digital integration elevates the drive belt from a simple mechanical consumable to a valuable, data-generating asset essential for modern fleet management and operational optimization in the technologically advanced farm of the future.

Market growth is predominantly driven by increasing global demand for high efficiency in agricultural output and essential food security, leading to higher rates of farm mechanization, particularly in rapidly developing nations. This growth is amplified by continuous technological advancements in belt materials (such as superior EPDM compounds and high-strength aramid fibers) which substantially extend component lifespan and enhance machinery power transmission efficiency.

Precision agriculture requires absolute operational accuracy. This necessity significantly boosts the demand for specialized, high-performance synchronous (timing) belts, as these components ensure the precise, non-slip synchronization essential for computer-controlled planting and variable-rate application equipment, minimizing costly input waste and maximizing crop yield per hectare.

The Original Equipment Manufacturer (OEM) channel secures the largest overall revenue value share, based on high-volume initial procurement contracts for new machine builds. However, the robust Aftermarket segment provides the most structurally stable and continuous source of revenue due to the mandatory cyclical replacement of worn-out belts across the massive and globally aging installed fleet of farming equipment.

The dominant material trend involves the widespread adoption of high-performance synthetic rubbers, chiefly Ethylene Propylene Diene Monomer (EPDM), due to its exceptional resistance to heat, ozone, UV, and static charge buildup. This is coupled with the critical integration of high-modulus tensile cords, such as aramid and fiberglass, essential for handling the high torque and minimal stretch requirements of modern, powerful agricultural machinery.

AI is increasingly vital for enabling advanced predictive maintenance strategies. By analyzing real-time data from embedded sensors (known as smart belts), AI algorithms accurately forecast component degradation and optimize replacement schedules proactively, significantly reducing the probability of unplanned, catastrophic machinery downtime during critical farming operations, thereby improving overall operational throughput.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.