ID : MRU_ 431799 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

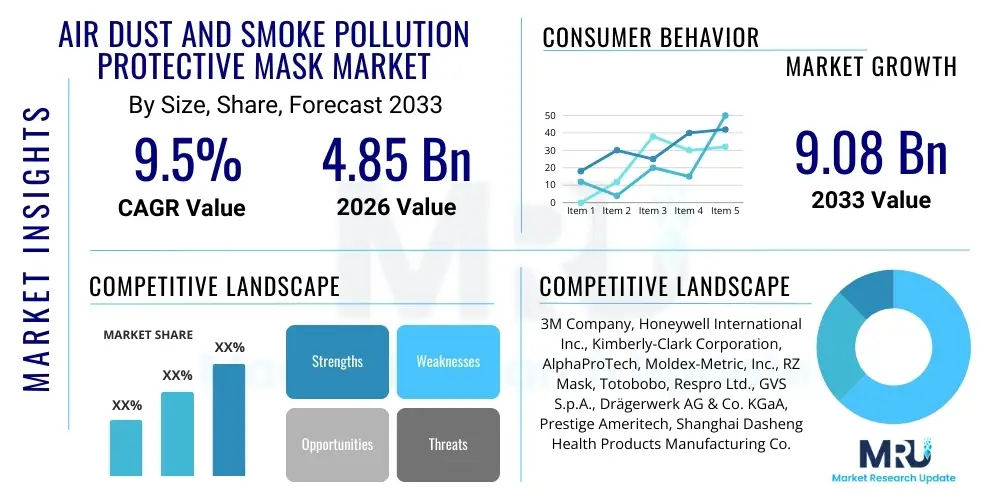

The Air Dust and Smoke Pollution Protective Mask Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 4.85 Billion in 2026 and is projected to reach USD 9.08 Billion by the end of the forecast period in 2033.

The robust growth trajectory of the market is primarily attributable to the escalating severity of air pollution globally, driven by rapid industrialization, urbanization, and the increasing frequency and intensity of natural disasters like wildfires and dust storms. Governmental mandates regarding workplace safety and the implementation of stringent environmental protection acts in highly polluted regions, particularly across Asia Pacific, Europe, and parts of North America, are instrumental in driving the demand for certified protective masks. Furthermore, heightened public awareness concerning the long-term respiratory health risks associated with particulate matter (PM2.5 and PM10) exposure is encouraging prophylactic usage among the general population, shifting masks from primarily industrial tools to essential consumer safety products. This preventive health approach, coupled with sustained media coverage of air quality issues, has solidified the protective mask as a non-negotiable personal item in many densely populated, heavily polluted urban centers worldwide, ensuring stable baseline demand independent of immediate emergency situations. The expansion of regulatory scopes to include finer particulate standards also necessitates the adoption of higher-efficiency respirators, thereby increasing the average selling price and overall market valuation over the forecast period.

Technological innovation plays a crucial role in market expansion, with manufacturers focusing intently on developing masks that offer superior filtration efficiency, improved breathability, and enhanced user comfort, addressing long-standing issues of user compliance in both industrial and general consumer settings. The integration of advanced materials, such as sophisticated nanofiber filters, electrostatically charged media, and activated carbon layers, allows masks to effectively filter ultra-fine particulates, smoke residue, noxious gases, and volatile organic compounds (VOCs). Beyond basic filtration, the market is seeing differentiation through ergonomic design, focusing on creating better seal integrity across diverse face shapes and sizes, crucial for maximizing protection in occupational environments. The sustained normalization of mask usage, initially propelled by the profound impact of the COVID-19 pandemic on global behavioral norms, has fundamentally altered consumer perceptions, establishing protective masks as a standard component of personal protective equipment (PPE) in urban environments, contributing significantly to the sustained market valuation projected for 2033. This cultural shift creates a robust platform for long-term growth, moving beyond emergency use to routine, precautionary health maintenance.

The Air Dust and Smoke Pollution Protective Mask Market encompasses the manufacturing, distribution, and sale of specialized respiratory protective devices meticulously engineered to filter out airborne contaminants. These contaminants include fine particulate matter (PM2.5 and PM10), various forms of industrial dust, photochemical smog, vehicle exhaust emissions, and the toxic smoke generated from combustion sources such as agricultural burning and catastrophic wildfires. The product spectrum spans a wide array of devices, ranging from affordable, single-use disposable filtering facepiece respirators (such as N95, KN95, and the FFP series) to highly durable, reusable elastomeric respirators, including Powered Air-Purifying Respirators (PAPRs). All products are rigorously tested and certified against specific, globally recognized safety standards established by leading regulatory bodies like the National Institute for Occupational Safety and Health (NIOSH) in the U.S., the European Committee for Standardization (EN), and the Standardization Administration of China (GB). The foundational mission of these products is to provide an essential barrier, safeguarding the respiratory system of the wearer from inhaling hazardous microscopic particles that are proven precursors to a wide spectrum of acute and chronic respiratory illnesses, cardiovascular complications, and other systemic health issues, thereby proactively mitigating the substantial burden of pollution-related health crises on global public health infrastructure.

The market caters to an increasingly diverse array of application sectors, significantly expanding beyond its traditional base in industrial environments (such as construction, mining, heavy manufacturing, and petrochemical operations) to encompass the healthcare sector, particularly for protecting clinicians during high-risk procedures or against severe ambient pollution, and, most importantly, the vastly expanding segment of personal consumer use in high-pollution urban and wildfire-affected zones. Major functional applications include ensuring mandatory worker protection against occupational hazards like carcinogenic silica dust, welding fumes, and metal particulates, providing critical safety during extreme environmental exposure events (e.g., severe smog alerts or volcanic ash falls), and offering foundational protection during complex disaster relief and environmental remediation operations involving significant smoke and dust inhalation risks. Key benefits driving sustained market adoption are the scientifically validated superior filtration efficiency of certified products, strict compliance with evolving national and international occupational health and safety regulations, the demonstrated effect on reducing employee sick days linked to airborne pathogen transmission and particulate irritation, and offering profound psychological assurance to consumers navigating environments plagued by persistent and visible pollution challenges, culminating in an overall enhancement of general health and perceived quality of life.

Key driving factors propelling this sophisticated sector include the rapid and stringent enforcement of occupational safety regulations worldwide, particularly targeting exposures related to crystalline silica, asbestos, and combustible dusts in major industrial economies; the alarming, exponential increase in the annual global incidence and geographical reach of devastating wildfire events, which generate acute, massive-scale demand surges often necessitating strategic governmental intervention; and persistent, severe environmental degradation associated with unchecked rapid industrialization in key emerging economies. Furthermore, continuous product innovation, concentrating on the development of highly advanced ergonomic features and the integration of ‘smart mask’ functionalities (such as built-in air quality monitoring sensors, filter life indicators, and advanced fit checks) continues to redefine the market, attracting affluent and tech-aware consumer segments. The market dynamics are intricately linked to seasonal pollution cycles, major shifts in geopolitical manufacturing capacity, and continuous technological refinements aimed not just at maximizing filtration protection, but simultaneously minimizing breathing resistance and enhancing overall user comfort to ensure high compliance rates.

The Air Dust and Smoke Pollution Protective Mask Market is strategically positioned for dynamic and accelerated expansion, defined by a critical evolution from being exclusively perceived as an industrial safety necessity to its current status as a widely accepted, routine consumer health product. This paradigm shift is fundamentally fueled by the synergistic forces of acutely deteriorating global air quality, persistent awareness campaigns regarding airborne health risks, and the enduring behavioral normalization of mask-wearing stemming from recent global health crises. Business trends indicate a high degree of supply chain consolidation, characterized by aggressive strategic mergers and acquisitions executed by established industry leaders aimed at securing robust raw material supply lines, integrating specialized material science expertise (especially in nanofiber technology), and expanding global regulatory compliance footprints. Manufacturers are increasingly prioritizing environmentally sustainable practices, dedicating significant R&D investment towards exploring fully biodegradable mask components, recyclable packaging, and developing highly durable, long-life reusable respiratory systems to counteract the immense environmental burden generated by disposable PPE waste. Concurrently, the proliferation and enhanced sophistication of digital distribution channels, particularly major e-commerce platforms, have drastically improved market accessibility, enabling certified masks to reach remote industrial sites and individual consumers swiftly, establishing intense competitive dynamics among regional and international vendors.

From a regional perspective, the Asia Pacific (APAC) region continues its dominance, functioning as both the largest production base and the most significant consumption market globally. This unparalleled growth in APAC is underpinned by staggering industrial expansion, unprecedented urban population density, and critically high ambient pollution indices in economic giants such as China, India, and Vietnam, where governmental and municipal bodies are now rapidly strengthening and enforcing environmental pollution control and occupational safety regulations, translating directly into mandatory mask procurement. North America and Europe, while inherently mature and saturated in comparison to APAC, demonstrate robust value-based growth spurred by sophisticated regulatory environments and high disposable income, driving demand for premium, high-specification products (e.g., P100 and FFP3). Crucially, the increasing frequency and widespread impact of devastating seasonal environmental phenomena, such as the extensive North American wildfire seasons, necessitate systematic stockpiling and large-scale public distribution of high-grade filtering facepiece respirators, ensuring sustained market vibrancy in these regions.

Segmentation analysis clearly highlights a prevailing trend of high-volume adoption in the filtering facepiece respirator (FFR) segment, specifically the N95/FFP2 classes, valued for their optimal balance between regulatory compliance, high filtration efficiency, and manufacturing cost-effectiveness. However, the reusable/elastomeric respirator segment is simultaneously experiencing rapid valuation growth, primarily in highly controlled industrial and hazardous environments where superior sealing, durability, and a lower total cost of ownership over time are essential requirements. This growth is also bolstered by sustainability-conscious institutional buyers. The application segmentation vividly illustrates the seismic shift in market focus: the personal protective use category, encompassing anti-smog and wildfire protection, now commands explosive volume growth, surpassing the traditional, but stable, industrial segments like construction and general manufacturing. This evolution confirms the market's transition towards a broad consumer safety model, where air quality protection is increasingly being integrated into daily health maintenance routines rather than reserved solely for acute emergency or occupational exposure scenarios.

User inquiries regarding Artificial Intelligence (AI) in the protective mask sector predominantly concentrate on AI’s capabilities in predictive supply chain management, ensuring resilience against unexpected global crises like environmental disasters or pandemics, thereby avoiding critical mask shortages. A central theme is the expectation that AI should leverage deep learning models to analyze complex, real-time datasets—including hyper-localized air quality index (AQI) readings, meteorological forecasts, epidemiological data, and regional industrial activity trends—to accurately forecast localized demand spikes weeks or months in advance. Users also frequently query the application of AI in accelerating the R&D cycle, specifically utilizing machine learning to simulate and optimize the molecular structure and performance of next-generation filtration media (e.g., assessing the efficiency of new nanofiber composites against specific particulate mixtures in smoke). Furthermore, there is a strong consumer-driven expectation for ‘smart mask’ integration, where embedded AI provides personalized real-time feedback on mask fit, filter efficacy remaining, and individual exposure monitoring, effectively demanding a transition towards highly intelligent, data-aware respiratory protective equipment that maximizes user safety and compliance.

AI's most transformative role within the protective mask ecosystem currently lies in optimizing the highly sensitive logistics and manufacturing processes. Predictive analytics powered by machine learning models dynamically assess global air quality indicators and regional public health data to create sophisticated demand forecasts that are highly responsive to volatile environmental factors, such as the onset and spread of wildfire seasons or seasonal smog formation in mega-cities. This proactive forecasting enables manufacturers to adjust production volumes and inventory distribution across various regional hubs efficiently, minimizing both inventory holding costs and the devastating impact of stockouts during critical demand periods. Within the factory environment, AI systems utilizing computer vision are deployed for ultra-fast, high-precision quality control, automatically detecting minute manufacturing defects, such as imperfections in the ultrasonic welds or inconsistencies in filter layer density, guaranteeing that millions of units adhere strictly to stringent international certification standards like N95 or FFP3, thereby safeguarding product integrity and consumer trust at scale.

Looking ahead, the long-term impact of AI is focused on radical product personalization and enhanced user interaction. The integration of advanced sensor technology into masks, coupled with onboard edge AI processing, allows for the collection and rapid analysis of individual user data, including breathing volume, internal mask temperature, and immediate exposure to ambient contaminants. AI algorithms process this complex interaction data to provide highly personalized feedback via connected mobile applications, offering real-time alerts if the mask seal is broken, if the user is exhibiting excessive breathing resistance, or if filter saturation levels indicate imminent replacement. This capability moves the market beyond static PPE to dynamic, intelligent monitoring systems, fostering greater user compliance and enabling healthcare providers and industrial safety officers to gain objective, quantifiable insights into exposure risk. Such advancements solidify the high-value segment of the market, catering to users who prioritize data-driven, proactive respiratory protection solutions.

The operational landscape of the Air Dust and Smoke Pollution Protective Mask Market is defined by a powerful and multidimensional set of Drivers, Restraints, and Opportunities (DRO), which collectively shape the market’s trajectory and constitute its core Impact Forces. The primary driver is the undeniable, globally recognized decline in ambient air quality, stemming from geopolitical shifts towards heavy industry, unchecked vehicular emissions, and the increasingly devastating consequences of climate change manifesting as protracted wildfire seasons and intense dust events. This environmental imperative is strongly bolstered by the increasing harmonization and stringent enforcement of occupational safety regulations worldwide, where governmental bodies require documented compliance through the mandatory use of certified respirators in high-risk professional environments, creating a baseline, non-negotiable demand across all major industrial economies. Furthermore, the sustained global public health focus on airborne diseases has created a permanent shift in consumer behavior, establishing mask use as a routine, low-threshold preventive health measure in urban areas, transcending the temporary emergency response demand cycle.

However, the market faces several entrenched restraints that challenge sustainable growth and consumer trust. Foremost among these is the pervasive issue of product counterfeiting and the widespread circulation of masks that falsely claim compliance with high international standards (e.g., fake N95 or FFP3 markings). This rampant proliferation of sub-standard quality products severely erodes genuine consumer confidence in the efficacy of protective gear and creates unfair competitive pressure on certified manufacturers who adhere to rigorous quality controls. A further significant restraint is the economic barrier: the substantial cost differential between non-certified, low-filtration comfort masks and genuinely high-efficiency certified respirators (e.g., P100 cartridges or advanced reusable systems) often prohibits widespread adoption in economically disadvantaged populations or developing markets, leaving large segments unprotected. Finally, intrinsic user discomfort—relating to heat buildup, breathing resistance, and poor fit—remains a persistent restraint, leading to poor compliance rates, particularly in non-mandated personal use scenarios or extended industrial shifts.

Significant opportunities are simultaneously redefining the market’s potential and offsetting these restraints. The most impactful opportunity stems from the institutionalization of pandemic preparedness and strategic governmental stockpiling efforts, driven by lessons learned from recent global health crises, securing long-term, high-volume contracts for certified masks irrespective of short-term pollution fluctuations. Technologically, the rapid maturation of the reusable mask sector, which integrates highly efficient, easily replaceable, sustainable filter systems and utilizes advanced elastomeric materials for superior, personalized fit, presents a major opportunity to address both sustainability and comfort concerns, offering a compelling long-term value proposition. The development and commercialization of ‘smart’ protective masks, which integrate advanced sensor arrays, environmental monitoring, and connectivity features (IoT), enable manufacturers to penetrate the high-margin technology sector, differentiating their products beyond simple filtration capabilities and appealing to sophisticated consumer and high-tech industrial buyers seeking data-driven respiratory health management tools, positioning the industry for substantial growth through value-added features.

The Air Dust and Smoke Pollution Protective Mask Market is intricately segmented across various dimensions—product type, material composition, end-user application, and distribution strategy—to precisely map consumer purchasing behaviors, regulatory requirements, and competitive landscapes. Product type segmentation clearly distinguishes between disposable respirators, which capture the majority of the market volume due to their low cost and convenience, and reusable respirators (including half-face, full-face, and PAPRs), which command higher value due to their durability, superior seal performance, and adaptability for severe, prolonged hazard exposure in industrial settings. The core distinction often lies in the balance between cost, efficiency, and the operational environment. Disposable masks dominate non-mandated consumer use and single-shift industrial applications, whereas reusable devices are favored in environments requiring protection against high contaminant concentrations or where compliance with stringent fit-testing protocols is mandatory for worker safety, offering a robust long-term investment profile.

Material science forms the foundation of mask performance, segmenting the market into categories defined by filtration media. The dominant material remains non-woven fabrics, primarily polypropylene, which utilizes electrostatic charging to attract and capture particulate matter. However, the rapidly expanding high-performance segment relies heavily on next-generation materials: sophisticated nanofiber membranes, offering superior mechanical filtration efficiency against ultra-fine particles and smoke residues at significantly lower pressure drops, maximizing breathability. Furthermore, the inclusion of specialized functional materials, such as activated carbon layers, is crucial for masks designed to combat smoke and industrial fumes, as activated carbon effectively adsorbs gaseous pollutants and volatile organic compounds (VOCs) that conventional particulate filters cannot capture, positioning these products at the high-end of the performance and price spectrum and targeting markets exposed to petrochemical or urban pollution.

Analysis of the end-user application reveals a pivotal shift in demand dynamics. Historically, the Industrial sector (encompassing construction, mining, and manufacturing) was the primary consumer, driven entirely by regulatory compliance for occupational safety. While this remains a cornerstone segment, the Personal/Consumer Use segment has witnessed unprecedented expansion globally, propelled by rising air pollution levels, public health crises, and media exposure to environmental hazards like wildfires. This consumer segment requires masks that prioritize comfort, aesthetic design, and ease of use. The Healthcare segment represents a constant, albeit specialized, demand for surgical masks and certified N95/FFP2 respirators used during specific patient care activities and surges of airborne infections. The distribution segmentation highlights the growing importance of e-commerce, which has democratized access to protective masks for individual consumers, contrasting with the critical role of specialized industrial safety distributors and direct manufacturer contracts essential for serving large institutional buyers and government entities requiring guaranteed certified supply chains.

The operational efficiency and cost structure of the Air Dust and Smoke Pollution Protective Mask market are fundamentally shaped by its complex value chain, starting with highly specialized upstream sourcing. The upstream segment is dominated by highly technical material suppliers who produce the essential components: melt-blown non-woven synthetic polymers (primarily polypropylene and sometimes PTFE), and the sophisticated charging equipment necessary to impart the vital electrostatic capture capability for high-efficiency filtration media. Furthermore, suppliers of advanced materials like electrospun nanofiber mats and granular activated carbon play a crucial, high-value role. The upstream sector dictates the performance characteristics and certification potential of the final product, necessitating rigorous quality control and technical expertise. Due to the strict technical specifications required to achieve standards like FFP3 or N100, switching costs between highly certified raw material providers are high, which grants specialized suppliers significant leverage within the value chain and makes global commodity price volatility for polymer resins a direct cost risk for manufacturers.

The midstream manufacturing phase involves substantial capital investment in automated assembly lines, ultrasonic welding technology, and maintaining controlled, hygienic production environments, essential for product integrity, especially in the production of certified medical-grade masks. Manufacturers focus on product differentiation through patented design features that enhance fit, breathability, and ease of use, such as proprietary head strap systems or unique folding designs. This stage is where intellectual property rights regarding filtration media formulation and ergonomic design become critical competitive advantages. Downstream activities involve navigating a dual channel distribution strategy. The B2B channel, relying on specialized industrial safety distributors and direct sales forces, manages large volume contracts for occupational use, requiring technical support, fit-testing services, and guaranteed compliance documentation. The B2C channel, utilizing retail and e-commerce platforms, focuses on rapid fulfillment, consumer branding, and appealing to aesthetic and comfort preferences for personal anti-pollution use.

The distribution ecosystem is continuously evolving, with direct-to-consumer e-commerce gaining strategic importance, particularly after recent supply chain disruptions highlighted the need for diversified sales channels. Direct sales minimize reliance on third-party distributors and allow manufacturers to capture higher margins while maintaining control over brand messaging and combating counterfeiting through authenticated online storefronts. However, traditional industrial supply houses remain indispensable for serving niche, technically demanding markets like mining and heavy construction, where specialized inventory management, bundled PPE solutions, and localized technical expertise are required. The overall value chain is highly sensitive to geopolitical tensions, trade tariffs on raw materials, and the rapid changes in regional safety standards, demanding continuous adaptation and redundancy planning across all stages to ensure an uninterrupted supply of critical protective equipment globally, particularly during unpredictable environmental or health crises.

The universe of potential customers for Air Dust and Smoke Pollution Protective Masks is highly stratified, encompassing institutional buyers driven by regulatory mandates and individual consumers driven by personal health consciousness. Institutional customers constitute the largest and most stable segment of the market, primarily comprised of heavy industrial entities such as large construction firms engaged in infrastructure development, mining companies extracting raw materials, and manufacturing sectors including automotive, chemical, and metal processing, all of which are obligated by law to provide high-grade respiratory protection to their workforce against specific regulated airborne contaminants (e.g., crystalline silica, welding fumes, chemical vapors). These B2B customers prioritize compliance documentation, reliable supply, bulk pricing, fit-testing support, and product durability, often leading to long-term procurement contracts for reusable elastomeric respirators and high-filtration disposable FFP3 or P100 cartridges.

The second major category involves governmental and quasi-governmental organizations, including national health services, civil defense organizations, fire and rescue departments, and municipal public health agencies. These B2G buyers represent crucial strategic customers, particularly in the context of pandemic preparedness and mitigating the impact of large-scale disasters like wildfires. Their demand is characterized by cyclical procurement aimed at maintaining strategic national stockpiles of millions of certified N95/FFP2 units, prioritizing transparency in the bidding process, guaranteed material certification, and demonstrable capacity for surge supply during national emergencies. Their purchasing decisions are often less sensitive to price fluctuations than the B2B sector, provided the products meet stringent governmental quality and storage requirements, ensuring a critical safety buffer for the general population and first responders.

The fastest-expanding customer base is the individual consumer (B2C) segment, which consists of urban commuters, residents of highly polluted metropolitan areas, patients with pre-existing respiratory conditions, and residents subjected to seasonal wildfire smoke or dust storms. These consumers are discretionary purchasers, meaning their demand is directly influenced by real-time air quality reports, public health recommendations, media coverage, and perceived personal health risk. This segment demands masks that are comfortable, lightweight, aesthetically acceptable, and easy to carry, often preferring disposable or fashion-integrated reusable masks with certified internal filters. Successfully addressing this segment requires high-impact consumer branding, accessible retail distribution, and leveraging digital platforms to educate consumers on the specific benefits and proper usage techniques for highly effective air pollution protection.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.85 Billion |

| Market Forecast in 2033 | USD 9.08 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | 3M Company, Honeywell International Inc., Kimberly-Clark Corporation, AlphaProTech, Moldex-Metric, Inc., RZ Mask, Totobobo, Respro Ltd., GVS S.p.A., Drägerwerk AG & Co. KGaA, Prestige Ameritech, Shanghai Dasheng Health Products Manufacturing Co., Ltd., Makrite, Sure Safety India, Medline Industries, Inc., MSA Safety Inc., SENSIT Technologies, Suzhou Sanical Protective Product Manufacturing Co., Ltd., Sinotex, O&P Safety. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution of the Air Dust and Smoke Pollution Protective Mask market centers around three core pillars: enhancing filtration efficiency, minimizing breathing resistance, and integrating smart functionalities. The most transformative technological advancement is the widespread adoption of nanofiber filtration media. Unlike traditional melt-blown filters that rely heavily on electrostatic charge which degrades over time and with exposure to humidity, nanofiber technology creates a highly porous yet densely structured web of fibers, typically less than 100 nanometers in diameter. This allows for superior mechanical interception of ultra-fine particles, including the most penetrating particle size (MPPS) around 0.3 microns, while simultaneously creating a thinner, more breathable layer. Manufacturers are employing advanced electrospinning techniques to precisely control fiber diameter and distribution, significantly improving the efficacy of N99 and N100 respirators while maintaining the low pressure drop required for comfortable, prolonged use in industrial and daily environments.

The second major area of innovation is in smart respiratory technology, marking the entry of the Internet of Things (IoT) into personal protective equipment. These 'smart masks' incorporate miniaturized sensors for monitoring ambient air quality (PM2.5, CO2, VOCs), filter usage duration, and real-time assessment of the mask-to-face seal integrity. Data collected by these sensors is processed by on-board microprocessors and communicated wirelessly to smartphone applications, providing the user with actionable insights such as alerts for unsafe CO2 buildup, warnings about insufficient fit, or notifications for mandatory filter replacement based on actual environmental exposure. Furthermore, integration with augmented reality (AR) systems is being explored for industrial training, allowing supervisors to monitor worker compliance and physiological data remotely. This level of data integration moves protective masks from simple commodity items to complex health management tools, driving the premiumization of the high-end market segment.

Finally, significant R&D efforts are focused on advanced ergonomic design and sustainable material development. Addressing user compliance requires overcoming discomfort; thus, manufacturers are utilizing computational fluid dynamics (CFD) to optimize internal airflow patterns, efficiently managing heat and moisture buildup (the primary cause of discomfort). Materials innovation includes the development of self-cleaning or self-sanitizing mask surfaces using antimicrobial coatings, and the transition toward certified biodegradable polymers for disposable components, responding directly to global environmental sustainability pressures regarding PPE waste. For reusable systems, the focus is on developing lightweight, durable, and highly adaptive elastomeric seals that fit a wider range of facial geometries, ensuring consistent, leak-proof performance crucial for protection against toxic smoke and industrial aerosols, maximizing protection effectiveness across diverse global populations.

The global Air Dust and Smoke Pollution Protective Mask market displays significant regional variation in adoption rates, regulatory drivers, and market maturity, with Asia Pacific (APAC) serving as the undisputed epicenter of both consumption and manufacturing. This region, encompassing rapidly industrializing nations such as China, India, and Indonesia, suffers from some of the world's most severe ambient air pollution due to dense urban populations, heavy industrial output, and reliance on coal-based power generation. Consequently, the demand for both occupational respirators (for factory workers and construction sites) and personal anti-pollution masks is extraordinarily high, often driven by government-mandated emergency responses to severe smog episodes. While the regulatory landscape in APAC is highly fragmented, leading market players are aggressively pursuing regional certifications (e.g., KN95, KC Mark) and establishing localized production facilities to meet the massive scale of demand and overcome logistical challenges.

North America and Europe represent mature markets characterized by stringent occupational safety regulations (NIOSH in the US, EN standards in Europe) that mandate the use of high-efficiency respirators (N95/P100 and FFP2/FFP3) in hazardous industrial settings. Growth in these regions is increasingly propelled by acute environmental crises, particularly the escalating frequency and intensity of wildfires, which generate vast smoke plumes affecting major population centers far from the burn areas. This phenomenon has normalized the seasonal adoption of protective masks among the general public in affected areas, leading to predictable spikes in demand every summer and fall, driving robust governmental stockpiling initiatives. Furthermore, high consumer income levels allow for greater expenditure on premium, reusable, or technologically advanced "smart" mask solutions, focusing on comfort and enhanced features.

Latin America and the Middle East & Africa (MEA) are emerging regions exhibiting rapid market potential, primarily driven by large-scale infrastructure projects, expansion in the construction and mining sectors, and increasing regulatory emphasis on worker protection following international best practices. While consumer awareness about general pollution risks is rising, the industrial segment currently dominates the demand profile, particularly in oil and gas, and mining operations across countries like Brazil, Saudi Arabia, and South Africa. These regions face challenges related to product standardization and the prevalence of lower-cost, sometimes uncertified, imports. However, the adoption of international safety standards and growing investments in public health infrastructure are expected to accelerate the uptake of certified, high-quality protective masks throughout the forecast period, transitioning these markets from nascent to high-growth areas, particularly in urban centers experiencing rapid, often uncontrolled, growth.

Both N95 (US standard, NIOSH) and FFP2 (European standard, EN 149:2001) respirators are certified to filter out at least 94% to 95% of airborne particles (0.3 microns and larger). The primary difference is the regulatory body and testing criteria they adhere to, but they offer functionally equivalent protection against dust, smoke, and non-oil-based particulates, making them internationally recognized equivalents for high-efficiency filtration.

Wildfires and severe smog events act as significant short-term catalysts, creating acute, non-seasonal spikes in demand, especially for certified P95/N95 masks capable of filtering smoke particulates. These events drive massive governmental and consumer purchases, accelerate public awareness regarding respiratory safety, and pressure supply chains to increase production and stockpiling capacity, thereby boosting both revenue and production capacity expansion long-term.

Improvements in breathability and comfort are primarily driven by advanced filtration media, particularly nanofiber technology, which maintains high efficiency while lowering air pressure drop. Additionally, ergonomic design using lightweight silicone elastomers and integrating exhalation valves (where permitted) significantly reduces heat and moisture buildup inside the mask, enhancing compliance for prolonged wear in industrial and consumer settings.

Yes, the reusable mask segment, typically comprising elastomeric respirators with replaceable cartridges, offers superior sustainability by drastically reducing material waste compared to high-volume disposable masks. While the initial investment is higher, the long-term cost of ownership is generally lower in industrial settings due to the affordability of replacement filters versus continuous procurement of disposable units, coupled with their robust durability and potential for better sealing.

Asia Pacific (APAC) holds the strongest future growth potential, driven by unrelenting urbanization, sustained industrial output, and escalating air pollution levels. While established markets like North America and Europe offer high-value sales, APAC countries like India, China, and Southeast Asian nations provide massive untapped volume potential as regulatory enforcement strengthens and consumer spending on personal protective health items increases rapidly over the forecast period.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.