ID : MRU_ 434516 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

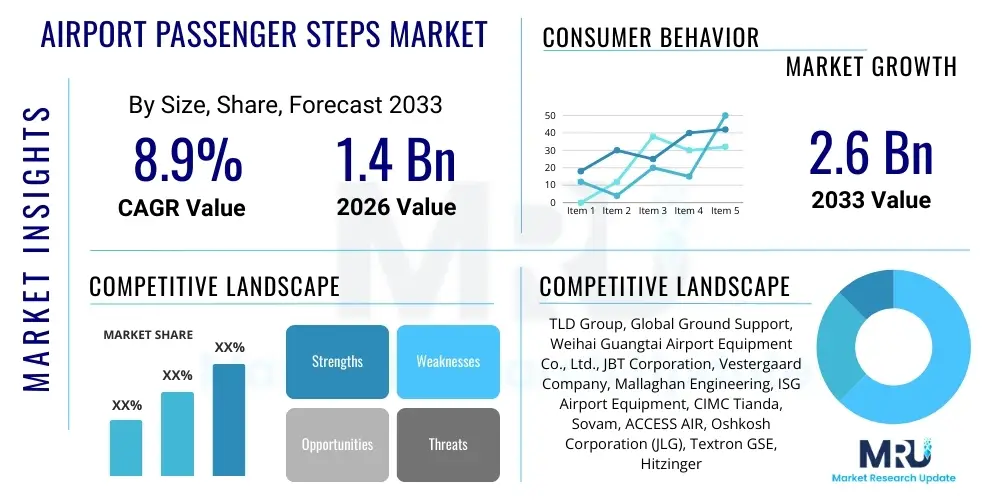

The Airport Passenger Steps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2026 and 2033. The market is estimated at USD 1.4 Billion in 2026 and is projected to reach USD 2.6 Billion by the end of the forecast period in 2033.

The Airport Passenger Steps Market encompasses the design, manufacturing, distribution, and maintenance of specialized ground support equipment (GSE) utilized for safely embarking and disembarking passengers from various types of aircraft. These steps, often referred to as airstairs or passenger stairs, are crucial components of airport operations, particularly at gates where jet bridges are unavailable or for low-cost carriers operating quick turnarounds on remote aprons. The market includes a range of products, from simple towable manual steps to complex, self-propelled, motorized units equipped with advanced safety features and height-adjustment capabilities designed to service the growing diversity of modern commercial aircraft, including both narrow-body and wide-body jets. The foundational purpose of these products is to ensure efficiency, safety, and compliance with strict aviation standards.

The primary driving factors for this market involve the relentless expansion of global air travel, especially in emerging economies, and the continuous infrastructural development and modernization of existing airports. As global passenger traffic increases, the demand for reliable and efficient GSE escalates commensurately. Furthermore, the product itself—the passenger step—has evolved significantly, transitioning from purely hydraulic systems to advanced electronic control systems (ECS) that offer precision docking, enhanced stability, and reduced maintenance costs. The versatility of modern passenger steps, capable of accommodating varying door sill heights and loading configurations, makes them indispensable assets for efficient ground operations management across small regional airports and large international hubs alike.

Major applications of airport passenger steps extend beyond standard boarding/deboarding at remote stands; they are also integral to specialized operations such as VIP services, military troop movement, and emergency evacuation training. The key benefits derived from their usage include maximized operational flexibility, particularly during peak travel times or adverse weather conditions, and improved accessibility for passengers, including those with reduced mobility (PRM), through integrated platform lifts and compliant step designs. The market is highly competitive, driven by innovation focusing on reducing environmental impact, improving energy efficiency (especially for electric self-propelled units), and integrating telematics for predictive maintenance and operational monitoring, thus aligning with the broader industry trend towards smart airport infrastructure.

The global Airport Passenger Steps Market is experiencing robust growth driven by significant capital investment in airport infrastructure expansion across Asia Pacific and the Middle East, coupled with the increasing fleet size of global airlines favoring quick turnarounds. Key business trends indicate a strong pivot towards self-propelled, electric, and hybrid passenger steps, reflecting the industry's commitment to sustainability and reduced carbon footprints on the apron. Technological integration, particularly in automated positioning systems and collision avoidance sensors, is becoming standard, ensuring enhanced safety and operational efficiency, thereby minimizing ground damage and delays. Furthermore, the consolidation within the Ground Support Equipment (GSE) manufacturing sector means market players are increasingly offering integrated solutions that include steps, dollies, and baggage handling systems, enhancing overall value proposition for large airport operators and handling companies.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine, fueled by the establishment of new international airports and the massive expansion of low-cost carrier (LCC) operations that heavily rely on mobile passenger steps rather than fixed jet bridges to reduce infrastructure costs. North America and Europe, while mature markets, demonstrate demand primarily for replacement equipment and advanced models featuring advanced automation and electric powertrains to comply with stringent environmental regulations and operational safety standards imposed by organizations like the FAA and EASA. The Middle East continues its trend of massive capital projects, driving high demand for heavy-duty, wide-body compatible steps necessary to service the large Airbus A380 and Boeing 747 fleet operated by regional flagship carriers.

Segment trends indicate that the self-propelled segment is dominating revenue generation due to its inherent operational flexibility and labor efficiency compared to towable alternatives. By application, the demand for steps capable of servicing wide-body aircraft is growing faster, reflecting the expansion of long-haul international routes. Moreover, there is a clear segmentation shift focusing on specialized steps for regional aircraft in developing markets and enhanced safety-focused steps catering to aging fleets in established regions. The emphasis across all segments remains on durability, operational uptime, and total cost of ownership (TCO) reduction through modular design and integrated diagnostics, cementing the market's trajectory toward high-tech, sustainable GSE solutions.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Airport Passenger Steps Market predominantly revolve around three critical areas: achieving zero-error docking accuracy, automating maintenance scheduling, and optimizing equipment deployment across congested airport aprons. Users frequently question how AI algorithms can ensure the precise, millimeter-level positioning required to safely interface steps with varying aircraft door sills under diverse environmental conditions (wind, rain, low visibility). Furthermore, airport managers are concerned with how machine learning can transform preventative maintenance from scheduled checks into predictive interventions, significantly increasing the equipment's operational uptime and lifespan. The key expectations center on AI’s ability to fully integrate passenger steps into the broader Smart Airport ecosystem, optimizing traffic flow and resource allocation in real-time to prevent costly ground delays and incidents.

The Airport Passenger Steps Market is profoundly influenced by a complex interplay of Drivers (D), Restraints (R), and Opportunities (O), which collectively determine the growth trajectory and competitive landscape, summarized as Impact Forces. The primary driver is the accelerating growth in global air passenger traffic, necessitating more frequent and rapid aircraft turnarounds, particularly in high-volume regional hubs and international gateway airports. This is compounded by regulatory pressures mandating high safety standards and enhanced accessibility features (e.g., ADA compliance in North America, and EU regulations for Persons with Reduced Mobility - PRM), which forces airport operators to upgrade or replace aging GSE with modern, compliant units. Furthermore, the drive toward sustainability is creating a major push for electric and hybrid-powered steps, moving away from conventional diesel equipment, thus revitalizing the market with new product cycles and innovative powertrain technologies.

Conversely, significant restraints hinder market potential. High initial acquisition costs associated with advanced, self-propelled, motorized steps, especially those with complex electronic controls and safety systems, pose a barrier to entry, particularly for smaller regional airports or ground handling companies operating on tight margins. Furthermore, the lack of standardized technical specifications across different aircraft types and manufacturers necessitates highly adjustable and complex step designs, increasing manufacturing complexity and maintenance requirements. The long operational lifespan of GSE also slows down replacement cycles in mature markets like Western Europe and North America, where replacement demand is cyclical rather than continuous. Lastly, the increasing proliferation of fixed jet bridges at modernized gates naturally limits the application scope for mobile passenger steps, restricting their usage primarily to remote stands and low-cost carrier terminals.

Opportunities within the market are substantial, chiefly centered on technological innovation and geographical expansion. The burgeoning development of smart airport infrastructure globally creates a niche for integrating passenger steps with airport operations management systems (AOMS) through IoT and telematics, enabling real-time diagnostics and efficiency monitoring. Geographically, the massive airport construction and expansion projects currently underway in high-growth regions like Southeast Asia, India, and the Gulf Cooperation Council (GCC) countries offer lucrative avenues for market penetration. Moreover, the aftermarket services segment, covering maintenance, repair, and overhaul (MRO), presents a stable revenue stream, especially as operators look to extend the life and improve the performance of their existing, expensive GSE assets rather than purchasing new ones immediately. These forces collectively shape a market where technological adopters gain competitive advantages by offering superior safety, efficiency, and sustainability features.

The Airport Passenger Steps Market is systematically segmented primarily based on mobility type (Towable vs. Self-Propelled), power source (Diesel, Electric, Hybrid), operational mechanism (Manual vs. Motorized), and application (Narrow-Body, Wide-Body, Regional Aircraft). This structure allows stakeholders to analyze demand drivers specific to different operational environments and capital expenditure capabilities. The segmentation by mobility type is crucial, as self-propelled steps, while more expensive, offer superior efficiency and maneuverability crucial for high-traffic international airports, contrasting with simpler, cost-effective towable steps favored by smaller regional facilities or dedicated cargo operators. Furthermore, the segmentation by power source directly reflects global regulatory shifts and corporate sustainability goals, pushing substantial growth in the electric and hybrid categories.

Detailed analysis of the market segments reveals distinct purchasing patterns influenced by the predominant fleet mix of the servicing airport. Airports serving large intercontinental hubs prioritize steps rated for Wide-Body aircraft (like the Boeing 777 or Airbus A380), requiring robust load capacities and extensive height adjustment ranges. Conversely, airports dominated by short-haul and regional traffic focus on agility and rapid deployment inherent in equipment designed for Narrow-Body jets (such as the Airbus A320 family or Boeing 737 series). The continued investment in advanced features like automated leveling systems, integrated sensor arrays for anti-collision, and ergonomic designs emphasizes the industry's commitment to maximizing safety and minimizing human interaction during complex docking procedures.

The complexity within the segmentation also allows manufacturers to tailor products precisely. For instance, the convergence of motorized mechanisms with self-propelled chassis creates the premium segment, which demands high reliability and minimal labor input. This is contrasted with the niche market for manual, towable steps which serves as a cost-effective backup solution or primary equipment for low-traffic aerodromes. Understanding these segment dynamics—how end-users balance acquisition cost against long-term operational efficiency and compliance—is critical for defining competitive pricing and market penetration strategies within the diverse global airport ecosystem.

The value chain for the Airport Passenger Steps Market begins with the upstream suppliers providing critical raw materials and components, including specialized metals (high-grade steel and aluminum alloys for structure and durability), complex hydraulic systems, high-efficiency electric motors and batteries, and advanced electronic control units (ECUs). Innovation in the upstream segment, particularly concerning lightweight, high-strength materials and reliable, maintenance-free hydraulic components, directly impacts the final product's performance and lifespan. Manufacturers rely heavily on consistent quality and competitive pricing for these raw materials, which constitute a significant portion of the total production cost. Strategic sourcing and long-term supply agreements are essential to mitigate risks associated with volatile commodity prices and specialized component availability, ensuring manufacturing efficiency.

The core of the value chain involves the manufacturing and assembly process, where leading GSE companies design, engineer, and fabricate the final passenger steps, integrating safety features like automated leveling, anti-collision sensors, and weather protection enclosures. Distribution channels are predominantly direct, especially for large, customized orders placed by major international airports or large ground handling conglomerates, necessitating dedicated sales teams, technical support, and extensive pre-sales consultation. Indirect distribution via regional distributors and leasing companies is often utilized for smaller markets or by airports preferring operational expenditure models (leasing) over capital expenditure (direct purchase), offering financial flexibility and comprehensive maintenance packages built into the leasing agreement.

Downstream activities center around the end-users—commercial and military airports, and specialized ground handling service providers—who utilize the steps for day-to-day operations. The long-term profitability in the downstream market is heavily reliant on the aftermarket services segment, including spare parts supply, routine preventative maintenance, and major overhaul contracts. Manufacturers often establish specialized MRO facilities globally to minimize equipment downtime, generating stable, recurring revenue streams long after the initial sale. The quality of these post-sale services is a critical competitive differentiator, ensuring the operational readiness and longevity of the highly utilized and safety-critical passenger steps, thereby completing the robust value chain from raw material to operational readiness.

Potential customers for airport passenger steps primarily comprise three key groups: global commercial airport operators, independent ground handling service providers (GHSPs), and governmental entities, specifically military airbases and defense procurement agencies. Commercial airports, ranging from major hubs managing millions of passengers annually to smaller regional airports focusing on connectivity, are direct purchasers when they manage their own GSE fleet. Their buying decisions are driven by fleet compatibility, safety compliance, long-term durability, and increasingly, the availability of electric and eco-friendly models to meet sustainability targets and noise reduction mandates.

Independent ground handling companies represent a rapidly growing and substantial segment of the customer base. These firms, such as Swissport, Menzies Aviation, and Dnata, contract with numerous airlines and airports globally to provide end-to-end ramp services, including the provision and operation of passenger steps. Their purchasing strategy is focused on achieving high utilization rates, minimum total cost of ownership (TCO), and maximum operational flexibility across diverse environments and aircraft types. They often favor highly maneuverable, self-propelled steps with proven reliability, viewing their GSE fleet as a direct operational leverage point that impacts turnaround efficiency and contractual fulfillment.

Finally, governmental and private entities, including military air transport commands and Fixed-Base Operators (FBOs) servicing private and corporate jets, constitute specialized customers. Military organizations require robust, heavy-duty steps designed for rapid deployment and often compliance with ruggedized specifications to operate in austere environments. FBOs, serving high-net-worth clients, demand aesthetically superior, premium steps that integrate advanced features and high-level comfort and safety, reflecting the luxury nature of the private aviation sector. These distinct customer segments ensure a diverse demand landscape across the globe, each prioritizing specific attributes from the GSE suppliers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.4 Billion |

| Market Forecast in 2033 | USD 2.6 Billion |

| Growth Rate | 8.9% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TLD Group, Global Ground Support, Weihai Guangtai Airport Equipment Co., Ltd., JBT Corporation, Vestergaard Company, Mallaghan Engineering, ISG Airport Equipment, CIMC Tianda, Sovam, ACCESS AIR, Oshkosh Corporation (JLG), Textron GSE, Hitzinger GmbH, Adelte, Aviramp Ltd., Liftking, Fast Global Solutions, Hydro Systems, Guangtai, Shenzhen Sino-American Logistics Equipment Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Airport Passenger Steps Market is rapidly evolving, moving away from purely mechanical and hydraulic systems toward sophisticated electronic and digital integration. A primary innovation focus is the transition to electric and hybrid powertrains, driven by the global imperative to decarbonize airport ground operations. Modern electric steps utilize high-density lithium-ion batteries and highly efficient drive motors, offering zero tailpipe emissions, significantly reduced operational noise, and lower fuel costs. These systems require advanced Battery Management Systems (BMS) to ensure safety, rapid charging capabilities, and consistent power delivery throughout demanding operational shifts, making battery technology a critical area for competitive differentiation among manufacturers.

Another major technological advancement is the integration of advanced sensor technology, telemetry, and the Internet of Things (IoT). Modern passenger steps are equipped with Lidar, ultrasonic sensors, and sophisticated cameras that enable automated collision detection and highly accurate, semi-autonomous docking systems. These systems guide the operator precisely to the aircraft door, minimizing the risk of expensive ground damage, a leading cause of operational downtime. Furthermore, IoT connectivity allows the step's operational data—including engine performance, lift cycle count, operational hours, and fault codes—to be transmitted in real-time back to airport operations control centers and GSE maintenance teams, facilitating highly effective remote diagnostics and predictive maintenance scheduling.

The design and engineering process itself has been revolutionized through the adoption of modular construction and composite materials. Modular steps allow for easier maintenance, rapid replacement of damaged components, and enhanced scalability to accommodate varying aircraft heights and accessibility requirements. The use of advanced materials, while improving structural integrity and longevity, also contributes to overall weight reduction, which is crucial for maximizing efficiency in electric models. Future technology deployment is anticipated to focus heavily on enhanced cyber-security for integrated control systems, and further automation, potentially leading to fully autonomous, programmed steps that integrate seamlessly into the AI-driven logistics of tomorrow's smart airport environments.

The global Airport Passenger Steps Market displays significant regional variations in growth drivers, technology adoption, and replacement demand, fundamentally reflecting the maturity and growth rates of local aviation sectors. Asia Pacific (APAC) stands out as the epicenter of new demand, driven by massive investments in greenfield airports (especially in China, India, and Southeast Asia) and the rapid expansion of regional and low-cost carrier fleets that rely extensively on apron operations. The push in APAC is for both volume and technological readiness, with many new airports integrating requirements for electric GSE from the outset to meet ambitious environmental goals. The high volume of new construction projects ensures that APAC will maintain the highest compound annual growth rate throughout the forecast period, requiring thousands of new units annually.

North America and Europe represent mature markets characterized primarily by replacement demand and regulatory-driven modernization. In these regions, the emphasis is heavily placed on transitioning legacy diesel fleets to electric or hybrid models to comply with strict emissions regulations (e.g., EU Green Deal mandates and California Air Resources Board standards). While the overall number of new airport builds is low, the requirement for high-specification, safety-compliant, and fully automated steps for existing major hubs (such as those in the US and Germany) ensures steady, high-value procurement cycles. European markets, in particular, show a strong preference for innovative PRM (Persons with Reduced Mobility) accessible steps and modular designs to optimize existing, often space-constrained apron environments.

The Middle East and Africa (MEA) region presents a dichotomy, with the Gulf Cooperation Council (GCC) countries exhibiting extremely high demand driven by ongoing mega-projects (e.g., new terminals and satellite airports) and the servicing needs of the world’s largest wide-body aircraft fleets. Investments here focus on heavy-duty, highly durable steps capable of withstanding extreme climate conditions and providing reliable service for A380s and B747s. Conversely, the African market, while representing future growth potential, is currently characterized by low penetration rates and a preference for cost-effective, easily maintainable towable and manual steps, though modernization efforts in regional hubs like South Africa and Nigeria are beginning to drive interest in entry-level motorized units.

The primary drivers are stringent global environmental regulations, particularly in North America and Europe, which mandate reduced noise and zero or low emissions on the apron. Additionally, electric steps offer lower long-term operational costs (fuel and maintenance) and improved corporate sustainability profiles for airport operators and airlines.

Segmentation by aircraft application dictates the required capacity and vertical reach of the steps. Wide-Body compatible steps are high-value, complex units needed primarily at international hubs, whereas Narrow-Body steps prioritize maneuverability and speed, essential for efficient short-haul and low-cost carrier operations, driving higher unit volume demand.

Asia Pacific (APAC) currently offers the highest growth opportunities, primarily due to large-scale infrastructure investments, continuous development of new international airports, and the rapid expansion of air travel and fleet modernization programs across Southeast Asia and India.

Modern passenger steps incorporate advanced safety technologies such as anti-collision sensors (Lidar/Ultrasonic), automated leveling and stabilization systems, integrated sensor diagnostics, and enhanced ergonomic design to minimize operational hazards and prevent expensive ground damage to aircraft fuselages.

Ground handling companies generally prefer self-propelled steps, particularly for high-volume operations, due to their superior efficiency, faster deployment times, and enhanced maneuverability. Towable steps are typically reserved for low-volume regional airports or serve as emergency backup units.

The operational lifespan of a high-quality, motorized self-propelled passenger step typically ranges between 15 to 25 years, heavily dependent on the quality of maintenance, operating environment, and frequency of use. Predictive maintenance via telematics integration is helping operators maximize this lifespan.

IoT and Telematics significantly influence the market by enabling real-time remote monitoring of equipment status, predictive fault detection, optimization of utilization rates, and detailed reporting on operational efficiency. This connectivity reduces downtime and lowers the total cost of ownership (TCO).

The growth of LCCs directly boosts demand for mobile passenger steps, as LCCs frequently use remote stands instead of jet bridges to minimize gate rental costs and maximize rapid aircraft turnaround times (TAT). This drives the need for flexible, reliable GSE capable of quick deployment.

Yes, there are specialized steps designed for regional aircraft. These units are typically smaller, lighter, and feature lower minimum platform heights to accommodate the distinct door sill levels of regional jets and turboprops, focusing on quick service and high stability.

The primary restraints include the significantly higher initial capital expenditure required for electric models compared to diesel steps, and the lack of robust charging infrastructure and dedicated maintenance skills required to support high-voltage battery systems in many developing market airports.

Automation is crucial for enhanced safety and efficiency, focusing on automated vehicle guidance systems (AVGS) for precise docking, self-leveling platforms to compensate for ground unevenness, and integrated diagnostic reporting, moving towards fully autonomous operation within constrained apron boundaries.

Manufacturers ensure compatibility through highly adjustable, wide-ranging platform height mechanisms, often utilizing telescopic or variable inclination staircases. Modern self-propelled steps are designed with extensive operational envelopes to service everything from small regional jets to the largest commercial liners.

The primary factor driving replacement demand is regulatory compliance, specifically the need to replace older, high-emission diesel equipment with newer electric or low-emission units, alongside incorporating mandatory safety upgrades and compliance features for accessibility (PRM).

While electric steps have a higher initial purchase price, their TCO is often lower over the equipment's lifespan due to drastically reduced energy costs, lower maintenance requirements (fewer moving parts, no oil changes), and potential tax incentives for green GSE.

Extreme weather conditions (high winds, ice, extreme heat) pose challenges related to structural stability, traction, and the reliability of hydraulic and electronic systems. Manufacturers address this by ruggedizing components, integrating specialized heating elements, and designing steps for increased lateral stability.

Yes, specialized boarding ramps, particularly motorized or towable units designed to offer ramp access or high-capacity PRM solutions (often supplied by companies like Aviramp), are considered a high-value niche segment within the broader Airport Passenger Steps Market.

Modern passenger steps primarily utilize high-strength steel for the chassis and structure to ensure durability and load-bearing capacity, coupled with lightweight aluminum alloys for the stairs and platforms, reducing overall weight while maintaining structural integrity.

The aftermarket services segment (MRO, spare parts) is extremely important, often representing a highly profitable and stable recurring revenue stream for manufacturers. Effective MRO services are critical to ensuring high operational uptime for customers' critical ground support assets.

FBOs drive demand for a specialized, high-end segment of the market, requiring aesthetically pleasing, highly reliable, and often customized steps with premium finishes, designed specifically to cater to the luxury and safety demands of private and corporate aviation clients.

The market recovery is marked by accelerated GSE fleet renewal, driven by pent-up demand and regulatory pressure to modernize. Airports are prioritizing resilient, flexible, and sustainable equipment (electric) to prepare for anticipated long-term growth and avoid future operational disruptions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.