ID : MRU_ 433088 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

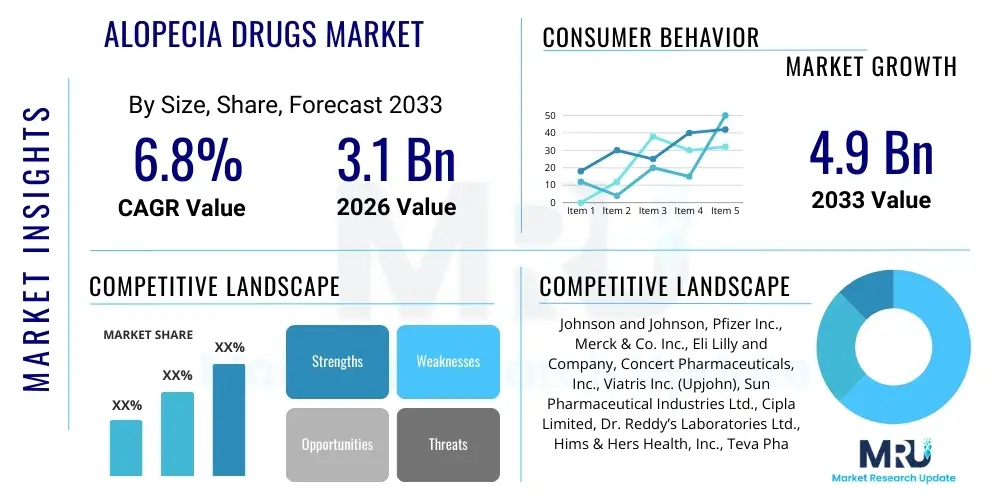

The Alopecia Drugs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 3.1 Billion in 2026 and is projected to reach USD 4.9 Billion by the end of the forecast period in 2033.

The Alopecia Drugs Market encompasses pharmaceutical products designed for the treatment of various forms of hair loss, ranging from androgenetic alopecia (pattern baldness) to autoimmune conditions like alopecia areata. This specialized therapeutic domain is characterized by a strong focus on dermatological innovation and personalized medicine. The market includes widely recognized treatments such as topical minoxidil and oral finasteride, alongside newer classes of drugs like Janus Kinase (JAK) inhibitors, which are transforming the treatment landscape for severe autoimmune-related hair loss. Product development is increasingly centered on enhancing efficacy, reducing side effects, and developing delivery mechanisms that improve patient adherence, addressing a significant global cosmetic and psychological health concern.

Major applications of these drugs primarily revolve around managing chronic hair loss conditions. Androgenetic alopecia remains the largest segment, driven by high prevalence in both male and female populations. However, the market is experiencing rapid expansion in treating complex indications such as chemotherapy-induced alopecia and scarring alopecias. The core benefit of alopecia drugs is the stimulation of hair regrowth and the prevention of further hair miniaturization, leading to improved quality of life and enhanced self-esteem for patients. Furthermore, research is intensely focused on understanding the molecular pathways of hair follicle cycling to develop targeted therapies that offer curative or long-lasting results, moving beyond symptomatic management.

Driving factors for market growth include the rising prevalence of chronic diseases, stress-related hair loss (telogen effluvium), and genetic predispositions, coupled with increased aesthetic awareness globally. Demographic shifts, particularly the aging population, also contribute significantly to the demand for effective treatments. Crucially, increased research funding and regulatory approvals for novel drug classes, particularly in the biologics and small molecule inhibitor categories, are accelerating market expansion. Improved diagnostic tools and greater physician awareness regarding the underlying causes of different alopecia types enable more precise treatment initiation, thereby boosting the adoption rates of prescription drugs.

The Alopecia Drugs Market is undergoing a significant transformation, marked by robust business trends focusing on targeted therapies and non-surgical interventions. Key business trends include substantial investment in late-stage clinical trials for JAK inhibitors, shifting the treatment paradigm for alopecia areata from corticosteroids to oral systemic agents. Pharmaceutical companies are prioritizing pipeline development through strategic mergers, acquisitions, and licensing agreements to access innovative drug candidates and delivery technologies. Furthermore, the market sees a trend toward combination therapies, utilizing established treatments alongside novel biological agents to maximize therapeutic outcomes, particularly in recalcitrant cases of hair loss, thereby broadening the commercial opportunities for market players.

Regional trends indicate North America maintaining its dominance due to high healthcare expenditure, established reimbursement policies, and the rapid adoption of advanced therapies, especially new FDA-approved treatments. Europe follows closely, driven by increasing awareness and access to specialty dermatological care. However, the Asia Pacific region is projected to exhibit the highest growth rate during the forecast period. This accelerated growth is primarily attributed to the vast, untapped patient pool, improving healthcare infrastructure, and the growing urbanization and disposable incomes that facilitate access to expensive prescription treatments, creating strong demand for both generic and branded products.

Segment trends reveal that the prescription drugs segment, particularly JAK inhibitors, is witnessing the fastest expansion, overshadowing traditional over-the-counter (OTC) products in value generation. Among disease indications, alopecia areata is the most dynamic segment due to the introduction of highly effective systemic treatments. By distribution channel, the hospital pharmacy segment continues to be vital for specialty drugs, but the retail pharmacy and online pharmacy segments are gaining momentum, driven by patient preference for convenience and the rising trend of direct-to-consumer healthcare models. Technological advances in drug formulation, such as liposomal and microneedle-assisted delivery systems, are enhancing drug absorption and local efficacy, further refining segment performance.

Common user questions regarding AI's impact on the Alopecia Drugs Market frequently center on its role in drug discovery acceleration, personalized treatment prediction, and enhancing diagnostic accuracy. Users are keen to know if AI can identify novel molecular targets for non-responders to current treatments, specifically asking about AI’s capability to analyze complex genomic and proteomic data to predict patient response to minoxidil or finasteride, or the newer JAK inhibitors. Concerns often involve data privacy related to patient images and genetic profiles used by AI algorithms, and the integration of AI-powered diagnostic tools into standard clinical practice. Expectations are high regarding AI’s potential to optimize clinical trial designs, reducing cost and duration, and leading to faster market entry for novel alopecia therapies.

The key themes summarized from user inquiries focus predominantly on predictive analytics in clinical settings and efficiency improvements in Research and Development (R&D). Users expect AI to move beyond simple automation, predicting which patients are most likely to benefit from specific drugs, thereby optimizing resource allocation and minimizing unnecessary drug exposure for non-responsive individuals. There is significant interest in how machine learning (ML) models can process vast amounts of dermatological imaging data—like trichoscopy images—to provide earlier and more precise diagnoses of different alopecia subtypes (e.g., distinguishing between telogen effluvium and early androgenetic alopecia), which traditionally relies heavily on subjective clinical assessment.

Ultimately, users anticipate AI will revolutionize the development lifecycle of alopecia drugs. This includes using deep learning to screen compound libraries for potent small molecule inhibitors targeting inflammation or hair cycle pathways, predicting toxicity profiles early in development, and optimizing dosing strategies based on virtual patient cohorts. The integration of AI tools is expected to lead to the emergence of truly personalized treatments, moving away from the current one-size-fits-all approach, and significantly improving the success rates of new drug candidates entering the clinical pipeline for hair loss conditions.

The Alopecia Drugs Market is propelled by significant drivers, notably the increasing global prevalence of hair loss conditions fueled by lifestyle factors, chronic stress, and genetic susceptibility. Restraints, however, include the high cost associated with novel biologic therapies, the long treatment duration required for efficacy, and significant patient non-adherence due to perceived side effects or slow results. Opportunities are abundant, centered around the development of highly specific topical formulations, the repurposing of existing drugs (such as topical prostaglandins or immunosuppressants), and the expansion into emerging markets where prevalence rates are rising but treatment penetration is low. These forces collectively shape the competitive landscape and dictate the trajectory of pharmaceutical innovation and commercial strategy within the sector.

Key drivers include the dramatic advancements in understanding the immunological basis of alopecia areata, leading to the regulatory approval and subsequent high adoption rate of systemic JAK inhibitors. Increased consumer awareness, amplified by social media and aesthetic culture, drives patients to seek medical consultation earlier, increasing prescription rates. Furthermore, robust investment in R&D by major pharmaceutical and biotechnology firms, particularly in gene therapy and stem cell research aimed at permanent hair restoration, acts as a powerful long-term growth catalyst. The availability of effective generic versions of established drugs like finasteride also improves accessibility for a broader population base, expanding the total addressable market.

Restraints primarily revolve around the challenges in achieving sustained and complete hair regrowth across diverse patient populations. Current treatments often lead to partial recovery, and cessation of treatment typically results in relapse. Regulatory hurdles for novel biologics require extensive safety data due to their systemic effects, slowing down market entry. A significant impact force is the competition from non-pharmaceutical alternatives, including surgical procedures (hair transplantation) and cosmetic products, which divert consumer interest, especially among patients seeking rapid, non-daily interventions. Pricing pressure from healthcare systems and payers, particularly concerning expensive specialty drugs, also acts as a constraint on market value expansion, mandating strong efficacy data to justify high costs.

The Alopecia Drugs Market segmentation provides a detailed structural analysis based on drug class, indication, distribution channel, and route of administration, enabling stakeholders to pinpoint key areas of growth and investment. The market is primarily segmented based on the mechanism of action of the drugs, differentiating between hormonal modulators (like 5-alpha reductase inhibitors), growth stimulants (like vasodilators), and immunomodulators (like JAK inhibitors). The indication segmentation highlights the specific therapeutic areas driving revenue, with androgenetic alopecia traditionally dominating, but alopecia areata showing the highest recent growth due to new product launches. Analyzing these segments is crucial for understanding current prescribing patterns and anticipating future therapeutic advancements, particularly in personalized medicine approaches.

The drug class segmentation is vital as it reflects the current state of R&D and regulatory success. For instance, the recent emergence and success of oral JAK inhibitors have fundamentally reshaped the competitive dynamics within the immunomodulatory segment, offering high efficacy for moderate-to- severe alopecia areata previously unachievable with topical or conventional systemic agents. Concurrently, the route of administration distinction—topical versus oral—reflects patient preference and side effect profiles. Topical solutions remain popular for early or mild cases due to lower systemic risk, while oral treatments are reserved for more severe or widespread conditions, creating distinct revenue streams within the market structure.

Geographically, market segmentation reveals disparities in treatment adoption and drug availability, influencing commercial strategies. Developed economies see high penetration of branded and specialty drugs, while emerging markets rely more heavily on generics and accessible OTC options. The distribution channel segmentation, covering hospital pharmacies, retail pharmacies, and online channels, tracks the flow of these medicines to the end consumer. As telehealth and prescription digitalization gain traction, the online pharmacy segment is expected to capture a larger share, particularly for chronic, long-term treatments like alopecia drugs, requiring efficient and discreet fulfillment methods.

The value chain for the Alopecia Drugs Market begins with extensive upstream activities encompassing R&D, active pharmaceutical ingredient (API) manufacturing, and clinical trials. This phase is characterized by high capital investment and intellectual property protection, particularly for novel biologics and small molecule inhibitors. The efficiency and success of the upstream segment depend heavily on technological innovation in target validation and formulation science, ensuring the purity and stability of APIs like Finasteride or specialized compounds used in JAK inhibitors. Key upstream players include specialized biotech firms and large pharmaceutical R&D divisions responsible for identifying therapeutic leads and managing the complex, multi-stage regulatory approval process required before commercialization.

The midstream phase involves drug manufacturing, formulation, and primary packaging. This stage ensures compliance with Good Manufacturing Practices (GMP) and involves converting the API into finished dosage forms—tablets, capsules, or topical solutions. Contract Manufacturing Organizations (CMOs) play a significant role here, offering specialized facilities and scaling capabilities. Downstream activities are centered on distribution, marketing, and sales. The distribution channel is critical, involving warehousing, logistics providers, wholesalers, and specialized distributors who handle temperature-sensitive or controlled substances. Due to the high patient volume and chronic nature of alopecia treatments, efficiency in the downstream supply chain directly impacts market access and profitability.

The final layer involves the connection to the end-users through direct and indirect channels. Direct channels often involve specialty pharmacies dispensing high-cost drugs directly to clinics or patients, particularly for rare or severe alopecia cases requiring specialized handling. Indirect channels utilize the extensive network of retail pharmacies and, increasingly, online pharmacies for common prescriptions like Minoxidil and Finasteride. Effective marketing strategies, often targeting dermatologists and primary care physicians, are essential for driving prescriptions. Pricing strategies and reimbursement negotiations with payers also represent a critical function in the value chain, directly influencing the final accessibility and uptake of both branded and generic alopecia medications.

Potential customers for the Alopecia Drugs Market are diverse, primarily segmented by demographic factors (age and gender), the specific type and severity of hair loss, and their willingness to invest in long-term pharmaceutical solutions. The primary end-users are individuals diagnosed with chronic hair loss conditions, with a significant concentration in the middle-aged and elderly populations globally, as the incidence of androgenetic alopecia increases with age. However, the rapidly expanding segment of autoimmune alopecia patients (Alopecia Areata) represents a high-value customer base, as these individuals often require expensive, newly approved systemic therapies like JAK inhibitors, translating into higher average revenue per patient for manufacturers.

The immediate buyers, or prescribers, include dermatologists who specialize in hair and scalp disorders, endocrinologists dealing with hormonal imbalance-related hair loss, and increasingly, general practitioners who manage mild to moderate cases. The growth in aesthetic and anti-aging medicine clinics also broadens the customer base, as these clinics actively market pharmaceutical solutions alongside cosmetic procedures. Furthermore, patients who have previously failed or experienced side effects from conventional treatments (e.g., surgical hair transplants or nutritional supplements) are high-potential customers for innovative, targeted drug therapies currently in the pipeline.

A crucial customer group includes health insurance providers and government healthcare programs (payers). Although not the direct consumers, their coverage decisions determine the accessibility and affordability of expensive branded alopecia drugs. Manufacturers must continuously demonstrate superior efficacy and cost-effectiveness to secure favorable formulary placement. Finally, over-the-counter (OTC) consumers form a large segment, purchasing topical Minoxidil without a prescription, driven by convenience and perceived lower risk, representing a continuous, high-volume revenue stream for established brands in the consumer healthcare division of pharmaceutical companies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.1 Billion |

| Market Forecast in 2033 | USD 4.9 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Johnson and Johnson, Pfizer Inc., Merck & Co. Inc., Eli Lilly and Company, Concert Pharmaceuticals, Inc., Viatris Inc. (Upjohn), Sun Pharmaceutical Industries Ltd., Cipla Limited, Dr. Reddy’s Laboratories Ltd., Hims & Hers Health, Inc., Teva Pharmaceutical Industries Ltd., Almirall S.A., Shionogi & Co. Ltd., Aclaris Therapeutics Inc., Astellas Pharma Inc., Bausch Health Companies Inc., Organon & Co., Arena Pharmaceuticals, Cassiopea S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Alopecia Drugs Market is rapidly evolving, moving beyond traditional small molecule treatments toward sophisticated biological and delivery systems. A primary technological focus is on the development and optimization of Janus Kinase (JAK) inhibitors. This class of drugs leverages advanced small molecule chemistry to target specific inflammatory pathways (JAK-STAT signaling) crucial in the pathogenesis of autoimmune alopecia areata. The complexity lies in developing highly selective JAK inhibitors (like JAK1/2 or JAK3 specific) to maximize efficacy while minimizing systemic side effects, requiring advanced medicinal chemistry techniques and rigorous pre-clinical profiling to ensure optimal therapeutic indices.

Beyond systemic treatments, significant technological innovation is dedicated to enhancing the delivery of existing and new topical agents. Technologies such as microneedle arrays are being researched to create transient channels in the skin, dramatically improving the transdermal absorption of active ingredients like minoxidil and specific peptides, bypassing the barrier function of the stratum corneum. Furthermore, liposomal and nanocarrier technologies are employed to encapsulate drugs, protecting them from degradation and enabling targeted release directly into the hair follicle unit, maximizing local concentration and reducing systemic exposure, which is critical for patient safety and long-term adherence to treatment protocols.

Future technological advancements are heavily invested in regenerative medicine and gene therapy. Research involves leveraging stem cell technology to regenerate hair follicles from dermal papilla cells, potentially offering a permanent cure for androgenetic alopecia. Gene editing techniques, while nascent, are exploring ways to correct or modulate genes associated with hair loss susceptibility. These high-risk, high-reward technologies require cutting-edge molecular biology, bioinformatics, and controlled delivery systems (e.g., viral vectors) to ensure safe and effective cellular reprogramming. These technological pillars collectively signify a transition toward curative and highly personalized treatments, fundamentally shifting the market dynamics away from symptomatic management.

North America commands the largest share of the Alopecia Drugs Market, primarily driven by high disposable incomes, sophisticated healthcare infrastructure, and significant patient awareness regarding treatment options. The region benefits from early and rapid adoption of novel, high-cost systemic therapies, such as the FDA-approved JAK inhibitors for alopecia areata. Furthermore, a high prevalence of androgenetic alopecia coupled with robust R&D investment by leading US-based pharmaceutical companies reinforces the region's market leadership. Favorable reimbursement scenarios and a strong regulatory environment supporting drug innovation also contribute to North America's dominance in terms of market value.

Europe represents the second-largest market, characterized by stringent regulatory standards (EMA) and strong academic research focused on dermatology. The market growth in major European economies like Germany, France, and the UK is propelled by increasing geriatric populations and favorable market access for established generic drugs. While adoption of highly expensive specialty drugs may be slower than in the US due to cost containment measures by national health systems, the increasing focus on patient quality of life and the established network of specialized dermatological clinics ensure steady, predictable growth.

The Asia Pacific (APAC) region is projected to be the fastest-growing market during the forecast period. This accelerated growth is primarily attributed to rapidly improving healthcare accessibility, vast population size, and rising health expenditure, particularly in China and India. Increased Westernization and changing lifestyles contribute to higher reported incidences of hair loss. Local manufacturers are expanding their generic portfolios of minoxidil and finasteride, making treatments affordable, while the adoption of branded specialty treatments is increasing rapidly among the affluent patient segment in developed APAC nations like Japan and South Korea, driving significant market expansion opportunities.

The primary driver is the rising global prevalence of chronic hair loss conditions, particularly androgenetic alopecia and the increasing incidence of alopecia areata, coupled with significant advancements and regulatory approvals for novel drug classes like JAK inhibitors.

JAK inhibitors are transformative, offering the first highly effective systemic oral treatments for moderate-to-severe alopecia areata by targeting the specific immune pathways responsible for hair follicle destruction, thereby shifting the standard of care from conventional immunosuppressants.

The Asia Pacific (APAC) region is projected to record the highest CAGR, driven by improving healthcare infrastructure, rising disposable incomes facilitating access to treatments, and a large, aging population base contributing to higher disease incidence.

Key restraints include the long duration of treatment necessary to observe results, high cost and limited reimbursement for newer specialty drugs, and patient adherence challenges often related to potential side effects or dissatisfaction with the speed of hair regrowth.

Technology is crucial in enhancing drug delivery through microneedle patches and nanocarriers for better topical absorption, and in accelerating R&D through AI for target identification and personalized medicine, leading towards future gene therapy and regenerative solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.