ID : MRU_ 436122 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

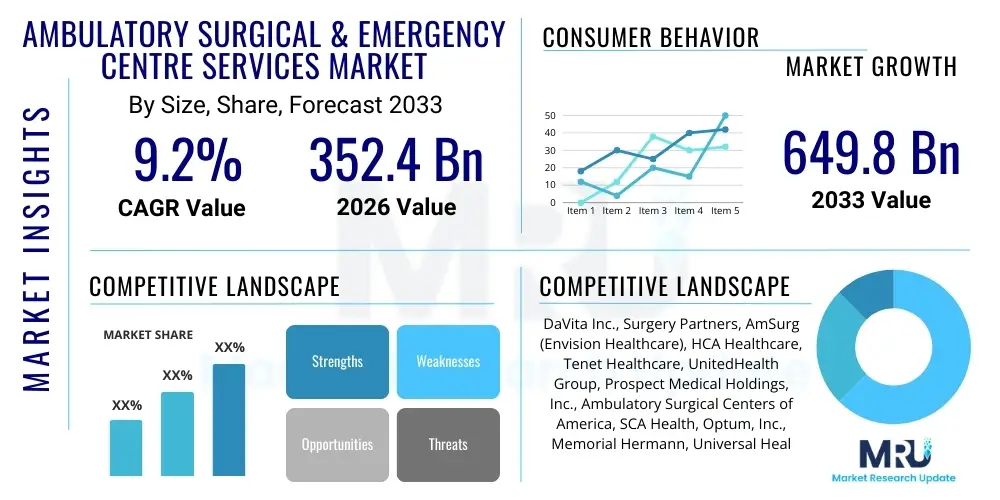

The Ambulatory Surgical & Emergency Centre Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2026 and 2033. The market is estimated at USD 352.4 Billion in 2026 and is projected to reach USD 649.8 Billion by the end of the forecast period in 2033. This robust expansion is primarily driven by the increasing global demand for cost-effective, high-quality, and minimally invasive surgical procedures performed in outpatient settings, coupled with significant technological advancements that enable complex procedures to move outside traditional inpatient hospital environments.

The Ambulatory Surgical & Emergency Centre Services Market encompasses facilities specifically designed to provide surgical procedures, diagnostic interventions, and acute emergency care that do not require an overnight hospital stay. These centers, often referred to as Ambulatory Surgical Centers (ASCs) or Urgent Care Centers (UCCs) providing emergency stabilization, are positioned as crucial alternatives to inpatient hospitals, offering enhanced convenience, reduced operational costs, and lower risks of hospital-acquired infections (HAIs). The core product of this market is the delivery of specialized, same-day surgical and emergency services across various specialties including orthopedics, ophthalmology, gastroenterology, and pain management. The efficiency inherent in the ASC model allows for quicker patient turnover and optimized resource utilization compared to traditional hospital settings, making them highly attractive to payers and patients alike.

Major applications of these services include cataract removal, endoscopic procedures, joint arthroscopy, and minor trauma care. The primary benefits driving market penetration are the reduced procedural costs, typically 40% to 60% lower than corresponding hospital services, and improved patient experience characterized by personalized care and faster recovery timelines. Furthermore, the shift towards value-based care models globally places a premium on high-quality, low-cost delivery settings, further cementing the role of ASCs. Driving factors propelling this market growth include the aging population requiring frequent surgical interventions, continuous technological innovation in surgical robotics and minimally invasive techniques, and favorable reimbursement policies supporting outpatient migration of procedures deemed safe for ambulatory settings.

The Ambulatory Surgical & Emergency Centre Services Market is undergoing a rapid transformative phase characterized by consolidation, technological integration, and a persistent shift in procedural volumes from inpatient to outpatient settings. Business trends indicate a strong move toward corporate and hospital system ownership, as larger entities seek economies of scale and leverage negotiating power with payers, leading to significant merger and acquisition activity across North America and Europe. Segment trends highlight that Orthopedics and Pain Management specialties are experiencing the fastest growth rates, driven by the rising prevalence of musculoskeletal disorders and chronic pain conditions necessitating outpatient interventions. Furthermore, the integration of advanced imaging and navigation systems within ASCs is expanding the scope of procedures that can be safely performed outside the traditional hospital environment, significantly enhancing service delivery efficiency.

Regional trends demonstrate North America's dominance, fueled by well-established reimbursement frameworks, high healthcare expenditure, and the presence of numerous specialized, highly efficient ASC networks. However, the Asia Pacific region is emerging as the fastest-growing market, propelled by increasing healthcare infrastructure investment, rising disposable incomes, and government initiatives aimed at expanding access to localized healthcare services, particularly in countries like China and India. The market dynamics are largely centered around maximizing throughput and optimizing the patient care pathway; therefore, successful operators are those that effectively manage supply chain costs, invest strategically in specialized medical equipment, and implement robust operational efficiency protocols.

User inquiries regarding the integration of Artificial Intelligence (AI) in the Ambulatory Surgical & Emergency Centre Services Market frequently focus on operational efficiency, predictive analytics for resource allocation, and enhancement of diagnostic accuracy. Key themes revolve around how AI can minimize wait times in emergency centers, optimize surgical scheduling to reduce facility downtime, and improve pre-operative risk stratification for ASC patients. Concerns often center on data privacy, the high initial investment required for AI infrastructure, and the validation of AI algorithms in diverse clinical settings. Users expect AI to revolutionize administrative tasks, potentially automating billing and coding processes, and anticipate its utility in real-time surgical guidance to enhance procedural outcomes and minimize complications, thereby reinforcing the reputation of ASCs as high-quality, low-risk options.

The implementation of AI algorithms is fundamentally altering workflow management within these centers. For instance, AI-driven scheduling tools can analyze historical data, predict no-show rates, and dynamically adjust appointment slots, leading to higher capacity utilization rates. In the clinical domain, machine learning models are increasingly being used to analyze patient vitals and imaging data quickly in emergency settings, aiding clinicians in rapid triaging and diagnosis of critical conditions. This technological transformation not only improves the patient experience by reducing bottlenecks but also provides administrators with powerful data-driven insights necessary for strategic expansion and quality assurance initiatives, solidifying the market's trajectory towards digitalization and enhanced operational rigor.

The Ambulatory Surgical & Emergency Centre Services Market is shaped by powerful synergistic forces encapsulated in its Drivers, Restraints, and Opportunities (DRO). Key drivers include the overwhelming pressure from payers (governments and private insurers) to migrate procedures out of expensive inpatient settings, coupled with significant advancements in minimally invasive surgical techniques that make complex operations feasible on an outpatient basis. Restraints predominantly involve stringent regulatory hurdles related to facility certification and accreditation, concerns over patient eligibility criteria for certain high-acuity procedures in non-hospital settings, and the ongoing challenge of securing adequate reimbursement parity with hospital outpatient departments (HOPDs). Opportunities are vast, centered around adopting advanced technologies like specialized robotics and telemedicine integration for pre- and post-operative care, and expanding market presence in underserved rural areas and emerging economies lacking robust centralized hospital infrastructure.

Impact forces in this market are heavily influenced by the competitive landscape and technological disruption. The shift towards value-based care models, where providers are reimbursed based on quality outcomes rather than volume, strongly favors the efficient, high-quality, focused delivery model of ASCs. Furthermore, consumer preference for convenience and cost transparency exerts significant pressure on traditional hospitals, forcing them to either partner with or replicate ASC service models. However, the scarcity of specialized clinical staff, particularly certified surgical nurses and anesthesiologists willing to work exclusively in an ambulatory setting, acts as a critical constraint that influences the scalability and operational capacity of these centers, necessitating continuous focus on workforce development and competitive compensation strategies across the industry.

The Ambulatory Surgical & Emergency Centre Services Market is analyzed across critical dimensions including Service Type, Specialty, and Ownership structure, providing a detailed view of the evolving service delivery ecosystem. Service Type segmentation distinguishes between highly planned surgical interventions and rapid response emergency services, with surgical services typically dominating revenue due to high procedure volumes in elective fields like ophthalmology and orthopedics. The Specialty segment allows for granular understanding of demand concentration, where procedures such as endoscopic gastrointestinal treatments and chronic pain injections represent significant growth vectors. Ownership structure dictates operational strategy, with large corporation-owned facilities leveraging standardized protocols and strong payer negotiations, while physician-owned facilities often offer highly specialized, localized expertise and greater procedural autonomy.

Understanding these segments is vital for stakeholders making investment decisions. For instance, the growing complexity of procedures being performed, enabled by advancements like specialized hybrid operating rooms within ASCs, necessitates targeted investment in specific specialties. Orthopedics remains a dynamic segment, continuously moving high-cost procedures like total joint replacement into the outpatient setting. Moreover, the segmentation based on ownership reflects varying degrees of integration into larger healthcare networks; corporation-owned ASCs are often integrated into broader health systems (e.g., Optum or HCA Healthcare), benefiting from centralized purchasing and administrative support, whereas physician-owned centers maintain agility but face higher administrative burdens and negotiating challenges with major insurers.

The value chain for Ambulatory Surgical & Emergency Centre Services is relatively streamlined compared to traditional hospital models, focusing heavily on efficiency from patient intake to post-discharge care. Upstream activities involve the procurement of highly specialized medical equipment, surgical instruments, pharmaceuticals, and essential medical supplies. Key suppliers include large medical device manufacturers and pharmaceutical companies. The negotiation power of ASCs, especially those under corporate ownership, is a critical determinant of operational costs in this phase. Maintaining optimal inventory levels and ensuring timely delivery of consumables are paramount to operational continuity and cost management, with many corporate chains implementing centralized purchasing organizations (CPOs) to maximize discounts and standardization.

Downstream activities center around the direct delivery of patient care, encompassing surgical procedures, anesthesia administration, recovery monitoring, and comprehensive patient education for post-operative management. Effective scheduling and minimizing turnover time between cases are vital for optimizing throughput and maximizing revenue capture. The distribution channel predominantly involves direct interaction with the patient (B2C) and crucial contractual relationships with insurance payers (B2B), who act as the primary source of revenue. Direct channels emphasize personalized patient engagement, quick administrative processes, and transparent pricing structures to enhance patient satisfaction and market competitiveness, while indirect channels rely on robust referrals from primary care physicians and specialists.

The primary customers of Ambulatory Surgical & Emergency Centre Services are multifaceted, encompassing the individual patients requiring outpatient procedures, the physicians who utilize the facilities, and the healthcare payers who contract with the centers. Individual patients, particularly the elderly population and those with chronic conditions manageable via elective surgery, are significant end-users seeking the cost-effectiveness, convenience, and low infection risk associated with ASCs. These patients prioritize centers offering specialized expertise, minimal wait times, and comprehensive post-care instructions, leading them to increasingly bypass large hospitals for non-complex procedures.

Healthcare payers, including large private insurance companies, government healthcare programs (Medicare/Medicaid in the US), and corporate self-insured plans, are pivotal customers. Their objective is to drive down the total cost of care while maintaining high-quality outcomes. ASCs represent a critical strategy for payers to achieve savings, leading to favorable reimbursement strategies and payer negotiations that steer patients toward ambulatory settings. Finally, the physicians themselves are key internal customers; ASCs compete to attract and retain specialized surgeons by offering high-quality equipment, efficient operational support, and flexible block time scheduling, enabling them to maximize their procedural output and professional satisfaction.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 352.4 Billion |

| Market Forecast in 2033 | USD 649.8 Billion |

| Growth Rate | 9.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DaVita Inc., Surgery Partners, AmSurg (Envision Healthcare), HCA Healthcare, Tenet Healthcare, UnitedHealth Group, Prospect Medical Holdings, Inc., Ambulatory Surgical Centers of America, SCA Health, Optum, Inc., Memorial Hermann, Universal Health Services, Inc. (UHS), IntegraMed America, Inc., Medical Facilities Corporation, ASD Management, Regent Surgical Health, Nueterra, Scope Health, Surgical Care Affiliates (SCA), Shields Health Solutions. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The operational and clinical efficiency of Ambulatory Surgical & Emergency Centres is fundamentally dependent on the integration of cutting-edge medical and digital technologies designed for high-throughput, outpatient settings. Key technological investments are concentrated in specialized surgical equipment, particularly high-definition endoscopy and laparoscopy systems that facilitate minimally invasive procedures, reducing recovery times and hospital stay requirements. Furthermore, advanced imaging modalities, such as mobile C-arms and localized MRI units, are becoming standard in specialized ASCs, enabling immediate intraoperative feedback and precision critical for procedures like orthopedic joint replacements and spine interventions. The necessity for quick and accurate diagnosis in emergency centers drives the adoption of advanced point-of-care testing (POCT) devices, offering rapid laboratory results essential for timely treatment decisions.

Beyond clinical tools, digital infrastructure forms the backbone of modern ASC and UCC operations. Electronic Health Record (EHR) systems optimized for outpatient workflows are essential for seamless patient data management, scheduling, and billing. There is a marked increase in the implementation of sophisticated Patient Management Software (PMS) that integrates online booking, patient portals for pre-operative instructions, and post-discharge follow-up via telemedicine platforms. Furthermore, the rising importance of cybersecurity technologies is recognized as crucial for protecting sensitive patient data (PHI) stored in interconnected digital systems, ensuring compliance with stringent regulatory standards like HIPAA and GDPR. The strategic integration of these technologies allows centers to operate efficiently, deliver high-quality outcomes, and remain competitive by maximizing both clinical safety and operational throughput.

The global Ambulatory Surgical & Emergency Centre Services Market exhibits distinct regional dynamics driven by varying regulatory environments, healthcare expenditure levels, and prevalence of specific medical conditions. North America, particularly the United States, commands the largest market share due to its mature ASC infrastructure, favorable commercial payer reimbursement landscape actively incentivizing outpatient migration, and the high concentration of key market players and physician expertise. The regulatory environment in the U.S. continually expands the list of procedures approved for the outpatient setting, further fueling growth. Within this region, the continued consolidation of independent ASCs into larger corporate networks remains a dominant trend, seeking optimization and strong negotiation leverage against private insurers.

Europe represents the second-largest market, characterized by significant variation across countries. Western European nations, supported by robust public health systems, are increasingly adopting ASC models to manage growing surgical backlogs and achieve cost efficiencies, with countries like Germany and the UK seeing steady growth. However, growth is often slower compared to the US due to heavier government regulation and typically lower reimbursement rates for private surgical services. Asia Pacific (APAC) is projected to be the fastest-growing region, driven by massive investments in private healthcare infrastructure in rapidly developing economies. Countries such as India and China are witnessing a surge in demand for affordable, accessible, and high-quality surgical services, making ASCs a viable solution to bridge the gap between overwhelmed public hospitals and rising patient expectations. This growth is significantly supported by medical tourism and the adoption of Western clinical protocols in private facilities.

The primary driver is the intense pressure from healthcare payers and consumers to reduce overall healthcare costs. ASCs offer high-quality services at significantly lower prices (often 40-60% less) than traditional inpatient hospitals, coupled with patient preference for quicker recovery and convenient, specialized settings, accelerating the migration of procedures to outpatient venues.

Orthopedics and Pain Management are seeing the fastest migration. Complex procedures, including total joint replacements (knee and hip), are increasingly performed in ASCs due to advancements in anesthesia, pain protocols, and minimally invasive techniques, ensuring patient safety and expedited recovery outside the hospital environment.

Technology, particularly advanced diagnostic tools and Electronic Health Records (EHRs), is critical. Rapid point-of-care testing (POCT) and AI-driven triage systems significantly reduce wait times and improve diagnostic accuracy in UCCs, optimizing patient flow and ensuring timely intervention for acute, non-life-threatening conditions.

The market is primarily segmented into Hospital-Owned/Joint Ventures, Physician-Owned, and Corporation-Owned facilities. Corporate ownership (e.g., SCA Health, Optum) is growing rapidly due to the ability to achieve economies of scale, centralized administrative support, and stronger contract negotiation power with national payers.

Major restraints include complex and varying state-level licensure requirements, stringent federal certification standards (e.g., Medicare certification for higher acuity procedures), and challenges associated with achieving reimbursement parity with hospital outpatient departments (HOPDs) for specific, newly migrated surgical codes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.