ID : MRU_ 435997 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

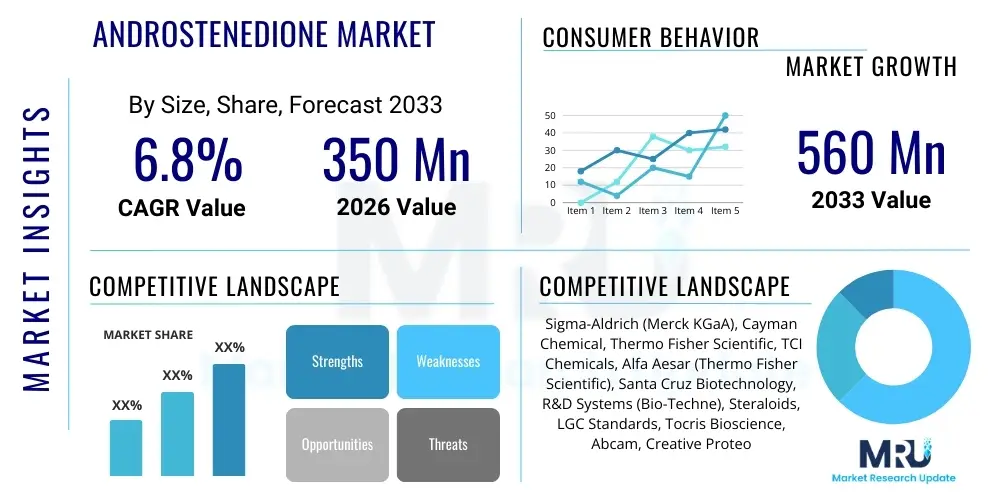

The Androstenedione Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 350 Million in 2026 and is projected to reach USD 560 Million by the end of the forecast period in 2033.

The Androstenedione market encompasses the global trade and utilization of the steroid hormone androstenedione (also known as 4-androstene-3,17-dione). This compound serves as a crucial biochemical intermediate in the steroidogenic pathway, acting as a direct precursor to testosterone and estrogens (estrone and estradiol). Its primary commercial applications revolve around the pharmaceutical industry, where it is vital for the synthesis of various steroidal drugs, including specialized contraceptives, corticosteroids, and hormone replacement therapies. The growing prevalence of endocrine-related disorders and the continuous need for innovative pharmaceutical treatments requiring steroid backbone synthesis are key factors driving market demand across major economies.

Product description highlights Androstenedione’s role as an endogenous androgen and its chemical importance, often synthesized commercially through microbial conversion of plant sterols like phytosterols or diosgenin, which offers a cost-effective and scalable production method compared to total chemical synthesis. Market growth is significantly impacted by stringent regulatory frameworks, particularly in regions like North America and Europe, which regulate its use due to its potential misuse as a performance-enhancing substance. Despite regulatory hurdles concerning over-the-counter sales, its essential nature as a pharmaceutical starting material ensures sustained demand, especially for research purposes and controlled drug manufacturing.

Major applications span hormone replacement therapy, treatment of hypogonadism, and its essential function in research laboratories investigating steroid metabolism, oncology, and endocrinology. Benefits derived from its use include providing a highly pure and necessary precursor for life-saving and quality-of-life-enhancing medications. Driving factors include advancements in biocatalysis for steroid production, expanding applications in veterinary medicine, and rising geriatric populations globally, necessitating increased hormone-based pharmaceutical interventions. Furthermore, the sustained investment in personalized medicine and targeted drug delivery systems utilizing steroid compounds further cements Androstenedione's critical market position.

The Androstenedione market demonstrates steady expansion, fundamentally driven by robust demand from the global pharmaceutical sector, which relies on this steroid backbone for synthesizing complex medications. Business trends indicate a strong move toward enhancing supply chain efficiency and investing heavily in biocatalytic synthesis methods to improve yield and sustainability, mitigating the risks associated with volatile raw material prices for plant sterols. Key market players are prioritizing collaborations with specialized biotech firms to secure proprietary fermentation and conversion technologies, thereby gaining a competitive edge in producing high-purity pharmaceutical grade Androstenedione. Furthermore, the trend toward vertical integration, where companies control both the extraction of precursors (like diosgenin) and the final conversion to Androstenedione, is becoming increasingly visible, aiming to stabilize pricing and quality control.

Regional trends reveal that the Asia Pacific (APAC) region, particularly China and India, is emerging as the dominant manufacturing hub, capitalizing on lower operational costs and the presence of established large-scale chemical and pharmaceutical production infrastructure. North America and Europe, while characterized by stringent regulations regarding consumer use, remain the primary consumption markets due to advanced healthcare systems, high research intensity, and significant demand for hormone replacement and cancer therapies. Growth in APAC is further fueled by the rising domestic pharmaceutical industries catering to massive internal healthcare needs and serving as global exporters of active pharmaceutical ingredients (APIs). Regulatory convergence initiatives globally are also impacting the market, pushing producers to adhere to stricter Good Manufacturing Practice (GMP) standards, especially when exporting to highly regulated markets.

Segmentation trends highlight that the High Purity Grade segment, essential for injectable and highly sensitive pharmaceutical applications, commands a significant revenue share and is projected to exhibit the fastest growth, driven by increasing regulatory demands for API purity. Application-wise, the Pharmaceuticals segment overwhelmingly dominates the market, dwarfing the Research and Dietary Supplements segments due to the consistent, high-volume requirement for drug synthesis. Within the Pharmaceuticals segment, specialized applications in oncology treatments utilizing steroid modulators and reproductive health medications are witnessing accelerated growth. Companies are increasingly focusing their R&D efforts on producing enantiomerically pure forms of Androstenedione, catering to specialized therapeutic needs and expanding the product portfolio beyond standard chemical intermediates.

Common user inquiries regarding AI in the Androstenedione market center on how artificial intelligence can accelerate drug discovery processes utilizing steroid compounds, particularly in identifying novel therapeutic targets where androstenedione or its derivatives might play a role. Users are also concerned about AI's potential in optimizing complex biochemical synthesis pathways, such as biocatalytic fermentation, to maximize yield and minimize impurities, thereby enhancing production efficiency and reducing costs. Furthermore, there is significant interest in AI's role in predictive modeling of market demand and regulatory compliance, especially concerning the complex and often contentious status of steroid hormones across different international jurisdictions. Key expectations include personalized dosing regimens enabled by AI analysis of patient endocrinological profiles and advanced quality control systems leveraging machine vision and deep learning to ensure the highest grade of API purity.

The application of Artificial Intelligence is poised to revolutionize several critical facets of the Androstenedione market, primarily through enhancing research and development efficiency and streamlining manufacturing operations. In R&D, AI algorithms are capable of analyzing vast datasets related to steroid-receptor interactions, predicting the binding affinity and metabolic fate of androstenedione derivatives with unprecedented speed. This accelerates the identification of viable drug candidates for conditions ranging from prostate cancer to hormone deficiency syndromes, reducing the time and cost traditionally associated with preclinical development. By simulating millions of potential chemical reactions and their outcomes, AI drastically improves the efficiency of identifying optimal synthetic routes, moving beyond traditional trial-and-error methodologies.

In the production landscape, AI and machine learning are being integrated into bioprocess engineering to optimize fermentation parameters critical for the microbial conversion of phytosterols into Androstenedione. Predictive maintenance models analyze sensor data from bioreactors to prevent deviations, ensuring consistent environmental conditions (pH, temperature, oxygen levels) that maximize microbial productivity and purity output. This advanced process control minimizes batch failures and reduces waste, offering substantial operational savings. Moreover, AI-driven demand forecasting tools assist manufacturers in managing complex global supply chains, anticipating fluctuating pharmaceutical needs, and ensuring just-in-time inventory management of this critical precursor, crucial for mitigating supply shocks related to raw material sourcing.

The dynamics of the Androstenedione market are shaped by a complex interplay of growth drivers stemming from pharmaceutical innovation, significant restraints primarily imposed by regulatory bodies and public perception, and emerging opportunities in specialized medical fields. Impact forces include intense competition among Asian manufacturers for cost leadership and the constant threat of substitution from chemically synthesized alternatives, though biological conversion remains the preferred method due to stereoselectivity advantages. The market’s sensitivity to global health trends, particularly the increasing lifespan and resulting demand for hormone therapies and anti-aging medications, provides consistent growth momentum, while ongoing enforcement actions against illicit dietary supplement use act as a constant brake on market expansion outside strictly controlled pharmaceutical channels.

Drivers include the continuous expansion of the global pharmaceutical industry, particularly in the production of corticosteroids, oral contraceptives, and specialized sex hormones where Androstenedione is an indispensable intermediate. Furthermore, technological advancements in fermentation processes and enzyme engineering have significantly reduced production costs and increased purity levels, making Androstenedione a more economically viable precursor. Restraints are predominantly centered on the strict regulatory classification of Androstenedione, often treated as a controlled substance or banned by major sports organizations (WADA/IOC), which severely limits its distribution and marketing, especially in the over-the-counter wellness segment. The public health controversy surrounding its historical misuse as a dietary supplement continues to cast a shadow, necessitating cautious market navigation and compliance overheads for legitimate producers.

Opportunities are arising from the burgeoning field of veterinary endocrinology, where Androstenedione derivatives are used for hormonal treatments in animals. The expansion of high-end research applications in metabolomics and oncology, requiring ultra-pure standards for analytical validation and clinical trials, also presents high-margin growth avenues. Impact forces such as environmental regulations affecting chemical processing and waste disposal in steroid manufacturing are increasingly important, pushing companies toward sustainable, green chemistry methods like advanced biocatalysis. Competitive intensity remains high, driven by the presence of large multinational chemical suppliers and specialized steroid manufacturers, demanding continuous process optimization and competitive pricing strategies to maintain market share.

The Androstenedione market is systematically segmented primarily based on Product Type (Purity Grade) and Application (End-use industries). Purity grade segmentation is crucial as pharmaceutical manufacturers demand extremely high purity levels (typically >99.5%) to meet stringent regulatory requirements for human injectable and oral medications, differentiating these high-value products from standard-grade materials used for basic research or intermediate chemical synthesis. The market’s structure reflects a value hierarchy where high-purity Androstenedione commands significant price premiums and is predominantly supplied by established, GMP-compliant Western and select Asian manufacturers, while standard grades are more commoditized.

Application segmentation clearly defines the primary revenue streams, with the Pharmaceuticals segment dominating due to its consistent, large-volume requirements for synthesizing downstream steroid drugs, including DHEA, Estrone, and various glucocorticoids. The research segment, though smaller in volume, is critical for innovation, requiring small batches of high-cost, specialized, and often custom-synthesized Androstenedione standards. The dietary supplements segment, though highly restricted in many major markets, still represents a niche demand in less regulated regions, contributing marginally to overall market size but facing significant regulatory headwinds that limit its long-term growth potential.

Understanding these segments allows market participants to tailor their production capabilities and marketing strategies effectively. For instance, companies targeting the pharmaceutical segment must invest heavily in quality control, facility validation, and global regulatory filing support, whereas those focusing on the research sector emphasize specialized synthesis capabilities and high technical support. The ongoing trend toward bioconversion methods further intersects with segmentation, as these methods often inherently produce higher-purity, stereospecific products desirable for the most lucrative pharmaceutical applications, reinforcing the shift towards premium grades.

The Androstenedione value chain begins with the upstream acquisition of natural sterols, primarily diosgenin sourced from yams (Dioscorea species) or phytosterols obtained from soybeans and other plant oils. This raw material supply phase is geographically concentrated, heavily relying on agricultural output from regions like Mexico, China, and specific parts of Africa, making the early stages of the supply chain susceptible to climate variability and geopolitical factors. The crucial step involves the extraction and purification of these sterol precursors, a chemical process requiring significant specialized equipment and expertise before the precursors are ready for conversion into Androstenedione. Efficiency at this stage dictates the purity and cost-effectiveness of the final product.

The midstream process is dominated by specialized steroid manufacturers who utilize complex microbial fermentation (biocatalysis) to convert the acquired sterols into Androstenedione, a highly technical and proprietary step. This conversion stage represents the highest value addition due to the required biological engineering expertise and the necessity for cGMP compliance. Downstream, the distribution channel is primarily direct from the manufacturer to large pharmaceutical companies (B2B), particularly for high-purity API use. For smaller volumes and research standards, indirect channels involving specialized chemical distributors (e.g., Sigma-Aldrich, Thermo Fisher) are utilized, ensuring global accessibility to research institutions and smaller biotech firms.

Direct sales dominate the high-volume pharmaceutical segment, fostering long-term supply agreements and requiring stringent auditing protocols to ensure API quality and consistent supply. Indirect distribution is vital for geographical reach and catering to fragmented demand from academic and non-pharmaceutical sectors, where distributors add value through inventory management, specialized packaging, and technical support. The entire chain is heavily scrutinized by regulatory agencies, especially concerning cross-border trade and end-use verification, which significantly increases transaction complexity and operational costs compared to generic chemical markets.

The primary consumers and end-users of Androstenedione are global pharmaceutical corporations and contract manufacturing organizations (CMOs) that synthesize a broad spectrum of steroidal drugs. These customers require bulk quantities of high-purity Androstenedione to serve as the critical starting material for synthesizing corticosteroids (used in anti-inflammatory and immunosuppressive therapies), estrogen and progestin compounds (used in oral contraceptives and HRT), and specialized hormonal antagonists used in oncology, particularly for breast and prostate cancer treatments. Their demand is highly inelastic and driven by global healthcare expenditure and regulatory approvals for new drug entities.

A secondary, yet crucial, customer base includes academic research institutions, government laboratories, and major analytical testing facilities. These entities typically purchase smaller, but higher-value, amounts of Androstenedione, often requiring isotope-labeled or ultra-pure analytical standards for conducting endocrinology studies, drug metabolism research, forensic toxicology, and quality control validation. Their purchasing decisions are primarily influenced by product purity, availability of specialized standards, and certification authenticity, rather than bulk pricing.

Furthermore, specialized veterinary pharmaceutical companies constitute a growing customer segment, utilizing Androstenedione derivatives for treating hormonal imbalances in livestock and companion animals, aligning with the rising global expenditure on animal health. The controlled segment of sports nutrition and specialty supplement manufacturers also represents a potential, albeit highly restricted and heavily scrutinized, customer group in jurisdictions where its use as a precursor is permitted under specific conditions, though this segment remains minor and high-risk due to enforcement pressures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350 Million |

| Market Forecast in 2033 | USD 560 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sigma-Aldrich (Merck KGaA), Cayman Chemical, Thermo Fisher Scientific, TCI Chemicals, Alfa Aesar (Thermo Fisher Scientific), Santa Cruz Biotechnology, R&D Systems (Bio-Techne), Steraloids, LGC Standards, Tocris Bioscience, Abcam, Creative Proteomics, Clearsynth Labs, Toronto Research Chemicals, Huateng Pharmaceutical, Diosynth (DSM), Shandong Xinhua Pharmaceutical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape for Androstenedione production is primarily defined by the shift from multi-step chemical synthesis toward highly efficient and stereoselective microbial bioconversion processes. Historically, the synthesis involved complex and environmentally taxing chemical reactions starting from cholesterol or other chemical precursors. Today, the leading technology utilizes specific strains of microorganisms, such as certain species of Mycobacterium or Bacillus, engineered to convert readily available plant sterols (like beta-sitosterol or diosgenin) directly into Androstenedione via fermentation. This biocatalytic route is favored because it often produces higher yields with fewer impurities, minimizing the need for harsh solvents and intensive purification steps, aligning with global green chemistry initiatives and lowering overall manufacturing costs substantially.

Advanced techniques within biocatalysis include enzyme immobilization and directed evolution, where researchers modify microbial enzymes to enhance their catalytic efficiency and specificity towards the desired sterol conversion step. Furthermore, process intensification technologies, such as continuous flow chemistry applied to the later purification stages, are being adopted to increase throughput and maintain consistent high quality, especially for pharmaceutical-grade APIs. These technologies are crucial for meeting the increasing regulatory pressure for quality, ensuring that the final product adheres to strict pharmacological purity standards while optimizing energy consumption during the complex fermentation cycle.

The digitalization of manufacturing, including the integration of Process Analytical Technology (PAT) and automation, represents another significant technological trend. PAT systems enable real-time monitoring of critical process parameters (CPPs) within the bioreactors, allowing for immediate adjustments to maintain optimal conditions for microbial activity, thereby reducing variability between batches. The adoption of analytical techniques such as High-Performance Liquid Chromatography (HPLC) coupled with Mass Spectrometry (MS) for impurity profiling is standard practice, ensuring that manufacturers can confidently verify the high purity essential for critical pharmaceutical applications, solidifying the technological barrier to entry for new market players.

The primary commercial use of Androstenedione is as a crucial chemical intermediate (API precursor) in the pharmaceutical industry for the high-volume synthesis of other essential steroids, including corticosteroids, estrogens, progestins, and certain specialized anti-cancer hormonal agents. This application significantly outweighs its smaller, regulated use in research or dietary supplements.

The main technological advancement driving the market is the widespread adoption of microbial bioconversion (biocatalysis), which utilizes engineered microorganisms to convert plant sterols (like diosgenin) into high-purity Androstenedione. This technique is more efficient, stereoselective, and environmentally sustainable than traditional multi-step chemical synthesis, leading to reduced production costs and enhanced API quality.

Asia Pacific, particularly China and India, dominates manufacturing due to cost efficiencies derived from lower operational expenses, extensive established chemical manufacturing infrastructure, and proximity to primary natural sterol sources (raw materials). These factors allow APAC manufacturers to produce high volumes of API precursors competitively for global export.

Major restraints include stringent global regulatory controls and the classification of Androstenedione as a controlled substance in many major economies (North America, Europe) due to its historical misuse in sports and dietary supplements. This regulatory environment creates high compliance costs, limits consumer access, and necessitates complex distribution tracking, hindering market expansion outside pharmaceutical applications.

Purity grade is critical; High Purity Grade Androstenedione (>99.5%) demands a significant price premium because it is mandatory for human pharmaceutical APIs, particularly for injectable or highly sensitive drug formulations requiring strict adherence to cGMP standards. Standard Grade products, used for less critical chemical synthesis or research, are typically priced lower due to less intensive purification and quality assurance requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.