ID : MRU_ 434324 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

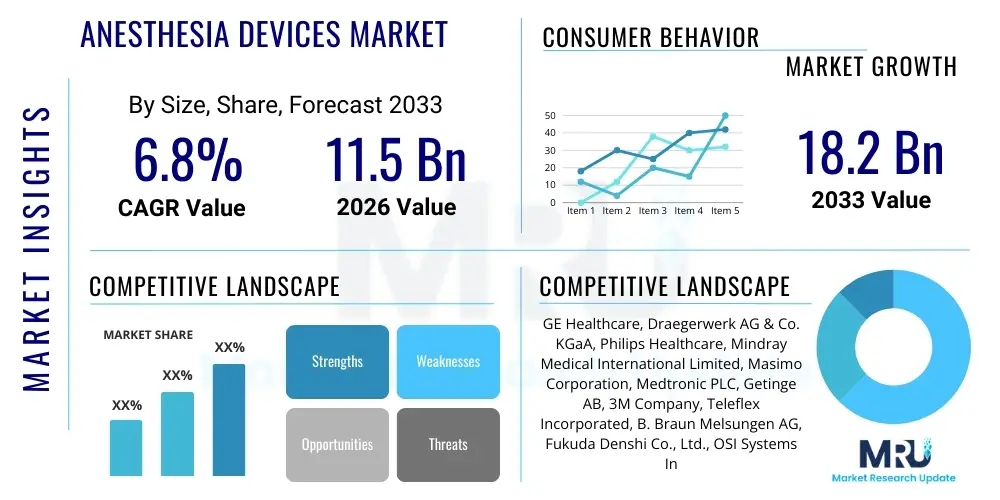

The Anesthesia Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 11.5 Billion in 2026 and is projected to reach USD 18.2 Billion by the end of the forecast period in 2033.

The Anesthesia Devices Market encompasses a wide range of medical equipment used for administering and monitoring anesthesia during surgical, diagnostic, and therapeutic procedures. This category includes highly sophisticated Anesthesia Delivery Systems (workstations), advanced patient monitoring equipment (measuring physiological parameters like oxygen saturation, end-tidal carbon dioxide, and anesthetic agent concentration), and essential consumables and accessories. The core function of these devices is to ensure patient safety, maintain optimal physiological stability, and provide controlled delivery of anesthetic agents, thereby facilitating complex medical interventions across various healthcare settings globally.

Major applications span critical areas such as general surgery, cardiovascular procedures, neurosurgery, orthopedic interventions, and outpatient dental or cosmetic surgeries. The increasing global burden of chronic diseases, coupled with a rapidly aging population requiring complex surgical care, significantly drives the demand for reliable and modern anesthesia technology. Furthermore, the shift towards minimally invasive procedures and the expansion of Ambulatory Surgical Centers (ASCs) necessitate portable, efficient, and integrated anesthesia solutions that enhance recovery times and reduce hospital stays, making sophisticated anesthesia devices indispensable components of modern perioperative care infrastructure.

Key driving factors accelerating market growth include continuous technological advancements, such as the integration of electronic records (EHRs), advanced ventilation modes, and closed-loop feedback systems that automate drug delivery based on patient feedback. The benefits derived from these devices—including improved accuracy in gas mixing, enhanced patient safety protocols, real-time physiological monitoring, and compliance with stringent international safety standards—solidify their central role in the healthcare continuum. Regulatory mandates emphasizing patient safety and the growing investment in high-quality healthcare infrastructure in emerging economies further catalyze market expansion.

The Anesthesia Devices Market is characterized by robust growth driven primarily by the escalating volume of surgical procedures worldwide and the continual upgrade cycle for advanced, feature-rich anesthesia workstations. Business trends indicate a strong focus among manufacturers on developing integrated systems that merge monitoring, ventilation, and data analytics capabilities, enhancing workflow efficiency and reducing the risk of human error. There is a palpable shift towards modular design and portability, catering specifically to the needs of rapidly proliferating Ambulatory Surgical Centers (ASCs) and critical care transport environments. Furthermore, stringent regulatory scrutiny, particularly in developed regions like North America and Europe, mandates the adoption of advanced monitoring technologies, creating a sustained demand for premium products that offer superior precision and safety features.

Regionally, North America maintains the dominant market share due to established reimbursement policies, high healthcare expenditure, and the presence of major industry players involved in continuous product innovation and research. However, the Asia Pacific (APAC) region is poised to exhibit the highest growth rate throughout the forecast period. This accelerated growth is attributed to massive investments in healthcare infrastructure development, the expansion of medical tourism, increasing awareness regarding patient safety during surgery, and the rising disposable incomes enabling greater access to advanced medical treatments in countries like China, India, and South Korea. Europe remains a steady market, focused on incorporating sustainable, low-flow anesthesia techniques to reduce operational costs and environmental impact.

Segment trends highlight the dominance of Anesthesia Delivery Systems (workstations) within the product type category, primarily due to their high capital cost and necessity in almost all surgical settings. Within the End-User segment, Hospitals are the largest consumer, though Ambulatory Surgical Centers (ASCs) are the fastest-growing segment, reflecting the broader trend of shifting surgical volume to outpatient settings. The increasing adoption of advanced monitoring technologies, particularly those measuring Depth of Anesthesia (DOA), underscores the segmentation focus on improving patient outcomes and preventing intraoperative awareness, driving innovation in both hardware and sophisticated analytical software integrated into these devices.

Common user inquiries concerning the impact of Artificial Intelligence (AI) on the Anesthesia Devices Market frequently revolve around the potential for autonomous drug delivery systems, the role of predictive analytics in risk management, and the integration of machine learning into real-time patient monitoring. Users express both anticipation for enhanced safety features and concern regarding the regulatory pathway and reliability of AI-driven closed-loop systems. Key themes analyzed include how AI can reduce workload for anesthesiologists, personalize anesthesia protocols based on complex patient data (comorbidities, genetics), and minimize the incidence of critical events such as hypotension or hypoxic episodes. The overarching expectation is that AI will transform anesthesia delivery from a reactive process to a proactive, predictive discipline.

The implementation of AI algorithms is primarily focused on optimizing drug titration and ventilation settings. For instance, Machine Learning (ML) models are being trained on vast datasets of physiological responses to recommend precise dosages of anesthetic agents and muscle relaxants, moving beyond traditional weight-based calculations to truly personalized medicine. This not only enhances therapeutic efficacy but also significantly reduces drug consumption and associated costs. Furthermore, AI contributes substantially to sophisticated alarm management systems, differentiating between critical events requiring immediate intervention and benign physiological fluctuations, thereby reducing alarm fatigue among clinical staff.

The long-term impact of AI will revolutionize perioperative care by providing comprehensive predictive risk assessment tools, allowing clinicians to anticipate hemodynamic instability or delayed emergence from anesthesia hours before symptoms manifest. This transition shifts the focus from managing complications to preventing them entirely, necessitating advanced Anesthesia Information Management Systems (AIMS) capable of handling, processing, and interpreting the massive data streams generated by contemporary anesthesia devices. Regulatory bodies are currently focused on establishing guidelines for the safe and ethical deployment of these autonomous and semi-autonomous AI-driven systems within critical care environments.

The Anesthesia Devices Market is propelled by significant drivers, predominantly the global surge in surgical procedure volumes, an expanding elderly demographic requiring specialized anesthetic care, and continuous technological migration towards integrated, intelligent monitoring systems. These factors create robust, sustained demand for advanced capital equipment and associated consumables. Simultaneously, market growth is restrained by the high initial cost of modern anesthesia workstations, which presents a significant barrier to adoption, particularly in lower-income settings and small-to-mid-sized healthcare facilities. Furthermore, stringent and complex regulatory approval processes often lengthen product commercialization cycles, potentially slowing the pace of innovation diffusion across all major geographic regions.

Opportunities within this dynamic market revolve around the development and penetration of affordable, portable, and ruggedized anesthesia solutions specifically tailored for mobile healthcare units and emerging markets facing infrastructure constraints. The growing trend toward personalized medicine creates an opportunity for specialized monitoring devices focusing on neuromuscular blockade monitoring and depth of anesthesia sensors, ensuring higher precision in drug effects. Furthermore, manufacturers focusing on interoperability and seamless integration with existing Hospital Information Systems (HIS) and Electronic Health Records (EHR) stand to gain substantial competitive advantages through improved clinician workflow efficiencies.

The principal impact force shaping the market trajectory is the increasing emphasis on patient safety mandates and standardized care protocols enforced by international bodies like the World Health Organization (WHO) and regional regulatory agencies. These mandates compel healthcare providers to phase out older, less reliable equipment and invest in advanced monitoring capabilities, thereby accelerating the replacement cycle of capital equipment. Additionally, fierce competitive rivalry among key market players, driven by rapid technological iteration (e.g., electronic gas mixing, advanced ventilation modes), forces continuous product enhancement and strategic pricing adjustments to maintain market share, influencing overall pricing and feature availability across the device spectrum.

The Anesthesia Devices Market is extensively segmented across multiple dimensions, primarily defined by the product type, end-user settings, and specific application areas. The segmentation allows manufacturers to tailor their product offerings—ranging from complex, high-end integrated workstations designed for tertiary care hospitals to simple, cost-effective portable units suitable for ASCs or rural clinics. Understanding these segments is crucial for strategic market penetration, as the purchase criteria, budget constraints, and technological requirements vary significantly between segments, influencing the sales velocity and adoption rates of new technologies across the healthcare landscape.

Product type segmentation reflects the technological complexity and intended use, differentiating between capital equipment (delivery systems and monitors) and high-volume consumables (masks, breathing circuits, disposable CO2 absorbers). The end-user analysis provides insights into the primary purchasing power, with hospitals representing the largest segment due to the high volume of complex surgeries performed, while the rapid expansion of Ambulatory Surgical Centers (ASCs) signals a shift towards demand for smaller, more efficient, and faster-turnaround devices. Geographically, segmentation provides a critical view of regulatory harmonization, technological maturity, and purchasing capabilities across developed and emerging economies, dictating global market strategy and resource allocation.

The value chain for the Anesthesia Devices Market begins with upstream activities focused on the sophisticated design, research, and development of core components, including proprietary sensors, specialized software algorithms, and high-precision gas delivery mechanics. This stage is dominated by specialized component suppliers who provide critical technologies such as mass spectrometers, electronic gas mixers, and high-resolution display units. Intellectual property (IP) protection and technological expertise form the foundation of competitive advantage upstream, dictating the innovation potential of the final product. Manufacturers then engage in intricate assembly, rigorous testing, and quality assurance processes to comply with global medical device standards (e.g., FDA, CE Mark), which are capital-intensive and highly regulated steps.

Downstream activities center around efficient logistics, specialized distribution channels, and comprehensive post-sale support. Given the complexity and capital nature of anesthesia equipment, direct distribution channels, involving the manufacturer's own highly trained sales and technical teams, are frequently employed, particularly for high-end workstations sold to major hospital networks. This allows for direct negotiations, comprehensive training, and tailored maintenance contracts. However, indirect channels, utilizing regional distributors or third-party logistics providers, are crucial for reaching smaller clinics, remote markets, and efficiently delivering high-volume, low-margin consumables. The after-sales service, including calibration, repair, and software updates, constitutes a significant revenue stream and directly influences customer loyalty and market reputation.

The crucial element linking manufacturing to end-users is the specialized nature of the sales process, which requires deep clinical knowledge on the part of the sales force to communicate the device's clinical benefits and economic value proposition (e.g., reduced anesthetic agent consumption via low-flow capabilities). Effective distribution channels must manage complex inventory, particularly for disposable components, while ensuring the timely delivery of capital equipment. Direct distribution provides manufacturers maximum control over pricing and customer relationships, whereas indirect distribution allows for scalability and rapid market penetration in regions where established local networks are necessary, highlighting the strategic importance of balancing both models within a globalized market structure.

The primary end-users and potential customers of Anesthesia Devices are institutional purchasers within the healthcare ecosystem, characterized by structured procurement processes, high budgetary allocations, and strict adherence to clinical standards. Hospitals, encompassing large public university systems, tertiary care centers, and private multi-specialty facilities, represent the largest and most foundational customer base due to the high volume and complexity of surgical cases requiring round-the-clock anesthesia services. These institutions demand technologically advanced, fully integrated workstations capable of handling critically ill and complex patient profiles, driving the market for premium products and comprehensive service contracts.

The fastest-growing segment of potential customers includes Ambulatory Surgical Centers (ASCs) and specialized outpatient clinics (e.g., plastic surgery, dental maxillofacial surgery). ASCs prioritize efficiency, rapid patient turnover, and cost containment, favoring modular, space-saving, and highly reliable mid-range anesthesia systems and monitors that facilitate streamlined workflows. This segment seeks devices that are easy to maintain and require minimal footprint, offering significant growth potential for manufacturers specializing in portable and user-friendly technology tailored for outpatient settings where capital budgeting is often tighter than in large hospitals.

Furthermore, government and non-governmental organizations involved in global health initiatives, military healthcare, and research institutions constitute secondary, yet significant, customer segments. These organizations often require ruggedized, mobile anesthesia solutions suitable for challenging environments or disaster relief efforts. Academic and research centers also function as key buyers, prioritizing cutting-edge technology for clinical trials, teaching, and developing new anesthetic techniques, often driving the early adoption of highly specialized monitoring tools like advanced depth of anesthesia sensors and continuous cardiac output monitoring capabilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 18.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | GE Healthcare, Draegerwerk AG & Co. KGaA, Philips Healthcare, Mindray Medical International Limited, Masimo Corporation, Medtronic PLC, Getinge AB, 3M Company, Teleflex Incorporated, B. Braun Melsungen AG, Fukuda Denshi Co., Ltd., OSI Systems Inc., Schiller AG, Heyer Medical AG, Penlon Ltd., Northern Meditec Limited, Amsino International Inc., SunMed LLC, Vyaire Medical, Inc., Intersurgical Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Anesthesia Devices Market is rapidly evolving, moving away from conventional mechanical gas mixers toward sophisticated electronic flow control and fully integrated workstations that offer advanced ventilation capabilities, traditionally found only in dedicated Intensive Care Unit (ICU) ventilators. A major technological focus is the adoption of minimally invasive and low-flow anesthesia techniques, facilitated by precise electronic mixers and vaporizers, which significantly reduce the consumption of expensive volatile agents, offering substantial economic benefits and reducing the environmental footprint of anesthetic gases. Furthermore, advancements in digital connectivity enable seamless integration with hospital IT networks (AIMS/EHR), facilitating data capture, analysis, and compliance reporting.

A second critical technological pillar is the enhancement of patient monitoring accuracy and depth. There is a concerted effort to develop and standardize depth of anesthesia (DOA) monitoring systems (e.g., BIS, Entropy) to prevent intraoperative awareness, coupled with robust neuromuscular transmission monitoring (NMT) to ensure complete reversal of muscle relaxants post-surgery, thereby minimizing residual paralysis risk. These monitoring systems often utilize advanced digital signal processing and machine learning algorithms to interpret complex physiological data in real-time, providing actionable insights to the anesthesia provider and improving patient outcomes during emergence and recovery phases.

The emergence of Closed-Loop Anesthesia Delivery (CLAD) systems represents the frontier of technological innovation. CLAD systems utilize real-time patient feedback (such as DOA indices or blood pressure) to autonomously adjust the concentration of anesthetic agents and vasopressors, aiming for fully automated, precision anesthesia maintenance. While still facing regulatory hurdles and requiring constant human oversight, these systems promise unprecedented levels of titration accuracy, workload reduction, and highly stable physiological control. Parallel advancements in portability, driven by powerful battery technology and miniaturized components, are enabling high-fidelity anesthesia delivery in increasingly diverse settings, including field hospitals and remote surgical suites.

The primary drivers are the increasing global volume of complex surgical procedures, the necessity for enhanced patient safety mandated by global healthcare bodies, and technological integration of advanced monitoring features (e.g., closed-loop drug delivery) that improve clinical precision and efficiency in operating rooms and ambulatory centers.

ASCs are the fastest-growing end-user segment. They significantly influence demand for cost-efficient, compact, and rapidly deployable anesthesia equipment suitable for outpatient procedures, favoring mid-range systems that prioritize quick setup, reliability, and minimal maintenance costs over complex, high-end features.

Key technological trends include the integration of Artificial Intelligence (AI) for predictive monitoring and automated drug titration (Closed-Loop Systems), the widespread adoption of low-flow anesthesia techniques for cost and environmental benefits, and enhanced patient monitoring, especially Depth of Anesthesia (DOA) and Neuromuscular Transmission (NMT) monitoring.

Manufacturers face rigorous and lengthy regulatory approval processes, particularly under the EU Medical Device Regulation (MDR) and FDA requirements. These regulations demand extensive clinical validation, robust cybersecurity protocols for connected devices, and stringent post-market surveillance, increasing the time and cost associated with product commercialization.

The Asia Pacific (APAC) region, specifically emerging economies like China and India, offers the highest compound annual growth rate (CAGR). This growth is supported by substantial government investment in healthcare infrastructure expansion, rising medical tourism, and increasing patient disposable income leading to higher demand for modern surgical care facilities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.