ID : MRU_ 434915 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

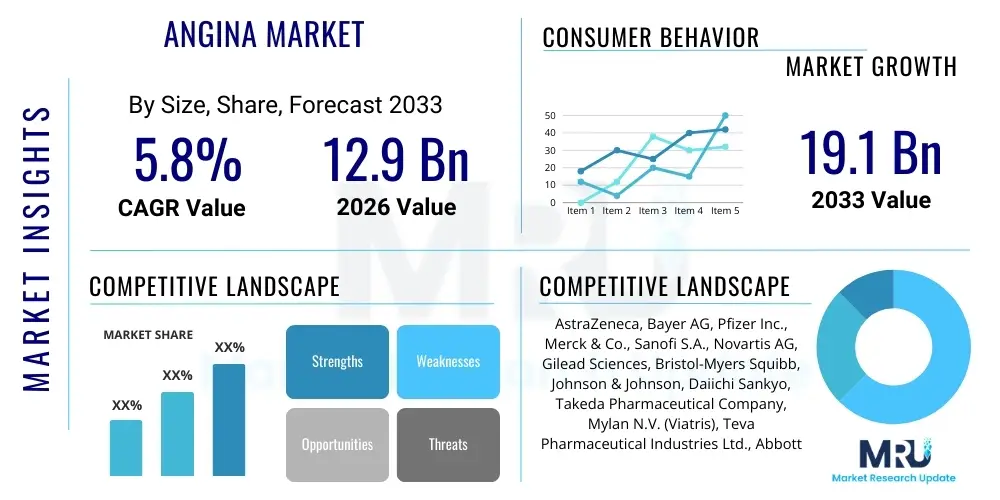

The Angina Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 12.9 Billion in 2026 and is projected to reach USD 19.1 Billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by the escalating global incidence of coronary artery disease (CAD), for which angina pectoris is a primary symptomatic manifestation. Furthermore, advancements in diagnostic technologies and the introduction of novel anti-anginal drugs with improved efficacy and fewer side effects contribute significantly to market expansion.

The valuation reflects robust demand for both traditional pharmaceuticals, such as nitrates and beta-blockers, and newer, more targeted therapeutic agents designed to improve myocardial perfusion or reduce cardiac workload. Increased healthcare expenditure in emerging economies and enhanced public awareness regarding cardiovascular health management also play pivotal roles in bolstering market size. The stable angina segment, being the most common form, accounts for the largest market share, but the focus on early diagnosis and management of unstable angina drives higher revenue per case in specialized treatment centers.

The Angina Market encompasses pharmaceutical and medical device sectors dedicated to the diagnosis, management, and treatment of angina pectoris, a clinical syndrome characterized by chest discomfort due to myocardial ischemia, typically caused by coronary artery disease. Key products include various drug classes such as nitrates, beta-adrenergic blocking agents, calcium channel blockers, and novel anti-ischemic agents like Ranolazine and Ivabradine. Major applications revolve around symptomatic relief, prevention of acute myocardial infarction, and enhancement of patient quality of life. The primary benefits offered by these treatments are the reduction of pain frequency and severity, improved exercise tolerance, and reduced hospitalization rates. Driving factors for market growth include the aging population susceptible to cardiovascular diseases, the global rise in lifestyle-related risk factors such as obesity and diabetes, and continuous innovation in drug delivery systems ensuring patient compliance and effectiveness.

The Angina Market is poised for steady growth, characterized by significant business trends focusing on personalized medicine and combination therapies. Pharmaceutical companies are heavily investing in Phase III trials for second-line anti-anginal treatments that offer improved hemodynamic profiles. Regional trends indicate that North America and Europe currently dominate the market due to high healthcare spending and early adoption of premium pharmaceuticals, while the Asia Pacific region is expected to exhibit the highest growth rate, driven by a large patient pool and improving healthcare infrastructure. Segment trends highlight a shift towards novel anti-anginal drugs, which, despite being expensive, are preferred for patients refractory to standard treatments. Furthermore, the market for diagnostic devices, particularly stress tests and advanced imaging technologies used to confirm coronary artery disease severity, remains a strong and consistent revenue stream supporting treatment decisions and driving overall market dynamics.

User queries regarding the impact of Artificial Intelligence (AI) in the Angina Market frequently center on its ability to revolutionize diagnosis, personalize treatment protocols, and accelerate drug discovery. Common concerns include the accuracy of AI-driven diagnostic tools in diverse patient populations and the integration cost into existing hospital systems. Users expect AI to significantly enhance the early detection of underlying coronary artery disease by analyzing complex electrocardiogram (ECG) data, cardiac imaging results (CT, MRI), and patient biomarkers far more efficiently than traditional methods. Furthermore, there is high anticipation for AI algorithms to predict patient response to various anti-anginal medications, allowing clinicians to tailor drug combinations and dosages, thereby minimizing side effects and optimizing therapeutic outcomes, particularly in complex cases like microvascular angina. The overarching theme is that AI will shift the treatment paradigm from reactive management to proactive, predictive cardiovascular care, leading to substantial improvements in patient morbidity and mortality rates related to ischemic heart disease.

The integration of deep learning and machine learning models within cardiovascular medicine is fundamentally reshaping how angina is approached, moving beyond conventional risk stratification. These technologies are capable of processing vast datasets, including electronic health records and genomic information, to identify previously unrecognized patterns associated with the progression of CAD and the onset of angina symptoms. This enhanced analytical capability is not only accelerating the preclinical phase of drug development by predicting compound efficacy and toxicity but is also optimizing the design and recruitment phases of clinical trials for anti-anginal agents, ensuring that new treatments reach the market faster and are targeted towards the most responsive patient demographics. Consequently, AI is becoming an indispensable tool for maximizing therapeutic precision and efficiency across the entire care continuum for angina patients.

The dynamics of the Angina Market are heavily influenced by a confluence of accelerating drivers (D), significant restraints (R), and compelling opportunities (O), collectively acting as strong impact forces. Key drivers include the global proliferation of cardiovascular risk factors such as sedentary lifestyles, hyperlipidemia, and hypertension, which increase the incidence of coronary artery disease and subsequent angina episodes. Furthermore, improvements in healthcare access and diagnosis globally, particularly in developed regions, ensure that more patients are identified and prescribed appropriate anti-anginal medications. These drivers are fundamentally linked to demographic shifts, notably the rapidly expanding geriatric population, which has a higher propensity for chronic cardiac conditions requiring long-term pharmacological management, thus sustaining market demand and necessitating continuous innovation.

Conversely, the market faces notable restraints, primarily the high cost associated with innovative, patented anti-anginal drugs, leading to accessibility issues in lower-income settings and prompting generic substitution in established markets. Additionally, the prevalence of adverse side effects associated with certain drug classes (e.g., hypotension from nitrates, bradycardia from beta-blockers) can lead to non-compliance or discontinuation of therapy, limiting the effective patient base. The threat of patent expiration for blockbuster drugs also imposes downward pressure on pricing, impacting the revenue streams of major pharmaceutical entities. These factors require strategic market management, including the development of better-tolerated formulations and robust patient support programs to mitigate restraint impacts.

The primary opportunities lie in the development of third-generation anti-anginal agents with novel mechanisms of action, specifically targeting microvascular angina or endothelial dysfunction, conditions that remain inadequately addressed by current standard treatments. The growing acceptance of combination therapies and fixed-dose combinations (FDCs) offers benefits in terms of patient compliance and synergistic efficacy, presenting a strong commercial avenue. Moreover, the integration of advanced monitoring technologies, such as wearable devices for continuous symptom tracking and remote patient management, represents a substantial technological opportunity to improve patient outcomes and optimize therapeutic adjustments, thereby expanding the utility and value proposition of anti-anginal treatments in the long-term management of cardiovascular disease.

The Angina Market is meticulously segmented based on several critical parameters, including the type of angina, the class of drug utilized for treatment, and the major distribution channels employed to reach end-users. Understanding these segments is crucial for strategic market positioning and resource allocation. The segmentation by angina type—primarily stable, unstable, and microvascular—determines the urgency and complexity of treatment, directly influencing market volume and revenue per patient. Stable angina, managed primarily by pharmacological agents and lifestyle adjustments, constitutes the largest segment, while the treatment of unstable angina drives higher expenditure on critical care and interventional procedures, including angiography and stenting, which indirectly support the pharmaceutical market for immediate stabilization and post-procedural recovery. The complexity of treating microvascular angina, often requiring novel approaches, presents a high-growth niche.

Segmentation by drug class reflects the standard of care guidelines established by major cardiac societies. The first-line therapies (beta-blockers and calcium channel blockers) maintain high volume due to their established efficacy and generic availability. However, the rapidly expanding segment of novel anti-anginal drugs (e.g., metabolic modulators, late sodium channel blockers) commands premium pricing and is crucial for patients unresponsive to conventional treatment, serving as a primary driver of market value growth. Furthermore, the segmentation across distribution channels—hospital pharmacies, retail pharmacies, and online channels—reveals shifting purchasing patterns. Hospital pharmacies dominate the unstable angina segment due to immediate need and acute management, whereas retail and online pharmacies are primary channels for chronic, long-term medication dispensing for stable angina patients, benefiting from increased accessibility and convenience, especially for repeat prescriptions.

The value chain for the Angina Market is intricate, beginning with intense upstream activities focused on pharmaceutical research and development (R&D) and clinical trials. Upstream analysis involves the discovery and synthesis of active pharmaceutical ingredients (APIs), which are often complex processes demanding significant capital investment and specialized scientific expertise to identify molecules targeting myocardial ischemia. Key upstream players include specialized biotech firms and large pharmaceutical companies collaborating with academic institutions. Quality control and regulatory compliance during the API manufacturing phase are paramount, setting the foundation for product efficacy and safety. The efficiency of R&D directly determines the introduction of breakthrough anti-anginal therapies, significantly impacting the market's competitive structure and pricing power.

The downstream analysis focuses on the transformation of APIs into finished dosage forms (tablets, capsules, injections) through highly regulated manufacturing processes, followed by packaging and distribution. Distribution channels play a critical role, involving a multi-tiered network of wholesalers, distributors, hospital systems, and retail outlets. Direct channels include sales forces targeting cardiologists and primary care physicians, particularly for newly launched, patented products that require specialized promotion and education regarding their clinical benefits. Indirect channels, primarily relying on wholesalers and pharmacy networks, handle the high-volume distribution of generic and established anti-anginal drugs, ensuring widespread availability across diverse geographic regions and facilitating efficient inventory management within the complex healthcare supply chain.

The primary end-users and buyers in the Angina Market are diverse, ranging from specialized healthcare facilities to individual patients and government procurement agencies. Hospitals and acute care centers represent critical immediate customers, especially for managing unstable angina and administering intravenous or high-dose therapies during acute ischemic events. Cardiology clinics and specialized cardiac care centers are major buyers of prescription drugs for long-term maintenance therapy for patients with stable angina, driving consistent demand for established and novel anti-anginal agents. Furthermore, integrated health systems and managed care organizations act as significant purchasers, often negotiating bulk discounts for formulary inclusion of preferred drugs to manage large patient populations diagnosed with Coronary Artery Disease (CAD).

Retail pharmacies and mail-order services serve as the direct point of contact for individual patients purchasing medications for chronic use, making them essential components of the downstream market. Governments and public health organizations, particularly in countries with centralized healthcare systems, are substantial bulk buyers, often driven by cost-effectiveness metrics to supply essential anti-anginal drugs through public healthcare programs. Physicians (cardiologists and general practitioners) act as key influencers, determining the prescription volume and class of drugs purchased. Ultimately, the end-user base is characterized by chronic medication dependency, ensuring a steady, long-term revenue stream for market participants, provided patient compliance and therapeutic adherence remain high.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 12.9 Billion |

| Market Forecast in 2033 | USD 19.1 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AstraZeneca, Bayer AG, Pfizer Inc., Merck & Co., Sanofi S.A., Novartis AG, Gilead Sciences, Bristol-Myers Squibb, Johnson & Johnson, Daiichi Sankyo, Takeda Pharmaceutical Company, Mylan N.V. (Viatris), Teva Pharmaceutical Industries Ltd., Abbott Laboratories, Hikma Pharmaceuticals, GlaxoSmithKline (GSK), Eisai Co., Ltd., Servier Laboratories, Eli Lilly and Company, Actavis (Teva). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Angina Market is defined by continuous innovation in both pharmaceutical formulation and diagnostic capabilities aimed at optimizing patient outcomes. In pharmaceuticals, advancements focus on creating sustained-release and extended-release formulations of established drugs like nitrates and beta-blockers. These technologies improve drug pharmacokinetics, ensure stable plasma concentrations over 24 hours, and significantly enhance patient compliance by reducing the dosing frequency, thus overcoming a major limitation of older therapies. Furthermore, the use of novel drug delivery systems, such as transdermal patches or biodegradable implants, is explored for specific high-risk patient segments to provide consistent anti-ischemic protection, minimizing the risk of symptom breakthrough, particularly during high-stress periods or physical exertion.

Beyond drug formulation, diagnostic technology plays a critical supportive role. Non-invasive imaging techniques are essential for confirming the presence and severity of coronary artery disease, which underlies most angina cases. High-resolution computed tomography angiography (CCTA) and cardiac magnetic resonance imaging (CMRI) offer superior visualization of coronary arteries and myocardial viability compared to conventional angiography, allowing for more precise treatment planning, distinguishing between stable and unstable plaques, and guiding revascularization decisions. These technologies are increasingly integrated with functional testing, such as stress echocardiography and stress nuclear perfusion imaging, to assess the hemodynamic significance of arterial stenoses. The fusion of imaging and functional assessment, often enhanced by AI analysis, forms the cutting-edge technology that drives diagnostic accuracy and ultimately shapes the therapeutic strategies adopted in the Angina Market, increasing the demand for sophisticated cardiac equipment in both hospital and specialized clinic settings.

The market is primarily driven by the escalating global prevalence of coronary artery disease (CAD), the growth of the geriatric population, increased awareness leading to earlier diagnosis, and continuous innovation in sustained-release drug formulations and novel anti-ischemic agents like Ranolazine and Ivabradine, which offer improved efficacy profiles.

Key segmentation by drug class includes Nitrates (to relieve acute symptoms), Beta-Blockers and Calcium Channel Blockers (first-line prophylactic therapy to reduce cardiac workload), and Novel Anti-anginal Agents (second-line therapies targeting metabolic pathways or specific ion channels for refractory cases).

Technological advancements include high-resolution non-invasive cardiac imaging (CCTA and CMRI) for precise diagnosis, the development of fixed-dose combination (FDC) pharmaceuticals for enhanced patient compliance, and the integration of AI for personalized therapeutic recommendations and accelerated drug discovery processes, particularly in complex angina types.

North America currently holds the largest market share, attributed to its advanced healthcare infrastructure, high reimbursement rates for specialized cardiac procedures and patented medications, and a high incidence of cardiovascular disease supported by robust patient monitoring and management systems.

Therapeutic options for refractory angina, defined as persistent symptoms despite maximum conventional therapy, include novel pharmacological agents (e.g., Ranolazine, Trimetazidine), spinal cord stimulation, Enhanced External Counterpulsation (EECP), and, in rare, highly selected cases, specialized surgical interventions like Transmyocardial Laser Revascularization (TMLR).

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.