ID : MRU_ 435014 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

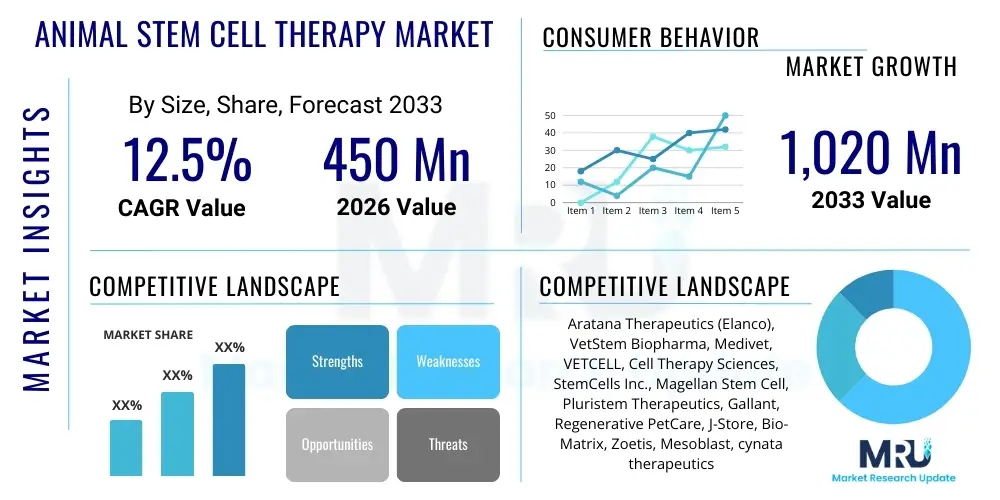

The Animal Stem Cell Therapy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 1,020 Million by the end of the forecast period in 2033.

This robust growth trajectory is primarily fueled by the increasing pet ownership globally and the subsequent rise in awareness regarding advanced veterinary care options. Stem cell therapy, leveraging regenerative medicine principles, offers promising solutions for chronic conditions like osteoarthritis, tendon injuries, and spinal cord ailments in companion animals, particularly dogs and horses. The non-invasive nature and superior efficacy compared to conventional treatments are major adoption drivers.

Furthermore, advancements in stem cell sourcing techniques, including allogeneic and autologous approaches, coupled with regulatory approvals for specific veterinary applications, contribute significantly to market expansion. Investment in clinical research aimed at optimizing dosage protocols and expanding the therapeutic scope across various animal species is expected to maintain the high growth momentum throughout the forecast period.

The Animal Stem Cell Therapy Market encompasses the research, development, production, and distribution of biological therapeutics utilizing stem cells for the treatment of diseases and injuries in livestock and companion animals. This advanced veterinary segment focuses on harnessing the regenerative potential of mesenchymal stem cells (MSCs) derived primarily from adipose tissue, bone marrow, or umbilical cord blood. These products are crucial for promoting tissue repair, reducing inflammation, and modulating immune responses in animals suffering from degenerative conditions or acute trauma. Major applications span orthopedic conditions such as arthritis and ligament injuries, neurological disorders, renal failure, and ophthalmic diseases. The primary benefits include faster recovery times, minimized reliance on long-term pharmacological intervention, and improved quality of life for animals. Driving factors include rising disposable income leading to increased expenditure on pet health, technological standardization in cell culture and delivery, and a growing veterinary specialty sector adopting innovative regenerative treatments.

The Animal Stem Cell Therapy Market is poised for substantial expansion, underpinned by strong business trends focusing on commercializing allogeneic cell products for off-the-shelf use, thereby reducing treatment complexity and cost. Key industry players are aggressively investing in R&D to obtain specific regulatory clearances across North America and Europe, targeting conditions prevalent in companion animals like canine osteoarthritis and equine tendonitis. Regional trends indicate North America currently dominates the market share due to high consumer acceptance of advanced veterinary procedures and a dense network of specialized veterinary clinics, while the Asia Pacific region is forecast to exhibit the highest CAGR, driven by rapid urbanization, increasing pet ownership in countries like China and India, and rising awareness of advanced animal healthcare. Segment trends highlight the dominance of the companion animals segment, particularly dogs, in terms of application volume, with adipose-derived stem cells remaining the preferred source due to ease of collection and high yield, further supported by growing demand for autologous treatments in specialized veterinary practices.

Common user questions regarding the impact of AI in Animal Stem Cell Therapy frequently revolve around how artificial intelligence can optimize cell culture protocols, predict treatment efficacy in diverse animal breeds, and streamline preclinical trial data analysis. Users express concerns about the ethical implications of using AI to select ideal donor cells and the feasibility of integrating complex machine learning models into standard veterinary practice, especially in smaller clinics. Key themes emerging from these inquiries include the expectation that AI will enhance personalized veterinary medicine by correlating patient-specific biomarkers with stem cell characteristics to improve success rates. Furthermore, there is significant interest in using predictive modeling to identify early indicators of regenerative failure or complications, optimizing treatment timing and minimizing adverse effects, thereby transitioning regenerative therapies from a specialized intervention to a more predictable and scalable clinical tool.

The Animal Stem Cell Therapy Market is profoundly influenced by dynamic Drivers, Restraints, and Opportunities, collectively forming the core Impact Forces shaping its competitive landscape. Primary drivers include the massive increase in global pet insurance penetration and the willingness of pet owners to invest significant resources in advanced, high-cost therapies when conventional treatments fail. This financial commitment is coupled with technological advancements in cell processing and cryopreservation, which have made these treatments more accessible and standardized across different veterinary settings. The expanding body of scientific evidence supporting the long-term benefits of MSCs in treating common conditions like canine osteoarthritis further strengthens market momentum, establishing regenerative medicine as a standard therapeutic option rather than a last resort.

However, the market faces significant restraints, chiefly stemming from the high cost of therapy and the persistent lack of standardized regulatory frameworks across diverse geographical regions. While certain countries have specific guidelines, the heterogeneity in approval processes for autologous versus allogeneic products creates market friction and delays commercialization. Furthermore, the specialized training required for veterinarians to perform cell harvesting, processing, and application acts as a bottleneck, limiting the number of clinics capable of offering these advanced services. Public skepticism regarding the long-term safety and efficacy of these relatively new biological products also presents a minor restraint that requires sustained educational effort to overcome.

Opportunities for growth are abundant, primarily revolving around the development of species-specific and 'off-the-shelf' allogeneic therapies, which significantly simplify the treatment process and broaden market reach. Expanding the application scope beyond orthopedics into treating chronic metabolic, endocrine, and neurological diseases in animals represents a vast, untapped market potential. The increasing use of induced pluripotent stem cells (iPSCs) in veterinary research, coupled with advancements in biobanking services tailored for animal stem cells, provides a robust foundation for future market evolution, promising more personalized and effective treatments. These combined forces drive significant investment and innovation in the ecosystem.

The Animal Stem Cell Therapy Market is meticulously segmented based on key factors including Animal Type, Source, Application, and End-User, providing a comprehensive view of market dynamics and adoption patterns across the veterinary healthcare landscape. Segmentation by Animal Type clearly delineates the dominance of companion animals, particularly dogs and horses, due to their higher lifetime value and owner expenditure, although livestock and exotic animals represent niche yet growing opportunities. Source segmentation highlights the preference for mesenchymal stem cells derived from readily available tissues like adipose fat and bone marrow, which are easier to harvest and process for both autologous and allogeneic applications. Application segmentation demonstrates the therapeutic focus primarily on musculoskeletal and joint disorders, while end-user analysis confirms veterinary hospitals and specialized clinics as the primary points of treatment delivery.

Understanding these segments is crucial for strategic market entry and product development. For instance, therapies targeting equine athletes require specific formulation and delivery systems to treat tendon and ligament injuries, which differ significantly from the protocols used for small animal osteoarthritis. The commercial viability of allogeneic versus autologous treatments also varies by segment; companion animals often utilize autologous treatments where speed is not critical, while large animal clinics treating multiple animals might prefer standardized, off-the-shelf allogeneic products for efficiency. Furthermore, geographic differences in regulatory acceptance profoundly influence which segment strategy is prioritized in a given region, driving localized innovation in product sourcing and preparation.

The value chain for the Animal Stem Cell Therapy Market is complex, involving specialized upstream research and manufacturing followed by a highly regulated downstream distribution process. Upstream activities begin with extensive research and development (R&D), focusing on cell sourcing, isolation, expansion, and quality control protocols. This stage is dominated by specialized biotechnology firms and academic institutions that develop proprietary cell lines or processing methods. The manufacturing phase involves controlled environment processing (GMP standards are often sought) to ensure cell viability and sterility. Key challenges upstream include maintaining consistent cell quality across batches and achieving cost-effective large-scale expansion for allogeneic products, which requires significant capital investment in specialized laboratory infrastructure and regulatory compliance.

Downstream activities center around distribution, application, and post-treatment monitoring. Distribution channels are predominantly indirect, relying on specialized cold-chain logistics providers capable of maintaining the ultra-low temperatures required for cell transport. Products flow primarily from manufacturers to centralized veterinary specialty hospitals, academic veterinary centers, or certified independent veterinary clinics. Direct distribution is rare but occurs when manufacturers have proprietary logistics networks or provide autologous services where processing is done in-house or by a local, dedicated lab partner. The final stage involves the veterinary specialist administering the therapy and subsequent follow-up care, which often involves collaboration between the clinic and the research lab for efficacy tracking.

The efficiency of the distribution channel is paramount, especially for temperature-sensitive cell products. The involvement of highly specialized veterinary surgeons or certified regenerative medicine practitioners at the point of care distinguishes this value chain. Furthermore, the regulatory scrutiny applied to veterinary biologics necessitates comprehensive documentation and traceable systems throughout the entire chain, from donor selection (for allogeneic) to final injection. The value creation is maximized when intellectual property protections are strong in the R&D phase and when distribution minimizes risk of cell damage or degradation.

The primary end-users and buyers of Animal Stem Cell Therapy are deeply segmented, spanning professional veterinary practitioners, specialized animal owners, and large research institutions. The largest customer segment consists of owners of high-value companion animals, particularly dogs suffering from chronic, debilitating conditions like severe osteoarthritis, where conventional non-steroidal anti-inflammatory drugs (NSAIDs) no longer provide adequate relief. These pet owners often possess higher disposable incomes, high emotional attachment to their pets, and often carry pet insurance policies that cover advanced regenerative treatments, making them willing and able to pay the premium prices associated with these therapies. Specialized canine rehabilitation centers and small animal veterinary hospitals serve as the direct purchasers and applicators for this segment.

Another crucial customer segment involves the equine industry, specifically racehorse trainers, equestrian competitors, and breeding farms. Horses, valued highly as athletes and breeding stock, require rapid and effective treatment for musculoskeletal injuries (tendon tears, ligament damage) to maximize their performance window and extend their competitive careers. In this segment, the focus is on therapies that offer superior healing with minimal scarring and maximum tissue strength recovery. Specialized equine veterinary clinics and mobile large animal practitioners are the key service providers, often utilizing standardized allogeneic products due to the time-sensitive nature of treatment in athletic injuries.

Lastly, academic and government-funded research organizations represent an important, albeit non-clinical, customer base. These institutions purchase stem cell products and specialized media for ongoing research aimed at developing new veterinary indications, optimizing cell delivery systems, and conducting pharmacokinetic studies. Their demand drives innovation in the upstream technology and supports the foundational science needed for future commercialization efforts. This diverse customer base requires manufacturers to maintain varied product lines, ranging from ready-to-use clinical doses to high-purity research-grade reagents.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 1,020 Million |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Aratana Therapeutics (Elanco), VetStem Biopharma, Medivet, VETCELL, Cell Therapy Sciences, StemCells Inc., Magellan Stem Cell, Pluristem Therapeutics, Gallant, Regenerative PetCare, J-Store, Bio-Matrix, Zoetis, Mesoblast, cynata therapeutics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Animal Stem Cell Therapy market is defined by continuous innovation in cell isolation, expansion, and delivery methodologies aimed at improving cell viability and therapeutic effectiveness. A pivotal technology involves advanced cell culture systems, including bioreactors and specialized growth media, which maximize the yield and maintain the purity of mesenchymal stem cells (MSCs) during ex vivo expansion. Techniques for non-enzymatic isolation of adipose-derived stem cells (ADSCs) are gaining traction as they simplify the isolation process, increase safety, and reduce processing time in clinic settings. Furthermore, technologies focusing on quality control, such as flow cytometry and automated cell counting systems, are essential for ensuring that the final therapeutic product meets stringent viability and potency criteria before administration, which is critical for regulatory adherence and clinical success.

Delivery technology is another rapidly evolving area. Traditional delivery involves simple intra-articular or intravenous injection, but emerging methods include incorporating stem cells into biomaterial scaffolds (hydrogels or porous matrices) that are implanted directly at the injury site. These advanced delivery systems are designed to enhance cell retention, promote localized regenerative signaling, and control the rate of cell differentiation, offering superior outcomes for complex orthopedic and soft tissue repairs. Cryopreservation technology also remains fundamental, enabling the widespread commercialization of allogeneic, off-the-shelf products by ensuring long-term storage and maintaining cellular integrity during transport across international markets.

The latest technological frontiers involve the use of induced Pluripotent Stem Cells (iPSCs) in veterinary models, offering a potentially unlimited supply of cells for species-specific treatments, although this technology is currently mainly restricted to the research phase due to regulatory hurdles related to tumorigenicity concerns. Additionally, gene editing tools like CRISPR are being explored to modify stem cells, enhancing their anti-inflammatory or regenerative properties before transplantation. These technologies, though complex, represent the next generation of animal regenerative medicine, promising therapies that are more effective, highly reproducible, and scalable for treating large populations of animals.

The global Animal Stem Cell Therapy Market exhibits significant regional disparities in terms of adoption rates, regulatory maturity, and market size, necessitating region-specific strategic approaches. North America, encompassing the United States and Canada, currently holds the largest market share. This dominance is attributed to high pet ownership rates coupled with high per capita expenditure on advanced veterinary care. The presence of sophisticated veterinary infrastructure, key market players, and relatively progressive regulatory bodies (such as the FDA Center for Veterinary Medicine) that facilitate conditional approvals for veterinary biologics further solidify its leading position. The strong insurance penetration rate also supports the affordability of these expensive procedures for pet owners across the region.

Europe represents the second-largest market, characterized by stringent yet established veterinary biological product regulations, particularly in major economies like the UK, Germany, and France. The European market sees strong demand driven by equine sports medicine, where stem cell therapy is widely accepted for treating high-value competition horses. However, regulatory fragmentation across the European Union can sometimes slow down the market entry of novel products. The trend toward natural and biological treatments in animal health complements the adoption of stem cell therapies, providing sustained growth momentum within this mature market.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period. This rapid expansion is primarily driven by socio-economic changes, including surging disposable incomes, increasing Westernization of pet care practices, and a cultural shift toward viewing pets as family members in countries like China, Japan, and South Korea. While the veterinary infrastructure is still developing compared to North America, government investments in biotechnology and the establishment of local manufacturing facilities for biologics are rapidly accelerating market penetration. Latin America and the Middle East & Africa (MEA) remain emerging markets, where adoption is generally restricted to affluent urban centers and specialized equine facilities, presenting long-term opportunities as economic stability and healthcare awareness improve.

Stem cell therapy is most widely recognized and clinically proven for treating orthopedic conditions, particularly chronic canine osteoarthritis, severe joint disease, tendon and ligament injuries in horses, and non-healing wounds. These mesenchymal stem cells (MSCs) primarily function to reduce inflammation and promote localized tissue regeneration.

The market utilizes both approaches, but autologous therapy (using the animal's own cells, typically adipose-derived) remains common due to minimal rejection risk. Allogeneic therapy (using cells from a donor animal) is gaining popularity, especially in equine practice, as it provides standardized, off-the-shelf treatments that can be used immediately without requiring a cell harvesting procedure.

Stem cell therapy represents a high-cost treatment modality, often ranging significantly higher than conventional pharmacological treatments or basic surgery due to the complexity of cell processing, regulatory compliance, and specialized veterinary expertise required. However, the long-term benefit of reduced pain medication dependency can offset lifetime costs for chronic conditions.

Regulatory challenges include the lack of globally standardized guidelines for veterinary biologics, classification ambiguity (is it a drug or a biological product), and the stringent requirements for proving long-term safety and efficacy across diverse animal species and breeds. This variability slows down product market entry in numerous geographies.

Adipose tissue (fat) is the most frequently utilized source for generating mesenchymal stem cells (ADSCs), particularly in autologous treatments. Adipose tissue is relatively easy to harvest minimally invasively, provides a high yield of viable cells, and possesses robust differentiation capacity, making it highly preferred by specialized veterinary practitioners globally.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.