ID : MRU_ 433620 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

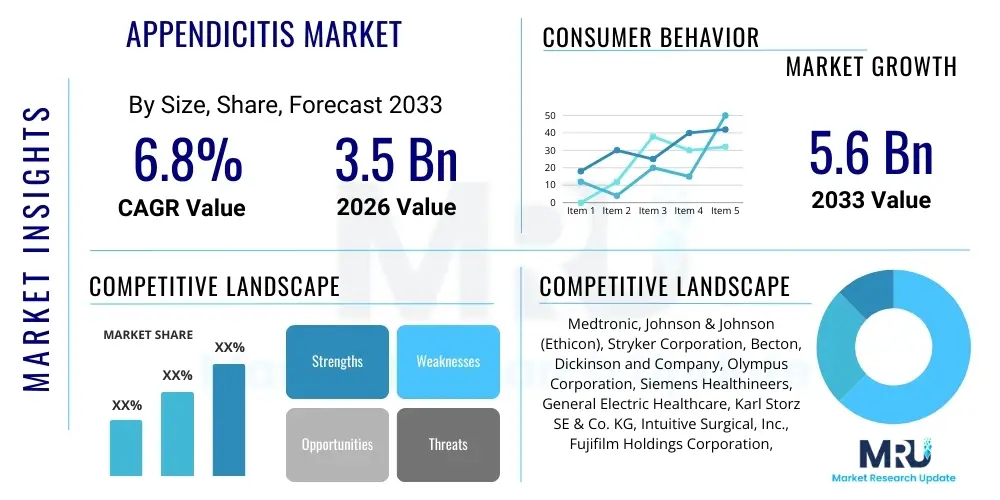

The Appendicitis Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 5.6 Billion by the end of the forecast period in 2033.

The Appendicitis Market encompasses the comprehensive range of diagnostic tools, treatment modalities, and related medical services utilized in the management of appendicitis, a common acute abdominal emergency caused by inflammation of the vermiform appendix. This condition necessitates rapid and accurate diagnosis to prevent severe complications, such as perforation, peritonitis, and sepsis. The market is defined by the flow of innovative products, particularly high-resolution imaging devices like Computed Tomography (CT) and Magnetic Resonance Imaging (MRI), alongside advanced surgical techniques, predominantly minimally invasive laparoscopy. The rapid clinical presentation and the need for immediate surgical or non-operative intervention drive consistent demand across global healthcare systems.

Major applications within this market center around accurate and timely diagnosis, which is critical for positive patient outcomes. Diagnostic tools include clinical assessment, laboratory tests (white blood cell count, C-reactive protein), and sophisticated medical imaging. Treatment primarily involves surgical removal of the appendix, known as appendectomy, which is increasingly performed using laparoscopic techniques due to reduced recovery time and lower complication rates compared to traditional open surgery. Non-operative management using antibiotics is emerging as a viable option for select cases of uncomplicated appendicitis, further diversifying the market landscape and influencing product demand.

The core benefits driving market expansion include continuous advancements in surgical instrumentation, improved diagnostic accuracy leading to fewer negative appendectomies, and shorter hospital stays resulting from minimally invasive procedures. Key driving factors are the rising global geriatric population, which is more susceptible to delayed diagnosis, increasing public and professional awareness regarding acute abdominal pain symptoms, and substantial investments by both private and public sectors into advanced healthcare infrastructure, particularly in developing economies. Furthermore, technological integration, such as robotic-assisted surgery, is pushing the boundaries of surgical precision and safety, reinforcing market growth trajectories.

The Appendicitis Market is characterized by robust technological adoption, particularly in imaging and surgical robotics, defining current business trends. Major market players are focusing on strategic collaborations and mergers & acquisitions to integrate diagnostic platforms with therapeutic solutions, aiming for end-to-end management protocols. A significant trend involves the shift towards value-based care models, where the focus is on reducing overall treatment costs through faster diagnosis and lower complication rates associated with advanced laparoscopic and non-operative interventions. Investments in AI-driven diagnostic assistance tools are becoming paramount, addressing the challenge of minimizing variability in radiological interpretation across different clinical settings globally.

Regionally, North America maintains market dominance due to high healthcare expenditure, established reimbursement policies, and early adoption of advanced medical technologies, including high-end CT scanners and robotic surgical systems. However, the Asia Pacific (APAC) region is projected to exhibit the fastest Compound Annual Growth Rate (CAGR) throughout the forecast period. This accelerated growth is primarily attributed to rapidly improving healthcare infrastructure, substantial government investments in public health services, expanding insurance coverage, and a large, aging patient base. European markets are driven by stringent quality standards and a strong emphasis on non-operative management strategies, supported by comprehensive clinical guidelines.

Segment trends highlight the increasing preference for the minimally invasive treatment segment, specifically laparoscopic appendectomy, due to its clinical advantages. Within the diagnostic segment, the utilization of advanced imaging modalities like CT scans remains crucial, although there is a concerted effort to increase the use of Ultrasound and MRI, particularly in pediatric and pregnant populations, to mitigate radiation exposure risks. End-user trends show hospitals continuing to be the primary revenue generators, but specialized Ambulatory Surgical Centers (ASCs) are gaining traction, especially in North America, by offering cost-effective and streamlined surgical services for routine appendectomy procedures.

User queries regarding the impact of Artificial Intelligence on the Appendicitis Market frequently revolve around speed and accuracy: Can AI significantly reduce the time needed for radiological diagnosis? Will AI tools reliably differentiate acute appendicitis from other abdominal pathologies? What role does predictive modeling play in identifying patients suitable for non-operative antibiotic management? These questions underscore a high user expectation for AI to serve as a pivotal tool in clinical decision support, particularly in high-volume emergency settings. The consensus emerging from the market is that AI algorithms, trained on vast datasets of medical images and clinical parameters, hold immense potential to enhance the sensitivity and specificity of appendicitis diagnosis, minimize human error, and standardize treatment protocols across various clinical environments.

The primary influence of AI is observed in streamlining the diagnostic workflow. Machine learning models are being developed to automatically analyze CT and ultrasound images for subtle signs of appendiceal inflammation, edema, and perforation, often flagging areas of concern more rapidly than human radiologists can in complex cases. This acceleration of diagnosis is crucial because treatment delay directly correlates with increased morbidity and mortality in perforated appendicitis. Furthermore, AI-powered predictive analytics are being applied to clinical data—including lab results, patient history, and demographics—to calculate the probability of uncomplicated versus complicated appendicitis, aiding clinicians in deciding between immediate surgery and observation or non-operative management.

However, user concerns often touch upon data privacy, algorithmic bias, and the necessity of validation in real-world clinical settings before widespread adoption. The integration of AI into existing hospital systems requires significant investment in infrastructure and training. Despite these barriers, the expectation remains high that AI will optimize resource allocation (e.g., predicting operative vs. non-operative needs), improve risk stratification for personalized medicine, and ultimately reduce the rate of negative appendectomies, which remains a key metric of quality control in emergency surgery. AI's role will evolve from simple image analysis to comprehensive clinical recommendation engines, transforming the standard of care for acute appendicitis.

The dynamics of the Appendicitis Market are fundamentally shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming the market's Impact Forces. Key drivers propelling market expansion include the high and consistent global incidence of appendicitis, demanding constant healthcare system preparedness and throughput. Furthermore, technological progress in surgical equipment, specifically the continuous refinement of laparoscopic instruments and the increasing adoption of robotic surgical platforms, makes treatment safer and faster, thereby driving utilization. Restraints include the significant capital investment required for advanced diagnostic infrastructure, such as multi-detector CT scanners and high-field MRI systems, which limits adoption in resource-constrained regions. Additionally, ongoing clinical debate regarding the long-term effectiveness and patient suitability of non-operative management versus surgical intervention introduces market uncertainty in certain treatment segments.

Opportunities for growth are primarily centered on capitalizing on diagnostic refinement and penetrating underserved markets. A major opportunity lies in developing highly accurate, low-cost point-of-care diagnostic tools, such as advanced ultrasound techniques and specific biomarker assays, which can reduce reliance on expensive and radiation-intensive CT scans, especially in pediatric populations. Furthermore, the growth potential in emerging economies, driven by improved access to healthcare and government initiatives aimed at modernizing emergency medical services, presents a substantial revenue stream for manufacturers of both diagnostic and surgical equipment. The increasing trend towards outpatient and short-stay surgeries, facilitated by minimally invasive techniques, also opens opportunities for specialized Ambulatory Surgical Centers (ASCs).

The overarching impact forces thus dictate a market trend toward efficiency and precision. Technological innovation acts as the primary driver, forcing hospitals to upgrade equipment to meet the standard of care, while cost constraints and accessibility issues serve as significant restraints, especially globally. The ongoing search for non-invasive or less invasive solutions (both diagnostic and therapeutic) represents the major opportunity, pushing research and development efforts toward antibiotic-only treatment protocols and advanced imaging that minimizes patient risk. These forces collectively ensure that the market remains highly competitive, prioritizing products that offer superior clinical outcomes coupled with cost-effectiveness.

The Appendicitis Market segmentation provides a granular view of revenue distribution across distinct categories based on diagnosis, treatment modality, end-user type, and severity. Understanding these segments is crucial for market participants to tailor their strategies, focusing investment on high-growth areas, such as the minimally invasive surgery category and advanced imaging solutions. The market is primarily bifurcated based on treatment, where surgical management (laparoscopic and open appendectomy) continues to dominate, but the non-operative management segment (antibiotic therapy) is witnessing rapid growth, driven by positive clinical trial results for uncomplicated cases. Diagnostic modalities form another critical segmentation, encompassing clinical scoring systems, laboratory tests, and sophisticated radiological imaging, with computed tomography holding the largest market share due to its high accuracy in confirming diagnosis and ruling out differential pathologies.

The Value Chain of the Appendicitis Market begins with the upstream segment, which involves the research, development, and manufacturing of core medical technologies. This includes suppliers of raw materials (polymers, metals for surgical instruments), specialized component manufacturers for diagnostic equipment (X-ray tubes, sensors, detectors for CT/MRI), and pharmaceutical companies providing antibiotics used in non-operative management protocols. Key activities at this stage focus on innovation, quality control, and obtaining regulatory approvals (FDA, CE Mark) to ensure safety and efficacy. High competition exists among specialized device manufacturers aiming to improve instrument maneuverability and imaging resolution.

The intermediate stage encompasses distribution channels, which are vital for bridging the gap between manufacturers and end-users. Distribution is complex, involving both direct sales forces, particularly for high-capital equipment like robotic systems sold directly to large hospital networks, and indirect channels relying on third-party distributors, wholesalers, and specialized medical supply logistics providers. The effectiveness of the supply chain depends heavily on managing inventory, timely delivery of sterilized surgical supplies, and providing technical support for complex imaging machinery. Indirect channels are particularly important for reaching smaller clinics and hospitals in geographically dispersed regions.

The downstream segment represents the point of care, where products and services are consumed. This includes hospitals, which utilize diagnostic devices and perform the vast majority of surgical interventions, Ambulatory Surgical Centers (ASCs) focused on elective or routine cases, and specialized diagnostic imaging facilities. Reimbursement policies and relationships with payors (private insurance, government programs) are critical components at this stage, influencing the adoption rate of newer, often more expensive, technologies like robotic surgery. Ultimately, patient outcome data collected downstream feeds back into the upstream segment, driving continuous product improvement and market strategy refinement.

The primary consumers and end-users of products and services within the Appendicitis Market are large healthcare institutions that serve as emergency receiving centers. Hospitals, particularly those with comprehensive emergency departments, surgical suites, and advanced radiological capabilities, constitute the largest segment of potential customers. These institutions require high-volume consumables (suture materials, trocar ports, specialized staplers), sophisticated diagnostic machinery (CT and MRI scanners), and ongoing maintenance services for these complex systems. Their purchasing decisions are heavily influenced by clinical efficacy, total cost of ownership, and integration capabilities with existing Electronic Health Record (EHR) systems.

A rapidly expanding customer base includes specialized medical facilities such as Ambulatory Surgical Centers (ASCs). These centers are increasingly performing uncomplicated appendectomies, taking advantage of minimally invasive techniques that allow for short recovery times. ASCs prioritize surgical systems that are efficient, portable, and require minimal footprint, focusing on cost-effective solutions to maintain competitive pricing compared to large hospitals. This segment represents a high-growth area for manufacturers of standard laparoscopic instruments and related disposable products designed for outpatient settings.

Furthermore, specialized Diagnostic Imaging Centers and independent clinical laboratories represent crucial potential customers, particularly for imaging consumables, contrast agents, and advanced laboratory testing reagents used in screening and initial diagnosis. Government healthcare purchasing bodies and large regional health networks also act as major customers, often dictating procurement standards and volume pricing through centralized purchasing agreements. This latter group is especially interested in achieving diagnostic accuracy while ensuring broad accessibility and standardized care protocols across diverse geographic locations within their jurisdiction.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.6 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Johnson & Johnson (Ethicon), Stryker Corporation, Becton, Dickinson and Company, Olympus Corporation, Siemens Healthineers, General Electric Healthcare, Karl Storz SE & Co. KG, Intuitive Surgical, Inc., Fujifilm Holdings Corporation, B. Braun Melsungen AG, Teleflex Incorporated, Cook Medical, CONMED Corporation, Boston Scientific Corporation, Richard Wolf GmbH, Hologic, Inc., Drägerwerk AG & Co. KGaA, McKesson Corporation, Zimmer Biomet. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Appendicitis Market is rapidly evolving, driven primarily by the pursuit of minimizing invasiveness in surgery and maximizing accuracy in diagnosis. In treatment, the dominance of laparoscopic surgery relies on high-definition visualization systems, advanced insufflation equipment, and specialized energy devices for dissection and hemostasis. Key technological progress includes the development of articulating instruments and vessel sealing devices that enhance surgeon dexterity and safety during minimally invasive procedures. Furthermore, the increasing integration of Robotic-Assisted Surgery (RAS) platforms offers surgeons 3D visualization and tremor filtration, although their adoption is currently limited to high-volume centers due to high initial investment and disposable costs.

On the diagnostic front, the market relies heavily on cross-sectional imaging, with Multi-Detector Computed Tomography (MDCT) scanners being the gold standard for rapid, definitive diagnosis, especially in adults. The technological focus here is on reducing radiation dose while maintaining image quality, leading to the proliferation of Low-Dose CT protocols. For radiation-sensitive groups, such as children and pregnant women, high-field MRI technology (1.5T and 3T systems) offers superior soft tissue differentiation without ionizing radiation, driving investments in MRI-compatible surgical planning tools and dedicated fast-scanning protocols. Point-of-care ultrasound devices, enhanced with superior image processing and artificial intelligence tools for automated measurements, are also gaining traction for initial screening.

Emerging technologies also include novel biomarker diagnostics. While traditional laboratory tests like leukocytosis and elevated CRP are non-specific, research is focused on identifying highly specific inflammatory markers or genetic signatures that could confirm appendicitis diagnosis early or predict the success of non-operative management. The integration of telemedicine and remote consultation tools is also an increasing factor, especially for accessing specialist radiological interpretation in remote or rural emergency settings, ensuring rapid access to expert opinions regardless of geographical location. The confluence of advanced imaging, robotic surgery, and predictive analytics characterizes the current technological trajectory.

North America, comprising the United States and Canada, holds the largest market share in the Appendicitis Market due to several foundational factors. The region benefits from a highly developed healthcare infrastructure, characterized by high investment in advanced medical technology and a robust private insurance system that facilitates the rapid adoption of premium diagnostic and surgical tools, including robotic systems. High procedural volumes, standardized clinical guidelines, and strong emphasis on high-quality patient outcomes contribute to the high utilization of advanced CT/MRI scanning for diagnosis and laparoscopic surgery for treatment. Furthermore, the presence of major medical device manufacturers and continuous R&D activities solidifies North America's leadership position in innovation and market value.

Europe represents a mature market, driven by universal healthcare coverage and stringent regulatory environments focusing on patient safety and cost-effectiveness. Western European countries, particularly Germany, the UK, and France, exhibit high adoption rates of minimally invasive surgical techniques and are leaders in clinical research concerning non-operative management (antibiotic protocols) for uncomplicated appendicitis. The market is characterized by a balance between technological utilization and cost containment, favoring established, reliable laparoscopic systems and emphasizing the use of ultrasound initially to triage patients before resorting to CT, thereby managing healthcare expenditures effectively. Eastern Europe is experiencing growth driven by infrastructure upgrades and increasing access to advanced medical devices.

The Asia Pacific (APAC) region is forecasted to be the fastest-growing market during the projection period. This rapid expansion is fueled by massive populations, increasing urbanization, rising disposable income, and significant public and private sector investments aimed at improving healthcare access and quality. Countries like China and India are pivotal to this growth, focusing on expanding hospital capacity and modernizing surgical facilities. While cost sensitivity remains a factor, leading to a higher prevalence of open surgery in certain rural areas, the demand for advanced imaging and imported laparoscopic instruments is surging in metropolitan centers, reflecting an increasing alignment with Western standards of care.

Latin America and the Middle East & Africa (MEA) represent emerging markets with substantial untapped potential. Growth in these regions is heterogeneous, heavily reliant on national economic stability and government healthcare priorities. In MEA, particularly the Gulf Cooperation Council (GCC) countries, high oil revenues translate into investment in state-of-the-art hospitals, driving demand for premium products. Latin American growth is driven by expanding middle-class populations and improving insurance penetration, though political and economic volatility can occasionally restrain large-scale technology adoption, leading to higher reliance on more fundamental diagnostic and treatment modalities compared to developed markets.

The current standard of care primarily involves surgical intervention, specifically laparoscopic appendectomy, due to its minimally invasive nature, reduced recovery time, and lower infection risk compared to traditional open surgery. However, non-operative management using broad-spectrum antibiotics is increasingly accepted for selected patients presenting with uncomplicated, non-perforated appendicitis, guided by strict clinical criteria and follow-up imaging.

Advanced diagnostic technology, particularly Multi-Detector Computed Tomography (MDCT) and high-resolution ultrasound, significantly enhances accuracy by providing detailed visualization of the appendix and surrounding structures. Emerging technologies like AI-powered image analysis are further improving diagnostic speed and consistency, reducing the rate of misdiagnosis and unnecessary negative appendectomies.

The minimally invasive treatment segment, specifically laparoscopic and robotic-assisted appendectomy, is projected to maintain the highest growth rate within the Appendicitis Market. This growth is driven by increasing patient preference for less invasive procedures, improved surgical outcomes, and expanded availability of advanced surgical instruments globally, especially in emerging economies seeking to upgrade surgical capabilities.

Key restraints include the substantial capital investment required for implementing and maintaining high-end diagnostic imaging equipment, such as CT and MRI scanners, which limits accessibility in lower-resource settings. Furthermore, ongoing patient safety concerns regarding radiation exposure, particularly in pediatric diagnosis, and the relatively high cost of advanced robotic surgical platforms act as significant limiting factors.

Non-operative management, utilizing targeted antibiotic therapy, plays a critical role by offering an alternative treatment pathway for select patients with uncomplicated appendicitis. Although surgery remains dominant, the non-operative segment is growing rapidly, supported by clinical evidence demonstrating efficacy similar to surgery in certain cases, thus reducing the need for hospitalization and surgical risk for a specific patient subset.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.