ID : MRU_ 433725 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

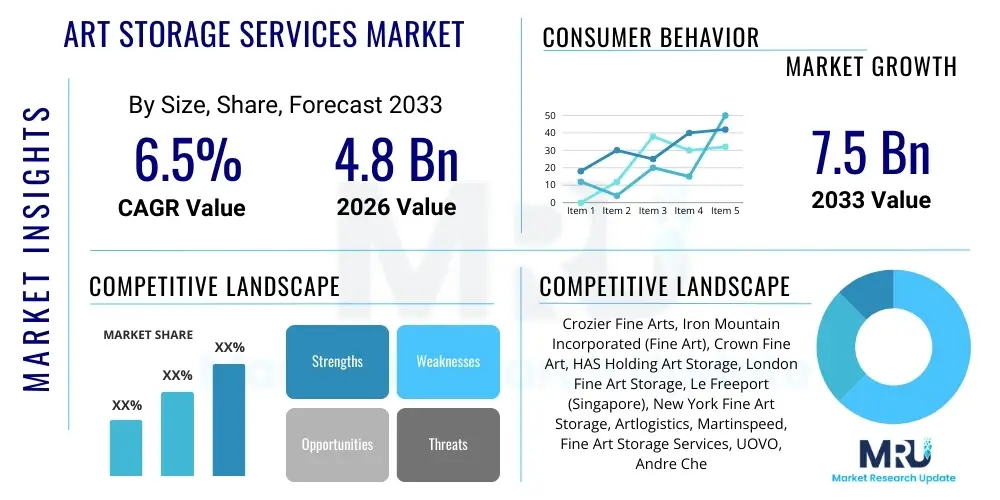

The Art Storage Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. This consistent growth trajectory is driven primarily by the escalating value of global art collections, the need for specialized environmental controls, and increased cross-border trade of high-value assets. The inherent specialization required for storing fine art—including paintings, sculptures, and historical artifacts—mandates the use of certified facilities that often exceed standard commercial storage specifications.

The market is estimated at USD 4.8 Billion in 2026, reflecting the current installed capacity and the existing client base comprising high-net-worth individuals (HNWIs), museums, galleries, and investment funds. The substantial market valuation underscores the premium pricing associated with secure, climate-controlled environments and integrated services such as inventory management, viewing rooms, and specialized insurance consultation. Demand concentration is notable in major art hubs globally, where transactional volumes necessitate robust and reliable storage infrastructure.

The Art Storage Services Market is projected to reach USD 7.5 Billion by the end of the forecast period in 2033. This anticipated expansion is fueled by the continuing digitalization of art provenance and inventory systems, alongside the geographical diversification of art ownership, particularly across emerging economies in Asia Pacific and the Middle East. Furthermore, regulatory compliance related to cultural heritage preservation in various jurisdictions will increasingly necessitate high-standard, third-party storage solutions, solidifying long-term market growth.

The Art Storage Services Market encompasses specialized logistical and warehousing solutions designed exclusively for preserving and safeguarding valuable fine art and cultural artifacts. These services are distinguished from conventional storage by their mandatory inclusion of museum-grade climate control (temperature and humidity regulation), high-level security protocols, fire suppression systems utilizing inert gases, and detailed inventory tracking capabilities. The primary users of these specialized facilities are institutions such as major museums and auction houses, alongside private collectors who require optimal preservation conditions to maintain the intrinsic value and integrity of their assets over extended periods. The specialized nature of the product minimizes the risk of damage from environmental factors, theft, or catastrophic events, which is paramount for non-fungible, irreplaceable cultural assets.

Major applications of art storage services include temporary storage during transit or exhibitions, long-term archival storage for estate planning, inventory management for large corporate collections, and secure holding for assets undergoing valuation or transfer of ownership. A significant benefit derived from utilizing professional art storage services is the simplification of insurance compliance, as insurers often mandate specific storage conditions for high-value policies. This professional stewardship alleviates the logistical and liability burden from collectors and institutions, allowing them to focus on acquisition, exhibition, and research. Additionally, these facilities often provide integrated services such as conservation consulting, bespoke crating, and transportation using specialized art handlers.

Driving factors for the market include the exponential growth in global wealth leading to increased private art accumulation, the subsequent surge in international art trade requiring complex transit and holding logistics, and the trend toward fractional ownership and art investment funds which demand impartial, institutional-grade custodianship. The increasing stringency of preservation standards set by international cultural heritage organizations also pushes smaller institutions and private entities toward professional third-party storage solutions. Furthermore, geopolitical uncertainties often prompt collectors to move assets into highly secure, neutral storage jurisdictions, boosting demand in established art logistics hubs like Switzerland, Luxembourg, and Singapore.

The Art Storage Services Market is characterized by robust business trends centered on technological integration and service differentiation. Key trends include the transition from traditional paper-based inventory to advanced digital asset management systems leveraging RFID and blockchain for immutable provenance tracking. Businesses are increasingly investing in proprietary software that offers clients real-time environmental monitoring and remote inventory visualization, moving beyond basic storage toward comprehensive collection management platforms. Regional trends show rapid growth in Asia Pacific, particularly driven by new wealth accumulation in China and Southeast Asia, requiring expansion of high-security facilities in regional financial centers like Hong Kong and Singapore. North America and Europe, while mature, maintain dominance due to established auction houses and long-standing private collections, focusing on ultra-high-security vault services and specialized freeports.

Segmentation analysis highlights the increasing importance of the climate-controlled segment, which dominates the market value due to its non-negotiable requirement for sensitive materials like oil paintings and rare documents. The services segment shows high growth, particularly for value-added services such as conservation consultation, customs management (especially critical for trans-continental shipments), and private viewing rooms designed for prospective buyers and collection review sessions. In terms of end-users, Private Collectors remain the primary revenue drivers, though Institutional Users (museums and endowments) provide stable, long-term contracts. The shift toward art as a recognized asset class, rather than purely aesthetic enjoyment, is compelling financial institutions and wealth managers to utilize high-end storage facilities as part of structured asset protection portfolios.

Overall, the market remains highly fragmented yet competitive at the ultra-luxury tier, dominated by specialized logistics providers capable of managing the entire lifecycle of art movement and preservation. Successful market participation necessitates high capital investment in infrastructure (seismic bracing, optimized HVAC systems) and rigorous compliance with global customs and security standards. Strategic geographical placement near major transit hubs and free trade zones remains a crucial determinant of market share, enabling seamless integration with the global art trade network. The market outlook is overwhelmingly positive, driven by persistent wealth creation and the inelastic demand for superior asset protection solutions.

Users frequently inquire about how AI can enhance the security, efficiency, and provenance tracking within specialized art storage facilities. Common questions revolve around AI’s role in predictive maintenance of climate control systems, automated anomaly detection (e.g., unauthorized access or environmental drift), and sophisticated inventory management. Concerns often center on data privacy, the potential cost of implementing AI-driven systems, and whether AI can accurately assess conservation needs without human expertise. Key expectations include AI integrating seamlessly with existing inventory databases (like TMS or Collection Management Systems) to offer optimized space utilization based on collection rotation patterns and predictive risk modeling related to specific artwork vulnerabilities. The consensus highlights that AI is viewed primarily as an enhancement tool for risk mitigation and operational streamlining rather than a revolutionary disruption to the fundamental service of physical preservation.

The Art Storage Services Market is shaped by a powerful interplay of drivers, restraints, and opportunities that dictate operational strategy and investment decisions. Key drivers include the massive expansion of the global ultra-high-net-worth individual population, increasing the volume of private collections requiring professional custody, and the formal recognition of art as a substantial, liquid asset class by major financial institutions. These drivers necessitate the development of specialized "freeports"—secure, duty-free zones—that simplify international transit and financial transactions related to art. However, the market is restrained by the exceptionally high capital expenditure required to establish and maintain museum-grade facilities, particularly regarding energy-intensive climate control systems and sophisticated multi-layered security infrastructure. Furthermore, regulatory complexity surrounding the cross-border movement of cultural property and stringent import/export controls in highly protectionist countries present significant operational hurdles.

Opportunities in this sector primarily lie in the geographic diversification of high-end storage facilities, particularly targeting emerging markets in the Middle East (e.g., UAE) and specific locations in Latin America, capitalizing on regional wealth creation. Another significant opportunity is the integration of digital twin technology and blockchain for enhanced provenance security, attracting clients seeking immutable records of ownership and condition reports. The growing market for fractional ownership and digitized art (NFTs) also opens new ancillary service lines focused on integrating digital asset records with their physical counterparts, creating hybrid storage and management contracts. The increasing awareness of environmental sustainability in logistics is prompting facility operators to invest in green technologies and energy-efficient climate control, positioning themselves favorably to environmentally conscious clients.

The impact forces within the market are predominantly technological and regulatory. The impact of security technology (biometrics, anti-intrusion systems) is high, directly affecting client trust and insurance costs. Regulatory forces, particularly international tax and customs laws regarding temporary importation and permanent storage in free trade zones, exert profound influence on market profitability and geographical attractiveness. Economically, the volatility of the global art market (determined by auction results and investment sentiment) indirectly affects storage demand; periods of high asset valuation often lead to increased long-term storage commitments. Sociocultural trends, such as the increased institutionalization of private collections and higher standards for conservation mandated by academic and museum communities, continually push the operational floor higher, benefiting professionalized service providers over general warehouse options.

The Art Storage Services Market is rigorously segmented based on the type of storage environment, the nature of the assets stored, and the specific end-user category, reflecting the diverse and specialized needs of the clientele. The primary differentiation exists between standard climate-controlled storage, which meets basic preservation parameters, and specialized ultra-high-security vault storage, often required for irreplaceable masterworks or collections with sensitive historical value. Service offerings further segment the market, ranging from simple warehousing to highly integrated collection management platforms that include transport, customs clearance, conservation, and viewing room access. This stratification ensures that service providers can effectively cater to the highly varied requirements of museums needing bulk, long-term archival space versus private collectors needing frequent access and bespoke handling.

Analyzing the segmentation by asset type reveals distinct handling protocols and pricing structures. While paintings and sculptures constitute the largest volume of assets stored, specialized segments like manuscripts, rare books, and historical artifacts demand unique micro-climates and handling expertise, commanding premium rates. The segmentation by end-user remains critical, as institutional clients like museums and galleries prioritize long-term contractual stability and proximity to transit routes, whereas private collectors often prioritize discretion, personalized access, and integrated wealth management solutions. Understanding these segment dynamics is essential for providers to tailor infrastructure investment and marketing strategies effectively, ensuring optimal service delivery across the complex ecosystem of art ownership and preservation.

The value chain for Art Storage Services is sophisticated, beginning with upstream inputs focused heavily on specialized infrastructure and security technology. Upstream activities involve securing real estate in strategically advantageous locations (often near airports or free trade zones), procuring high-precision HVAC and air filtration systems capable of maintaining museum standards, and installing certified security infrastructure (vault doors, multi-zone alarm systems, surveillance tech). Key suppliers include specialized construction firms, high-security technology vendors, and climate control system manufacturers who must meet stringent international standards for asset protection. The quality and reliability of these upstream inputs directly determine the service tier a provider can offer and significantly impact operational expenditure, particularly energy costs.

Midstream activities are centered on the core service delivery: the secure handling, inventorying, and physical preservation of the artwork. This stage involves meticulous processes such as object reception and condition reporting, secure placement, and continuous environmental monitoring. Distribution channels in this market are highly dependent on specialized art logistics firms, which function as essential intermediaries. These handlers provide door-to-door, secure transportation services, often utilizing armored vehicles and specialized climate-controlled containers. Direct distribution often occurs when institutions or major collectors contract directly with storage providers, whereas indirect distribution involves complex routing through auction houses or dealers who manage the storage logistics on behalf of the ultimate owner. Efficiency in customs clearance and insurance brokering, often integrated into the distribution model, adds significant value.

Downstream analysis focuses on the end-user interaction and post-storage services. This includes facilitating access for viewing, coordinating conservation work, managing insurance claims, and preparing items for transport to exhibitions or sale. The final value delivered to the customer is comprehensive asset protection and liquidity facilitation. Direct channels (storage provider to collector) emphasize long-term relationships and personalized service, whereas indirect channels (storage provider via an auction house) focus on transactional efficiency and rapid turnaround. Continuous integration of digital inventory platforms and robust reporting systems enhances customer transparency and trust, constituting a major competitive differentiator in the downstream segment.

The primary end-users and buyers of art storage services are stratified across individuals, institutions, and financial entities, all sharing a common requirement for high-level asset preservation and security. High-net-worth individuals (HNWIs) and ultra-high-net-worth individuals (UHNWIs) constitute the largest segment by revenue, driven by personal acquisition and estate management needs. These collectors often own substantial, sensitive collections that exceed the capacity or security capabilities of their private residences, leading them to seek discrete, professional custody. Their purchasing decisions are heavily influenced by reputation, location near major auction centers, and the availability of specialized viewing rooms that maintain confidentiality and facilitate private sales.

Institutional buyers, including national museums, major public galleries, university art departments, and corporate collections, represent the most stable customer base. These entities require large volumes of archival storage, usually under long-term contracts, to house their extensive permanent collections or rotating loan acquisitions. For institutions, compliance with rigorous conservation standards and budgetary predictability are crucial factors. Furthermore, Auction Houses (like Christie’s and Sotheby’s) and major Art Dealers are essential short-term customers, using storage facilities as temporary holding grounds for consignment items awaiting sale, or during complex transit logistics between continents. They require flexibility, expedited customs processing, and stringent security during periods of high transactional risk.

A rapidly emerging customer segment includes Art Investment Funds and Wealth Management Firms. As art transitions into a formal alternative asset class, these financial entities utilize specialized storage facilities as secure, verifiable custodianship points for their portfolios. They require transparent auditing capabilities, verifiable condition reports for valuation purposes, and often prefer freeport locations to optimize tax liabilities during holding periods. The integration of storage services with financial reporting tools is a key requirement for this segment. Ultimately, the market caters to anyone holding non-fungible, high-value cultural assets that require environmental stability and unparalleled protection from external threats.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 7.5 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Crozier Fine Arts, Iron Mountain Incorporated (Fine Art), Crown Fine Art, HAS Holding Art Storage, London Fine Art Storage, Le Freeport (Singapore), New York Fine Art Storage, Artlogistics, Martinspeed, Fine Art Storage Services, UOVO, Andre Chenue, Constant Art Service, Helu-Trans Group, Gander & White, Fine Art Bunkers, MTAB Group, AXA ART, Fortress Fine Art Storage, Poly Auction (Storage Services) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Art Storage Services Market is defined by the necessity of integrating robust physical security with advanced digital management systems to ensure comprehensive asset protection and operational efficiency. Central to this is the implementation of highly sophisticated environmental control technologies. These include HVAC (Heating, Ventilation, and Air Conditioning) systems engineered for extremely tight tolerances in temperature (typically 70°F +/- 2°) and relative humidity (typically 50% +/- 5%). These systems utilize multiple redundancy layers and high-efficiency particulate air (HEPA) filtration to mitigate pollutants and prevent microbiological contamination, which is vital for the long-term preservation of organic materials like canvases and wood.

In terms of security, the market relies on multi-layered defenses. This involves physical defenses such as reinforced concrete vaults, seismic resistance measures, and penetration-proof vault doors certified to high industry standards. These physical barriers are complemented by electronic security measures, including advanced biometric access control (iris and fingerprint scanning), multi-zone passive infrared (PIR) sensors, and ground-level vibration detection systems. Furthermore, inert gas fire suppression systems (e.g., Argon or Nitrogen-based) are preferred over traditional water sprinklers to prevent irreversible damage to artwork in case of a fire incident, demonstrating the sector’s high technology adoption specific to asset preservation.

Digital technology is increasingly driving operational value. The adoption of modern Collection Management Systems (CMS) is mandatory, integrating high-resolution digital imaging, detailed condition reports, and real-time location tracking using technologies like RFID (Radio Frequency Identification) and Ultra-Wideband (UWB) tracking for precise spatial location within large facilities. Emerging technologies include the use of blockchain for secure, tamper-proof recording of art provenance, ownership transfers, and conservation history, enhancing transparency and trust. The continuous convergence of IoT sensors for micro-climate monitoring and cloud-based inventory management tools defines the competitive edge in modern art storage operations.

Regional dynamics heavily influence the Art Storage Services Market, reflecting global wealth distribution, geopolitical stability, and the concentration of major art trading centers. North America, driven primarily by the high-volume markets in New York and Los Angeles, remains the dominant revenue generator. Facilities in this region emphasize ultra-high security and seamless integration with complex US tax and customs regulations. The demand is heavily sustained by the vast number of HNWIs and the presence of world-leading auction houses and museums that require domestic and international logistical support. Providers often focus on offering comprehensive collection management platforms tailored to sophisticated American estate planning.

Europe holds a unique position, dominated by established freeports located in Switzerland (Geneva, Zurich), Luxembourg, and recently, the UK post-Brexit. These European hubs specialize in customs-bonded storage, allowing international collectors to store assets without immediate payment of duties or VAT, making them critical nodes for global transit and trade. The focus here is on regulatory expertise, international tax optimization, and maintaining a neutral, highly secure environment, appealing to global investors seeking jurisdictional stability. Western European markets are also critical centers for conservation expertise, often integrating storage services with high-level restoration facilities.

Asia Pacific (APAC) is the fastest-growing market, largely fueled by burgeoning wealth in mainland China, Hong Kong, and Singapore. These regions are rapidly expanding their infrastructure to meet the demand from local collectors who previously stored assets abroad. Singapore's Le Freeport, for instance, has become a key strategic hub, leveraging the region's strong legal framework and political stability. Investment in APAC is focused on creating facilities that match Western security and climate standards while addressing the unique logistical challenges associated with regional transit and complex importation laws specific to fast-growing economies. The Middle East, particularly the UAE (Dubai and Abu Dhabi), is also emerging, driven by cultural investment initiatives and the establishment of global art events, necessitating professional local storage capacity.

Professional, museum-grade art storage requires maintaining stringent environmental conditions, typically a temperature of 70°F (+/- 2°F) and a relative humidity (RH) of 50% (+/- 5%). These parameters are critical to preventing material degradation, such as cracking, warping, or mold growth, which can severely impact the artwork's intrinsic value and structural integrity over time.

A freeport is a customs-bonded warehouse, typically located near major international transit hubs, that allows collectors to store high-value assets, including art, without incurring immediate import duties, VAT, or other taxes. This jurisdictional neutrality benefits global collectors and dealers by facilitating international trade, simplifying logistics, and deferring tax liabilities until the art enters the local market for consumption or sale.

Modern art storage leverages advanced technology, including multi-layered biometric access controls, seismic and vibration detection systems, inert gas fire suppression (instead of water), and AI-driven video analytics for real-time threat detection. Digital security is further enhanced through RFID and UWB tracking for precise inventory location and immutable provenance tracking using blockchain technology.

The primary client base includes Ultra-High-Net-Worth Individuals (UHNWIs) and large private estates, major international auction houses (for consignments), large institutional users such as museums and galleries (for long-term archives), and increasingly, specialized art investment funds and financial institutions utilizing art as a managed asset class.

Collectors should prioritize regulatory compliance (especially for customs and tax), facility accreditation (e.g., ISO certifications), the provider's insurance coverage and liability limits, the presence of museum-grade climate control redundancy, and the availability of integrated value-added services such as specialized art handling, conservation consulting, and private viewing rooms.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.