ID : MRU_ 431733 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

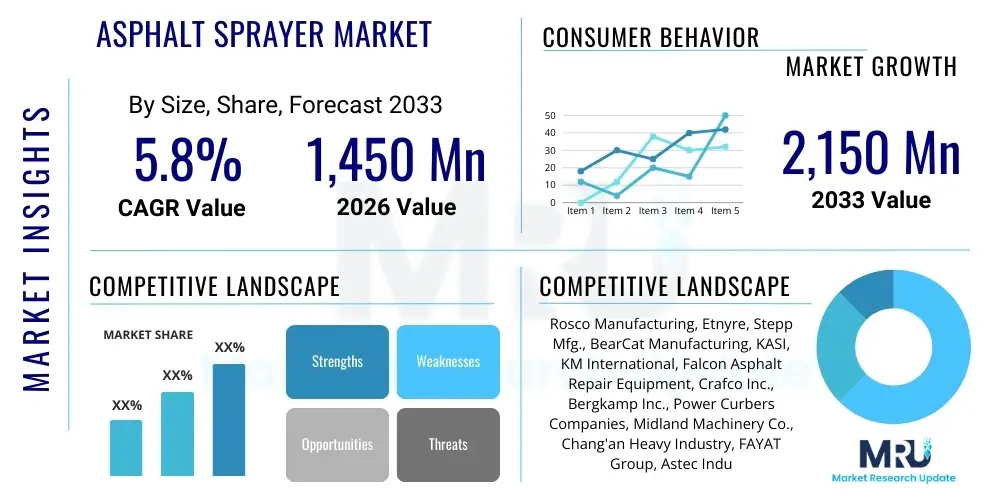

The Asphalt Sprayer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 1,450 Million in 2026 and is projected to reach USD 2,150 Million by the end of the forecast period in 2033.

The Asphalt Sprayer Market encompasses specialized construction equipment designed for the uniform and controlled application of liquid asphalt, emulsions, or cutbacks onto road surfaces. These machines are fundamental to paving and maintenance activities, ensuring proper tack coats, prime coats, and seal coats are applied before overlaying or as part of pavement preservation strategies. The primary function of the equipment is to provide an adhesive layer that bonds the new asphalt layer or chips (in chip sealing) to the existing substrate, enhancing structural integrity and longevity. Market growth is intrinsically tied to global infrastructure development, particularly road construction and the increasing emphasis on preventative maintenance schedules adopted by governmental transportation authorities worldwide.

Asphalt sprayers, which range from small, walk-behind units for patch repair to large, truck-mounted distributors capable of covering long highway stretches, utilize sophisticated pumping systems, heated tanks, and adjustable spray bars to maintain precise application rates and temperatures. Product evolution focuses heavily on accuracy, efficiency, and environmental compliance, driven by regulations mandating the reduction of volatile organic compounds (VOCs) and the optimization of material usage. Modern sprayers incorporate advanced calibration systems and GPS technology to minimize waste and ensure compliance with stringent engineering specifications for road quality.

Major applications of asphalt spraying equipment include routine road maintenance, new highway construction, airport runway paving, and municipal street repair. The inherent benefits of using specialized sprayers include superior bonding strength, reduced material consumption due to accurate distribution, and enhanced worker safety compared to manual application methods. Key driving factors propelling the market include escalating global government investments in road infrastructure renewal, the expansion of smart city projects requiring high-quality urban pavement, and the necessity to repair aging infrastructure in mature economies like North America and Europe.

The Asphalt Sprayer Market is experiencing robust growth driven primarily by a surge in global infrastructure revitalization projects and the shift toward proactive pavement preservation techniques. Business trends indicate a strong move towards automation and integration of telematics, allowing contractors to monitor and optimize fleet performance and material usage in real-time. Leading manufacturers are focusing on developing high-capacity, low-emission distributors that cater to large-scale highway projects while simultaneously refining smaller, maneuverable units for urban utility and repair tasks. Furthermore, the rising cost of raw asphalt bitumen is pushing end-users towards equipment capable of handling highly viscous, modified emulsions, thereby maximizing material efficacy and reducing operational costs.

Regional trends highlight the Asia Pacific (APAC) region as the dominant growth engine, fueled by massive national infrastructure programs in countries like India and China, alongside rapid urbanization across Southeast Asia. North America and Europe maintain stable demand, driven primarily by rehabilitation and repair work on extensive existing road networks, often requiring specialized, high-precision sprayers compliant with strict environmental standards. Segment trends reveal that the Truck-Mounted segment holds the largest market share due to its capacity and suitability for major highway projects, while the demand for Trailer-Mounted and handheld units is expanding rapidly within municipal and private maintenance sectors due to their cost-effectiveness and versatility.

The competitive landscape is characterized by established global machinery giants alongside specialized regional manufacturers. Strategic moves include mergers, acquisitions focused on technology integration (especially for calibration and GPS guidance), and extensive investment in after-sales service networks. The market is consolidating around efficiency, with superior fuel economy and low maintenance cycles becoming critical differentiators. Overall, the market outlook remains highly positive, supported by long-term governmental commitment to improving transportation logistics and ensuring roadway safety and quality standards across all geographies.

User inquiries regarding AI in the Asphalt Sprayer Market primarily revolve around how machine learning can optimize material consumption, enhance application precision, and facilitate predictive maintenance for the machinery itself. Key concerns include the feasibility of integrating complex AI algorithms into rugged construction environments and the return on investment for small-to-medium contractors. Users are seeking AI applications that can automatically adjust spray rates based on real-time surface temperature, texture variations, and speed, moving beyond simple calibration to dynamic process control. Expectations center on AI enabling autonomous operations for defined tasks (e.g., crack sealing preparation) and providing deep diagnostic insights into pump wear and nozzle efficiency, significantly reducing downtime and ensuring optimal pavement quality consistency across large projects.

The Asphalt Sprayer Market is shaped by a complex interplay of drivers, restraints, and opportunities that determine its long-term trajectory and competitive dynamics. The primary driver is the pervasive requirement for maintenance and repair of existing road infrastructure globally, which necessitates continuous deployment of spraying equipment for preventative treatments like chip sealing and fog sealing. This demand is further amplified by significant governmental policy shifts favoring public-private partnerships (PPPs) in infrastructure development, accelerating project timelines and increasing the need for specialized, high-efficiency machinery. Technological advancements, particularly in fuel efficiency, emission control, and automated calibration systems, also act as a strong driver, encouraging fleet renewal among contractors seeking operational cost reductions.

Conversely, the market faces significant restraints. Volatility in crude oil prices directly impacts the cost of liquid asphalt, leading to unpredictable procurement costs for end-users and fluctuating project budgets, potentially delaying or scaling back maintenance contracts. Furthermore, the availability of skilled labor capable of operating and maintaining technologically sophisticated sprayers poses a challenge, particularly in developing economies. Regulatory hurdles related to environmental protection, especially in mature markets, require continuous and costly redesign of equipment to comply with stricter noise and emission standards, raising the barrier to entry for smaller manufacturers and increasing product costs for consumers.

Opportunities for growth are predominantly concentrated in the modernization of municipal fleets and the expansion into niche applications such as airport paving and specialized industrial flooring. The adoption of sustainable road construction practices, including the use of bio-based binders or recycled asphalt pavement (RAP) treatments, creates a demand for specialized sprayers capable of handling non-traditional materials. The impact forces acting on the market—ranging from economic cycles influencing government budgets to shifts in material science—dictate that market players must prioritize agility, investing heavily in modular designs that can adapt to varying road materials and regulatory environments across different geographic markets. The balance between maximizing capacity (truck-mounted units) and optimizing maneuverability (trailer and handheld units) is a crucial competitive impact force.

The Asphalt Sprayer Market is comprehensively segmented based on three key dimensions: Type, Application, and Capacity. Analyzing these segments provides critical insights into purchasing trends and technological preferences across different end-user groups. The segmentation by Type primarily differentiates between equipment based on its mounting mechanism, influencing its portability, capacity, and suitability for varying project sizes. Application segmentation defines the ultimate use case, highlighting the demand generated by new construction versus essential maintenance, which typically requires different levels of precision and volume capability. Capacity segmentation is fundamental, distinguishing between small units used for minor repairs and massive distributors required for continuous highway work.

The value chain for the Asphalt Sprayer Market begins with the upstream procurement of essential raw materials and specialized components. Upstream activities involve sourcing high-grade steel and alloys for tanks and chassis, specialized heating elements (burners), pumping systems (positive displacement pumps are critical), and sophisticated hydraulic and electronic control components. Key suppliers are industrial metal producers, specialized pump manufacturers, and electronic system developers who provide the necessary technology for calibration and control. Maintaining consistent quality and negotiating stable supply contracts for these high-value components significantly impacts the final cost and reliability of the asphalt sprayer.

The mid-stream segment encompasses manufacturing, assembly, and testing. Manufacturers focus on optimizing chassis integration, ensuring the heating and insulation systems meet regulatory safety standards, and rigorously calibrating the spray bar systems for uniform flow and pressure. This stage is highly capital-intensive and requires specialized welding, fabrication, and quality assurance processes. Post-production, the distribution channel takes over, involving both direct sales to large construction companies and governmental bodies, and indirect sales through a network of specialized construction equipment dealers and rental companies. The effectiveness of the dealer network in providing local inventory, financing options, and immediate technical support is crucial for market penetration.

The downstream activities involve end-user deployment (construction companies, municipal public works departments), operation, and crucial after-market services, which include spare parts provision, maintenance, and periodic system recalibration. The profitability in the downstream is heavily influenced by the reliability of the equipment and the efficiency of the spare parts logistics. Direct distribution allows manufacturers better control over pricing and customer relationships, particularly for large, bespoke units. Indirect channels, through regional dealers, are vital for servicing geographically dispersed smaller contractors and providing essential local maintenance services, thereby closing the loop of the value chain through continuous customer support.

Potential customers for asphalt spraying equipment are predominantly entities involved in large-scale civil engineering, infrastructure development, and pavement maintenance. The primary end-users include governmental agencies, specifically national and regional departments of transportation (DOTs), which either own and operate their maintenance fleets or mandate the use of this equipment through contracting requirements. These public sector entities drive demand for high-capacity, robust truck-mounted distributors suitable for extensive highway networks and long-term asset management strategies focused on pavement preservation.

The second major segment comprises large private construction and civil engineering firms. These companies execute major infrastructure contracts (e.g., highway construction, toll road development) and require high-precision, technologically advanced sprayers to meet strict quality and timeline specifications. Their purchasing decisions are often influenced by machine longevity, operational efficiency (fuel economy), and integrated features like GPS-guided application mapping. These firms typically prefer truck-mounted and high-end trailer-mounted units to maximize productivity across varied work sites.

Finally, municipal public works departments and specialized pavement maintenance contractors form a crucial customer base, particularly for smaller, more maneuverable units (trailer-mounted and handheld). Municipalities focus on maintaining urban streets, parking lots, and local roads where capacity requirements are lower but precision in confined spaces is essential. Specialized maintenance contractors, often focused solely on chip sealing or crack filling, value versatility and low operational cost, driving demand for affordable, reliable entry-level and mid-range spraying equipment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1,450 Million |

| Market Forecast in 2033 | USD 2,150 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Rosco Manufacturing, Etnyre, Stepp Mfg., BearCat Manufacturing, KASI, KM International, Falcon Asphalt Repair Equipment, Crafco Inc., Bergkamp Inc., Power Curbers Companies, Midland Machinery Co., Chang'an Heavy Industry, FAYAT Group, Astec Industries, LeeBoy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution within the Asphalt Sprayer Market is centered on achieving unparalleled application accuracy, maximizing heating efficiency, and integrating digital control systems. One critical technology is the development of advanced variable spray bar controllers, which utilize sophisticated sensors to monitor vehicle speed, atmospheric temperature, and spray pressure simultaneously. This allows the system to instantaneously adjust the flow rate across different nozzles, ensuring a consistent application rate per square meter, regardless of minor fluctuations in vehicle speed. This level of precision is vital for meeting DOT specifications and is a significant improvement over older, manually calibrated systems, drastically reducing material wastage and optimizing cost efficiency on large projects.

Another pivotal technological area is the advancement in heating systems. Modern asphalt distributors employ highly efficient, indirect firing burners and sophisticated insulation materials to maintain the emulsion or bitumen at the optimal viscosity without overheating or localized scorching, which can compromise the material quality. Furthermore, integration of engine exhaust heat recirculation systems is becoming standard practice, enhancing fuel efficiency and reducing the thermal energy required from primary burners. These energy-saving technologies address both rising fuel costs and stricter environmental performance mandates, making the equipment more attractive to cost-conscious and sustainability-focused contractors.

The rise of telematics and GPS integration marks a transformation toward Smart Construction Equipment. Modern sprayers are equipped with onboard computers that log operational data, including the exact location, quantity of material sprayed, and application rate for every segment of the road. This data is transmitted in real-time to fleet management software, providing contractors and project owners with auditable proof of quality and compliance. Furthermore, electronic flowmeters, pressure transducers, and automated cleaning systems are now standard features, minimizing manual intervention, enhancing operator safety, and ensuring reliable performance across diverse liquid asphalt products, including polymer-modified binders.

The regional analysis of the Asphalt Sprayer Market reveals significant disparities in growth rates and technology adoption, primarily driven by varying levels of infrastructure maturity and government expenditure priorities. North America, encompassing the US and Canada, represents a mature market characterized by demand centered on replacement cycles and technologically advanced equipment. Infrastructure spending in this region is substantial, often focused on large-scale rehabilitation projects, particularly under recent long-term federal funding packages. Contractors in North America prioritize high-capacity, automated truck-mounted units featuring advanced GPS mapping and telematics integration to optimize efficiency and comply with stringent environmental standards, driving premium pricing and technological leadership.

Europe mirrors North America in its focus on maintenance, but with an added layer of regulatory complexity concerning emissions (Euro VI standards) and noise pollution. Demand here is stable, supported by extensive Trans-European Network (TEN-T) corridor upgrades and national road network preservation. The market exhibits strong interest in trailer-mounted and specialized low-emission units tailored for urban areas and smaller, specialized road maintenance tasks. Western European countries demonstrate high adoption of precision spraying technologies, while Eastern European nations show increasing growth rates as they expand and modernize their arterial road systems, often utilizing imported or licensed technology.

The Asia Pacific (APAC) region is the most dynamic and fastest-growing market globally. This exponential growth is fueled by massive infrastructure deficits, rapid urbanization, and government initiatives in key economies like India, China, and Indonesia dedicated to building new highways, rural roads, and economic corridors. While China remains the largest single market, showing strong demand for both imported high-tech and domestically manufactured cost-effective sprayers, countries in Southeast Asia are driving future growth. The APAC market accepts a broader spectrum of equipment, ranging from simple, robust, low-cost units to sophisticated high-capacity distributors, reflecting the diverse scale and complexity of projects undertaken.

Latin America (LATAM) and the Middle East and Africa (MEA) represent emerging markets with high potential, although growth is often subject to geopolitical and economic volatility. In the Middle East, high-volume infrastructure projects (e.g., smart city development, expansion of oil and gas transport routes) drive demand for very high-capacity, durable sprayers capable of operating reliably in extreme temperatures. African markets, particularly those benefiting from increased foreign direct investment (FDI) in mining and road connectivity, show high reliance on versatile, rugged, and easy-to-maintain trailer-mounted units. The focus in these regions is on building basic road networks and enhancing connectivity rather than just preservation, making them critical targets for global manufacturers seeking untapped demand.

The predominant growth factor is the global increase in governmental investment toward road infrastructure maintenance, particularly preventative pavement treatments such as chip sealing and fog sealing, aimed at extending the lifespan of existing road networks efficiently.

Modern sprayers utilize advanced electronic control systems coupled with GPS and real-time speed sensors. These systems dynamically adjust pump output and spray bar pressure to ensure a precise, consistent application rate per unit area, minimizing material waste and ensuring compliance with engineering specifications.

Truck-mounted asphalt distributors dominate the market, especially in major highway construction and large-scale rehabilitation projects, due to their superior tank capacity (often exceeding 2,500 gallons), high operational speed, and robust capabilities for long-haul application.

Crude oil price volatility directly affects the cost of asphalt bitumen (the primary spraying material). High material costs can lead public and private entities to defer non-essential maintenance projects, potentially constraining short-term demand for new spraying equipment.

The future landscape is being shaped by integrated telematics for fleet management, AI-driven calibration systems for dynamic rate adjustment, and enhanced heating technology focused on fuel efficiency and low emissions, facilitating smarter and more sustainable paving practices.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.