ID : MRU_ 432273 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

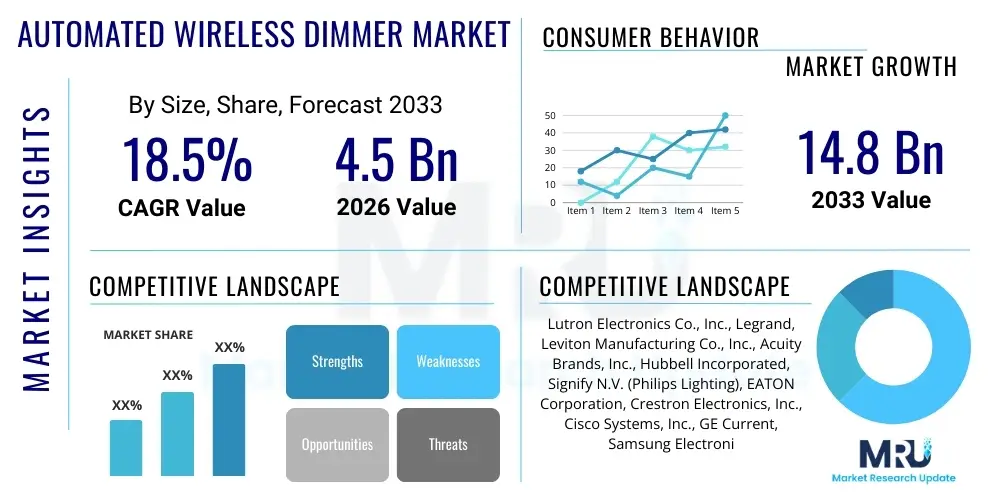

The Automated Wireless Dimmer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 14.8 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the accelerated adoption of smart home technologies globally, coupled with a pervasive focus on energy conservation measures across residential and commercial infrastructures. The increasing affordability and ease of integration of IoT-enabled lighting solutions are key factors enabling this exponential market trajectory.

The Automated Wireless Dimmer Market encompasses devices and systems designed to modulate the brightness of lighting fixtures remotely or autonomously without the need for physical wiring between the controller and the fixture. This technology represents a crucial component within the broader ecosystem of smart lighting and the Internet of Things (IoT). Products typically integrate standard communication protocols such as Wi-Fi, Zigbee, Z-Wave, or Bluetooth to facilitate seamless connectivity and control through centralized hubs, mobile applications, or voice assistants. The primary function is to enhance user convenience, improve ambiance, and, critically, achieve significant energy savings by optimizing light levels based on ambient conditions or pre-set schedules.

Major applications span both the residential sector—where consumers seek integrated smart home experiences for comfort and security—and the commercial sector, including offices, retail spaces, and hospitality environments that prioritize operational efficiency and compliance with green building standards. These systems offer dynamic control over illumination, allowing users to create complex scenes and schedules that respond automatically to time of day, occupancy, or incoming natural light levels. This adaptability provides substantial benefits, moving beyond simple on/off switching to sophisticated light management.

The market is primarily driven by the falling costs of sensor technology and microcontrollers, standardized communication protocols, and the increasing consumer awareness regarding the long-term cost benefits associated with smart lighting systems. Furthermore, regulatory mandates promoting energy efficiency in new construction and retrofitting projects significantly bolster demand for automated dimming solutions. The convergence of lighting control with security systems and HVAC management through centralized smart platforms positions wireless dimmers as an indispensable element of modern building automation.

The Automated Wireless Dimmer Market is undergoing rapid transformation, characterized by intense technological competition and strategic acquisitions aimed at expanding interoperability across different smart home ecosystems. Business trends indicate a strong shift towards subscription-based services accompanying hardware installation, offering advanced features like predictive maintenance and detailed energy analytics. Major players are focusing on open standards, such as Matter, to overcome historical compatibility challenges, thus accelerating mainstream adoption in multi-vendor environments. The residential segment, particularly the DIY and mid-range market, is experiencing explosive growth, fueled by affordable starter kits and simplified installation processes.

Regionally, North America and Europe currently dominate the market due to high disposable incomes, mature smart home infrastructure, and stringent government regulations pushing for energy efficiency in commercial buildings. However, the Asia Pacific (APAC) region is projected to register the highest growth rate during the forecast period, driven by massive urbanization, rapid infrastructure development, and growing consumer interest in intelligent building management systems in countries like China and India. Latin America and the Middle East & Africa (MEA) represent emerging markets where the demand is primarily concentrated in luxury residential projects and large-scale hospitality developments.

In terms of segmentation, technology based on Zigbee and proprietary mesh networks holds significant market share due to robustness and low power consumption, especially crucial for large installations. However, Wi-Fi and Bluetooth mesh technologies are gaining traction, capitalizing on ease of deployment and integration with existing networking infrastructure. Application-wise, the commercial segment, despite facing higher initial investment hurdles, offers greater long-term market potential due to the scale and complexity of installations, where optimized lighting management translates directly into massive operational savings. This continuous evolution necessitates manufacturers to prioritize modularity and backward compatibility in their product development strategies.

User inquiries regarding AI's influence on the Automated Wireless Dimmer Market frequently center on themes such as predictive behavior, energy optimization, and the personalization of lighting experiences. Users are concerned about how AI can move beyond simple scheduled dimming to anticipating human needs, adapting light based on tasks (e.g., reading vs. watching TV), and truly minimizing energy waste without human intervention. Common questions explore the transition from rule-based automation to adaptive, machine-learning driven control, the necessary data privacy implications, and the role of Edge AI in ensuring real-time responsiveness. The primary expectation is that AI integration will make dimming systems invisible, highly intuitive, and significantly more efficient, reducing the complexity often associated with sophisticated smart home configurations. This summarizes a widespread desire for autonomous, hyper-personalized, and highly efficient lighting management.

The Automated Wireless Dimmer Market is propelled by powerful drivers centered on energy conservation mandates and the explosive growth of the Internet of Things (IoT). The core restraint remains the historical fragmentation of connectivity standards and the high initial capital expenditure compared to traditional lighting systems. Opportunities are significantly expanding through the development of cross-platform standards like Matter, enabling seamless integration across diverse ecosystems, and the large untapped potential in retrofitting older commercial infrastructure. These forces collectively shape the competitive landscape, pushing manufacturers toward greater innovation in security and interoperability. The primary impact force is the strong synergy between governmental push for sustainability and consumer demand for technologically sophisticated living and working environments.

The Automated Wireless Dimmer Market is comprehensively segmented based on technology, product type, application, and communication protocol, reflecting the diverse needs of end-users and the complexity of installation environments. This segmentation is crucial for vendors to tailor products specifically for residential or commercial use, ensuring optimal performance and cost efficiency. Key differentiating factors include the communication range, power requirements, network topology support (mesh vs. star), and compatibility with major smart home ecosystems. Understanding these segments allows for targeted marketing and efficient resource allocation in product development, especially concerning the balance between proprietary and open-source standards.

The value chain for the Automated Wireless Dimmer Market begins with upstream suppliers providing critical electronic components, including semiconductors, microprocessors, RF modules, and specific aesthetic materials like specialized polymers and casings. Manufacturing involves intricate processes of circuit board assembly, firmware development, and quality control testing to ensure robust wireless connectivity and precise dimming calibration. Midstream activities are dominated by specialized system integrators and software developers who create the interoperability platforms and user interfaces necessary for practical application. These integrators are pivotal as they bridge the gap between diverse hardware protocols and end-user needs, often providing customized solutions for complex commercial projects.

Downstream activities involve a diverse array of distribution channels, ranging from traditional electrical wholesalers and home improvement retailers to high-growth e-commerce platforms and direct-to-consumer sales. The channel choice significantly impacts product reach and technical support requirements. Direct channels, particularly through professional electrical contractors and IoT system integrators, dominate the high-value commercial and industrial segments, ensuring expert installation and long-term maintenance contracts. Indirect channels, primarily online and brick-and-mortar retail, cater more effectively to the mass-market residential DIY segment, prioritizing ease of installation and competitive pricing.

This structure emphasizes the increasing importance of software and service provision over purely hardware manufacturing. Value creation is heavily concentrated in the integration layer, where companies focus on proprietary algorithms for energy management and seamless compatibility across platforms (e.g., Amazon Alexa, Google Home, Apple HomeKit). Successful market players maintain tight control over their software stack while collaborating aggressively with protocol alliances (like Zigbee Alliance and the Connectivity Standards Alliance) to maintain relevance in a rapidly unifying technological landscape.

The primary end-users and buyers of automated wireless dimmers are broadly categorized into four groups: residential consumers, commercial facility managers, hospitality industry operators, and institutional entities like healthcare and education facilities. Residential consumers, particularly those undertaking new builds or renovations, seek these products primarily for enhanced convenience, personalized ambiance settings, and tangible monthly energy savings. The modern homeowner views integrated smart lighting as essential to the overall value and comfort of their property, driving adoption of user-friendly, aesthetically pleasing solutions.

Commercial real estate owners and facility managers constitute a highly profitable segment, driven by the operational necessity of reducing energy overheads, complying with environmental sustainability mandates (such as LEED certification), and improving tenant satisfaction. For these large-scale deployments, the ability of wireless systems to provide centralized control, detailed energy usage reports, and zone-specific scheduling without disruptive structural wiring is paramount. Reliability, scalability, and integration with Building Management Systems (BMS) are the critical purchasing criteria for this customer base.

The hospitality and healthcare sectors utilize automated dimming for specialized purposes. Hotels use dynamic lighting to enhance guest experience, setting specific scenes for arrival, relaxation, and sleep, thereby reinforcing brand luxury and optimizing operational staff efficiency. Healthcare facilities, conversely, leverage sophisticated dimming and color tuning (human-centric lighting) to align with circadian rhythms, supporting patient recovery and improving staff vigilance. These institutional buyers require robust, secure, and highly customizable systems that meet stringent regulatory requirements regarding safety and system uptime.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 14.8 Billion |

| Growth Rate | CAGR 18.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lutron Electronics Co., Inc., Legrand, Leviton Manufacturing Co., Inc., Acuity Brands, Inc., Hubbell Incorporated, Signify N.V. (Philips Lighting), EATON Corporation, Crestron Electronics, Inc., Cisco Systems, Inc., GE Current, Samsung Electronics Co., Ltd., Xiaomi Corporation, Schneider Electric SE, Honeywell International Inc., ABB Ltd., Nexia Intelligence, Inc., TP-Link Corporation Limited, Develco Products, Enerlites, Inc., Loxone Electronics GmbH. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Automated Wireless Dimmer Market is defined by the ongoing standardization and maturation of wireless communication protocols designed for mesh networking and low power consumption. Zigbee and Z-Wave have historically dominated due to their robust mesh capabilities, which extend network range and reliability, crucial for large residential and commercial installations. However, the introduction and rapid adoption of Bluetooth Low Energy (BLE) Mesh are challenging this dominance by leveraging the ubiquity of Bluetooth in modern mobile devices, simplifying initial setup and reducing reliance on dedicated gateways. Furthermore, standard Wi-Fi is being adapted for lighting control through specialized chips that balance power efficiency with the convenience of native IP connectivity.

A transformative development is the widespread industry commitment to Matter (formerly Project CHIP), a unified connectivity standard led by the Connectivity Standards Alliance (CSA). Matter aims to solve the chronic interoperability issues that have historically hampered smart home growth, providing a seamless, secure, and reliable communication protocol across various manufacturers and ecosystems (e.g., Apple HomeKit, Google Home, Amazon Alexa). The integration of Matter directly into new wireless dimmer hardware is expected to significantly accelerate consumer confidence and market expansion by reducing platform lock-in and installation friction. This shift toward a singular, open standard represents a monumental leap in the technological framework of automated dimming.

Beyond connectivity, advancements in semiconductor technology and Edge Computing are enabling dimmers to become smarter and more energy-efficient. Modern microcontrollers now support complex Artificial Intelligence (AI) and Machine Learning (ML) algorithms that run locally (at the edge), allowing for instantaneous decisions regarding dimming levels, occupancy sensing, and fault reporting without needing constant cloud communication. This local processing capability is vital for both enhancing security, by minimizing data transmission, and ensuring real-time responsiveness, essential for creating safe and effective lighting control experiences. The adoption of Human-Centric Lighting (HCL) systems, which require precise control over color temperature and intensity, further relies on these sophisticated control mechanisms embedded within the dimmer unit itself.

While Zigbee and Z-Wave offer robust, mesh-network security layers suitable for high-integrity installations, the emerging Matter standard is projected to offer the highest standardized security baseline. Matter utilizes best-in-class cryptographic practices and integrates with existing smart home ecosystems securely, enhancing data protection at both the device and network level. Selecting systems that allow for local, encrypted control (Edge Computing) also significantly mitigates external cyber threats, making them highly secure for sensitive commercial applications.

Automated wireless dimmers maximize energy savings by implementing precise scheduling, daylight harvesting, and occupancy-based control. Daylight harvesting sensors automatically dim artificial light when sufficient natural light is present, minimizing electricity use. Furthermore, network-wide optimization allows facility managers to precisely monitor and control consumption across vast spaces, often resulting in 40-60% lighting energy reduction compared to traditional manual systems, leading to rapid Return on Investment (ROI) for building owners.

The primary challenge is the historical fragmentation of proprietary and competing wireless standards (e.g., needing separate hubs for Zigbee, Z-Wave, and Wi-Fi devices). This forces consumers and integrators to manage complex, multi-protocol setups. However, the anticipated rollout and adoption of the Matter standard are poised to drastically simplify this landscape by providing a universally compatible application layer, allowing devices from different brands to communicate seamlessly without proprietary bridge requirements.

Yes, modern wireless dimmer systems are highly suitable for large-scale industrial applications due to the robust nature of mesh networking protocols like Zigbee and specialized proprietary mesh technologies. These protocols ensure high signal reliability over expansive areas and can manage hundreds of devices from a single network infrastructure. They offer critical advantages in industrial settings by facilitating zone control, high-bay lighting optimization, and real-time fault reporting, thereby minimizing downtime and maintenance costs.

AI is fundamental to the future of automated dimmers, shifting them from scheduled control to predictive, adaptive intelligence. Future dimmers will utilize AI and Machine Learning to learn human habits, analyze atmospheric and natural light data, and proactively adjust light levels and color temperature for optimal comfort and maximum energy efficiency, effectively creating a self-regulating, human-centric lighting environment that adapts continuously to nuanced requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.