ID : MRU_ 432994 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

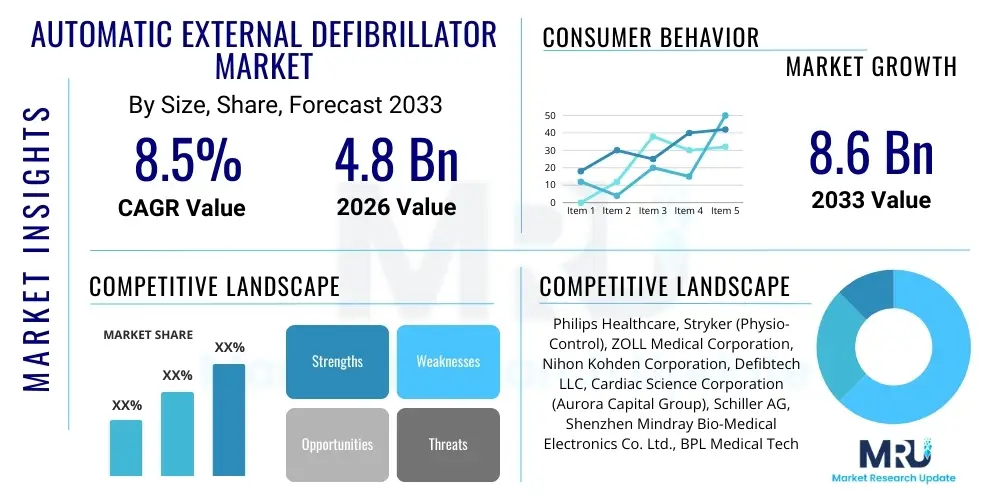

The Automatic External Defibrillator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 8.6 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global incidence of sudden cardiac arrest (SCA), combined with crucial public health initiatives mandating the placement of AEDs in public spaces, educational institutions, and corporate environments. Regulatory support and increased awareness regarding the importance of immediate bystander intervention are critical accelerators for market valuation growth.

The Automatic External Defibrillator (AED) Market encompasses devices used to treat sudden cardiac arrest (SCA) by delivering an electric shock to restore normal heart rhythm. These sophisticated, portable devices are designed for use by laypersons or minimally trained responders, providing immediate life-saving capability outside traditional hospital settings. AEDs automatically analyze the patient's heart rhythm, determine if a shockable rhythm (ventricular fibrillation or pulseless ventricular tachycardia) is present, and guide the user through the defibrillation process via voice prompts and visual cues. The inherent simplicity and effectiveness of these devices make them indispensable tools in the public health infrastructure focused on improving survival rates from SCA.

Major applications of AEDs include public access defibrillation (PAD) programs implemented in airports, schools, stadiums, fitness centers, and government buildings, as well as deployment within emergency medical services (EMS), hospitals, and corporate safety programs. The primary benefit of widespread AED deployment is the drastic reduction in time-to-defibrillation, which is the single most critical factor determining survival outcomes following SCA. As every minute delay reduces the chances of survival by approximately 10%, immediate accessibility of AEDs translates directly into saved lives. The market is heavily driven by increasing regulatory pressure across developed nations to make these devices readily available, coupled with technological advancements resulting in lighter, more durable, and increasingly connected devices.

Driving factors propelling market expansion include rising awareness campaigns globally, government investments in public health infrastructure, and the demographic shift toward an aging population susceptible to cardiovascular diseases. Furthermore, the advent of advanced connectivity features, such as remote monitoring and integration with electronic health records (EHRs), enhances the efficiency and maintenance of AED units, ensuring readiness when required. The market structure features intense competition focused on device reliability, ease of use, battery life, and cost-effectiveness for large-scale procurement, emphasizing the importance of innovation in electrode technology and energy delivery systems.

The Automatic External Defibrillator (AED) Market is characterized by robust growth, primarily fueled by global mandates for public access defibrillation (PAD) and significant technological integration, particularly in connectivity and data management. Business trends show a strong shift toward maintenance and subscription models for public-use AED fleets, ensuring compliance and operational readiness. Key industry movements include strategic mergers and acquisitions focused on consolidating technological capabilities in advanced monitoring systems and expanding global distribution networks. Manufacturers are increasingly emphasizing the development of pediatric-specific AED capabilities and implementing sophisticated battery management systems to reduce total cost of ownership, making AED implementation viable for smaller organizations.

Regionally, North America remains the dominant market, driven by established reimbursement policies, stringent regulatory requirements, and high public health expenditure. However, the Asia Pacific (APAC) region is poised for the highest growth trajectory due to improving healthcare infrastructure, massive population density, and growing government initiatives in countries like India and China to curb cardiac mortality rates. European growth is steady, supported by established PAD programs and high adoption rates in workplaces and transportation hubs. A crucial regional trend involves localized manufacturing and supply chain resilience to address varying electrical standards and regulatory approvals across diverse geographical markets.

Segmentation trends highlight the increasing demand for semi-automatic AEDs, favored for their balance between user intervention and automation, especially in highly trafficked public areas. Furthermore, the accessories segment, including batteries, pads, and carrying cases, is exhibiting high growth due to the recurring nature of replacements, which is vital for device upkeep and safety. The increasing adoption of connected AEDs, capable of real-time data transmission and location tracking, represents a significant segment shift, transforming the devices from standalone rescue tools into integrated components of broader emergency response ecosystems. This connectivity allows EMS to better track device locations and status, significantly improving response coordination.

Common user inquiries regarding the impact of Artificial Intelligence (AI) on the Automatic External Defibrillator market center predominantly on three areas: accuracy in rhythm analysis, predictive maintenance, and integration into larger smart city emergency networks. Users frequently ask if AI can reduce false positive or negative shock recommendations, thereby increasing device efficacy and minimizing risk. They also express strong interest in how AI algorithms can predict battery and pad failure before human inspection, ensuring continuous readiness of PAD units. Furthermore, there is anticipation regarding AI’s role in optimizing the geographic placement of AEDs based on real-time population density, cardiac risk mapping, and traffic flow data, thereby maximizing access during an emergency. The consensus expectation is that AI will enhance reliability, automate logistics, and fundamentally integrate AED deployment planning with public health data systems.

The Automatic External Defibrillator market is shaped by powerful forces encompassing increasing global health consciousness (Driver), stringent and time-consuming regulatory approval processes (Restraint), and the development of integrated, wearable cardiac monitors (Opportunity). The primary impact forces driving growth include mandatory public access defibrillation laws enacted by governments worldwide, especially in high-traffic zones. Conversely, the high initial acquisition cost of advanced AEDs and the associated ongoing costs of training, maintenance, and disposable accessories (pads and batteries) often act as significant barriers, particularly in emerging economies or for small organizations attempting to comply with PAD mandates. Successful market navigation requires manufacturers to address cost sensitivity while rigorously adhering to global medical device standards and reliability expectations.

Key drivers include the dramatic rise in cardiovascular disease prevalence attributable to lifestyle changes, obesity, and an aging population, making SCA a major public health concern globally. Furthermore, continuous technological advancements, such as biphasic waveform technology, improved battery longevity, and lightweight designs, enhance device portability and user confidence. Regulatory incentives and large-scale public safety initiatives, often involving subsidies or tax breaks for AED purchases, substantially increase procurement volume across institutional and corporate sectors, thereby mitigating the financial restraints associated with initial deployment.

However, major restraints include issues related to device recalls and safety alerts, which erode consumer and institutional trust, necessitating highly rigorous quality control measures throughout the manufacturing process. Furthermore, the lack of widespread, standardized lay rescuer training in many regions limits the effectiveness of deployed AED units, as untrained bystanders may hesitate to use the device, delaying crucial intervention. Opportunities abound in expanding into non-traditional markets like home use for high-risk individuals and leveraging telecommunications infrastructure to create fully connected, remotely managed AED networks. The development of advanced shock advisory systems based on sophisticated algorithms presents a crucial growth avenue for market differentiation.

The Automatic External Defibrillator (AED) market is extensively segmented based on device type, end-user, and distribution channel, reflecting diverse application requirements and procurement mechanisms globally. Device segmentation primarily divides the market into semi-automatic and fully automatic AEDs, where semi-automatic devices, requiring the user to press a button to deliver the shock, generally dominate professional and trained public access environments, while fully automatic devices, which deliver the shock autonomously, gain traction in areas where minimal user training is available. The underlying trend in segmentation is a growing emphasis on connectivity features and ease of data transfer, enhancing the value proposition across all segments regardless of automation level. Furthermore, the accessories market segment, including electrode pads and batteries, forms a crucial recurring revenue stream, intrinsically linked to the installed base of defibrillators.

End-user segmentation is critical, reflecting the varied needs of major purchasers ranging from hospitals and pre-hospital EMS to the significant and rapidly growing Public Access Defibrillation (PAD) segment, which includes transportation systems, schools, and corporate offices. The hospital segment demands advanced features, seamless integration with existing clinical monitoring systems, and robust data storage capabilities, often prioritizing devices with manual override options. In contrast, the PAD segment prioritizes ruggedness, intuitive design, long battery life, and often remote monitoring capabilities to ensure compliance and readiness, driving demand for simple, highly reliable units suitable for untrained bystanders.

The comprehensive understanding of segmentation allows manufacturers to tailor marketing strategies and product development efforts. For instance, catering to the burgeoning market for specialized electrodes for pediatric patients represents a high-growth niche within the accessories segment. Furthermore, the segmentation by distribution channel reveals a preference for direct sales to large hospital chains and government procurement bodies, whereas distribution through third-party specialized medical device distributors remains dominant for reaching smaller businesses and individual public venues. Future growth is anticipated to be heavily concentrated in the pre-hospital and public access settings, driven by regulatory mandates and societal demand for improved cardiac safety.

The value chain for the Automatic External Defibrillator market is complex, beginning with upstream activities focused on specialized component sourcing, design, and sophisticated manufacturing, moving through rigorous distribution, and culminating in post-sales services and recycling. Upstream analysis highlights the reliance on highly specialized suppliers for critical components, including high-capacity, long-life lithium batteries, precision sensors for ECG monitoring, and proprietary microprocessors capable of rapid rhythm analysis and energy management. Research and Development (R&D) forms the most crucial upstream activity, driving innovation in waveform technology, connectivity, and miniaturization. The need for strict adherence to quality management systems (ISO 13485) throughout the component manufacturing process adds complexity and cost to the initial stages.

Midstream activities involve the assembly and testing of the final AED device, followed by the crucial, time-intensive process of regulatory approval (e.g., FDA PMA or 510(k), CE Mark). Manufacturing efficiency and scalability are key competitive differentiators at this stage. Downstream analysis focuses on distribution and logistics, involving a mix of direct sales channels, especially to large government or military buyers and major healthcare organizations, and indirect sales through specialized medical device distributors and resellers who handle regional inventories and localized customer support. The efficiency of the distribution network is critical for ensuring that units reach public access locations quickly and that replacement accessories are readily available to minimize device downtime.

The distribution channel structure heavily favors specialized indirect distribution due to the requirement for product knowledge, local training support, and necessary certification documentation. Direct sales, however, are preferred for high-volume, standardized contracts where customization is minimal. Post-sales services, including warranty, maintenance contracts, and mandatory training sessions for end-users, contribute significantly to the total lifetime value of the customer relationship. The increasing shift towards connected devices necessitates robust IT infrastructure for remote monitoring and data management services, adding a layer of technological service provision to the traditional value chain model. Overall, the value chain is characterized by high value addition in R&D and post-sales service delivery.

The potential customer base for Automatic External Defibrillators is extremely broad, spanning professional healthcare providers, essential services, governmental bodies, and private sector enterprises focused on compliance and employee safety. End-users are primarily categorized into those focused on emergency response (EMS, hospitals) and those focused on preventative public safety (PAD placements). Hospitals and clinics represent a foundational customer segment, requiring advanced, often manual, or semi-automatic devices for immediate resuscitation efforts within clinical settings, prioritizing integration with patient monitoring systems and detailed post-event data retrieval capabilities for clinical analysis and quality assurance.

The largest and fastest-growing customer segment is the Public Access Defibrillation (PAD) market, encompassing diverse environments such as commercial airlines, rail networks, airports, schools, universities, fitness centers, large manufacturing plants, and corporate campuses. These buyers prioritize devices that are rugged, highly visible, require minimal training, and offer straightforward maintenance notifications, often procuring through bulk tenders managed by safety or facilities management departments. Regulatory mandates, such as those requiring AED placement in schools or athletic venues, are the primary purchasing catalyst for this segment.

Furthermore, specialized end-users, including military installations, police departments, and fire services, constitute another significant customer base, demanding durable, highly reliable units suitable for extreme operational environments. The emerging segment of home use, targeting individuals with known high cardiac risk factors or those residing in remote areas with slow EMS response times, represents future growth potential, driven by technological advancements making AEDs simpler and more affordable for personal use. Overall, any institution responsible for the safety of a large number of people constitutes a primary potential buyer, with purchasing decisions heavily influenced by liability concerns and adherence to occupational safety regulations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.6 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Philips Healthcare, Stryker (Physio-Control), ZOLL Medical Corporation, Nihon Kohden Corporation, Defibtech LLC, Cardiac Science Corporation (Aurora Capital Group), Schiller AG, Shenzhen Mindray Bio-Medical Electronics Co. Ltd., BPL Medical Technologies, Metrax GmbH, Mediana Co. Ltd., CU Medical Systems Inc., HeartSine Technologies (St. Jude Medical/Abbott), Progetti S.r.l., Bexen Medical, A.M.I. Italia, Avic International Holding Corporation, Primedic GmbH, Bionet Co. Ltd., Schiller India Pvt. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Automatic External Defibrillator market is rapidly evolving, driven by the core objectives of improving efficacy, enhancing user-friendliness, and enabling connectivity. The dominant technology utilized is biphasic waveform delivery, which significantly improves defibrillation success rates while reducing the energy required compared to older monophasic technology, thus minimizing potential myocardial damage. Modern AEDs incorporate advanced algorithms for analyzing ECG rhythms, ensuring precise determination of shockable conditions and minimizing the likelihood of inappropriate shock delivery, enhancing patient safety. Miniaturization and increased battery efficiency, often utilizing specialized lithium compounds, allow devices to be lighter, more portable, and capable of long periods of readiness without frequent maintenance checks, essential for PAD placements.

A major technological trend transforming the market is the integration of Internet of Things (IoT) and wireless connectivity. Connected AEDs utilize Wi-Fi or cellular networks to perform self-tests, report operational status (battery life, pad expiration, physical location), and automatically transmit post-event data to EMS or clinical review teams. This connectivity ensures that deployed AEDs are always rescue-ready, drastically reducing the high rate of non-functional devices found in public surveys. Furthermore, many devices are now incorporating sophisticated GPS and location-based services, allowing emergency dispatchers and nearby responders to quickly locate the nearest operational AED during a cardiac event, optimizing coordination in complex urban environments.

Future technological advancements are focused on creating highly adaptive and personalized defibrillation protocols. This includes research into utilizing AI and machine learning to interpret complex cardiac signals more accurately under noisy conditions, and developing electrode technology that provides better skin contact and signal quality across diverse patient demographics (varying skin resistance and body types). The rise of Wearable Cardioverter Defibrillators (WCDs) represents a convergence of monitoring and therapeutic technology, providing continuous protection for high-risk patients awaiting permanent implantable solutions. This ongoing innovation ensures that AEDs remain at the forefront of emergency cardiovascular care.

Regional dynamics play a crucial role in shaping the Automatic External Defibrillator Market, with significant differences in regulatory frameworks, healthcare expenditure, public awareness, and adoption rates across the globe. North America, encompassing the United States and Canada, currently holds the largest market share. This dominance is attributed to a high incidence of cardiovascular diseases, well-established and standardized emergency medical services (EMS), robust reimbursement policies, and proactive government legislation mandating AED placement in numerous public and commercial settings. The U.S. market, in particular, benefits from a high level of consumer awareness and substantial investment in advanced technological integration, including connected AED networks and predictive maintenance services, driving demand for premium, feature-rich devices.

Europe represents the second-largest market, characterized by stringent European Union medical device regulations (MDR) and a strong commitment to public health safety, particularly in Western European countries such as Germany, the UK, and France. These nations have highly mature Public Access Defibrillation (PAD) programs supported by national health services and public safety campaigns. Growth in Europe is steady, driven by the replacement cycle of older AED units and the expansion of PAD initiatives into smaller communities and residential areas. Eastern European nations are exhibiting rapid growth, albeit from a smaller base, as they invest significantly in modernizing their pre-hospital care infrastructure and adopting European standards for public safety equipment, often preferring cost-effective yet reliable devices.

The Asia Pacific (APAC) region is projected to register the fastest growth rate during the forecast period. This rapid expansion is driven by massive untapped market potential in highly populated countries like China, India, and Japan, where increasing affluence, rising prevalence of sedentary lifestyles, and rapidly improving healthcare access are driving demand. Governments in APAC are increasingly prioritizing public safety, leading to pilot programs and mandates for AED placement in major metropolitan hubs. While regulatory approval processes can be fragmented across the region, increasing foreign investment in healthcare infrastructure and favorable local manufacturing policies are accelerating market entry and widespread adoption of both basic and advanced AED models. Latin America and the Middle East & Africa (MEA) regions lag slightly in adoption but show promising growth tied to infrastructural developments in tourism, transportation, and industrial sectors, where occupational health and safety standards are being elevated.

Semi-Automatic AEDs require the rescuer to analyze the heart rhythm and then physically press a button to deliver the shock upon device prompt. Fully Automatic AEDs analyze the rhythm and deliver the shock automatically without rescuer input once the device is ready. Currently, Semi-Automatic AEDs generally dominate the market due to their prevalence in EMS and trained public access environments, offering an additional layer of human control and assessment before discharge, although demand for fully automatic units is rising in minimally trained public settings.

Regulatory compliance is a critical demand driver, particularly for Public Access Defibrillation (PAD) markets. Government mandates in regions like North America and Europe require the installation of AEDs in specific locations such as airports, schools, and large commercial facilities. These regulations create substantial, sustained procurement needs, fundamentally impacting market size and forcing manufacturers to adhere to extremely high standards of quality assurance and reliable performance documentation (e.g., FDA clearance and CE marking).

Connectivity is essential for ensuring AED readiness, transforming the market from simple device sales to integrated service models. IoT-enabled AEDs perform automatic self-checks and transmit vital status information (battery life, pad expiration, functional status) remotely to monitoring platforms. This drastically reduces the risk of device failure during an emergency, supports predictive maintenance strategies, and ensures compliance with regulatory operational standards, making connected devices the expected norm for institutional buyers.

The Asia Pacific (APAC) region, specifically emerging economies within it, demonstrates the highest growth potential. This rapid expansion is fueled by increasing investments in healthcare infrastructure, urbanization leading to densely populated areas requiring organized emergency response, and a growing middle class with higher health awareness. As governments in countries like China and India implement public health campaigns and local manufacturing initiatives, the adoption rate of AEDs is expected to surge significantly faster than in mature markets.

The primary recurring costs associated with AED ownership revolve around disposable accessories and mandatory services. These include the routine replacement of electrode pads (which expire typically every two years) and the replacement of specialized lithium batteries (which can last 2 to 5 years, depending on usage and model). Additionally, costs encompass mandatory refresher training for lay rescuers, and increasingly, subscription fees for remote monitoring and data management services required to ensure regulatory compliance and operational readiness.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.