ID : MRU_ 431740 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

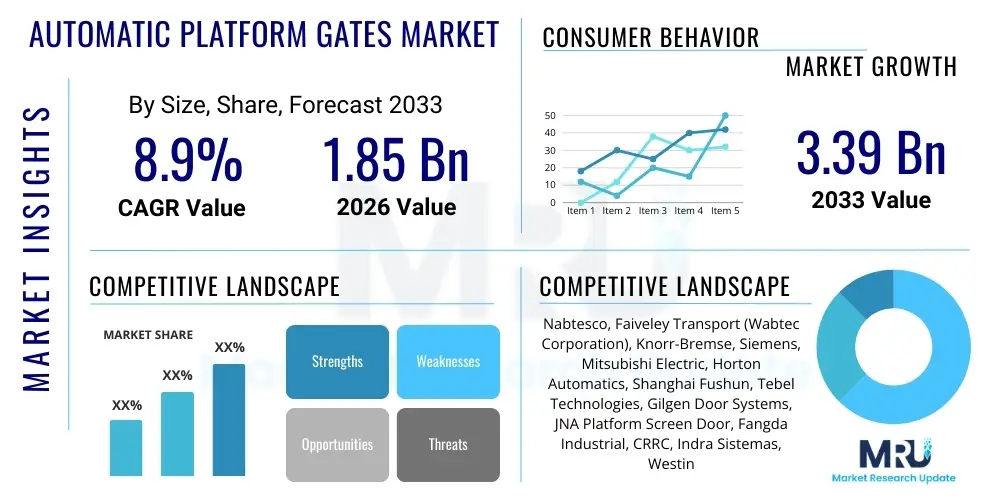

The Automatic Platform Gates Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2026 and 2033. The market is estimated at USD 1.85 billion in 2026 and is projected to reach USD 3.39 billion by the end of the forecast period in 2033.

The Automatic Platform Gates (APG) Market encompasses the infrastructure and associated systems designed to enhance passenger safety and operational efficiency within urban rail networks, primarily metros, subways, and commuter rail systems. APGs, also known as Platform Screen Doors (PSD) or Platform Edge Doors (PED), serve as physical barriers installed at the platform edge to prevent accidental falls onto the tracks, unauthorized track access, and wind gusts generated by passing trains. These systems are crucial components of fully automated railway lines (GoA Level 4) and are increasingly adopted in semi-automated and conventional lines upgrading their safety profiles.

The core product offerings include full-height Platform Screen Doors (PSDs), which enclose the entire platform area up to the ceiling, and half-height Automatic Platform Gates (APGs), which typically extend 1.5 to 1.8 meters high. Major applications span high-density urban transit environments where maximizing throughput and minimizing disruptions are paramount. Key benefits derived from APG deployment include a significant reduction in platform incidents, improved ventilation control, precise train stopping alignment due to integrated signaling, and enhanced psychological comfort for commuters.

The primary driving factors propelling this market expansion include stringent global regulatory mandates emphasizing passenger safety in public transport, the global proliferation of automated train operation (ATO) systems requiring precise docking, and substantial infrastructural investments in extending and modernizing existing metro lines, particularly across the Asia Pacific region. Furthermore, growing urbanization and the resultant overcrowding on platforms necessitate automated solutions to manage passenger flow safely and efficiently.

The Automatic Platform Gates Market is characterized by robust growth fueled primarily by global metropolitan expansion and regulatory emphasis on transit safety. Business trends indicate a strong shift towards half-height gate systems due to their lower installation costs and suitability for retrofitting older railway infrastructure, although full-height PSDs remain the standard for new, fully automated lines, especially in densely populated Asian cities. Leading industry players are focusing heavily on integrating advanced IoT sensors and predictive maintenance algorithms into gate operating mechanisms to minimize downtime and improve reliability, transforming maintenance from reactive to proactive, which provides a significant competitive edge.

Regionally, the Asia Pacific dominates the market landscape, driven by massive new metro construction projects in China, India, and Southeast Asia, where rapid urbanization demands high-capacity, safe transit solutions. Europe represents a mature but steady growth market, focusing on upgrading existing lines to comply with modern accessibility standards (e.g., TRAM/PRM standards) and implementing sophisticated communication-based train control (CBTC) systems that necessitate integrated APGs. North America's market growth is slower but concentrated on retrofitting existing urban systems in major cities like New York and Toronto, emphasizing resilient, vandal-resistant designs.

Segment trends reveal that the 'Sliding Doors' mechanism dominates due to its reliability and proven operational history, while 'Half-Height Gates' are gaining momentum in terms of volume of deployment, particularly in cost-sensitive markets. The Application segment remains overwhelmingly concentrated in the metro and subway sector, though high-speed rail stations are starting to adopt simplified variants for controlled boarding access. Future growth hinges on successful integration with next-generation train signaling and the development of modular, easily deployable systems suitable for varied architectural contexts.

User questions regarding AI's impact on Automatic Platform Gates (APG) primarily revolve around how these sophisticated systems can move beyond simple mechanical operation to offer intelligent safety and operational management. Common themes include queries about real-time fault prediction, optimized maintenance scheduling using machine learning (ML), and AI-driven passenger flow management during peak hours. Users are particularly concerned with whether AI can enhance safety protocols by detecting unusual behavior (e.g., intrusion attempts, fainting passengers near the edge) before an accident occurs, thus transforming APGs into smart perimeter defense systems rather than just physical barriers.

The integration of Artificial Intelligence, specifically computer vision and predictive analytics, is rapidly transforming APGs into integral components of smart railway infrastructure. AI algorithms analyze continuous streams of data from integrated sensors, including LiDAR, infrared cameras, and load sensors embedded in the platform structure. This enables systems to learn normal operating patterns and instantaneously flag anomalies, such as door misalignment deviations that predict an imminent mechanical failure, allowing maintenance teams to intervene proactively, substantially reducing Mean Time Between Failures (MTBF) and minimizing service disruptions, which is crucial for high-frequency urban rail systems.

Furthermore, AI significantly enhances passenger safety functions. Vision-based AI systems monitor the gap between the train and the platform edge, detecting objects or persons trapped in closing doors with greater precision than traditional pressure sensors. They also analyze crowding density and dispersion patterns on the platform, providing operators with real-time feedback to manage queues effectively, especially during emergency evacuations or severe delays. This transition from purely hardware-driven safety to data-driven, cognitive safety architectures represents the largest shift catalyzed by AI in the APG market.

The market dynamics of Automatic Platform Gates are fundamentally shaped by a confluence of regulatory demands, technological advancements, and high upfront capital expenditure requirements. The primary driver is the undeniable imperative for enhancing passenger safety in rapidly expanding and increasingly crowded metropolitan transit systems worldwide, which regulatory bodies are rigorously enforcing through modernization mandates. However, this growth is significantly constrained by the substantial financial investment required for initial system installation and the engineering complexities associated with retrofitting APGs into older, irregularly shaped platforms. Opportunities emerge through technological modularity, specifically the development of lighter, standardized systems that can be rapidly deployed in developing economies, thereby overcoming some of the installation cost hurdles and broadening market accessibility.

The key driving forces include global population migration to urban centers, necessitating higher capacity transit infrastructure, and the continuous push towards fully automated, driverless train operations (GoA4). Automated systems inherently require the precise, track-secured environment provided by APGs to operate safely and efficiently. Moreover, the long-term operational cost savings derived from reduced accident liability and minimized service delays often offset the initial investment, making APGs a sound strategic decision for transit authorities aiming for operational excellence and enhanced public trust. These drivers ensure a consistent pipeline of new projects and modernization mandates across all major global regions, underpinning market stability.

Conversely, the market faces significant restraints. Beyond the high capital cost, major implementation challenges include integrating APG signaling systems with diverse, often legacy, train control systems (TCS) used by different transit authorities, leading to prolonged testing and deployment timelines. Public resistance to service disruptions during installation phases also presents a practical barrier. The impact forces driving the market are substantial, defined by regulatory pressure (a consistent, high-impact force), followed closely by technological innovation (medium-to-high impact, influencing cost and reliability), and finally, macroeconomic urban development (a foundational, sustained high-impact force). Restraining forces, primarily high costs and integration complexity, act as frictional forces slowing, but not stopping, the overall trajectory of market growth.

The Automatic Platform Gates market is segmented primarily based on the height of the physical barrier (Type), the mechanical system used for operation (Mechanism), and the specific environment in which they are deployed (Application). The Type segmentation distinguishes between Full-Height Platform Screen Doors (PSDs), which offer maximum safety and climate control, and Half-Height Automatic Platform Gates (APGs), which are primarily focused on fall prevention and are often preferred for their cost-effectiveness and ease of retrofitting. This distinction is critical as it defines the scope of safety and automation level achievable within a transit system, with full-height systems being mandatory for GoA4 operations.

The Mechanism segmentation highlights the technical approach to movement, encompassing Sliding Doors, which are the industry standard for reliability and synchronization; Swing Doors, typically used for emergency exits or specialized access points; and Roping/Telescopic Systems, offering solutions for curved platforms or areas with space limitations. Understanding the operational mechanism is vital for maintenance planning and assessing system longevity. Sliding doors currently hold the largest share due to their widespread acceptance and proven performance over decades of operation in major global cities.

Finally, the Application segment categorizes deployment into Metro/Subway systems, which constitute the core market and demand the highest level of integration and reliability; Mainline and High-Speed Rail Stations, where implementation is more recent and focused on controlled boarding; and Other Transit Systems, including monorails and airport people movers. Market growth is heavily concentrated within new and expanding metro lines across developing nations, demanding scalable and resilient gate solutions. The varying structural and operational demands of these applications necessitate highly customized solutions, driving specialized R&D within vendors.

The value chain for the Automatic Platform Gates market is intricate, starting with highly specialized upstream suppliers and culminating in complex downstream integration and long-term maintenance contracts. Upstream activities involve the procurement of critical components such as high-strength tempered safety glass (often requiring specific lamination or treatment), precision electromechanical components (motors, reduction gears, and sophisticated sensors), and advanced programmable logic controllers (PLCs) that form the core control system. Due to the high safety criticality of APGs, component quality and adherence to strict railway standards (e.g., fire resistance, shock absorption) are non-negotiable, requiring stable, certified supplier relationships.

Midstream activities are dominated by specialized rail system integrators and gate manufacturers. This stage involves system design, bespoke manufacturing based on platform specifications (curvature, length, height), rigorous factory acceptance testing, and pre-assembly. Successful integration requires deep expertise in mechanical, electrical, and signaling engineering. Manufacturers often work directly with the transit authority or the main civil construction contractor. The high customization level inherent in APG projects means that design and manufacturing excellence are key differentiators, focusing on reliability, modularity, and resistance to environmental factors.

Downstream distribution channels are predominantly direct, involving direct negotiation and contracting between the APG manufacturer/system integrator and the Transit Authority or Government Agency responsible for infrastructure development. Indirect channels, such as general construction contractors or major railway rolling stock providers (acting as main system prime contractors), play a secondary role, managing the overall project but subcontracting the specific APG installation. The final, and arguably most profitable, segment of the downstream value chain involves long-term maintenance and service contracts, often spanning 10 to 20 years, focusing on preventive maintenance, immediate fault rectification, and software upgrades, ensuring sustained revenue streams for the original equipment manufacturer (OEM).

The primary end-users and buyers of Automatic Platform Gates are government-owned or privately operated metropolitan transit authorities responsible for managing urban rail networks. These organizations prioritize safety, operational reliability, and compliance with national and international accessibility and safety standards. Their purchasing decisions are heavily influenced by public funding cycles, long-term infrastructure planning, and the specific automation level of their rail lines (e.g., a transit authority planning for Grade of Automation 4 will mandate full-height PSDs). Major customers include entities such as the London Underground, New York MTA, Beijing Subway, and Delhi Metro Rail Corporation, focusing on systems that guarantee minimal failure rates over a service life exceeding 30 years.

A significant secondary customer segment includes large infrastructure construction consortia or system prime contractors (often multinational engineering firms) commissioned by governments to deliver turnkey rail projects. These entities procure APGs as part of the total signaling and station package. While they are the immediate buyers, their technical specifications and procurement budgets are dictated by the end-user transit authority. This group seeks reliable, pre-certified suppliers capable of large-scale production and seamless integration with other trackside equipment.

Furthermore, entities managing high-throughput, closed-loop transit systems, such as major international airports (for automated people movers/shuttles) and private theme park operators (for specialized rail attractions), represent niche but high-value potential customers. Although their volume requirements are lower, they often demand customized, aesthetically pleasing designs and the highest safety redundancy, making system customization a key focus for vendors targeting this segment. The fundamental requirement across all customer types is a certified system that significantly mitigates safety risks associated with platform edges.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.39 Billion |

| Growth Rate | 8.9% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Nabtesco, Faiveley Transport (Wabtec Corporation), Knorr-Bremse, Siemens, Mitsubishi Electric, Horton Automatics, Shanghai Fushun, Tebel Technologies, Gilgen Door Systems, JNA Platform Screen Door, Fangda Industrial, CRRC, Indra Sistemas, Westinghouse Electric, Hyundai Rotem, Schaltbau Holding AG, Toshiba Infrastructure Systems & Solutions, Beijing Platform Screen Door Technology, Huatie Heng'an, and Alstom. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological sophistication of Automatic Platform Gates hinges on three integrated pillars: the mechanical system for reliable movement, the sensing technology for absolute safety, and the control system for seamless synchronization with the train signaling infrastructure. Mechanically, the trend is towards high-efficiency, permanent magnet synchronous motors (PMSMs) coupled with robust, low-maintenance actuators designed to withstand high operational cycles (often over 1 million cycles per year) in harsh environments. Critical technical advancements focus on reducing noise pollution and vibration during operation, often utilizing advanced damping materials and precise motion control algorithms to ensure smooth, synchronized movement across multiple door sets simultaneously.

Sensing technology is undergoing rapid evolution, moving beyond simple photoelectric beams. Modern APGs incorporate sophisticated sensor fusion, combining safety-critical laser scanners (LiDAR), pressure-sensitive mats, and 3D imaging cameras at the door edge and platform gap. These advanced sensors provide comprehensive detection coverage, capable of distinguishing between human limbs, small objects, and unauthorized intrusions onto the track area, significantly increasing the probability of collision avoidance and rapid system response. The data generated by these diverse sensors feeds into the overarching control system for analysis and decision-making, fulfilling the rigorous SIL (Safety Integrity Level) requirements mandated for rail operations.

The control and communication landscape is defined by robust, redundant Programmable Logic Controllers (PLCs) and safety relays that manage the door synchronization sequence and interface directly with the Communication-Based Train Control (CBTC) or traditional interlocking systems. The ability of the APG system to receive precise train stop location data and transmit its operational status (open/closed, fault status) back to the central control room via secure, railway-specific communication protocols (e.g., Ethernet/IP or proprietary fieldbus protocols) is essential. Future technological focus involves leveraging edge computing to process sensor data locally, enabling faster reaction times for safety critical functions and supporting AI-driven predictive maintenance capabilities.

The Asia Pacific (APAC) region stands as the undisputed dominant force in the Automatic Platform Gates market, exhibiting the highest growth rate globally. This dominance is attributed primarily to unprecedented levels of investment in public transport infrastructure, particularly in countries like China, India, South Korea, and Japan. China continues to expand its vast urban metro networks, often adopting full-height PSD systems for all new lines to support GoA4 operations. India's major metropolitan areas, including Delhi, Mumbai, and Bangalore, are rapidly retrofitting existing lines and constructing new corridors, often opting for cost-effective half-height APGs to meet safety requirements quickly. The regional market is highly competitive, driven by both large international suppliers and strong local manufacturers.

Europe represents a mature market characterized by stringent safety regulations and a focus on modernization rather than entirely new construction (outside specific expansions in cities like Paris and London). Growth in Europe is stable, driven by the need to upgrade legacy systems to comply with modern European railway standards (e.g., TSI regulations) and improve accessibility for Persons with Reduced Mobility (PRM). Key markets include the UK, France, Germany, and Spain. European operators often demand highly customized solutions that blend seamlessly into historical station architectures while incorporating advanced reliability features and sophisticated control integration with complex existing signaling systems.

North America's market progression is steady but constrained by slower rates of new construction and the significant cost challenges associated with retrofitting aged subway systems in cities like New York, Chicago, and Boston. The focus here is on robust, durable designs capable of enduring harsh weather and heavy passenger loads, alongside high-reliability maintenance contracts. The Middle East (MEA), particularly the Gulf Cooperation Council (GCC) nations (UAE and Saudi Arabia), presents a high-value, high-growth niche. These nations are developing advanced, state-of-the-art metro systems (like the Riyadh and Doha Metros) from scratch, mandating the latest full-height PSD technology and often incorporating climate control features within the platform areas due to extreme temperatures.

Full-Height Platform Screen Doors (PSDs) offer superior safety, climate control, and are mandatory for fully automated (GoA4) lines, dominating new, high-budget construction. Half-Height Automatic Platform Gates (APGs) are favored for retrofitting existing, older stations due to their significantly lower cost, reduced structural requirements, and easier installation, prioritizing fall prevention over comprehensive track access control.

Installation and integration costs represent a major constraint, often accounting for a significant portion of the total project expenditure. The complexity arises from the necessity to precisely interface the gate control system with diverse legacy train signaling and control systems, requiring extensive custom engineering, prolonged testing phases, and temporary service disruptions which transit authorities seek to minimize.

The Asia Pacific (APAC) region, driven by countries like China and India, is the leading geographical market for APG deployment. Rapid urbanization necessitates vast expansion of metro systems, and large government-backed infrastructure projects ensure continuous, high-volume demand for both new installations and retrofitting to meet increasing safety mandates and operational efficiency targets.

AI significantly enhances APG functionality by enabling predictive maintenance, utilizing machine learning algorithms to forecast component failures before they occur, thus maximizing uptime. Furthermore, computer vision AI systems improve safety by performing real-time crowd analytics and sophisticated intrusion detection at the platform edge, moving beyond traditional sensor capabilities.

Key safety standards include the European CENELEC railway norms (EN 50126, 50128, 50129) which mandate specific Safety Integrity Levels (SIL) for all critical rail equipment. Additionally, local national regulations, such as accessibility standards (e.g., ADA in the US), dictate door opening widths, operational speeds, and emergency protocols to ensure fail-safe operation under all conditions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.