ID : MRU_ 431848 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

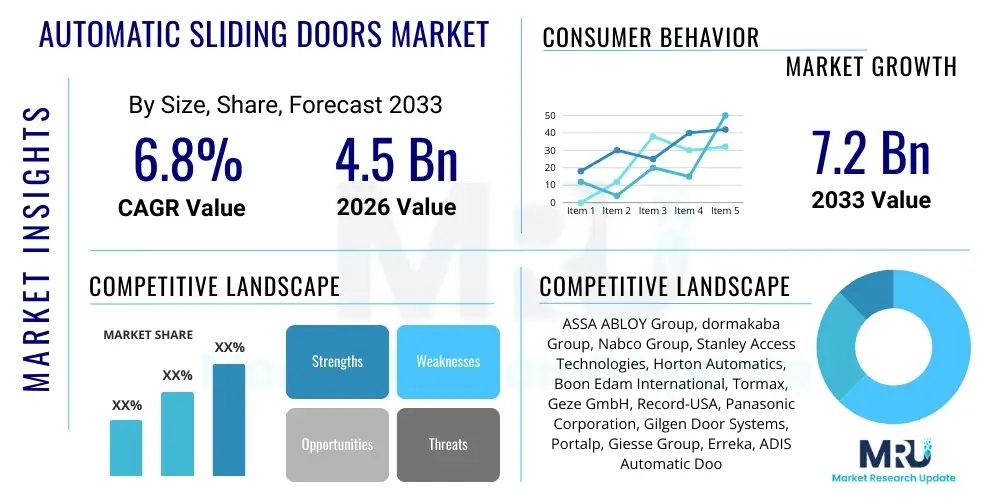

The Automatic Sliding Doors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 4.5 billion in 2026 and is projected to reach USD 7.2 billion by the end of the forecast period in 2033. This substantial growth trajectory is underpinned by increasing urbanization globally, stringent regulatory mandates concerning accessibility (such as the Americans with Disabilities Act in the US and similar standards in Europe), and a rising demand for energy-efficient building solutions in commercial and institutional infrastructure. Furthermore, technological advancements leading to smoother operation, enhanced security features, and integration with smart building management systems are major catalysts contributing to the overall market expansion.

The market valuation reflects strong investment cycles in the construction sector, particularly across Asia Pacific and the Middle East, where large-scale infrastructural projects and the development of modern retail spaces necessitate high-throughput, reliable access systems. While initial investments in automatic sliding door systems can be significant, the long-term operational efficiencies, coupled with reduced maintenance requirements for modern magnetic drive systems, provide compelling return on investment for building owners. The replacement market, driven by the need to upgrade older hydraulic or mechanical systems to energy-saving automatic versions, also plays a crucial role in maintaining consistent market momentum throughout the forecast period.

The Automatic Sliding Doors Market encompasses the manufacturing, distribution, installation, and maintenance of door systems that operate autonomously using sensors, motors, and control units to open horizontally upon detecting approach. These systems are crucial components in modern building designs, enhancing accessibility, managing pedestrian traffic flow efficiently, and contributing to climate control by minimizing the duration a door remains open. Key products include telescopic sliding doors, curved sliding doors, and standard linear sliding doors, catering to diverse architectural and operational requirements across various end-use sectors, including healthcare, retail, transportation hubs, and commercial complexes.

Major applications of automatic sliding doors are concentrated in high-traffic environments where seamless and rapid entry and exit are essential. Retail establishments utilize these doors to improve customer experience and energy conservation, while hospitals and healthcare facilities rely on them for sterile environments and ease of movement for patients and equipment. Transportation sectors, including airports and railway stations, employ heavy-duty automatic sliding doors for robust performance and secure segregation of environments. The primary benefits derived from these installations include improved energy efficiency through minimized air exchange, enhanced safety via anti-entrapment sensors, superior convenience, and compliance with modern building accessibility codes, establishing them as indispensable elements of contemporary infrastructure.

The market is significantly driven by several key factors, notably the rapid expansion of the global construction industry, particularly in emerging economies where modern infrastructure is being prioritized. Further impetus comes from governmental emphasis on public safety and mandatory disability access regulations, which accelerate the adoption of automatic systems in public buildings. The continuous integration of IoT and smart sensors allows for predictive maintenance and enhanced operational control, making these systems more appealing to facility managers. However, the market faces constraints related to high initial installation costs and the technical complexities associated with integrating these systems into legacy building structures, which necessitates specialized installation expertise.

The Automatic Sliding Doors Market is characterized by robust business trends focusing on innovation in drive mechanisms, emphasizing brushless DC motors for improved longevity and reduced noise, and increased penetration of modular systems that simplify installation and maintenance. Key market players are prioritizing expansion into emerging markets, particularly in Southeast Asia and Latin America, through strategic partnerships and localized manufacturing facilities to mitigate supply chain risks and capitalize on accelerating infrastructure spending. A critical trend involves integrating automatic doors with comprehensive building management systems (BMS) for centralized control over security, access authorization, and environmental conditions, transforming doors from simple mechanical devices into intelligent access points.

Regionally, the market exhibits divergent maturity levels. North America and Europe represent mature markets defined by stringent safety standards and high demand for retrofit installations featuring advanced energy-saving technologies. Conversely, the Asia Pacific (APAC) region is poised for the fastest growth, fueled by massive commercial and residential construction booms in China, India, and ASEAN nations. Government initiatives supporting smart city development and the rapid expansion of organized retail sectors in APAC are the primary growth engines. The Middle East and Africa (MEA) region shows strong demand driven by large-scale hospitality projects, airport expansions, and the development of ultra-modern urban centers requiring premium, customized access solutions.

Segment trends highlight a dominant position for the retail and commercial sectors due to the high volume of installations required for shopping malls, office complexes, and hotels. Furthermore, the technology segment is witnessing a significant shift towards microwave and infrared sensor technology, favored over traditional pressure mats for superior reliability and reduced false openings. Within the product type, standard bi-parting sliding doors maintain the largest market share, but telescopic sliding doors are gaining momentum, particularly where maximizing clear opening width in confined spaces is essential. The increasing focus on contactless access, accelerated by recent global health concerns, is driving significant investment in touchless activation technology within all end-use segments.

User queries regarding the intersection of Artificial Intelligence (AI) and the Automatic Sliding Doors Market frequently revolve around predictive maintenance capabilities, enhanced security measures, and personalized user experience. Common concerns include how AI can reduce false triggers, optimize energy consumption based on predicted traffic patterns, and whether AI integration increases the system's susceptibility to cyber threats. Users are keen to understand how machine learning algorithms can analyze real-time video feeds to differentiate between objects, pedestrians, and vehicles, thus improving safety and operational efficiency. The consensus expectation is that AI will move automatic door systems beyond simple sensor-based activation towards intelligent, self-learning, and highly optimized access solutions.

The implementation of sophisticated AI algorithms is poised to revolutionize door control logic. Machine learning models can analyze historical and real-time foot traffic data, weather patterns, and operational schedules to dynamically adjust parameters such as opening speed, hold-open time, and sensitivity thresholds. This capability significantly reduces energy wastage caused by unnecessary openings during low-traffic periods or high wind events. Moreover, AI-powered vision systems enhance security by performing object recognition, allowing the door system to interface seamlessly with existing security infrastructure, identifying authorized personnel, and detecting potential security breaches or tailgating incidents with higher accuracy than conventional sensor arrays.

Integrating AI capabilities fundamentally enhances the value proposition of automatic sliding doors, transforming them into smart components of a building’s IoT ecosystem. The shift towards predictive maintenance, enabled by AI analyzing sensor data anomalies, allows facility managers to preemptively address mechanical failures, minimizing downtime and reducing long-term repair costs. While initial integration costs and the need for robust data processing infrastructure present challenges, the long-term benefits in terms of efficiency, security, and optimized performance solidify AI as a critical transformative force shaping the future development and market adoption of advanced automatic sliding door systems globally.

The market dynamics for automatic sliding doors are currently defined by a powerful convergence of regulatory mandates favoring accessibility and sustainable building design, acting as primary Drivers. However, these positive influences are often moderated by significant Restraints, particularly the capital-intensive nature of high-end installations and the fragmented nature of the maintenance sector, which sometimes leads to inconsistent service quality. The principal Opportunity lies in leveraging smart technology integration, allowing for highly efficient, customized access solutions compatible with IoT standards, expanding the product's utility beyond basic entry control. These factors combine to create a significant impact force characterized by accelerated technological obsolescence of legacy systems and a heightened focus on total cost of ownership (TCO) among commercial developers, demanding systems that balance high upfront cost with exceptional durability and energy performance.

Key drivers underpinning market expansion include mandatory building codes prioritizing universal accessibility, necessitating automatic solutions in public and commercial spaces globally. Furthermore, the rising awareness and emphasis on 'green building' initiatives have significantly increased the demand for highly insulated, air-tight door systems that minimize thermal leakage, which automatic sliding doors, when properly installed, efficiently provide. Urbanization trends leading to the construction of dense commercial centers and transportation hubs also inherently require robust, high-cycle access systems. These drivers collectively push construction stakeholders toward advanced, automated solutions that comply with both safety and sustainability standards, offering long-term economic benefits through optimized energy management.

Conversely, the market faces notable restraints such as the volatility of raw material prices (steel, aluminum, specialized glass), which impacts manufacturing costs and, consequently, final product pricing. Technical complexity, particularly concerning the seamless integration of automatic doors with various building safety systems (e.g., fire alarms, smoke vents), requires highly skilled labor, which is often in short supply, especially in developing regions. Despite these challenges, the overwhelming opportunity provided by the global refurbishment market, upgrading millions of existing manual or semi-automatic door installations to fully automated, smart systems, along with the increasing application of sophisticated sensor technology for improved security and hygiene (touchless operation), ensures that the market trajectory remains robustly positive throughout the forecast period.

The Automatic Sliding Doors Market is rigorously segmented based on product type, drive technology, end-use application, and component structure, allowing manufacturers to tailor offerings precisely to specific architectural and functional requirements. Segmentation provides granular insights into demand patterns, revealing which technologies are gaining traction and which sectors are driving volume growth. The differentiation between standard linear, telescopic, and revolving automatic doors addresses varying space constraints and traffic capacities, while the distinction between electric, pneumatic, and hydraulic drive technologies highlights trade-offs concerning power consumption, speed, and reliability critical for specific operational environments like cleanrooms or heavy industrial settings. Understanding these segments is paramount for strategic market entry and product development focusing on specialized niche requirements.

Analysis by end-use application is arguably the most critical segmentation, dividing the market into high-volume segments such as Retail and Commercial Offices, and high-specification segments like Healthcare and Transportation. The needs of a large retail center prioritizing aesthetics and continuous cycle operation differ vastly from a hospital requiring hermetically sealed doors for infection control, driving differentiated product specifications and pricing structures across the market. Furthermore, the segmentation by component, separating the core operational mechanics (motors, sensors) from structural elements (frames, glass panels), helps track innovation hotspots, such as the increasing demand for high-strength, low-emissivity glass and advanced radar sensors, influencing sourcing and manufacturing strategies across the value chain.

Geographic segmentation is also vital, distinguishing high-growth regions like Asia Pacific, driven by new construction, from mature markets in North America and Europe, dominated by retrofit and replacement demands. The overall segmentation structure confirms that while the core technology remains centered on controlled horizontal movement, the sophistication of sensor arrays, motor control units, and materials used—all categorized under these segments—is continually evolving to meet demanding global standards for safety, energy efficiency, and modern design aesthetics. This granular view ensures that market strategies are aligned with specific regional and sectoral demand drivers.

The value chain for the Automatic Sliding Doors Market begins with upstream activities focused on the procurement and processing of fundamental raw materials, primarily specialized metals like aluminum and steel for frames and tracks, and sophisticated glass materials, including tempered, laminated, and low-emissivity (Low-E) glass, which are crucial for energy performance. Upstream component manufacturing also involves the production of highly engineered electronic components such as brushless DC motors, microprocessors for control units, and specialized sensor technologies (e.g., radar and infrared arrays). The quality and consistency of these inputs directly influence the longevity, reliability, and energy efficiency of the final automatic door system. Strategic partnerships with key component suppliers are vital for manufacturers to maintain control over quality and manage cost fluctuations inherent in the global commodities market.

Midstream activities encompass the core manufacturing, assembly, and testing of the complete door systems. This stage is highly specialized, requiring precision engineering for the alignment of tracks, belts, and carriages to ensure smooth, silent, and reliable operation over millions of cycles. Manufacturers often employ modular design principles to simplify customization and installation across various architectural specifications. The distribution channel then plays a pivotal role. Direct distribution involves sales teams engaging directly with large-scale architectural firms and major construction companies, offering customized solutions and comprehensive service contracts. Indirect distribution relies heavily on a network of authorized dealers, regional distributors, and specialized installers who handle smaller projects, retrofit jobs, and provide localized support and maintenance services.

Downstream activities focus on installation, integration, and post-sales service, which contribute significantly to the total lifetime cost and customer satisfaction. Professional installation is mandatory due to the stringent safety requirements and the need for seamless integration with building safety systems (e.g., emergency exit procedures). Service and maintenance contracts, often recurring revenue streams, involve preventative checks, software updates for control systems, and component replacement. The growing trend towards smart, interconnected doors necessitates skilled technicians capable of servicing complex electromechanical and network integrated systems, highlighting the increasing importance of training and certified expertise in the downstream segment to ensure sustained market performance and brand reputation.

The primary end-users and buyers of automatic sliding door systems span a broad spectrum of commercial, institutional, and high-end residential sectors, all seeking enhanced accessibility, energy efficiency, and sophisticated aesthetics. High-throughput environments, such as major international airports, metro stations, and large shopping centers, constitute major volume buyers due to their continuous need for robust, reliable systems capable of managing thousands of pedestrian cycles daily while ensuring climate control and security. These customers prioritize durability, compliance with international safety standards, and integration capabilities with large-scale surveillance and access control systems, often opting for high-specification telescopic or revolving automatic door models.

The healthcare sector represents a high-value, highly specific segment where door requirements are dictated by strict hygiene standards and operational necessities. Hospitals, specialized clinics, and laboratories require hermetically sealed automatic sliding doors to maintain sterile environments and prevent cross-contamination, especially in operating theaters and isolation wards. Buyers in this segment place paramount importance on materials that are easy to sterilize, touchless activation technologies (such as foot sensors or wave sensors), and silent operation, prioritizing functionality over initial cost, driving demand for specialized product variants that meet stringent medical facility guidelines.

Furthermore, the booming construction of modern commercial office towers and luxury residential complexes globally constitutes a rapidly expanding customer base. Office developers seek aesthetically pleasing, highly efficient systems that contribute to LEED certification goals and offer premium access control for tenants. Residential buyers, particularly those managing large multi-family or condominium complexes, purchase automatic doors for main lobbies to enhance accessibility and provide a secure, upscale entrance experience. This diversity of end-users requires manufacturers to maintain a comprehensive product portfolio covering standard commercial solutions through to highly customized, specialized, and security-focused applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ASSA ABLOY Group, dormakaba Group, Nabco Group, Stanley Access Technologies, Horton Automatics, Boon Edam International, Tormax, Geze GmbH, Record-USA, Panasonic Corporation, Gilgen Door Systems, Portalp, Giesse Group, Erreka, ADIS Automatic Doors, Dierre Group, FAAC Group, CAME Group, Entrematic Group, Auto Door Engineering |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Automatic Sliding Doors Market is rapidly evolving, moving far beyond basic electromechanical actuation. Current innovation is heavily focused on sensor technologies, specifically the transition from traditional pressure mats and simple photoelectric barriers to advanced radar and laser-based sensors. Radar sensors offer superior accuracy in distinguishing between approaching pedestrians and stagnant objects, significantly reducing false openings and improving energy conservation in high-wind or complex environments. Furthermore, the push towards touchless activation, accelerated by public health concerns, has popularized wave-to-open sensors and mobile application integration for secure, hands-free operation, thereby enhancing both hygiene and accessibility compliance across commercial and healthcare settings.

Drive mechanisms are also undergoing transformation, with high-performance, magnetic linear drive technology emerging as a premium alternative to traditional belt or gear-driven systems. Magnetic linear drives offer quieter operation, greater smoothness, enhanced speed control, and reduced mechanical wear and tear, leading to substantially lower long-term maintenance costs and increased reliability, particularly vital in high-traffic applications like airports. Simultaneously, the control systems utilize sophisticated microprocessor technology, enabling real-time diagnostics, performance logging, and seamless integration via communication protocols like Modbus or BACnet into overarching Building Management Systems (BMS), allowing facility managers centralized control and monitoring of door operational status and security parameters.

Connectivity and cybersecurity represent another crucial technological frontier. Modern automatic sliding door controllers are increasingly IoT-enabled, facilitating remote diagnostics, over-the-air software updates, and predictive maintenance alerts. As doors become networked endpoints, robust security protocols are being implemented to prevent unauthorized external access or malicious manipulation of the door’s operating parameters, ensuring safety and system integrity. The development of self-learning algorithms (AI) is the next technological leap, enabling doors to autonomously adjust their operational profile based on learned traffic patterns, environmental conditions, and time-of-day variables, thereby maximizing efficiency and minimizing energy expenditure throughout their operational lifecycle, cementing technology as the primary differentiation factor in a competitive market.

North America represents a technologically mature and highly regulated market, where growth is primarily driven by rigorous enforcement of accessibility laws (ADA) and a strong focus on renovating and upgrading existing commercial infrastructure. The demand here is concentrated on high-quality, durable, and energy-efficient systems, particularly those integrated with sophisticated security features and networked building controls. The US market, being the largest within the region, exhibits high adoption rates for advanced sensor technologies and premium telescopic sliding doors in metropolitan commercial centers. Although the rate of new construction is stable, the consistent need for system replacements and the demand for enhanced safety compliance ensures steady, sustained market valuation throughout the forecast period, with significant emphasis placed on certified installation and maintenance services.

Europe is characterized by a strong emphasis on sustainability, quality craftsmanship, and strict standardization (e.g., European Norms EN 16005). The Western European nations—Germany, France, and the UK—lead in adopting innovative magnetic drive technology and advanced insulation features to meet demanding climate control objectives. The market is highly competitive, driven by local manufacturing giants offering customized architectural solutions that blend aesthetics with high performance. Eastern Europe is experiencing faster growth rates, fueled by ongoing infrastructure modernization and increasing integration with EU safety and accessibility directives, creating strong demand for standardized, reliable automatic door systems in newly developed retail and governmental buildings.

Asia Pacific (APAC) stands out as the highest-growth region globally, propelled by unprecedented levels of urbanization, massive government investment in smart city infrastructure, and rapid expansion of the organized retail and transportation sectors, particularly in China and India. The sheer volume of new construction projects, ranging from mega-malls and large-scale residential complexes to new international airports, necessitates vast quantities of automatic door installations. While price sensitivity is higher in some sub-regions, the overall shift is towards reliable, high-cycle electromechanical systems, often sourced locally or through joint ventures, balancing cost-effectiveness with performance requirements for high-density traffic management. This region will be the primary engine of global market volume expansion.

Latin America is categorized as an emerging market where adoption rates are accelerating, driven by foreign investment in commercial and hospitality infrastructure, particularly in countries like Brazil and Mexico. The market is primarily focused on standard sliding door types, with growing interest in entry-level automation solutions that offer improved security and energy benefits over traditional manual doors. Challenges include economic instability and fragmented distribution channels, requiring market players to utilize flexible pricing strategies and emphasize localized customer support. Growth potential remains substantial as modern building standards gradually permeate regional construction practices.

Middle East and Africa (MEA) exhibits strong, selective growth concentrated in the Gulf Cooperation Council (GCC) states due to massive, high-profile infrastructure development, including specialized projects like the World Expo sites and new mega-cities. Demand is skewed towards premium, architecturally customized systems that can withstand extreme climate conditions (heat and sand ingress), necessitating specialized hermetic sealing and heavy-duty components. The African segment remains nascent, with demand largely concentrated in major urban centers and international entry points, though investment in retail and healthcare infrastructure promises future expansion as regulatory environments mature and construction standards rise.

Market growth is primarily driven by stringent global accessibility regulations (like the ADA and EN standards), increasing commercial and public infrastructure development fueled by urbanization, and the necessity for enhanced building energy efficiency, which modern automatic doors reliably support by minimizing air exchange.

AI integration improves efficiency through predictive maintenance, optimizing motor performance and reducing downtime. It enhances safety by utilizing advanced machine learning algorithms in sensors to reduce false activations and accurately differentiate between pedestrians and stationary objects, leading to more reliable and energy-saving operation.

The Commercial sector, encompassing retail complexes, office buildings, and hospitality venues, currently holds the largest market share due to the high volume requirement for reliable, aesthetic, and high-traffic access solutions that maximize customer flow and contribute positively to energy management strategies.

The most significant emerging trend is the increasing adoption of Magnetic Linear Drive technology. This advanced system replaces traditional belts and gears, offering superior benefits such as extremely quiet operation, reduced mechanical wear, higher speed control precision, and significantly lower long-term maintenance needs, especially in high-cycle environments.

North America is dominated by high-specification replacement and retrofit demand focused on ADA compliance and energy efficiency. Asia Pacific is characterized by high volume new construction, driven by rapid urbanization and infrastructure expansion, prioritizing cost-effective, high-reliability systems for rapidly growing urban centers and retail spaces.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.