ID : MRU_ 440349 | Date : Jan, 2026 | Pages : 246 | Region : Global | Publisher : MRU

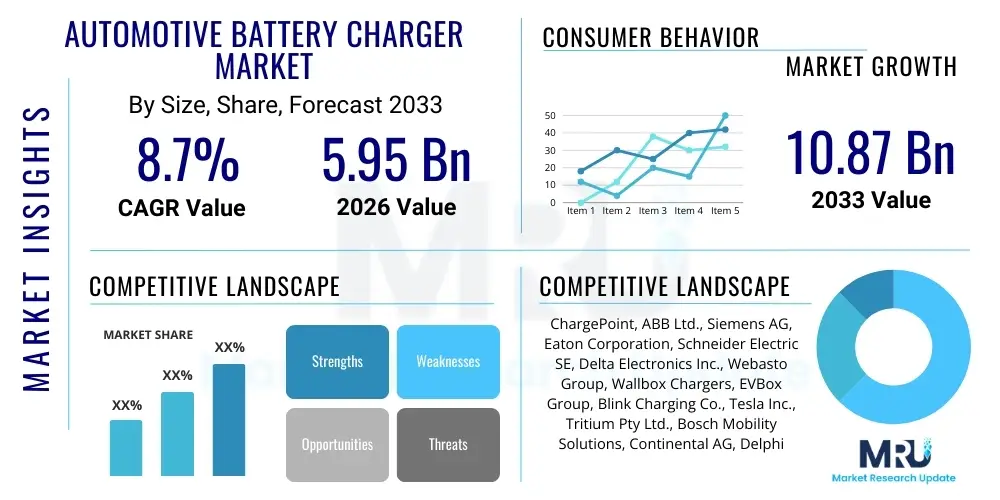

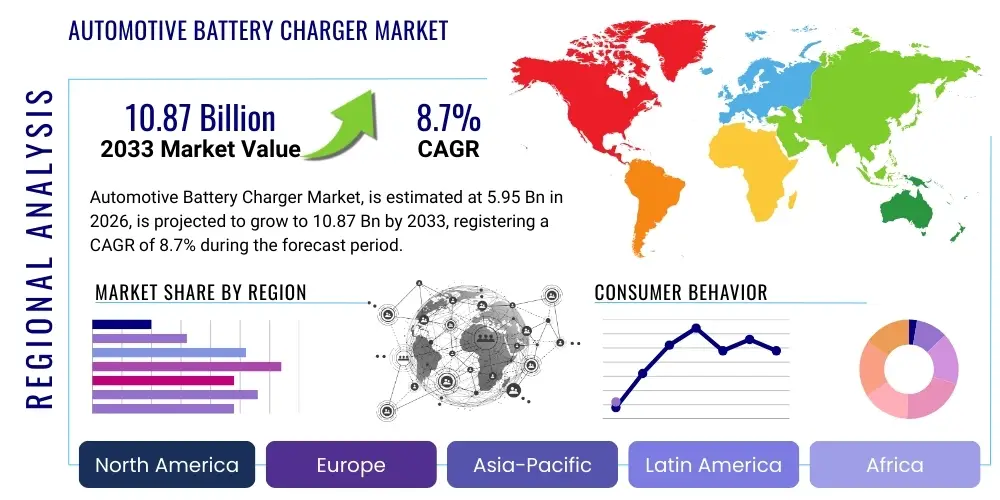

The Automotive Battery Charger Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2026 and 2033. The market is estimated at USD 5.95 billion in 2026 and is projected to reach USD 10.87 billion by the end of the forecast period in 2033. This growth is primarily fueled by the accelerating global adoption of electric vehicles (EVs) across various segments, including passenger cars, commercial vehicles, and electric two-wheelers. The increasing need for reliable, efficient, and faster charging solutions to support the expanding EV fleet is a significant market driver. Additionally, advancements in charging technology, such as smart charging, bidirectional capabilities, and wireless charging, are contributing substantially to market expansion.

The market's upward trajectory is also supported by supportive government policies, incentives for EV purchases, and robust investments in charging infrastructure development worldwide. Urbanization trends, coupled with rising environmental consciousness, are pushing consumers towards sustainable transportation options, thereby boosting the demand for automotive battery chargers. Furthermore, the integration of renewable energy sources with charging stations and the development of vehicle-to-grid (V2G) technology are opening new avenues for market growth. The continuous innovation in battery technology, leading to higher capacity and faster charging capabilities, also necessitates compatible and advanced charging solutions, further propelling the market forward.

The Automotive Battery Charger Market encompasses a wide range of devices designed to replenish the electrical energy in a vehicle's battery, essential for its operation. These products vary significantly in their power output, charging speed, and technological sophistication, catering to diverse vehicle types from conventional internal combustion engine (ICE) vehicles to a rapidly expanding fleet of electric vehicles (EVs), including Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Hybrid Electric Vehicles (HEVs). The primary function of these chargers is to convert alternating current (AC) from the grid into direct current (DC) that can be stored in the vehicle's battery, ensuring optimal performance and extending battery life. With the global pivot towards sustainable mobility and the significant investments in electric vehicle infrastructure, automotive battery chargers have become an indispensable component in the automotive ecosystem, supporting both daily vehicle usage and long-term battery health management.

Major applications of automotive battery chargers span across residential, commercial, and public sectors. In residential settings, consumers utilize chargers for overnight charging of their EVs, offering convenience and cost-effectiveness. Commercial applications include fleet charging for delivery services, taxis, and ride-sharing vehicles, where efficient and rapid charging is crucial for operational continuity. Public charging stations, ranging from Level 2 AC chargers to high-power DC fast chargers, are strategically located in urban centers, highways, and parking facilities to support long-distance travel and opportunistic charging. The benefits derived from these chargers are manifold, including enhanced vehicle reliability, improved battery longevity, convenience, and reduced carbon emissions by facilitating EV adoption. Key driving factors for this market include the global surge in electric vehicle sales, stringent emission regulations, government incentives for EV purchases and charging infrastructure, technological advancements in smart charging and bidirectional capabilities, and the increasing consumer awareness regarding environmental sustainability.

The Automotive Battery Charger Market is experiencing robust expansion, primarily propelled by the exponential growth in electric vehicle (EV) adoption and the escalating demand for advanced charging infrastructure. Business trends indicate a strong focus on innovation, with manufacturers heavily investing in research and development to introduce smarter, faster, and more efficient charging solutions, including those with bidirectional capabilities and integration with renewable energy sources. Partnerships between automotive OEMs, charging infrastructure providers, and utility companies are becoming increasingly common, aiming to create a seamless charging ecosystem and accelerate market penetration. There is a discernible shift towards subscription-based charging services and smart grid integration, optimizing energy management and user convenience. The aftermarket segment is also thriving, catering to the diverse needs of vehicle owners seeking upgraded or specialized charging solutions.

Regional trends highlight distinct growth patterns and market maturity levels. North America and Europe are leading the market in terms of infrastructure development and EV sales, driven by favorable government policies, high consumer awareness, and significant investments from both public and private sectors. The Asia Pacific region, particularly China, is demonstrating unparalleled growth, becoming a global powerhouse for EV manufacturing and adoption, consequently creating immense demand for charging solutions. Emerging economies in Latin America, the Middle East, and Africa are gradually catching up, with nascent EV markets showing promising potential as governmental support and infrastructure development begin to take root. Segment trends reveal a growing preference for DC fast chargers and smart chargers due to their ability to provide quicker charging times and offer enhanced features such as remote monitoring, scheduled charging, and energy management capabilities. The market is also witnessing diversification in terms of vehicle types, with a rising demand for charging solutions tailored for electric buses, trucks, and two-wheelers, alongside traditional passenger EVs.

User inquiries regarding AI's impact on the Automotive Battery Charger Market frequently revolve around how artificial intelligence can enhance charging efficiency, optimize energy usage, and improve the overall user experience. Users are keen to understand if AI can lead to faster charging times without compromising battery health, how it might integrate with smart home systems and renewable energy sources, and what implications it has for grid stability and vehicle-to-grid (V2G) capabilities. There's also significant interest in predictive maintenance for charging stations, personalized charging recommendations, and the potential for AI to manage complex charging networks in commercial and public settings, addressing concerns about cost, convenience, and the longevity of EV batteries. Essentially, the overarching theme is the transformation of basic charging into an intelligent, adaptive, and highly optimized energy management system driven by AI.

The Automotive Battery Charger Market is shaped by a complex interplay of drivers, restraints, opportunities, and various impact forces. Key drivers propelling the market forward include the unprecedented global surge in electric vehicle (EV) sales across all segments, from passenger cars to commercial fleets, necessitating robust and widespread charging infrastructure. Government incentives, subsidies, and stringent emission regulations globally are strongly encouraging EV adoption and, consequently, the demand for charging solutions. Rapid technological advancements in battery chemistry and charging technologies, such as increasing power density, faster charging speeds, and the emergence of smart charging capabilities, further fuel market expansion. Furthermore, growing consumer awareness regarding environmental sustainability and the benefits of electric mobility acts as a significant catalyst.

However, the market also faces notable restraints. The high initial cost associated with advanced charging infrastructure, particularly DC fast chargers, can be a barrier to widespread adoption in certain regions. Challenges related to grid infrastructure limitations and the slow rollout of charging networks in developing countries hinder market growth. Standardization issues across different charging protocols and connector types create fragmentation and inconvenience for users. Moreover, concerns regarding battery degradation from frequent fast charging and the perceived limited range of EVs (range anxiety) can dampen consumer enthusiasm. These restraints require strategic interventions, including policy support and technological harmonization, to mitigate their impact on market development.

Opportunities within the automotive battery charger market are abundant and transformative. The burgeoning demand for Vehicle-to-Grid (V2G) and Vehicle-to-Home (V2H) technologies presents a significant opportunity, allowing EVs to become active participants in energy management. The integration of renewable energy sources, such as solar and wind power, with charging stations offers a sustainable and decentralized charging ecosystem. The development of wireless charging technologies and ultra-fast charging solutions promises enhanced convenience and efficiency. Furthermore, the expansion into emerging economies with nascent EV markets, coupled with the increasing focus on smart cities and sustainable urban mobility, offers vast untapped potential. The continuous innovation in software platforms for charger management, payment solutions, and data analytics also creates new business models and revenue streams.

Impact forces influencing the market are multifaceted. Technological advancements, particularly in power electronics (e.g., GaN and SiC), IoT integration, and AI-driven energy management, significantly influence product development and market dynamics. The regulatory landscape, including safety standards, environmental policies, and infrastructure mandates, profoundly shapes market growth and investment decisions. Economic conditions, such as raw material costs, manufacturing expenses, and consumer purchasing power, directly affect pricing strategies and market accessibility. Societal shifts towards environmental consciousness and smart living drive consumer preferences and demand for eco-friendly and technologically advanced charging solutions. Geopolitical factors, trade policies, and supply chain disruptions can also impact the availability and cost of components, thereby affecting market stability and growth trajectory. These forces collectively dictate the pace and direction of innovation and expansion in the automotive battery charger sector.

The Automotive Battery Charger Market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation helps in identifying specific growth drivers, market challenges, and lucrative opportunities across various product types, charging levels, vehicle compatibility, application areas, and sales channels. By analyzing these distinct segments, stakeholders can tailor their strategies to address specific market needs, optimize product development, and enhance market penetration. The complexity of modern vehicle batteries and the evolving charging ecosystem necessitate a detailed breakdown, allowing for a clearer picture of market evolution.

The value chain for the Automotive Battery Charger Market encompasses a series of interconnected activities, beginning from raw material sourcing and extending to the end-users, involving multiple stakeholders. The upstream analysis focuses on the procurement of essential components such as semiconductors, power electronics (e.g., IGBTs, MOSFETs, GaN, SiC), microcontrollers, transformers, rectifiers, and wiring. Key raw materials like copper, aluminum, and various plastics are sourced from global suppliers. The efficiency and cost-effectiveness at this stage are crucial for the overall profitability and competitiveness of the final product. Strategic partnerships with component manufacturers and robust supply chain management are vital to ensure quality, availability, and cost control, especially given the global nature of electronic component supply.

Midstream activities involve the design, manufacturing, and assembly of the battery chargers. This stage includes sophisticated R&D for developing advanced charging technologies, power management systems, and safety features. Manufacturers invest heavily in automated production lines, quality control, and testing to ensure compliance with international standards and safety regulations. Customization for specific vehicle types and market requirements also takes place here. The downstream analysis primarily focuses on the distribution channels and sales mechanisms. These include direct sales to automotive OEMs for integration into new vehicles, sales to charging infrastructure developers, and sales to the aftermarket through retail stores, e-commerce platforms, automotive repair shops, and specialized EV accessory providers. The effectiveness of these channels is critical for market reach and customer accessibility.

Distribution channels can be broadly categorized into direct and indirect methods. Direct channels involve manufacturers selling directly to large fleet operators, public utility companies, or automotive OEMs, often through long-term contracts and direct sales teams. This approach allows for greater control over pricing, branding, and customer relationships. Indirect channels, on the other hand, leverage a network of distributors, wholesalers, retailers, and online platforms to reach a broader customer base, including individual EV owners and smaller businesses. These channels rely on established logistics networks and marketing efforts to efficiently deliver products to various end-users. After-sales support, including installation services, maintenance, and warranty provisions, forms an integral part of the value chain, enhancing customer satisfaction and loyalty. The interplay between these stages and channels determines market efficiency and consumer adoption rates.

The potential customers for the Automotive Battery Charger Market are diverse and span across various segments, driven by the expanding ecosystem of electric vehicles and traditional automotive needs. Individual electric vehicle owners constitute a significant segment, purchasing chargers for home use, ranging from basic Level 1 trickle chargers to faster Level 2 smart chargers, for daily charging convenience and energy cost management. These customers prioritize ease of use, safety features, and smart functionalities such as remote monitoring and scheduled charging. The increasing adoption of EVs as primary vehicles ensures a continuous demand from this demographic, as part of their initial vehicle purchase or as an aftermarket upgrade to enhance their charging experience.

Another critical customer segment includes commercial fleet operators, such as logistics companies, public transport agencies, ride-sharing services, and taxi operators. These entities require robust, reliable, and often high-speed charging solutions to ensure minimal downtime and maximum operational efficiency for their electric vehicle fleets. For them, factors like scalability, energy management systems, interoperability, and cost-effectiveness of bulk charging infrastructure are paramount. The shift towards electric buses and trucks for urban and regional transportation is particularly driving demand from this segment, necessitating specialized heavy-duty charging solutions.

Furthermore, businesses and public entities establishing public and workplace charging infrastructure represent a substantial customer base. This includes municipalities, property developers, retail establishments, hospitality venues, and workplaces looking to offer charging amenities to their employees and visitors. These customers typically invest in Level 2 and DC fast chargers, with an emphasis on network management, payment systems, and integration with smart city initiatives. Automotive Original Equipment Manufacturers (OEMs) also serve as significant customers, integrating charging solutions as part of their EV product offerings, either bundled with the vehicle or as recommended accessories, ensuring compatibility and optimal performance. Lastly, automotive service centers and dealerships also purchase chargers for maintenance, diagnostic, and vehicle preparation purposes for both ICE and EV batteries, albeit in smaller volumes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.95 Billion |

| Market Forecast in 2033 | USD 10.87 Billion |

| Growth Rate | 8.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ChargePoint, ABB Ltd., Siemens AG, Eaton Corporation, Schneider Electric SE, Delta Electronics Inc., Webasto Group, Wallbox Chargers, EVBox Group, Blink Charging Co., Tesla Inc., Tritium Pty Ltd., Bosch Mobility Solutions, Continental AG, Delphi Technologies, Ingeteam S.A., Enel X, Star Charge, Nio Power, Xpeng Motors |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Battery Charger Market is undergoing a rapid technological evolution, driven by the increasing demands of electric vehicles and the broader smart energy ecosystem. A pivotal technological shift involves the widespread adoption of advanced power electronics, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN) components. These materials enable higher switching frequencies, smaller form factors, greater power density, and significantly improved energy efficiency compared to traditional silicon-based components, leading to faster and more compact chargers with reduced heat dissipation. This allows for the development of ultra-fast DC chargers that can deliver substantial range in a short charging period, addressing a major concern for EV users.

Another significant technological advancement is the integration of smart charging capabilities, leveraging Internet of Things (IoT) connectivity and cloud-based platforms. These technologies enable real-time monitoring, remote control, diagnostic capabilities, and predictive maintenance for charging stations. Smart chargers can communicate with the electric grid to optimize charging times, take advantage of off-peak electricity rates, and integrate with renewable energy sources. This intelligence supports grid stability, reduces energy costs for users, and contributes to a more sustainable energy ecosystem. The development of sophisticated energy management systems (EMS) at both the individual charger and network level is critical for efficient operation.

Furthermore, the landscape is witnessing the emergence and refinement of bidirectional charging technology (Vehicle-to-Grid, V2G; Vehicle-to-Home, V2H). This technology allows EVs not only to draw power from the grid but also to feed surplus energy back into the grid or power a home, transforming EVs into mobile energy storage units. This capability has profound implications for grid resilience, renewable energy integration, and revenue generation for EV owners. Wireless charging technology, though still in its nascent stages for automotive applications, represents another frontier. Utilizing inductive power transfer, wireless chargers offer enhanced convenience by eliminating cables, potentially facilitating automated charging for autonomous vehicles and public transport systems. These innovations collectively define the cutting-edge of the automotive battery charger market, pushing the boundaries of efficiency, convenience, and integration with future energy infrastructures.

The Automotive Battery Charger Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2026 and 2033, driven primarily by increasing electric vehicle adoption and technological advancements in charging solutions.

Key drivers include the global surge in electric vehicle (EV) sales, supportive government incentives and regulations, continuous technological advancements in charging speed and intelligence, and increasing consumer awareness regarding environmental sustainability.

AI significantly impacts the market by enabling smart charging, optimizing energy usage through predictive analytics, enhancing grid stability, facilitating Vehicle-to-Grid (V2G) functionality, and providing personalized charging experiences, ultimately improving efficiency and convenience.

North America and Europe are leading in infrastructure development and EV sales, while the Asia Pacific region, especially China, is experiencing the fastest growth in both EV manufacturing and charging solution adoption.

The market primarily offers Smart Chargers, Basic Chargers, and Inductive/Wireless Chargers, categorized by product type. By charging level, they include Level 1 (AC), Level 2 (AC), and DC Fast Chargers (Level 3), each offering different charging speeds and power outputs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.