ID : MRU_ 431899 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

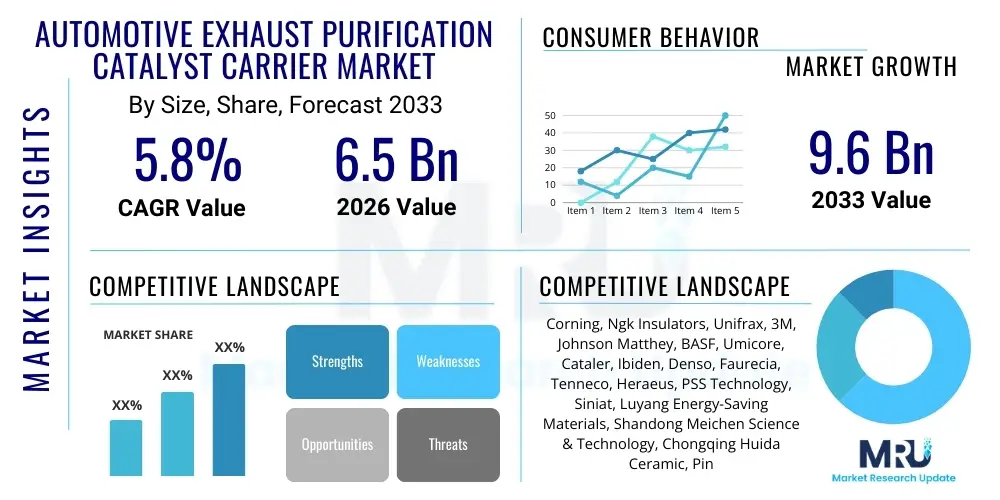

The Automotive Exhaust Purification Catalyst Carrier Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 6.5 billion in 2026 and is projected to reach USD 9.6 billion by the end of the forecast period in 2033.

The Automotive Exhaust Purification Catalyst Carrier Market encompasses the specialized ceramic or metallic substrates utilized within catalytic converters to support and maximize the surface area of precious metal catalysts (such as platinum, palladium, and rhodium). These carriers are engineered primarily to facilitate the conversion of harmful exhaust gases—including carbon monoxide (CO), unburned hydrocarbons (HC), and nitrogen oxides (NOx)—into less harmful substances like carbon dioxide, water vapor, and nitrogen. The design and material selection of the catalyst carrier, particularly its geometric structure (monoliths, foams, or beads) and thermal resistance, are critical determinants of the catalytic converter’s efficiency and durability under extreme operating conditions.

Major applications for these carriers span the entire automotive sector, specifically within passenger vehicles, light commercial vehicles (LCVs), and heavy-duty vehicles (HDVs) that rely on internal combustion engines (ICE) or hybrid powertrains. The growing stringency of global emission standards, notably Euro 6/7 in Europe, LEV III in the US, and China VI, directly mandates the deployment of highly efficient catalytic converters, thereby driving demand for advanced carrier materials like high-cell-density cordierite and silicon carbide (SiC) substrates. Benefits derived from optimized catalyst carriers include superior thermal stability, reduced back pressure on the engine, improved light-off temperature performance, and enhanced mechanical strength necessary for vibration resistance.

The market is predominantly driven by legislative pressure from environmental agencies worldwide seeking to curb urban air pollution. Furthermore, the persistent demand for higher performance and fuel efficiency in modern vehicles necessitates innovation in carrier geometry and material composition to reduce weight while maintaining high catalytic activity. While the long-term shift toward electric vehicles poses a potential restraint, the interim necessity for highly efficient hybrid powertrains and stringent regulations governing existing ICE vehicles ensure robust near-term market momentum for advanced catalyst carrier technology.

The Automotive Exhaust Purification Catalyst Carrier Market is poised for consistent growth, fundamentally propelled by aggressive global regulatory frameworks focused on reducing vehicular tailpipe emissions. Business trends indicate a strong industry focus on optimizing substrate materials, shifting from standard cordierite to advanced materials like silicon carbide (SiC) for diesel particulate filters (DPFs) and gasoline particulate filters (GPFs), particularly in markets adopting Euro 6d and Euro 7 standards. Key manufacturers are engaging in strategic partnerships with OEMs and leveraging advanced manufacturing techniques, such as additive manufacturing, to create complex, customized carrier geometries that improve mass transfer and thermal shock resistance. This innovation cycle is essential for meeting the demands of high-performance engines and complex exhaust aftertreatment systems, including Selective Catalytic Reduction (SCR) and Lean NOx Traps (LNT).

Regionally, the Asia Pacific (APAC) market, spearheaded by China and India, is expected to exhibit the highest growth rate due to rapidly implementing stringent emission norms (e.g., China VI and Bharat Stage VI). These developing economies represent massive volumes in vehicle production, creating unparalleled demand for catalyst carriers. Europe remains a critical innovation hub, driving demand for GPFs due to the increasing penetration of gasoline direct injection (GDI) engines. North America also maintains stable growth, primarily driven by the replacement market and the stringent requirements for heavy-duty commercial vehicles, which utilize larger and more durable ceramic carriers.

Segment trends highlight the dominance of ceramic carriers, specifically cordierite monoliths, owing to their cost-effectiveness and proven performance in gasoline engines. However, the Silicon Carbide (SiC) segment is forecast to be the fastest-growing material segment, attributed to its superior thermal stability and higher filtration efficiency required for particulate matter reduction in both diesel and gasoline applications. Passenger vehicles constitute the largest application segment, but the commercial vehicle segment is displaying accelerated growth due to the high capital investment required for efficient aftertreatment systems in trucks and buses, which require robust and high-capacity carriers to handle greater exhaust volumes and severe operating cycles.

Common user questions regarding AI's impact on the catalyst carrier market primarily revolve around predictive maintenance, optimized material composition, and enhancing manufacturing efficiency. Users are keenly interested in how Artificial Intelligence can model complex fluid dynamics and heat distribution within catalytic converters to design carrier structures that maximize catalytic efficiency and longevity. Key themes emerging include the potential for AI-driven simulation platforms to drastically reduce R&D cycles for new carrier geometries, concerns about the required data infrastructure for real-time exhaust system monitoring, and expectations regarding the role of machine learning in optimizing the washcoat application process and predicting carrier degradation under specific operational profiles. This collective user interest suggests a demand for AI not just as a tool for automation, but as a core component for performance optimization and predictive quality control, ensuring compliance with future hyper-stringent emission standards.

AI algorithms are increasingly integrated into the material science and engineering phases of catalyst carrier development. Specifically, machine learning models can analyze vast datasets concerning temperature variations, gas flow rates, and catalytic activity across various carrier geometries and porosities. This capability allows manufacturers to simulate millions of design permutations in silico, identifying optimal structures that minimize back pressure while maximizing surface area for catalyst deposition. This drastically accelerates the time-to-market for carriers compliant with next-generation regulations (such as Euro 7, which demands enhanced performance across a wider range of operating conditions).

Furthermore, AI-driven process control systems are revolutionizing the manufacturing floor. In the highly complex process of carrier extrusion and firing, machine vision and deep learning models monitor parameters such as slurry viscosity, drying consistency, and firing temperature in real time. This proactive quality control minimizes material waste, ensures the structural integrity of the resulting monolith, and achieves highly consistent cell densities and wall thicknesses, which are paramount for performance reliability. The application of AI also extends to supply chain management, optimizing the procurement and inventory of critical raw materials like cordierite powder and silicon carbide, thereby improving operational resilience and cost management for carrier producers.

The dynamics of the Automotive Exhaust Purification Catalyst Carrier market are shaped by a powerful interplay between stringent legislative mandates, technological advancements, and the underlying transition of the global automotive fleet. The primary drivers revolve around the continuous tightening of emission regulations globally, such as the implementation of Euro 6d and forthcoming Euro 7 standards, which necessitate carriers with higher thermal shock resistance and increased cell density for improved efficiency. Restraints primarily include the high capital investment required for SiC carrier manufacturing, the inherent complexity and cost associated with PGMs that rely on these carriers, and, crucially, the long-term structural threat posed by the accelerating global shift toward Battery Electric Vehicles (BEVs), which bypass the need for exhaust purification systems entirely.

Opportunities for growth lie significantly in the burgeoning demand for specialized filters, such as Gasoline Particulate Filters (GPFs), driven by the widespread adoption of Gasoline Direct Injection (GDI) engines, which produce particulate matter comparable to diesel engines. Furthermore, the commercial vehicle sector, particularly heavy-duty trucks and buses, presents a lucrative niche requiring large-volume, highly durable carriers for SCR and DPF systems. Innovation in thin-wall technology for cordierite monoliths and the development of alternative, lower-cost washcoat formulations also present critical avenues for market expansion, allowing manufacturers to balance performance requirements with cost pressures imposed by OEMs.

Impact forces analysis reveals that environmental and technological factors are the most potent influences. The regulatory pressure (Driver) consistently impacts technology adoption, compelling manufacturers to invest heavily in advanced materials (like SiC and metallic substrates) to meet compliance benchmarks, thereby increasing market costs (Restraint). The high entry barrier established by requiring deep technical expertise in ceramics and metallurgy acts as a protective force for incumbent players. The shift towards hybridization in vehicles, rather than pure electrification, offers a transitional opportunity, as hybrid vehicles still require sophisticated exhaust aftertreatment to qualify for regulatory incentives, sustaining demand for high-efficiency catalyst carriers for the medium term (up to 2035).

The Automotive Exhaust Purification Catalyst Carrier Market is segmented based on critical technical characteristics, including the material used for the substrate, the specific application in vehicle type, and the coating technology employed. The primary differentiation lies in Material Type, where manufacturers choose between ceramics (Cordierite, SiC) and metallic foils based on the required thermal performance and mechanical strength for the target engine type. Cordierite remains the volume leader due to its cost advantage and low thermal expansion, while SiC is gaining traction in regulated particulate filter markets.

Segmentation by Application is crucial, distinguishing between the high-volume Passenger Vehicle market and the more technically demanding Commercial Vehicle segment. Commercial vehicles (trucks, buses) often utilize larger, heavier-duty carriers designed to withstand long operating hours and extreme exhaust temperatures associated with diesel engines, frequently incorporating advanced DPF and SCR systems. Passenger vehicles, especially GDI models, are driving the adoption of smaller, highly efficient GPFs and three-way catalysts (TWC) utilizing thin-wall technology.

The market also segments implicitly by Coating Technology, primarily focusing on the washcoat formulation and the deposition of Precious Group Metals (PGMs). Advanced catalyst carriers require sophisticated washcoats that adhere effectively to the substrate while providing maximal surface area and thermal stability for the PGM catalysts, ensuring the entire exhaust system meets the increasingly strict regulatory thresholds for NOx and particulate matter conversion efficiency under diverse driving conditions, including critical cold-start performance.

The value chain for the Automotive Exhaust Purification Catalyst Carrier market begins with the extraction and processing of fundamental raw materials, primarily high-purity minerals such as kaolin, talc, and alumina for cordierite, and silica sand and carbon for silicon carbide (SiC). The upstream segment is characterized by specialized chemical and material processing companies that produce highly consistent ceramic powders or metallic foils. Quality control at this stage is paramount, as the purity and particle size distribution of the precursors directly determine the final thermal and mechanical properties of the carrier substrate, necessitating strong long-term relationships between raw material suppliers and catalyst carrier manufacturers.

The intermediate stage involves highly technical carrier manufacturing (extrusion, firing/sintering, canning) carried out by core players like Corning and NGK Insulators. These companies transform raw materials into complex monolithic structures. Following carrier production, the component moves to the catalyst coating firms, often the same entity or specialized chemical companies (like BASF or Umicore), which apply the washcoat and impregnate the substrate with expensive Precious Group Metals (PGMs). This step adds immense value, transforming the inert carrier into a functional catalytic converter component.

The downstream segment involves integration and distribution. The finished catalytic converter assembly (carrier + washcoat + canning) is either supplied directly to Original Equipment Manufacturers (OEMs) for integration into new vehicle exhaust systems (Direct Channel) or distributed through an aftermarket network consisting of wholesalers, specialized exhaust system distributors, and repair shops (Indirect Channel). The OEM channel dominates the volume market, driven by long-term procurement contracts and stringent quality checks, whereas the aftermarket channel provides necessary replacement components, influenced heavily by vehicle age, driving cycles, and regional inspection standards.

Potential customers for Automotive Exhaust Purification Catalyst Carriers are highly concentrated within the global automotive supply chain, primarily comprising the manufacturers responsible for integrating complete exhaust aftertreatment systems. The primary buyers are Tier 1 automotive suppliers who specialize in designing and assembling catalytic converters, such as Faurecia, Tenneco (now part of Aptiv), and others. These entities procure the bare carriers and then perform the highly critical and specialized washcoating and PGM loading processes before delivering the finalized system to the vehicle manufacturer.

Secondly, the vehicle Original Equipment Manufacturers (OEMs) themselves represent a major customer group, especially large, vertically integrated automotive conglomerates that may choose to purchase carriers directly and manage certain parts of the aftertreatment assembly in-house to maintain control over proprietary designs and cost structures. Key OEMs across various regions, including Volkswagen Group, General Motors, Toyota, and Tata Motors, significantly influence the market specifications, demanding customization in size, cell density, and material based on their engine architecture and compliance requirements for specific geographic markets. The aftermarket segment, though smaller in volume, includes wholesalers and distributors serving independent garages and specialized repair networks that require replacement carriers for vehicles no longer under warranty.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | CAGR 5.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Corning, Ngk Insulators, Unifrax, 3M, Johnson Matthey, BASF, Umicore, Cataler, Ibiden, Denso, Faurecia, Tenneco, Heraeus, PSS Technology, Siniat, Luyang Energy-Saving Materials, Shandong Meichen Science & Technology, Chongqing Huida Ceramic, Pingxiang Plansee, DCL International |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the automotive exhaust purification catalyst carrier market is dominated by advancements aimed at reducing thermal mass and increasing geometric surface area while enhancing thermal stability. The central technological challenge is achieving faster 'light-off'—the point at which the catalyst reaches the required operating temperature—to ensure pollutants are efficiently converted immediately after engine startup, a primary focus of upcoming Euro 7 regulations. Thin-wall technology is crucial here, involving the extrusion of ceramic monoliths with wall thicknesses significantly below 4 mils (0.1 mm), which drastically reduces the amount of material needing to be heated, leading to quicker light-off times without compromising mechanical integrity. Innovations in cordierite manufacturing processes focus heavily on achieving these ultra-thin walls while maintaining the structural soundness required for high-speed automated canning processes.

A second major technological development is the widespread adoption of Silicon Carbide (SiC) as the carrier material for Particulate Filters (DPFs and GPFs). SiC technology offers superior filtration efficiency and, crucially, much higher melting points and thermal conductivity compared to traditional cordierite, making it ideal for the highly exothermic regeneration processes required to burn off trapped soot, particularly in diesel applications. The technology involves intricate pore design and optimized wall-flow geometries to balance filtration efficiency (trapping particulate matter) and minimal pressure drop (maintaining engine performance). Continuous research focuses on reducing the cost of SiC production, which currently acts as a limiting factor, through more energy-efficient sintering techniques.

Furthermore, the integration of advanced coating methodologies, specifically related to the washcoat, represents a key technological frontier. Modern catalyst carriers require washcoats that utilize nano-structured materials to improve adherence, porosity, and thermal aging resistance. Technology development includes optimizing the rheology of the washcoat slurry and using precision application techniques (like spray coating or vacuum impregnation) to ensure a uniform layer thickness and distribution of stabilizers and oxygen storage components (OSCs). The goal is to maximize the utilization of expensive PGMs loaded onto the carrier surface, effectively minimizing the PGM content required per vehicle while meeting ever stricter emission targets.

The primary materials are Cordierite and Silicon Carbide (SiC). Cordierite is favored for its low thermal expansion and cost-effectiveness, ideal for conventional gasoline engines. SiC is chosen for its superior thermal stability and melting point, making it necessary for high-temperature diesel and gasoline particulate filters (DPFs/GPFs).

Stringent regulations (like Euro 7 and China VI) mandate higher pollutant conversion rates and faster catalyst activation ('light-off'). This drives demand for technologically advanced carriers featuring ultra-thin walls and high cell densities to maximize catalytic surface area and reduce thermal inertia.

In particulate filters, the carrier substrate is typically a wall-flow monolith (often SiC) designed to force exhaust gases through porous channel walls. The carrier acts as a physical filter to trap soot and particulate matter, which are later burned off during a high-temperature regeneration cycle, ensuring continued emission compliance.

Electric vehicles, being zero-emission at the tailpipe, eliminate the need for catalytic converters and thus catalyst carriers. While hybrid vehicles still require carriers, the long-term, global shift toward battery electric mobility poses a fundamental structural restraint on market expansion beyond the 2035 horizon.

The Asia Pacific (APAC) region, led by China and India, is experiencing the fastest market growth. This rapid expansion is due to high-volume vehicle manufacturing combined with the recent, aggressive adoption of Euro 6/BS VI equivalent emission standards, necessitating widespread deployment of advanced aftertreatment systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.