ID : MRU_ 433340 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

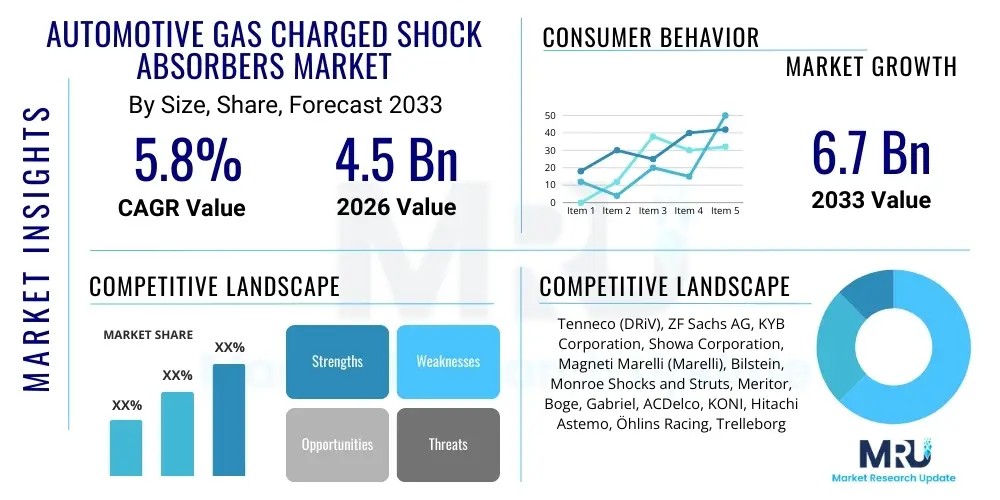

The Automotive Gas Charged Shock Absorbers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 4.5 billion in 2026 and is projected to reach USD 6.7 billion by the end of the forecast period in 2033.

The Automotive Gas Charged Shock Absorbers Market encompasses the global manufacturing and distribution of specialized suspension components that utilize pressurized inert gas, typically nitrogen, combined with hydraulic fluid to enhance vehicle ride quality, stability, and handling performance. Unlike traditional hydraulic-only shock absorbers, the addition of pressurized gas prevents fluid aeration (foaming or cavitation) during rapid operation, especially under strenuous driving conditions or high ambient temperatures. This resistance to aeration ensures consistent damping force and prevents "shock fade," a critical performance characteristic valued in modern automotive applications, ranging from high-performance sports cars to heavy-duty commercial vehicles requiring stable load management.

The fundamental role of these components is to dampen the oscillations of the vehicle’s suspension system, converting kinetic energy generated by road irregularities into thermal energy that is then dissipated. Gas charged absorbers achieve superior performance by maintaining constant pressure on the hydraulic fluid reservoir. This internal pressure suppresses the vaporization of the fluid and reduces the likelihood of the oil and gas mixing, which would lead to erratic damping response. Consequently, vehicles equipped with gas charged shock absorbers experience improved road holding capabilities, enhanced driver control during cornering and braking, and a generally firmer, yet controlled, ride quality. This technological advantage positions gas charged units as the preferred choice in both Original Equipment Manufacturing (OEM) and high-quality aftermarket replacement sectors.

Major applications of gas charged shock absorbers span across light-duty passenger vehicles (sedans, hatchbacks, SUVs), commercial vehicles (trucks, buses), and specialized off-road and racing vehicles where extreme conditions demand maximum reliability and consistent damping. Driving factors for market growth include stringent global safety regulations mandating superior vehicle stability, the increasing average age of vehicles on the road driving aftermarket demand for replacement parts, and the growing consumer preference for SUVs and crossover vehicles which necessitate robust suspension systems to handle higher centers of gravity. Furthermore, the continuous focus on vehicle dynamics and driver safety, particularly in emerging economies, solidifies the foundational demand for high-performance suspension components like gas charged shock absorbers, pushing manufacturers toward continuous material and design innovation.

The global Automotive Gas Charged Shock Absorbers Market is characterized by robust growth, primarily driven by the consistent expansion of the global automotive fleet and mandatory safety feature upgrades across major manufacturing regions. Business trends indicate a strong move toward advanced manufacturing techniques, focusing on integrating lightweight materials like aluminum alloys to reduce overall vehicle weight and improve fuel efficiency, a key compliance factor for OEMs. There is a discernible shift in the competitive landscape where major established players are acquiring smaller specialized firms to integrate advanced electronic damping technologies, preparing for the transition toward fully integrated semi-active and active suspension systems, which often rely on gas charging principles for base performance stabilization. Furthermore, the longevity and reliability of modern vehicles are increasing, extending the average vehicle replacement cycle, which in turn fuels the lucrative, high-volume aftermarket segment for replacement gas charged shock absorbers, supporting continuous revenue streams for specialized suppliers and distributors worldwide.

Regional trends reveal that the Asia Pacific (APAC) region, spearheaded by China and India, remains the dominant growth engine, attributed to surging vehicle production volumes, rapid urbanization, and increasing disposable income leading to higher demand for personal transportation, particularly SUVs and crossovers that require optimized damping. North America and Europe, while being mature markets, exhibit strong demand due to stringent vehicle maintenance mandates and a robust consumer base prioritizing performance and safety, driving uptake of premium, electronically adjustable gas charged units. These established regions are critical hubs for research and development, particularly concerning the integration of advanced driver-assistance systems (ADAS) where optimized vehicle handling is paramount. Consequently, regulatory frameworks in Europe focusing on vehicle safety and emissions are influencing design parameters, pushing manufacturers toward more efficient and durable components.

Segment trends highlight the dominance of the Twin-Tube design in the mass-market passenger vehicle category due to its cost-effectiveness and relatively simple construction, offering a balance between comfort and performance for everyday driving. Conversely, the Monotube segment is witnessing faster growth, predominantly in high-performance, heavy-duty, and premium vehicle applications, owing to its superior heat dissipation capabilities and consistent performance under extreme stress, directly addressing the requirements of modern electric vehicles (EVs) which have increased weight due to heavy battery packs. The aftermarket segment is projected to grow faster than the OEM segment during the forecast period, driven by the replacement needs of the massive installed vehicle base, coupled with customization trends where consumers upgrade their standard hydraulic shocks to performance-oriented gas charged variants for enhanced driving experience. This demand bifurcation requires manufacturers to maintain diverse product portfolios catering to both mass-market cost sensitivity and performance-oriented premium requirements.

User queries regarding AI in the shock absorber market primarily revolve around three themes: Predictive Maintenance (Can AI detect shock failure before it happens?), Manufacturing Optimization (How can AI improve production efficiency and reduce defects?), and Integration with Smart Suspension (Will AI manage the damping forces in real-time?). Users are keen to understand how AI-driven predictive analytics, utilizing sensor data from existing electronic suspension systems, can revolutionize aftermarket sales by accurately forecasting component replacement needs, thereby creating targeted sales opportunities for gas charged absorbers. Furthermore, there is significant interest in how AI and machine learning algorithms are being employed to optimize complex manufacturing processes, such as the precise gas charging and fluid filling stages, ensuring zero-defect rates and maintaining the high-pressure integrity required for longevity. The overarching expectation is that AI will transform the shock absorber from a passive mechanical component into an integral, intelligent part of the overall vehicle dynamics control system, particularly in autonomous and semi-autonomous vehicles, demanding highly responsive gas charged units capable of instantaneous electronic adjustment.

The integration of AI into the automotive suspension ecosystem marks a paradigm shift from traditional, purely mechanical damping solutions toward data-driven, adaptive systems. AI algorithms process continuous input from various vehicular sensors—including accelerometers, gyroscopes, and road surface recognition cameras—to instantly calculate the optimal damping force required for each wheel. This real-time calculation is then executed by electronically controlled gas charged shock absorbers, enabling a level of precision in ride comfort and safety previously unattainable. For instance, in an aggressive cornering scenario, AI can pre-emptively stiffen the outer shocks and soften the inner shocks to minimize body roll, thus maximizing tire grip and enhancing stability. This dependence on rapid, accurate adjustments elevates the importance of high-fidelity, consistent damping provided by gas charged units, particularly those equipped with solenoid valves for electronic control.

Beyond vehicle performance, AI significantly impacts the supply chain and end-user experience. Manufacturers are leveraging machine learning for demand forecasting, inventory management, and optimizing distribution channels, particularly crucial for the aftermarket where inventory needs to be closely matched with vehicle demographics and average component lifespan predictions. In the manufacturing plant, Computer Vision systems powered by AI are performing ultra-precise quality checks on critical weld points, sealing integrity, and gas pressure levels, surpassing human capabilities in detecting microscopic defects that could lead to premature failure. This analytical capability ensures that the final product—the gas charged shock absorber—meets the extremely high durability and performance standards required by modern vehicle platforms, thereby reducing warranty claims and enhancing brand reliability in a highly competitive component market.

The Automotive Gas Charged Shock Absorbers market growth is primarily driven by stringent global regulatory requirements focused on vehicle safety and occupant protection, demanding superior stability and control, particularly during emergency maneuvers. These regulations necessitate the use of components that ensure consistent road-holding capabilities, which gas charged shocks reliably deliver by minimizing shock fade. However, the market faces significant restraints, most notably the volatility and high cost of raw materials such as steel, specialized hydraulic oils, and the requisite seals and internal valves, which directly impact manufacturing costs and final product pricing, making cheaper conventional alternatives appealing in price-sensitive markets. Significant opportunities emerge from the convergence of suspension technology with Advanced Driver-Assistance Systems (ADAS) and the proliferation of electric vehicles (EVs). EVs, due to their heavy battery packs, require robust, high-performance damping systems to manage the increased mass and low center of gravity; gas charged shocks, especially those integrated with electronic control, are ideally suited to meet these specific dynamic requirements, presenting a crucial growth avenue. These forces collectively shape a market environment where technological innovation in materials and electronics is essential to overcome cost restraints and capitalize on regulatory and technological drivers.

The structural impact forces influencing the market trajectory are multifaceted. The first major impact force is the mandatory vehicle renewal cycle, particularly in mature economies, creating a stable, high-volume replacement market that buffers the industry against fluctuations in new vehicle sales. The second force is the increasing complexity of vehicle platforms, especially the adoption of SUVs and light trucks globally, which require more sophisticated, durable gas charged absorbers designed to handle higher loads and dynamic stresses compared to traditional sedans. The third critical force is the ongoing consolidation among Tier 1 suppliers, which allows for greater R&D investment into new technologies like continuous damping control (CDC) and magneto-rheological fluids, enhancing the performance envelope of gas charged designs. Conversely, the threat of substitution by highly advanced, non-shock-absorber suspension alternatives, although nascent, represents a long-term impact force that demands continuous innovation to maintain market relevance.

In terms of specific constraints, the complexity and precision required in the manufacturing process—specifically the high-pressure gas filling and sealing operations—pose technical hurdles. Maintaining the precise internal pressure and preventing gas leakage over the long lifespan of the vehicle necessitates capital-intensive machinery and rigorous quality control, acting as a barrier to entry for new competitors. Furthermore, consumer education remains a restraint; while performance enthusiasts understand the benefits of gas charged shocks, the average vehicle owner often defaults to the cheapest viable replacement, overlooking the safety and performance advantages of premium gas charged units. Market players must thus invest in both technological superiority and consumer outreach to fully leverage the opportunities presented by regulatory mandates and the undeniable performance benefits these components offer, especially concerning vehicle stability and reducing stopping distances, which are key safety metrics.

The Automotive Gas Charged Shock Absorbers Market is comprehensively segmented based on product design type, vehicle application, sales channel, and geographic region, allowing for granular analysis of market dynamics and targeted strategic development. The fundamental segmentation by Type differentiates between Monotube and Twin-Tube designs, reflecting varying performance capabilities, complexity, and cost structures, which dictate their suitability for different vehicle categories. The Monotube design, known for its superior heat dissipation and consistent performance, dominates the premium, racing, and heavy-duty segments, while the cost-effective and structurally simpler Twin-Tube design retains market leadership in volume passenger vehicles. Understanding this design dichotomy is crucial for manufacturers planning capacity and R&D investment, as the ongoing shift toward higher-performance vehicles favors the Monotube architecture due to its intrinsic performance advantages and ease of integration with electronic damping systems.

Segmentation by Vehicle Type is critical, differentiating between Passenger Vehicles (which include light-duty cars, SUVs, and crossovers) and Commercial Vehicles (HCVs and LCVs). Passenger vehicles represent the largest volume segment, heavily driven by aesthetic trends and comfort expectations, leading to rapid adoption of semi-active gas charged shocks that balance comfort and stability. Conversely, the Commercial Vehicle segment prioritizes durability, load-bearing capability, and long service life, focusing on heavy-duty gas charged designs capable of withstanding continuous, high-stress operation and extreme payload variations. Furthermore, the segmentation by Sales Channel—OEM vs. Aftermarket—highlights distinct logistical and pricing strategies; OEM contracts require stringent quality standards and bulk pricing, whereas the Aftermarket demands wide product availability, brand recognition, and competitive pricing for individual replacement units, offering significantly higher profit margins per unit.

The intricate nature of the suspension market requires detailed segmentation analysis to capture nuanced shifts in demand. For instance, within the aftermarket, there is a further distinction between standard replacement shocks and performance/upgrade shocks, with the latter showing rapid growth driven by vehicle customization trends among younger demographics and off-road enthusiasts. Regional segmentation remains paramount, as regulatory standards, road infrastructure quality, and consumer purchasing power vary drastically, requiring localized product specifications, particularly concerning damping settings and material choices to withstand environmental factors like extreme heat or heavy salt exposure. Successful market penetration relies on simultaneously mastering the technical specifications across Type and Application segments while optimizing the distribution efficiency across the distinct sales channels globally.

The value chain for Automotive Gas Charged Shock Absorbers is complex, beginning with the procurement of critical raw materials such as specialized high-strength steel tubes, piston rods, hydraulic sealing systems (elastomers), specialized low-foaming hydraulic fluids, and inert nitrogen gas. The upstream analysis focuses heavily on material sourcing and commodity pricing volatility, which greatly influence the manufacturing cost base. Key activities in this stage include forging, precision machining of internal components (like pistons and valving), and rigorous material quality testing to ensure components can withstand extreme internal pressures and repetitive dynamic loading over a vehicle’s lifespan. Strong relationships with reliable steel suppliers and specialized fluid manufacturers are critical to maintaining the quality and consistency required for high-performance gas charged units, where even minor variations in material composition can lead to performance degradation or premature failure.

The core manufacturing and assembly stage involves high-precision processes, including tube preparation, induction hardening of piston rods, specialized sealing installation, and the critical step of high-pressure gas charging. This stage represents the largest value addition, requiring significant investment in automated assembly lines and proprietary gas filling equipment to ensure precise internal pressure and leak-free operation. The distribution channel analysis highlights a dual structure: Direct distribution dominates the OEM channel, involving long-term supply agreements, just-in-time (JIT) delivery, and stringent quality audits at the manufacturer’s assembly plant. In contrast, the aftermarket relies on an indirect distribution network involving large national distributors, regional wholesalers, and local independent repair shops or specialized retailers, requiring extensive logistical support, inventory holding, and marketing efforts aimed at brand awareness and mechanic preference.

Downstream analysis centers on the end-user segments, which include global automotive OEMs for new vehicle installation and the vast independent service channels for replacement needs. The complexity of the product means that installation and technical service are crucial components of the downstream value proposition; specialized training for mechanics is often required, particularly for modern semi-active and active gas charged suspension systems that involve electronic sensors and control units. The longevity and reliability of the final product are paramount, directly influencing brand reputation and replacement cycle loyalty. Therefore, effective warranty management and customer support provided through both direct (OEM) and indirect (Aftermarket) channels are essential for maximizing total lifetime value and maintaining strong market positioning against competing suspension technologies.

The primary customers for Automotive Gas Charged Shock Absorbers are distinctly split between the Original Equipment Manufacturers (OEMs) and the expansive Aftermarket segment. OEMs, including global automotive giants such as Toyota, Volkswagen, General Motors, and emerging EV manufacturers like Tesla and BYD, represent the largest volume buyers, purchasing millions of units annually under highly competitive long-term contracts for their new vehicle production lines. These customers demand highly specific performance characteristics, rigorous quality control documentation, and seamless integration capabilities with vehicle chassis design and electronic control systems. Securing OEM contracts requires extensive R&D collaboration and often leads to customized product development, driving significant initial revenue and establishing the technological benchmark for the supplier in the industry.

The second substantial customer group comprises the various entities within the aftermarket channel, dedicated to vehicle maintenance, repair, and modification. This includes large multinational parts distributors (e.g., AutoZone, Advance Auto Parts, LKQ), independent wholesale parts dealers, specialized fleet maintenance operators (for heavy-duty trucks and buses), and local independent garages and repair shops who perform the final installation service. Aftermarket customers prioritize product availability, competitive pricing, ease of installation, and a comprehensive product catalogue covering a wide range of vehicle models and years. A rapidly growing niche within the aftermarket consists of performance enthusiasts and off-road modifiers who seek premium, adjustable gas charged units to enhance their vehicle’s dynamics beyond factory specifications, driving demand for specialized, high-margin product lines.

Furthermore, government agencies managing large public sector vehicle fleets (police cars, ambulances, municipal utility vehicles) also represent a crucial customer segment, particularly for heavy-duty gas charged shocks designed for continuous, high-stress operation and maximum reliability. These buyers focus on total cost of ownership (TCO) and durability, often selecting vendors who can provide centralized procurement and specialized technical support for their unique operational requirements. Consequently, suppliers must tailor their sales and marketing efforts to address the distinct priorities of each customer group—volume and compliance for OEMs, logistics and competitive pricing for mass aftermarket distributors, and technical performance and durability for specialty and fleet buyers—to capture maximum market share across the entire value spectrum.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 billion |

| Market Forecast in 2033 | USD 6.7 billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tenneco (DRiV), ZF Sachs AG, KYB Corporation, Showa Corporation, Magneti Marelli (Marelli), Bilstein, Monroe Shocks and Struts, Meritor, Boge, Gabriel, ACDelco, KONI, Hitachi Astemo, Öhlins Racing, Trelleborg |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Automotive Gas Charged Shock Absorbers Market is rapidly evolving, moving beyond simple passive damping toward sophisticated, electronically managed systems that still fundamentally rely on the gas charge principle for core performance stability. A significant area of focus is the development and commercialization of semi-active and active suspension technologies, such as Continuous Damping Control (CDC) and adaptive damping systems. These systems incorporate solenoid valves or magneto-rheological fluids within the gas charged shock absorber body, allowing the vehicle’s Electronic Control Unit (ECU) to adjust the damping force instantaneously, often hundreds of times per second. This real-time adjustability, which optimizes ride comfort and handling dynamically based on road conditions and driving style, represents the premium segment of the market and is increasingly adopted by luxury and performance vehicle manufacturers globally, offering a superior blend of stability and refinement.

Material science and manufacturing precision constitute another critical technological frontier. Manufacturers are actively pursuing lightweighting strategies, incorporating high-strength aluminum alloys and composites in non-critical components of the shock absorber assembly to reduce unsprung mass, thereby improving fuel efficiency and overall vehicle dynamics. Parallel advancements are seen in sealing technology, where new generation high-durability polymers and seal designs are being employed to ensure the longevity and integrity of the internal nitrogen gas charge, significantly extending the service life and performance consistency of the shock absorber, mitigating the risk of premature failure or gas leakage. Furthermore, specialized hydraulic fluids with advanced thermal stability and viscosity characteristics are being developed to withstand the increased heat generated by electronically controlled damping mechanisms operating under high frequency and stress.

Finally, the integration of sensor technology is transforming the passive component into a smart sensor node. Modern gas charged shocks are increasingly equipped with integrated displacement sensors or accelerometers that provide critical data back to the vehicle’s ADAS and central dynamics control system. This sensor feedback loop is vital for enabling predictive maintenance and enhancing safety features like electronic stability control (ESC) and roll mitigation systems. For the future, the research is centered on developing fully customizable, modular shock absorber designs that can be rapidly adapted for diverse platform architectures, particularly those supporting the rapid expansion of standardized EV chassis. These technological advancements ensure the continued relevance and necessity of gas charged shock absorbers even as the automotive industry transitions towards autonomous and fully electric powertrains, demanding unprecedented levels of reliability and real-time control over vehicle motion.

The global market for Automotive Gas Charged Shock Absorbers demonstrates distinct growth trajectories and competitive dynamics across key geographical regions, dictated by localized production volumes, regulatory environments, and consumer preferences for vehicle type and performance. Asia Pacific (APAC) holds the dominant market share and is expected to exhibit the fastest growth over the forecast period. This dominance is directly attributable to the massive automotive manufacturing base in countries like China, India, Japan, and South Korea, which collectively produce the highest volume of both passenger and commercial vehicles globally. The rapid infrastructure development and the increasing adoption of LCVs and SUVs across emerging Asian economies necessitate durable, reliable suspension components, creating immense OEM demand. Furthermore, the burgeoning middle class in APAC drives a strong replacement market as the installed fleet ages.

North America and Europe represent mature, yet highly profitable, markets characterized by high average revenue per unit. In North America, demand is heavily skewed toward high-performance, premium, and heavy-duty gas charged shocks due to the prevalence of light trucks, SUVs, and a strong culture of vehicle customization and high-mileage driving. Safety regulations are rigorously enforced, driving consistent aftermarket replacement demand for high-quality, dependable units. Europe is defined by stringent environmental and safety standards, which accelerate the adoption of advanced semi-active gas charged shocks integrated with complex electronic control systems. European manufacturers prioritize systems that improve vehicle dynamics while contributing to overall vehicle efficiency, focusing on lightweight materials and high-precision damping control.

The markets in Latin America (LATAM) and the Middle East and Africa (MEA) are emerging, characterized by increasing vehicle imports and rising regional assembly activities. While volume is currently lower compared to APAC, these regions present significant growth potential, driven by improving economic conditions and the necessity for robust suspension systems capable of handling challenging road conditions, often found in developing urban and rural areas. This environment favors durable, standard-issue gas charged shock absorbers, prioritizing longevity and load-bearing capacity over advanced electronic features. Strategic expansion into these regions involves establishing localized distribution partnerships and focusing on cost-competitive, reliable replacement products to capture the burgeoning demand for basic vehicle maintenance and repair needs.

Gas charged shock absorbers include a pressurized inert gas (usually nitrogen) separated from the hydraulic fluid, which prevents the fluid from foaming or aerating (cavitation) during rapid movement. This ensures consistent damping force, eliminates shock fade, and provides superior stability and handling, particularly under strenuous driving conditions compared to standard hydraulic units.

The Monotube design is generally superior for heavy-duty and performance vehicles. It offers a larger piston surface area and better heat dissipation due to its structure, leading to more consistent performance, greater durability, and superior resistance to shock fade when carrying heavy loads or operating continuously at high speeds.

EVs positively influence the market because their heavy battery packs necessitate high-performance, robust suspension components to manage the increased vehicle weight and lower center of gravity. Gas charged shocks, especially electronically controllable types, are essential for providing the stability, comfort, and precise damping required for modern electric vehicle architectures.

The aftermarket is driven by the increasing average age and mileage of the global vehicle fleet, which necessitates periodic replacement of worn-out shocks. Additionally, consumer demand for performance upgrades and vehicle customization, often involving switching from standard shocks to high-performance gas charged variants, significantly boosts aftermarket revenue.

AI is crucial for integrating these components into smart suspension systems (semi-active/active). AI algorithms process real-time sensor data to determine and instantaneously adjust the optimal damping force in the gas charged shock absorber via electronic valves, maximizing vehicle safety, stability, and ride comfort dynamically.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.