ID : MRU_ 433209 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

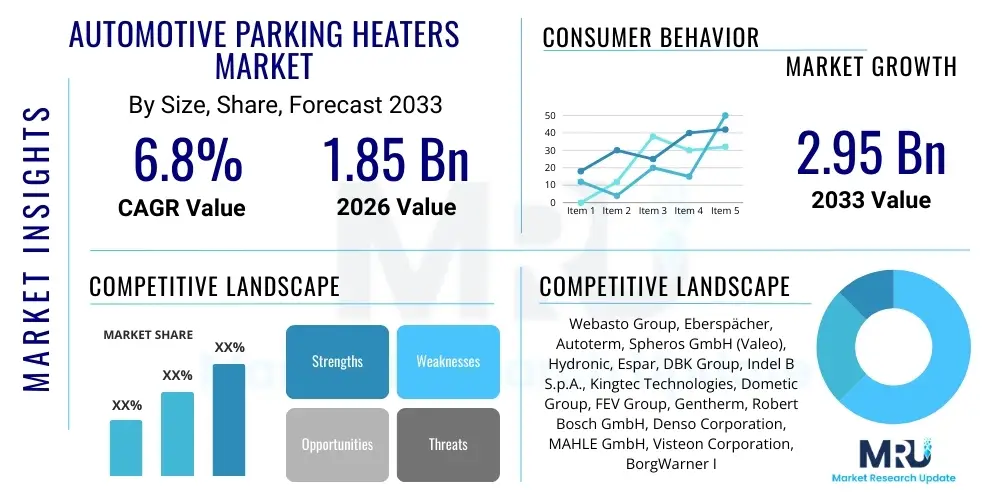

The Automotive Parking Heaters Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 2.95 Billion by the end of the forecast period in 2033.

The Automotive Parking Heaters Market encompasses advanced thermal management systems designed to autonomously heat a vehicle's engine and passenger compartment without requiring the engine to be running. These systems utilize fuel (diesel or gasoline) or electricity to generate heat, significantly improving driver comfort, vehicle performance in cold weather, and reducing harmful cold-start emissions. The primary product categories include air heaters, which directly heat the cabin, and water heaters, which integrate with the engine cooling system to preheat both the engine block and the cabin simultaneously, ensuring immediate optimal operating temperatures upon start-up.

Major applications for parking heaters span across various segments of the transportation industry, including heavy-duty trucks, buses, trains, marine vessels, recreational vehicles (RVs), and high-end passenger vehicles, particularly SUVs and luxury sedans in colder climates. In the commercial sector, these heaters are critical for fleet operations, allowing drivers to maintain comfortable cab temperatures during mandatory rest periods without idling the engine, thereby saving fuel and complying with increasingly stringent anti-idling regulations prevalent across North America and Europe. For passenger vehicles, the appeal lies in enhanced convenience and safety, ensuring clear windshields and a warm interior before the driver enters the vehicle.

Key benefits driving the market include substantial fuel consumption reduction compared to engine idling, significant cuts in harmful pollutant emissions (particularly nitrogen oxides and particulate matter), and extension of engine life by minimizing wear and tear associated with cold starts. The rising awareness regarding environmental sustainability and the concurrent implementation of supportive regulatory frameworks mandating reduced idling, especially in urban centers and commercial trucking operations, are pivotal factors accelerating market penetration globally. Furthermore, advancements in telematics and connectivity are making these systems more user-friendly, allowing remote activation and integration with vehicle diagnostic systems.

The global Automotive Parking Heaters market is currently characterized by robust technological development centered around efficiency and connectivity, shifting away from purely mechanical control towards sophisticated electronic interfaces and integration with smart vehicle systems. Business trends indicate a strong focus on the OEM segment, driven by vehicle manufacturers increasingly offering integrated heating solutions as premium features or standard equipment in models targeted at cold-weather markets. Furthermore, sustainability pressures are accelerating the transition towards electric and hybrid heater solutions, particularly in line with the surging electric vehicle (EV) penetration, prompting established market leaders to diversify their product portfolios to include high-voltage compatible systems designed for battery pre-conditioning and efficient cabin heating in zero-emission vehicles. Strategic acquisitions and long-term supply agreements between heater manufacturers and global Tier 1 automotive suppliers are consolidating the market structure.

Regionally, Europe maintains the dominant market share, primarily due to severe winter conditions, a high concentration of commercial trucking operations subject to strict anti-idling laws, and the historical presence of key manufacturing hubs for parking heater technology in countries like Germany and Sweden. However, the Asia Pacific (APAC) region, particularly China and Russia, is poised for the highest growth rate, fueled by rapid expansion of the logistics sector, increasing disposable incomes leading to higher passenger vehicle sales, and governmental efforts to improve transportation safety and energy efficiency in extremely cold territories. North America’s growth is steady, largely propelled by the heavy-duty truck segment adopting fuel-saving and compliance technologies, though the penetration rate in consumer passenger vehicles remains comparatively lower than in Northern Europe.

Segment trends highlight the growing preference for water heaters, especially in heavy commercial vehicles, due to their dual benefit of cabin comfort and engine protection, though air heaters remain dominant in smaller vans, RVs, and auxiliary heating applications where faster cabin warming is paramount. Regarding fuel type, while diesel heaters currently dominate the market due to the high prevalence of diesel engines in the commercial sector, the electric/battery-powered segment is witnessing exceptional growth. This acceleration is directly attributed to the industry-wide pivot toward electrification, demanding high-efficiency heating solutions that draw minimal power from the main traction battery while still providing adequate interior comfort and critical battery temperature management during charging and cold operation cycles.

User inquiries regarding AI's influence on the Automotive Parking Heaters market predominantly focus on predictive maintenance, optimization of energy consumption, and integration with intelligent vehicle systems. Users are concerned about how AI algorithms can ensure the heater operates only when necessary, minimizing battery drain and fuel waste, and how machine learning can predict component failures (like glow plug or pump issues) before they occur, reducing unexpected downtime, especially for commercial fleets. Key expectations center around personalized heating profiles and dynamic thermal management that adapts instantly to varying external temperatures, humidity, and real-time cabin occupancy, moving beyond simple timer settings to truly smart, anticipatory operations.

Artificial Intelligence is beginning to transform parking heater functionality by enabling sophisticated predictive thermal management. Instead of relying solely on preset timers or manual remote activation, AI-driven systems leverage external data sources—such as weather forecasts, geographical location, vehicle usage patterns, and calendar scheduling—to anticipate heating needs. This allows the heater to calculate the minimal effective operating time required to reach a desired temperature just before the user plans to depart, drastically improving energy efficiency, whether the unit is fuel-based or purely electric. Furthermore, AI helps optimize the duty cycle, ensuring efficient combustion in fuel heaters and managing power draw in electric systems to prevent excessive strain on the vehicle's electrical infrastructure, particularly in long-term parking scenarios.

The application of machine learning extends significantly into the aftermarket and fleet management sector, particularly concerning maintenance protocols. By continuously monitoring operational parameters such as fan speed, fuel delivery rate, exhaust gas temperature curves, and start-up cycle anomalies, AI algorithms can detect subtle deviations that signal impending component degradation. This capability shifts maintenance from reactive or time-based schedules to highly accurate condition-based monitoring, allowing fleet managers to proactively replace parts like fuel pumps or air intake filters during scheduled downtimes. This preventative approach maximizes operational uptime for commercial vehicles, providing a substantial return on investment for adopting smart heating systems integrated with telematics platforms.

The market growth is primarily propelled by stringent environmental regulations aimed at curbing vehicle idling emissions, coupled with the increasing emphasis on driver comfort and safety in commercial vehicle operations across cold regions. However, the market faces constraints related to high initial installation costs and the technical complexities associated with integrating advanced systems into modern, complex vehicle architectures. Opportunities emerge through rapid electrification of the automotive industry, demanding specialized electric heating solutions, and the expansion into emerging markets such like Russia and Central Asia. These factors collectively exert significant impact forces, compelling manufacturers to focus on product miniaturization, efficiency improvements, and system integration capabilities to maintain competitiveness and capitalize on global regulatory trends favoring non-idling solutions.

Key drivers include the global implementation of anti-idling laws, which incentivize the adoption of parking heaters as legal alternatives for maintaining cabin temperature during rest periods. Additionally, the severe weather conditions in Northern Europe, North America, and specific Asian regions necessitate reliable pre-heating solutions to ensure engine longevity and immediate driver visibility. Increased consumer awareness regarding the benefits of reduced fuel consumption and lower environmental impact also contributes significantly. On the restraint side, the primary obstacle is the substantial upfront capital expenditure required for premium parking heater units and professional installation, which can deter cost-sensitive private consumers and small fleet operators. Furthermore, technical issues related to battery voltage management, especially in aftermarket installations, sometimes raise user complaints regarding battery drain, creating a perception barrier.

Opportunities for market expansion are abundant in the field of electric parking heaters, specifically designed for Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs), which require highly efficient auxiliary heating to maximize driving range. Strategic focus on emerging markets with underdeveloped infrastructure but rapidly growing commercial sectors, such as Eastern Europe, Russia, and Central Asia, also presents lucrative potential. Impact forces include the high R&D intensity required to meet evolving efficiency standards and the constant pressure to reduce system weight and size. The competitive landscape is also shaped by intellectual property rights and strategic partnerships, as major players vie for exclusive OEM contracts to secure long-term stable revenue streams and establish technological dominance in connected and automated thermal management systems.

The Automotive Parking Heaters Market is analyzed based on product type, fuel type, vehicle type, and distribution channel, providing a granular view of market dynamics and adoption rates across different industrial and consumer applications. Product segmentation between air and water heaters is crucial, reflecting distinct functional requirements where air heaters prioritize rapid cabin heating, and water heaters offer comprehensive engine pre-heating alongside interior comfort. Fuel type segmentation highlights the necessary pivot from traditional diesel and gasoline systems towards electric solutions, which are becoming indispensable for the rapidly expanding electric vehicle fleet globally. Furthermore, the split between OEM and Aftermarket distribution channels indicates the maturity and growth strategy of suppliers, with OEM integration driving long-term stability and the aftermarket catering to replacement and fleet upgrade cycles.

Analysis by vehicle type reveals that the Heavy Commercial Vehicle (HCV) segment remains the most dominant consumer of parking heaters, driven by rigorous operational demands, long-haul transportation requirements, and regulatory compliance. However, the Light Commercial Vehicle (LCV) and Passenger Car segments are rapidly gaining traction, particularly as manufacturers integrate these systems into premium and cold-weather packages to enhance customer value proposition and differentiate products. The complexity and cost of installation often correlate directly with the vehicle type, with factory-installed OEM units on passenger cars demanding seamless integration into the vehicle’s CAN bus architecture and infotainment system for enhanced user control.

Geographical segmentation is paramount, demonstrating significant variances in market maturity and regulatory impact. Europe, with its established regulatory framework and severe winters, leads the consumption, showcasing high penetration rates in both commercial and passenger sectors. Conversely, high-growth potential is observed in APAC, driven by economic development in large countries like China and the vast, cold territories of Russia. Understanding these segmented dynamics allows stakeholders to tailor product offerings, marketing strategies, and distribution networks, focusing R&D investment on the specific technical requirements—such as high-altitude operation or extreme low-temperature start-up reliability—pertinent to the fastest-growing geographical segments.

The value chain for the Automotive Parking Heaters market begins with the upstream suppliers providing essential raw materials and specialized electronic and combustion components. This includes suppliers of high-grade ceramics for glow plugs, specialized polymers for housing and ducting, microcontrollers and sensors for system control, and precision-engineered fuel pumps. Efficiency in this stage is critical, as the quality of sensors and the thermal resistance of materials directly influence the heater's reliability and lifespan. Key manufacturers in the upstream segment focus on proprietary technologies, ensuring compliance with strict automotive quality standards (e.g., ISO/TS 16949) and achieving supply chain resilience to maintain consistent production volumes for major heater assemblers.

The core manufacturing and assembly phase involves the integration of these components into the final parking heater unit, a process dominated by specialized global companies like Webasto and Eberspächer. This stage encompasses rigorous testing for combustion efficiency, thermal output, electromagnetic compatibility (EMC), and operational safety. Manufacturers employ lean manufacturing techniques and automation to manage costs and maintain high production standards. Following assembly, the downstream phase focuses on distribution channels, primarily bifurcated into OEM supply and the aftermarket. OEM sales involve long-term contracts and direct supply lines to vehicle assembly plants, demanding just-in-time delivery and high customization based on specific vehicle architecture requirements.

Distribution channels for the aftermarket segment are diverse, involving independent workshops, certified installers, specialized automotive parts distributors, and increasingly, e-commerce platforms. Direct and indirect distribution strategies are heavily utilized; direct distribution often handles large fleet orders or specialized vehicle installations, ensuring professional integration and warranty compliance. Indirect channels leverage a broad network of retailers and certified installers who manage the sale, fitting, and maintenance of aftermarket units. The effectiveness of the indirect channel heavily relies on comprehensive training and technical support provided by the heater manufacturers to maintain installation quality, which is crucial for product performance and customer satisfaction, thus completing the flow from material sourcing to end-user application.

The primary customers for Automotive Parking Heaters are highly diversified, encompassing large commercial fleet operators, manufacturers of premium and heavy-duty vehicles, and individual consumers residing in geographical areas characterized by extended periods of low temperatures. Commercial buyers, such as logistics companies, public transportation authorities (buses and coaches), and construction firms, are driven by operational efficiency and regulatory adherence. For these entities, parking heaters are not luxury items but essential tools that maximize driver comfort during mandated rest periods (preventing costly fines associated with unauthorized engine idling), reduce unnecessary fuel expenditure, and ensure the reliability of engine starts in extreme cold, directly impacting their total cost of ownership (TCO).

The second major category of customers includes Original Equipment Manufacturers (OEMs) of passenger cars, particularly in the luxury and high-end SUV segments. OEMs purchase parking heaters for factory installation to enhance vehicle value, offering a distinct competitive advantage in cold-climate markets like Canada, Scandinavia, and Northern Russia. These purchasing decisions are guided by strict integration requirements, system efficiency, and seamless incorporation into the vehicle’s telematics and HMI (Human Machine Interface). Furthermore, manufacturers of specialized vehicles, including ambulances, police vehicles, military equipment, and refrigerated trucks (requiring auxiliary heating for cab or cargo management), represent specialized yet crucial customer segments demanding robust, reliable, and often explosion-proof or high-output heating solutions.

The final significant segment is the aftermarket consumer, comprising individual vehicle owners seeking to upgrade older vehicles or install heaters on vehicles where the option was not factory-installed (especially RVs and light commercial vehicles). These buyers are often motivated by personal comfort, desire for quick defrosted visibility for safety reasons, or environmental consciousness regarding idling. For this customer base, factors such as ease of installation, perceived brand reliability, warranty coverage, and the availability of professional certified installation services are paramount. The emergence of affordable and user-friendly remote-controlled or app-enabled systems is effectively lowering the barrier to entry for this consumer segment, expanding the overall market reach beyond traditionally high-cost applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.95 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Webasto Group, Eberspächer, Autoterm, Spheros GmbH (Valeo), Hydronic, Espar, DBK Group, Indel B S.p.A., Kingtec Technologies, Dometic Group, FEV Group, Gentherm, Robert Bosch GmbH, Denso Corporation, MAHLE GmbH, Visteon Corporation, BorgWarner Inc., Arctic Traveler, Thermo King (Trane Technologies), Kalori SAS |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Automotive Parking Heaters market is rapidly evolving, driven primarily by the need for increased energy efficiency, smaller footprints, and integration into the vehicle’s digital ecosystem. Modern fuel-fired heaters utilize advanced combustion technologies, including optimized burners and microprocessor control units (MCUs), to ensure clean, efficient combustion across a wide range of altitudes and fuel qualities. The shift is towards modulating heat output, where the heater dynamically adjusts its power level rather than simply cycling on and off, leading to smoother operation, significant fuel savings, and reduced carbon buildup. Furthermore, materials science improvements are focusing on lightweight yet durable alloys and ceramics that can withstand extreme thermal cycling and corrosive environments, enhancing overall product lifespan and reliability, which are critical factors for commercial applications.

Connectivity and telematics represent the most influential technological transformation currently impacting the market. New generation parking heaters are increasingly equipped with embedded communication modules (GSM/GPS) or are designed to interface seamlessly with the vehicle's onboard diagnostic (OBD) and Controller Area Network (CAN bus) systems. This integration enables sophisticated remote control via smartphone applications, allowing users to monitor cabin and battery temperatures, schedule heating cycles, and receive diagnostic alerts remotely. This smart connectivity not only enhances user convenience but also provides valuable operational data for fleet managers, supporting the earlier mentioned AI-driven predictive maintenance strategies and proving critical for establishing compliance with non-idling regulations through documented usage logs.

Perhaps the most strategically important technological shift is the development and optimization of high-voltage electric parking heaters (EPH) specifically engineered for Battery Electric Vehicles (BEVs) and fuel cell vehicles. Traditional resistive heaters are inefficient, rapidly depleting the traction battery and reducing the vehicle's range. Therefore, manufacturers are heavily investing in high-efficiency Positive Temperature Coefficient (PTC) ceramic heaters and advanced heat pump auxiliary systems, often paired with smart control algorithms to minimize power draw. These systems are crucial not only for passenger comfort but also for essential battery thermal management, ensuring the lithium-ion battery operates within its optimal temperature window for charging and maximum power output in cold weather, representing a high-growth technological niche within the overall market structure.

The global distribution of the Automotive Parking Heaters Market exhibits pronounced regional disparities, fundamentally driven by climate severity, economic activity, and the implementation of environmental regulations. Europe, particularly Northern and Eastern countries, serves as the mature cornerstone of the market, characterized by high penetration rates in both commercial vehicles and premium passenger cars, benefiting from long-standing regulatory support for anti-idling practices and a strong consumer demand for thermal comfort during harsh winters. Germany, Sweden, and Finland are central hubs for both production and consumption, driving technological innovation in fuel and electric heater solutions.

The Asia Pacific (APAC) region represents the highest potential for future growth, primarily propelled by the vast and severely cold territories of Russia (Far East), Northern China, and Central Asian republics. Rapid industrialization, significant infrastructure projects, and the expanding presence of logistics and heavy-haul trucking industries in these areas create an escalating need for reliable engine and cabin pre-heating systems. While the market historically favored lower-cost options, rising incomes and stricter governmental safety and environmental standards are encouraging the adoption of sophisticated, certified heating solutions, paving the way for substantial growth in both the OEM and certified aftermarket segments.

North America maintains a stable market presence, dominated by the Heavy Commercial Vehicle (HCV) sector, where anti-idling legislation in states like California and across major freight corridors strongly mandates alternative heating solutions. The focus here is overwhelmingly on diesel-fired air heaters for sleeper cabs, prioritizing cost-efficiency and compliance. While passenger vehicle penetration lags behind Europe, the increasing popularity of SUVs and trucks in the coldest regions of Canada and the Northern U.S. is gradually accelerating consumer interest in integrated parking heater options, supported by aggressive marketing efforts emphasizing the safety benefits of immediate windshield defrosting and improved cold-start reliability.

Air heaters are designed to rapidly warm the vehicle's cabin and cargo area directly using forced hot air and are commonly used in trucks and RVs. Water heaters integrate with the engine coolant system to preheat both the engine block and the vehicle interior simultaneously, reducing engine cold wear and ensuring immediate defrosting, making them suitable for passenger cars and comprehensive commercial applications.

Parking heaters drastically reduce overall fuel consumption and emissions by replacing engine idling, which typically burns significantly more fuel per hour. By ensuring efficient combustion and allowing the engine to start at optimal temperatures, they minimize the high pollutant output and fuel waste associated with prolonged cold starts and unnecessary idling, thereby complying with anti-idling regulations.

Yes, the market is rapidly transitioning towards high-voltage electric parking heaters (EPH), driven by the global shift towards Battery Electric Vehicles (BEVs). EPH units are crucial for efficiently managing cabin heating and vital battery pre-conditioning without drawing excessively on the vehicle’s main traction battery, a key factor in maximizing EV driving range during cold weather operation.

Connectivity is essential, enabling advanced features like remote activation via smartphone apps, scheduling capabilities, and integration with telematics systems. This technology enhances user convenience, allows for remote diagnostics and monitoring, and supports fleet management by providing data necessary for efficient operation and regulatory compliance documentation.

The primary restraints include the high initial purchase price of premium parking heater systems and the substantial cost associated with professional installation. Furthermore, consumer concerns regarding the potential for battery drain, particularly in aftermarket installations on older vehicle models, occasionally act as a psychological barrier to mass-market adoption.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.