ID : MRU_ 438423 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

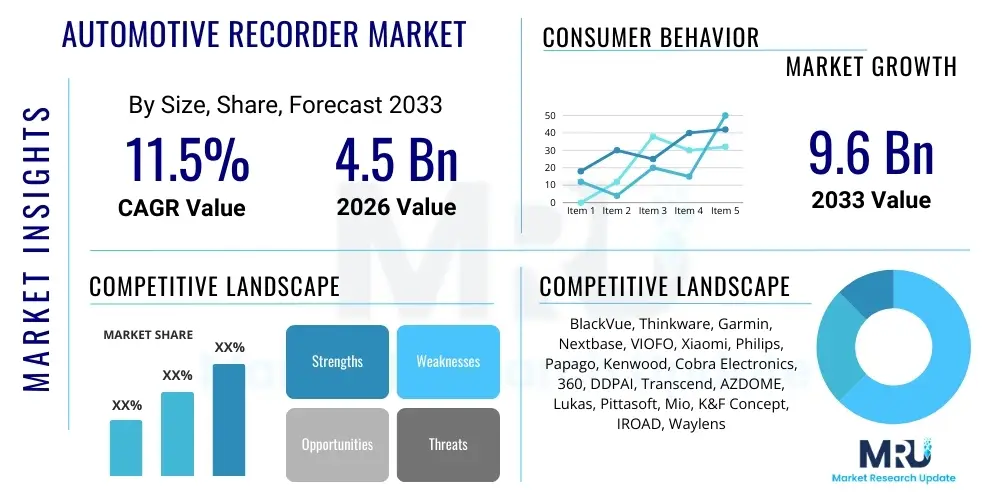

The Automotive Recorder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2033.

The Automotive Recorder Market, commonly encompassing dash cameras (dashcams) and integrated vehicle event recorders, is defined by devices installed in vehicles primarily to record visual and audio data of road events, critical for insurance claims, accident verification, and driver monitoring. These devices range from simple single-channel front-facing cameras to sophisticated multi-channel systems offering 360-degree coverage, integrated GPS logging, and advanced parking surveillance modes. The core function of these recorders is to provide an objective, tamper-proof record of events occurring both inside and outside the vehicle, significantly mitigating disputes in traffic incidents and enhancing road safety accountability.

Product sophistication has surged, moving beyond basic video capture to incorporate advanced features such as Wide Dynamic Range (WDR) and High Dynamic Range (HDR) for optimal clarity under varying light conditions, G-sensors for automatic incident detection and file locking, and integrated Wi-Fi or LTE connectivity for immediate cloud backup and remote access. Major applications span across individual consumer vehicles, fleet management operations, ride-sharing services, and commercial transport logistics. The primary benefits derived from these systems include reduced insurance premiums, faster claim settlements, improved driver behavior monitoring, and concrete evidence against fraudulent claims or road rage incidents. The escalating global awareness regarding road safety and the increasing prevalence of advanced driver-assistance systems (ADAS) further solidifies the foundational role of automotive recorders in the modern vehicle ecosystem.

The market expansion is fundamentally driven by stringent regulatory frameworks concerning vehicle safety, particularly in regions like Europe and specific Asian countries where mandatory installation is being explored or already implemented for commercial vehicles. Concurrently, the proliferation of ride-sharing and last-mile delivery services necessitates robust surveillance solutions to protect both assets and personnel. Technological advancements, particularly in memory storage, processing power, and miniaturization, allow for high-resolution 4K recording capabilities and seamless integration with the vehicle's electrical system, pushing the replacement cycle and encouraging consumer adoption of more premium, feature-rich devices.

The Automotive Recorder Market is experiencing robust acceleration, underscored by significant shifts in consumer perception from viewing these devices as optional accessories to essential safety and liability tools. Key business trends indicate a strong move toward integrated systems that communicate seamlessly with vehicle telematics and cloud infrastructure, fostering subscription-based models for data storage and value-added services such as geo-fencing and emergency notifications. The market is consolidating around manufacturers that can deliver superior image stabilization, low-light performance, and durable solid-state memory solutions suitable for harsh automotive environments. Furthermore, original equipment manufacturers (OEMs) are increasingly incorporating factory-installed recording solutions, posing a substantial challenge and simultaneously providing massive growth opportunities for aftermarket suppliers through collaboration and technology licensing.

From a regional perspective, Asia Pacific (APAC) currently dominates the market, driven primarily by high adoption rates in countries like South Korea, China, and Japan, where public awareness of insurance fraud and traffic density is exceptionally high, coupled with favorable regulatory environments. North America and Europe are exhibiting rapid growth, largely influenced by the expanding commercial fleet sector and the integration of dashcams into broader vehicular safety standards. The rise of litigation culture globally also fuels demand, positioning automotive recorders as non-negotiable proof points in legal proceedings. Emerging markets in Latin America and the Middle East and Africa (MEA) are showing increasing potential as vehicle penetration rises and concerns about road safety escalate.

Segmentation trends highlight the shift from basic standalone dashcams to more complex multi-channel systems (front and rear view, cabin view). The 4K resolution segment is rapidly becoming standard in the mid-to-high price tiers, meeting consumer demand for forensic-level detail. Furthermore, the connectivity segment—specifically Wi-Fi and 4G/5G enabled devices—is witnessing the highest growth rate, reflecting the consumer desire for instant access, real-time alerts, and remote monitoring capabilities, crucial for parking surveillance and fleet oversight. The commercial segment (fleet owners, logistics companies) continues to prioritize durability, reliability, and integration depth with existing telematics platforms, emphasizing the need for robust software management tools alongside hardware performance.

Common user questions regarding AI’s impact on the Automotive Recorder Market frequently center on enhanced safety features, data processing efficiency, and privacy implications. Users are primarily concerned with whether AI can accurately detect and predict dangerous driving behaviors (like drowsiness or distraction) in real-time, how AI-driven analysis will speed up insurance claims processing, and crucially, how large volumes of AI-processed personal video data are secured and anonymized. There is high expectation that AI will transform recorders from passive logging devices into proactive safety systems, but this must be balanced against legitimate concerns about continuous in-cabin surveillance and potential misuse of behavioral data, driving demand for explainable AI (XAI) features within these devices.

The integration of AI algorithms fundamentally elevates the function of automotive recorders. Currently, AI is extensively used for advanced image processing, including superior object recognition (differentiating pedestrians, cyclists, and vehicles), improved license plate reading under motion blur, and sophisticated night vision enhancement through deep learning models. This capability moves the recorder beyond basic incident documentation to providing high-fidelity, context-rich data. Furthermore, AI is critical in developing advanced Parking Mode functionalities, enabling the device to intelligently discern between benign vibrations and true accident impacts, minimizing false recordings and optimizing battery life. This intelligent data acquisition minimizes storage requirements and enhances the utility of the recorded footage for forensic analysis.

The most transformative application of AI is in Driver Monitoring Systems (DMS), particularly relevant for commercial fleets and safety-conscious consumers. AI analyzes facial expressions, head pose, and eye movements to detect signs of distraction, fatigue, or impairment in real-time, triggering immediate warnings to the driver or alerts to fleet managers. This proactive intervention significantly reduces preventable accidents. Furthermore, AI-powered event tagging and summary generation automate the process of sifting through hours of footage post-incident, immediately isolating the critical moments leading up to and following a collision, thereby streamlining the entire insurance verification and legal review process. The future direction involves integrating AI recorders directly into the vehicle's internal network to fuse data from CAN bus systems, providing a complete 360-degree environmental and vehicular state record.

The Automotive Recorder Market dynamics are governed by a robust interplay of Drivers (D), Restraints (R), Opportunities (O), and potent Impact Forces. Key drivers include the rising global incidence of road traffic accidents, leading to greater demand for verifiable evidence, and the continuous push by insurance providers to mitigate risk through incentivizing or mandating the use of recording devices, often through reduced premiums. Additionally, the rapid expansion of the fleet management sector, which utilizes recorders for accountability, efficiency monitoring, and asset protection, acts as a foundational growth engine. These drivers are bolstered by technological maturation, offering higher resolution, increased storage capacity, and integrated connectivity that enhances product value propositions for both consumers and commercial users.

However, significant restraints temper this growth. Primary concerns revolve around data privacy and security, particularly with AI-enhanced recorders capable of continuous in-cabin monitoring, which raises regulatory hurdles concerning General Data Protection Regulation (GDPR) compliance and similar international privacy laws. Furthermore, the inherent risk of data tampering or system failure, especially in less expensive, non-certified devices, creates consumer skepticism regarding reliability. Market penetration is also challenged by the high initial cost of premium, multi-channel systems and the technical complexity involved in integrating these devices with certain vehicle models or older electrical systems, necessitating professional installation and potentially voiding warranties in some jurisdictions.

Opportunities for market expansion are substantial, particularly in the realm of full OEM integration, moving recorders from aftermarket accessories to factory-standard safety features in new vehicles. The convergence of automotive recorders with ADAS and vehicle-to-everything (V2X) communication technologies presents a lucrative future pathway, enabling recorders to capture and contextualize not only video but also sensor data, crash metrics, and external network communications. Moreover, the shift towards subscription-based cloud services for video storage and advanced telematics features represents a strong opportunity for sustained recurring revenue streams. The increasing global focus on autonomous driving testing also necessitates highly reliable, redundant recording mechanisms to document every aspect of the test environment and vehicle behavior, thereby creating a high-value niche market.

The Automotive Recorder Market is comprehensively segmented based on product type, technology, application, and distribution channel, providing a granular view of specific market dynamics. The segmentation reflects the diverse range of end-user requirements, from individual consumer convenience to the rigorous standards of commercial fleet operations. Product complexity is a key differentiator, influencing price points, installation methods, and feature sets, while technology types, such as the shift from basic definition to high-definition and ultra-high-definition cameras, dictate the forensic quality of the captured data.

The application segmentation is particularly crucial, distinguishing between the high-volume consumer aftermarket and the specialized, mission-critical commercial segment, each requiring unique hardware ruggedness and software integration capabilities. The consumer segment often prioritizes ease of use and aesthetic integration, whereas the commercial segment demands centralized management, tamper-proof design, and deep telematics compatibility. Analyzing these segments helps stakeholders tailor product development and marketing strategies to address distinct functional needs across the automotive ecosystem, ensuring maximum market penetration and relevancy.

The Value Chain for the Automotive Recorder Market begins with upstream activities dominated by component manufacturing, including specialized sensor providers (CMOS image sensors), semiconductor companies (microprocessors and memory chips), and lens manufacturers. The competitive advantage at this stage often relies on securing reliable, high-performance components, particularly high-sensitivity image sensors crucial for low-light recording. Design and research & development (R&D) are critical middle-stream activities, where manufacturers integrate hardware with proprietary firmware, focusing heavily on durability, thermal management, and sophisticated software features like collision detection and cloud synchronization. Efficient management of the bill of materials (BOM) and effective intellectual property protection for embedded software are vital for maintaining profitability.

Downstream activities center on assembly, quality control, packaging, and distribution. Quality assurance is paramount, given the exposure of these devices to extreme temperatures and vibrations within a vehicle environment. Distribution channels are highly varied. The aftermarket segment relies heavily on both direct (online retail, dedicated brand websites) and indirect channels (specialty automotive electronics stores, large-format retailers, and third-party installers). This segment thrives on marketing to end-users and providing accessible, self-installation options. The OEM channel, conversely, involves long-term contracts and stringent quality checks, integrating the recorders directly into the vehicle assembly line and electrical architecture.

The crucial role of distribution channels is highlighted by the segmentation of sales between the high-volume, lower-margin aftermarket and the higher-margin, quality-focused OEM channel. Indirect channels, particularly e-commerce platforms, have significantly reduced barriers to entry for new market players, enabling rapid market reach but simultaneously intensifying price competition. For commercial applications, specialized distributors and telematics service providers often form the final link, bundling recorder hardware with fleet management software and installation services. Effective supply chain logistics and robust post-sales support, including software updates and warranty management, are key differentiators in this highly competitive consumer electronics segment of the automotive industry.

The primary consumers of automotive recorders span a wide demographic, segmented into individual vehicle owners focused on personal security and liability protection, and large-scale commercial entities prioritizing asset management, regulatory compliance, and driver safety optimization. Individual consumers are the largest volume buyers, often seeking plug-and-play devices that are easy to install and offer features such as high-resolution video, parking mode, and aesthetic design. Within this group, young drivers, new car owners, and individuals living in high-traffic or high-crime areas show the highest propensity for immediate purchase, utilizing the device primarily for insurance verification and personal evidence in case of an accident.

The commercial segment represents the fastest-growing and highest-value customer base. This category includes logistics and trucking companies requiring comprehensive fleet monitoring for regulatory adherence (e.g., hours-of-service compliance checks using video confirmation) and operational efficiency. Furthermore, ride-sharing and taxi operators are increasingly adopting cabin-view recorders to protect drivers from disputes and passengers from misconduct, making the footage an essential HR and legal resource. These enterprise customers prioritize reliability, centralized cloud data management platforms, G-sensor accuracy, and the ability to integrate recorders into existing GPS and telematics systems for a holistic operational overview.

Other key potential customers include insurance companies themselves, who may offer subsidized devices to policyholders as a loss prevention measure, and government agencies, such as police forces or public transit authorities, which utilize specialized, hardened recording systems for official vehicle fleets. The shift towards connected vehicles means that OEMs and Tier 1 suppliers are also significant buyers, either for proprietary integrated systems or for advanced modules that they incorporate into vehicle builds, addressing safety concerns at the point of manufacture and ensuring seamless interaction with the vehicle's electrical and informational backbone.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BlackVue, Thinkware, Garmin, Nextbase, VIOFO, Xiaomi, Philips, Papago, Kenwood, Cobra Electronics, 360, DDPAI, Transcend, AZDOME, Lukas, Pittasoft, Mio, K&F Concept, IROAD, Waylens |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Automotive Recorder Market is rapidly evolving, driven by the need for superior image fidelity, enhanced reliability, and seamless connectivity. Central to this evolution is the deployment of high-resolution image sensors, particularly those utilizing CMOS technology with backside illumination (BSI), which deliver exceptional low-light performance—a critical requirement for overnight monitoring and high-speed nighttime driving. The standard resolution is steadily shifting from 1080p (Full HD) to 4K (Ultra HD), supported by powerful system-on-chips (SoCs) capable of processing multiple video streams concurrently, essential for sophisticated dual or multi-channel systems. Furthermore, the adoption of advanced video compression codecs like H.265 (HEVC) is crucial for managing the larger file sizes associated with 4K recording without compromising memory card capacity or recording loop efficiency.

Another pivotal technological advancement is the integration of advanced connectivity features, primarily Wi-Fi and 4G/5G cellular modules. Wi-Fi allows for easy viewing and downloading of footage via smartphone apps, while cellular connectivity enables critical remote functionality, including real-time alerts for parking incidents, cloud storage backup for important event files, and GPS tracking updates for fleet management. This shift from purely localized recording to cloud-connected ecosystems enhances the value proposition by adding layers of security and accessibility. Moreover, the reliability of storage media has seen significant improvement, with manufacturers utilizing high-endurance memory cards or internal NAND flash memory designed to withstand the continuous write cycles and extreme temperature variations inherent in automotive environments, reducing failure rates and increasing overall device longevity.

Looking forward, the merging of automotive recorders with Advanced Driver-Assistance Systems (ADAS) represents the cutting edge of the technology landscape. Modern recorders are increasingly integrating ADAS features such as Lane Departure Warning System (LDWS) and Forward Collision Warning System (FCWS) directly into their firmware, leveraging their camera input for analysis. Furthermore, recorders are transitioning to capture not just video but also rich contextual data from the vehicle’s Controller Area Network (CAN bus), providing forensic details like speed, acceleration, brake usage, and steering angle at the moment of an incident. This comprehensive data capture is vital for reconstructing complex accident scenarios and is positioning the automotive recorder as a core component of the future intelligent vehicle infrastructure, moving far beyond its initial role as a simple surveillance camera.

Regional variations in market maturity, regulatory environment, and traffic safety awareness significantly influence the adoption and segmentation of automotive recorders globally. Asia Pacific (APAC) holds the largest market share, spearheaded by mandatory or high voluntary adoption rates in developed economies such as South Korea, where dashcam usage (often referred to as 'black boxes') is nearly universal, strongly encouraged by insurance companies and a culture of proving fault in densely populated urban areas. China and Japan also contribute substantially, driven by large vehicle ownership bases and domestic manufacturing prowess, often setting global trends in connectivity and miniaturization.

North America, encompassing the U.S. and Canada, is characterized by strong demand from the commercial fleet sector, logistics, and trucking industries, which utilize recorders for safety compliance, insurance mitigation, and liability defense. While consumer adoption is not as saturated as in parts of APAC, it is accelerating rapidly, particularly in states with high incidences of uninsured drivers or high insurance fraud rates. The focus here is on robust systems that offer integrated telematics and cloud-based fleet management solutions, with a growing trend towards professional installation and multi-channel coverage to protect against sideswipes and cabin incidents.

Europe represents a highly fragmented yet rapidly expanding market. Regulation plays a significant role, with varying legality concerning recording and data usage across countries (e.g., stricter privacy rules in Germany vs. high adoption in Russia and the UK). The market is being fueled by legislative efforts to mandate the use of event data recorders (EDRs) in new vehicles, which indirectly benefits the consumer aftermarket through increased public safety awareness. European consumers prioritize high build quality, discreet integration, and strict adherence to data protection standards (GDPR). Latin America and MEA are emerging markets, currently characterized by high demand driven by vehicle theft rates and concerns over road security, favoring essential, reliable, high-definition devices at competitive price points.

The Automotive Recorder Market is projected to exhibit a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033, driven by increasing regulatory support and higher consumer adoption of connected devices.

AI significantly enhances recorder functionality by enabling real-time Driver Monitoring Systems (DMS) for fatigue detection, improving object recognition accuracy for incident analysis, and optimizing storage use through intelligent event tagging.

The Multi-Channel recording segment (including front, rear, and cabin views) is experiencing the highest adoption growth, particularly in the commercial fleet and ride-sharing sectors due to the critical need for 360-degree liability coverage and personnel monitoring.

The primary restraints in the European market involve complex data privacy regulations, such as GDPR, which necessitate careful anonymization and storage practices, alongside varied national laws regarding the public and private use of recorded footage.

While OEM integration is growing rapidly, it is unlikely to entirely replace the aftermarket. Aftermarket recorders will continue to serve vehicles outside warranty, offer specialized feature sets (e.g., extreme high resolution or advanced battery management), and provide cost-effective solutions for fleet upgrades and specific consumer needs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.