ID : MRU_ 433009 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

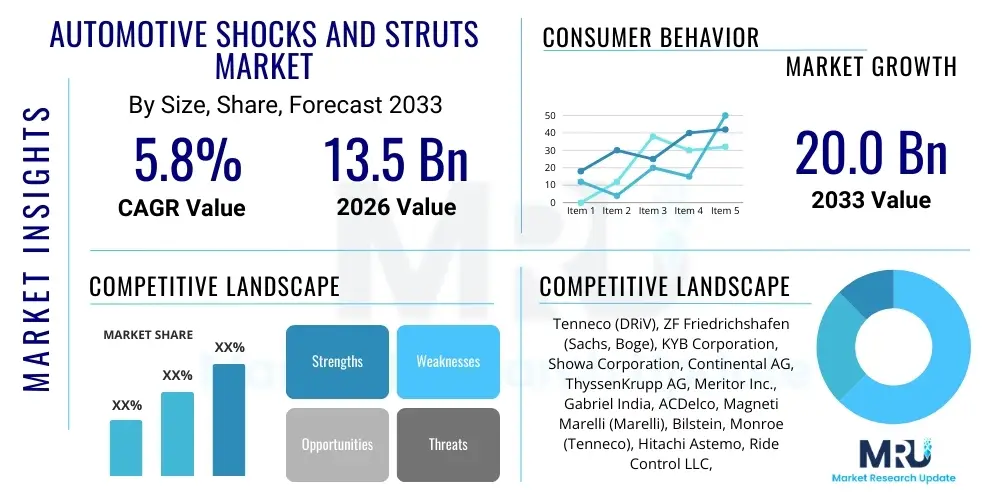

The Automotive Shocks and Struts Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 13.5 Billion in 2026 and is projected to reach USD 20.0 Billion by the end of the forecast period in 2033.

The Automotive Shocks and Struts Market encompasses the manufacturing, distribution, and sale of critical suspension components designed to dampen vehicle body movement, enhance ride comfort, and maintain tire contact with the road surface. These components, primarily categorized as hydraulic or pneumatic shocks and load-bearing struts (McPherson style), are fundamental to vehicle stability, handling, and safety across passenger vehicles, commercial trucks, and off-road applications. Product advancements are increasingly focused on integrating electronic controls, leading to the proliferation of adaptive and semi-active suspension systems that adjust damping characteristics in real-time based on road conditions and driver input, thereby moving beyond conventional passive mechanical systems. The core benefit of these components is the critical management of kinetic energy generated by road irregularities, ensuring optimal braking distance and steering response.

Major applications of shocks and struts span the entire spectrum of the automotive industry, divided broadly into Original Equipment Manufacturer (OEM) installation during vehicle production and the vast aftermarket for replacement and performance upgrades. The demanding schedules of modern logistics drive significant demand for heavy-duty shocks tailored for commercial vehicles, emphasizing durability and sustained performance under high load conditions. Simultaneously, the consumer segment seeks enhanced driving dynamics, fueling the adoption of high-performance monotube shocks and specialized air springs in luxury and sports vehicles. The reliability and lifespan of these parts are paramount, often determining vehicle safety ratings and overall customer satisfaction, making material science (such as advanced polymers and high-strength alloys) a key focus area for research and development.

Key driving factors accelerating market expansion include stringent global safety regulations mandated by governments to reduce road accidents, which necessitate superior vehicle control systems. Furthermore, the average age of vehicles in operation (VIO) is steadily increasing across developed regions, leading to a robust and persistent demand within the replacement aftermarket segment. The global transition toward electric vehicles (EVs) also introduces new design requirements, as EVs possess heavier battery packs, requiring specially calibrated shocks and struts capable of handling increased weight while preserving energy efficiency and maintaining dynamic stability, thereby serving as a significant technological impetus for market growth.

The Automotive Shocks and Struts Market is characterized by intense technological evolution, shifting from traditional hydraulic components to sophisticated electronic damping systems. Key business trends indicate a strong focus on lightweighting materials, particularly in components designed for electric vehicles, where minimizing mass directly translates to extended range. Mergers and acquisitions remain pivotal, allowing key players to consolidate market share, integrate niche technologies (like magnetic ride control), and optimize global supply chains. The aftermarket continues to be a resilient revenue stream, supported by consumer education regarding the necessity of timely suspension replacement for safety and comfort, often leveraging digital platforms for product sales and technical support. OEM relationships are becoming more collaborative, focusing on co-developing next-generation suspension architectures that support autonomous driving capabilities and connected car environments.

Regionally, the Asia Pacific (APAC) stands out as the primary growth engine, fueled by burgeoning automotive production in China and India, coupled with rapid urbanization that demands both new passenger cars and expanded commercial fleet operations. Europe demonstrates a high adoption rate of advanced electronic suspension technologies due to stringent regulatory frameworks favoring vehicle safety and performance standards, alongside a mature replacement market. North America maintains strong demand driven by the high prevalence of light trucks and SUVs, vehicles that often require heavy-duty or specialized load-leveling shock systems, further bolstered by significant infrastructure for performance modification and customization. Manufacturers are strategically positioning production facilities closer to these key consumption centers to mitigate geopolitical risks and shorten lead times.

Segment trends underscore the rising prominence of the semi-active and active suspension sub-segments. While conventional passive shocks retain market volume, the value segment is rapidly moving toward integrated systems that use sensors and Electronic Control Units (ECUs) to dynamically alter damping rates. By vehicle type, the SUV and light truck segments are experiencing the fastest growth, largely due to consumer preference shifting toward larger, multi-purpose vehicles globally. The electrification trend is forcing segment bifurcation, creating a specialized market for EV-specific shocks and struts that feature unique tuning and enhanced durability to manage the high static loads imposed by battery placement, ensuring thermal stability and improved battery protection against road impacts.

Analysis of common user queries related to the integration of Artificial Intelligence (AI) in the Automotive Shocks and Struts Market reveals dominant themes centered on predictive maintenance, optimization of active suspension systems, and the role of AI in autonomous vehicle stability. Users frequently inquire about how AI algorithms can anticipate component failure before it occurs, drastically reducing downtime and maintenance costs. There is significant interest in 'smart suspension' systems where AI processes real-time sensor data (from accelerometers, LiDAR, cameras) to instantly adjust damping forces, offering superior ride quality and enhanced emergency handling, far surpassing pre-programmed electronic systems. Furthermore, a major concern is how AI-driven suspension tuning will compensate for erratic movements or sensory inputs in Level 4/5 autonomous vehicles, ensuring passenger comfort and system redundancy. The consensus expectation is that AI will transform these components from passive mechanical parts into complex, data-driven safety systems.

The Automotive Shocks and Struts market dynamics are heavily influenced by the interplay of safety mandates, technological innovation in damping solutions, and macroeconomic factors governing vehicle production and maintenance cycles. Key drivers include the mandatory implementation of advanced safety features globally, pushing OEMs toward incorporating active and semi-active suspension systems to meet higher dynamic performance standards. Opportunities are abundant in the high-growth aftermarket segment, particularly in emerging economies where road infrastructure quality often mandates frequent component replacement, coupled with the specialized market for high-payload commercial vehicle shocks. Restraints largely involve the high initial cost associated with advanced electronic suspension technologies, making them prohibitive for entry-level vehicle segments, alongside the volatility in raw material prices, specifically steel and aluminum alloys, which affects manufacturing profitability.

Impact forces acting on the industry are predominantly driven by Porter's Five Forces analysis, demonstrating high buyer bargaining power due to the standardized nature of conventional products and intense competition among suppliers, particularly in the aftermarket. However, the bargaining power of suppliers is moderate, fluctuating based on specialized input materials required for high-end electronic components (e.g., specialized hydraulic fluids, complex sensor arrays). The threat of new entrants remains low due to high capital investment requirements, stringent quality certifications, and the necessity of establishing deep, trust-based relationships with major global OEMs. Substitutes, while limited, include air suspension systems or complex kinetic suspension concepts, which pose a threat primarily at the high-end luxury vehicle tier, prompting conventional shock manufacturers to diversify their offerings.

Specific market drivers focus on the global fleet electrification transition, which requires re-engineered, heavier-duty suspension components to manage significant battery mass. Restraints include the complexity of servicing and diagnosing faults in advanced electronic damping systems, demanding specialized training and diagnostic tools, which slows adoption in independent repair shops. Opportunities are found in leveraging Big Data and IoT sensors integrated within suspension systems to offer value-added services such as performance diagnostics and preventative maintenance alerts. The collective impact forces ensure continuous pressure on manufacturers to innovate, reduce cost, and improve product lifecycle, leading to a dynamic market where technological differentiation is crucial for maintaining competitive advantage.

The Automotive Shocks and Struts Market is highly segmented based on product design, technology level, sales channel, vehicle type, and application. This granularity allows manufacturers to tailor products precisely to meet the diverse requirements of OEMs and the aftermarket, ranging from basic twin-tube hydraulic shocks for standard passenger cars to complex, continuously variable damping (CVD) systems for high-performance vehicles. The primary segmentation delineates between passive components (fixed damping) and active/semi-active components (variable damping), reflecting the industry's progression toward smart suspension solutions. Understanding these segments is vital for assessing market potential, as the growth rates and profit margins vary significantly across technology types and distribution routes, particularly between the high-volume replacement market and the high-value OEM sector.

The value chain for the Automotive Shocks and Struts Market begins with the rigorous Upstream Analysis, which focuses on the procurement of critical raw materials such as specialized steel alloys for piston rods and cylinder tubes, high-grade aluminum for strut housings, and synthetic rubber and advanced polymers for seals and bushings. Key upstream activities involve intensive R&D in material science to enhance durability and reduce component weight, especially crucial for EV applications. Supplier consolidation and long-term contracts are common practice to ensure stable supply and quality control, as material failure can lead to catastrophic system breakdown. Component manufacturers rely heavily on precision machining and advanced coating technologies (e.g., chrome plating for piston rods) which are often outsourced to specialized tier-2 suppliers, emphasizing quality assurance at every stage.

Midstream operations involve the core manufacturing and assembly processes, which are highly automated and capital-intensive. This stage includes precision welding, fluid filling (hydraulic oil or nitrogen gas), and the integration of complex electronic sensors and solenoid valves for active systems. The process mandates strict quality control checks, including dynamometer testing and endurance simulations, often customized to meet specific OEM vehicle specifications. The manufacturing location is strategically important, with many major players establishing production hubs in low-cost regions (APAC) while maintaining R&D and high-tech component manufacturing in Europe and North America, necessitating complex global logistics and intellectual property management.

Downstream analysis centers on the Distribution Channel, which is distinctly bifurcated between the OEM channel and the Aftermarket channel. The OEM channel involves direct supply to vehicle assembly plants globally, characterized by large, scheduled volumes and stringent quality audits. The aftermarket relies on a complex network: Direct distribution to Original Equipment Suppliers (OES) parts dealers, and indirect distribution through independent wholesale distributors, jobbers, and local repair workshops. E-commerce platforms are rapidly gaining importance in the aftermarket, offering direct-to-consumer sales and increasing price transparency. Effective management of the downstream logistics, including inventory management and expedited shipping, is crucial for capturing the high-volume, quick-replacement needs characteristic of the global automotive maintenance cycle.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 13.5 Billion |

| Market Forecast in 2033 | USD 20.0 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tenneco (DRiV), ZF Friedrichshafen (Sachs, Boge), KYB Corporation, Showa Corporation, Continental AG, ThyssenKrupp AG, Meritor Inc., Gabriel India, ACDelco, Magneti Marelli (Marelli), Bilstein, Monroe (Tenneco), Hitachi Astemo, Ride Control LLC, Endurance Technologies, Visteon Corporation, Mando Corporation, WABCO Holdings, Sogefi SpA, Zhongshan Kama Shock Absorber. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The primary customer base for automotive shocks and struts is broadly segmented into two massive categories: Original Equipment Manufacturers (OEMs) and the end-user/replacement market. OEMs, including global giants like Toyota, Volkswagen, General Motors, and Tesla, constitute the highest volume consumer, demanding shocks and struts that meet precise, bespoke engineering specifications for every new vehicle platform. These buyers require consistent supply, zero-defect quality, and collaborative R&D capabilities to integrate components seamlessly with complex vehicle dynamics control systems (like ESP and traction control). Customer relationships with OEMs are typically long-term, high-stakes contracts based on proven reliability and cost-effectiveness over the vehicle’s production lifecycle, emphasizing supplier selection and certification based on rigorous quality assurance protocols.

The second major group comprises the aftermarket consumers, who are diverse and segmented by vehicle age, driving habit, and geography. This includes independent garages, specialized performance tuning shops, fleet operators (trucking and logistics companies), and individual vehicle owners purchasing parts through retail chains or online platforms. Fleet operators, especially those managing heavy commercial vehicles (HCVs) and buses, are highly sensitive to product durability and total cost of ownership (TCO), making them significant buyers of robust, heavy-duty shock systems designed for maximum mileage between replacements. The potential for repeat business and brand loyalty is high in the aftermarket, driven by perceived quality and the availability of performance-enhancing or heavy-duty alternatives to standard OEM parts.

Furthermore, niche potential customers include military and defense vehicle manufacturers, requiring highly specialized, extreme-duty suspension capable of operating in harsh environments, and the fast-growing segment of specialty Electric Vehicle (EV) startups. These emerging EV manufacturers often seek innovative, lightweight suspension solutions that maximize battery range and utilize advanced active damping technology to manage the instantaneous torque delivery and low center of gravity characteristic of electric powertrains. Targeting these high-technology, low-volume segments requires different sales strategies focused on technical consultancy and co-development rather than purely volume-based pricing, signaling a market shift toward specialized B2B engagement within the engineering sphere.

The technological evolution in the automotive shocks and struts market is defined by a shift from purely mechanical damping toward smart, electronically controlled suspension systems that utilize sophisticated sensor fusion and control algorithms. A major technological advancement is the widespread adoption of semi-active suspension systems, such as Continuously Variable Damping (CVD) and Magneto-Rheological (MR) fluids. CVD systems use electronically controlled valves to adjust damping force settings almost instantaneously, providing a dynamic balance between ride comfort and handling stability. MR technology, used by companies like Bilstein and Delphi, employs fluid whose viscosity can be rapidly altered by an applied electromagnetic field, offering superior response times essential for high-performance and safety-critical maneuvers, driving up the value proposition of these advanced components.

Another crucial technological frontier is the integration of air suspension systems, moving beyond traditional applications in luxury vehicles and heavy commercial transport to mainstream SUVs and performance crossovers. Modern air suspensions often integrate pneumatic springs with adaptive shocks and struts, allowing for adjustable ride height, automatic load leveling, and variable spring stiffness. This integration necessitates robust sensor technologies and reliable communication protocols (often CAN bus) to manage the complex interaction between the air compressor unit, the electronic control unit (ECU), and the damping mechanisms. Furthermore, the material science field is critical, focusing on developing lighter components using advanced composite materials and high-strength, thin-walled steel to reduce unsprung mass, which is vital for improving overall vehicle handling and maximizing fuel efficiency or EV range.

The future technology landscape is heavily influenced by the rise of electric vehicles and autonomous driving. EV suspension requirements are driving innovation in components that manage high static weight (due to batteries) while also minimizing power consumption. This has spurred interest in kinetic energy recovery systems built into shocks, effectively turning the damper into a generator to reclaim energy lost during suspension movement. For autonomous vehicles, suspension components are evolving into active safety systems, where highly responsive electronic shocks are integrated with vehicle stability software to manage sudden evasive maneuvers and maintain critical stability during sensor processing latency or system handover, ensuring passenger safety and confidence in self-driving technology.

Passive systems use fixed hydraulic or gas damping based on vehicle design. Semi-active systems electronically adjust the damping rate (stiffness/softness) in real-time using sensors and ECUs. Active systems go a step further, dynamically adjusting both the damping rate and the vehicle's height/stance, often using external power to force wheel movement independently of road input for superior control.

EVs possess significantly higher curb weights due to large battery packs, requiring shocks and struts with enhanced load-bearing capacity and durability. Furthermore, suspension tuning must minimize vibration transmission to the battery enclosure and often integrates energy recovery mechanisms to maximize vehicle range by recuperating kinetic energy lost during wheel movement.

While the OEM segment drives revenue based on new vehicle production volumes, the Aftermarket segment is the primary driver of consistent volume growth, particularly in developing economies. As the global average age of vehicles in operation increases, demand for routine replacement of worn-out passive shocks and struts ensures stable, high-volume sales through distribution networks.

Key trends include the increased use of high-strength, lightweight aluminum alloys to reduce unsprung mass, improving vehicle dynamics and fuel efficiency. Additionally, advanced elastomer compounds are being developed for bushings and seals to enhance durability and reduce friction, crucial for the reliable operation and longevity of complex electronic damping units.

AI is pivotal for predictive maintenance, analyzing sensor data to estimate remaining shock lifespan accurately. Critically, AI algorithms are used in advanced active suspension to process complex road and vehicle dynamic data in real-time, enabling instantaneous, optimal damping adjustments that enhance vehicle stability for both human-driven and autonomous operations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.