ID : MRU_ 432997 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

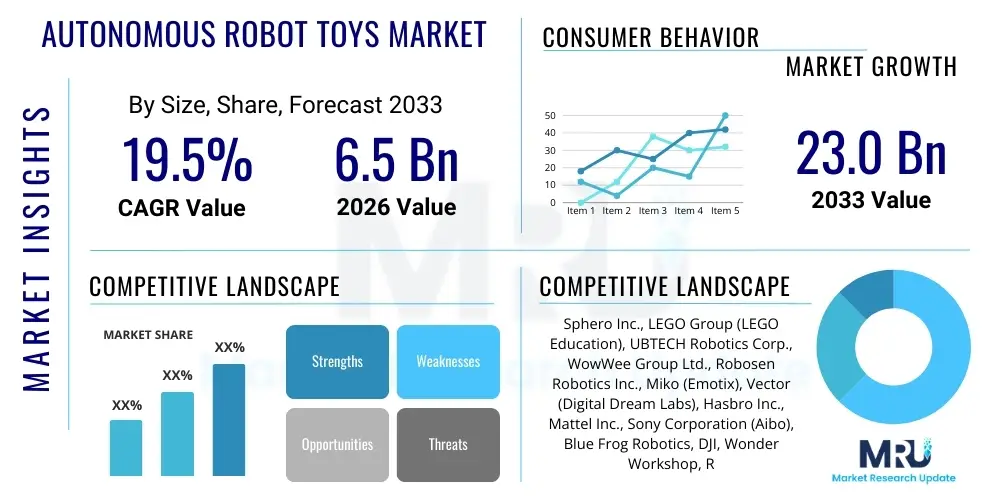

The Autonomous Robot Toys Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.5% between 2026 and 2033. The market is estimated at USD 6.5 billion in 2026 and is projected to reach USD 23.0 billion by the end of the forecast period in 2033.

The Autonomous Robot Toys Market encompasses sophisticated consumer products equipped with advanced sensor technology, artificial intelligence (AI), and machine learning capabilities, enabling them to perceive their environment, make decisions, and interact without constant human intervention. These toys move beyond simple remote control functions, offering dynamic and evolving play experiences. The core product description involves intricate hardware integration, combining microprocessors, inertial measurement units (IMUs), advanced computer vision systems, and proprietary algorithms designed for features like pathfinding, voice recognition, emotional response simulation, and behavioral adaptation. These characteristics differentiate autonomous robots from traditional electronic toys, positioning them as complex, intelligent systems that learn over time, thereby increasing their perceived value and longevity in the consumer electronics sector.

Major applications for autonomous robot toys span a broad spectrum, primarily divided between entertainment, education (STEM learning), and personal companionship. In the educational context, these robots serve as interactive tools, teaching fundamental concepts of coding, robotics, and engineering in a tangible and engaging manner, appealing heavily to parents and educational institutions focused on future-proofing curricula. For entertainment, they offer complex gaming scenarios, personalized interactions, and sophisticated display performances, often integrated with smart home ecosystems or digital platforms. The market benefits significantly from the confluence of rapid technological deflation, making high-fidelity sensor components more accessible, and the increasing societal acceptance of AI-driven consumer products, particularly among younger demographics who are digital natives.

The primary driving factors sustaining the robust growth trajectory include the rising global emphasis on Science, Technology, Engineering, and Mathematics (STEM) education, prompting significant consumer investment in educational technology. Furthermore, continuous innovation in battery technology, miniaturization of components, and the integration of highly responsive AI algorithms are enhancing the realism and capabilities of these toys, broadening their appeal to adult collectors and hobbyists. The ongoing improvement in connectivity standards, such as Wi-Fi 6 and 5G, also facilitates seamless over-the-air updates, enabling manufacturers to introduce new features post-purchase, which maintains product freshness and user engagement throughout the product lifecycle.

The Autonomous Robot Toys Market is characterized by intense technological competition and a shift towards educational applications leveraging deep learning models. Key business trends indicate a strong move toward subscription models for content and software updates, ensuring recurring revenue streams for manufacturers beyond the initial hardware purchase. Furthermore, strategic partnerships between technology developers and established toy manufacturers are crucial for successful market penetration, allowing smaller, innovative AI firms access to extensive global distribution networks. Regional trends reveal North America and Europe as dominant markets due to high disposable incomes and robust early adoption rates of sophisticated consumer electronics, while the Asia Pacific region is demonstrating the highest growth potential, fueled by increasing investment in STEM education across economies like China, Japan, and South Korea, coupled with a large, technologically-savvy consumer base eagerly adopting innovative products designed for educational outcomes. This geographic dynamism necessitates localized content development and regional pricing strategies tailored to specific market maturities and consumer spending habits within distinct Asian territories.

Segment trends highlight the dominance of the educational segment, particularly those robots designed for teaching coding and basic robotics principles to elementary and middle school students. Within the technology segment, AI & Machine Learning is the fastest-growing category, as consumers prioritize toys that offer genuine adaptive behavior and personalized interaction capabilities over pre-programmed movements. The distribution channel landscape is rapidly evolving, with online retail channels capturing an increasing market share due to the ability to provide detailed product demonstrations, consumer reviews, and direct-to-consumer (DTC) sales advantages, bypassing traditional brick-and-mortar limitations inherent to specialized, high-cost consumer electronics. This digital shift demands sophisticated e-commerce platforms and robust digital marketing strategies focused on showcasing the complex functionalities and long-term educational value proposition of the products.

In terms of competitive positioning, the market remains fragmented, yet the barrier to entry is high due to the required expertise in robotics, AI development, and safety certification processes. Companies that successfully integrate robust data privacy protocols into their products are gaining a significant competitive edge, addressing growing parental concerns over connected devices. The prevailing industry movement centers on developing "companion robots" that utilize advanced natural language processing (NLP) and emotional recognition algorithms to simulate genuine companionship, expanding the market beyond traditional play patterns and into therapeutic or assistance roles. The convergence of entertainment and educational technology (edutainment) is the central theme driving product innovation and market acceptance across all major geographic regions, ensuring the sustained commercial viability of this niche sector within the broader robotics industry.

Users frequently inquire about the safety implications, learning capabilities, and ethical considerations associated with integrating advanced AI, specifically deep learning and neural networks, into consumer toy products. Common questions center on how these robots learn, whether they can be exploited for data collection, the accuracy of their emotional recognition features, and the long-term educational efficacy versus traditional learning methods. There is significant user interest in understanding the distinction between simple scripted responses and true machine learning adaptation in the context of personalized play experiences. Furthermore, consumers often seek clarity on the extent to which manufacturers can update and improve the robot's intelligence post-purchase, ensuring the longevity and continued relevance of the high-cost investment. The key themes revolve around establishing trust, verifying educational claims through demonstrable long-term behavioral changes, and ensuring compliance with stringent child data privacy regulations like COPPA and GDPR. The underlying user expectation is that AI should provide demonstrable, superior interactive value compared to non-AI counterparts while maintaining absolute security.

The market dynamics of Autonomous Robot Toys are heavily influenced by a delicate balance between rapid technological advancements and inherent consumer skepticism regarding cost and privacy. Key drivers, such as the global focus on digital literacy and STEM education, are creating robust underlying demand, positioning these products as essential tools for future workforce preparation rather than mere luxury items. This educational imperative is further strengthened by technological enablers, including significant improvements in chip processing power and sensor miniaturization, which collectively reduce manufacturing costs and increase functional complexity. The market benefits from substantial venture capital investment flowing into the consumer robotics sector, accelerating the product development cycles and enabling rapid introduction of next-generation features, thereby maintaining a high pace of innovation and consumer interest in the intelligent toy category.

However, significant restraints temper this growth, primarily the high initial purchase price of advanced autonomous robots, which places them outside the budget range of many mainstream consumers, limiting mass-market penetration. Concerns surrounding data privacy and security are paramount; parents are increasingly wary of devices that collect spatial data, voice recordings, or behavioral patterns, especially those targeting young children, necessitating complex and costly compliance strategies for manufacturers. Furthermore, technical limitations, particularly restricted battery life and the need for frequent charging, interrupt the continuous play experience, impacting user satisfaction and product adoption rates in certain consumer segments. Overcoming these restraints requires manufacturers to achieve economies of scale rapidly and to implement verifiable, transparent data governance models.

Opportunities for market expansion are vast, centering on the integration of autonomous robot toys with the burgeoning smart home ecosystem, allowing robots to function as interactive extensions of IoT devices, performing tasks beyond entertainment. The growing acceptance of companion robots among older adults and individuals with special needs opens new B2B and therapeutic markets, diversifying revenue streams away from purely consumer retail. Impact forces, including competitive pricing pressure driven by Asian manufacturers and the shifting landscape of intellectual property rights protection for advanced algorithms, constantly reshape market structure. The lifecycle of these products is intensely accelerated by technological churn, requiring companies to commit substantial ongoing resources to software development and feature refreshes to prevent product obsolescence within two to three years of launch, demanding strategic foresight regarding component sourcing and software architecture scalability.

The Autonomous Robot Toys Market is fundamentally segmented based on the core technological capabilities, the intended application/use case, the primary target end-user demographic, and the dominant distribution channel through which they are sold. Analyzing these segments provides crucial insights into targeted product development and marketing strategies. The application segmentation, spanning educational, entertainment, and hobbyist/collector categories, reveals distinct consumer motivations, ranging from parental investment in skills development to adult demand for highly detailed, sophisticated display models. Technology-based segmentation (AI/ML, Computer Vision, Sensor Fusion) dictates pricing tiers and functional sophistication, with AI/ML typically commanding the highest premium due to advanced behavioral capabilities. This segmentation structure is pivotal for strategic forecasting, helping stakeholders allocate resources effectively across different product lines and geographic areas based on localized demand patterns.

The value chain for autonomous robot toys is intricate and starts with highly specialized upstream activities, primarily involving the sourcing of advanced micro-components such as application-specific integrated circuits (ASICs), custom microprocessors, specialized sensor arrays (e.g., high-resolution cameras, depth sensors), and sophisticated battery modules. Core value addition at the upstream level lies in intellectual property development, particularly proprietary AI algorithms and sophisticated operating system software necessary for autonomous function. Successful integration requires deep expertise in materials science, component miniaturization, and chip manufacturing, which often involves strategic partnerships with leading semiconductor and sensor technology companies based predominantly in Asia Pacific regions, forming the technological bedrock upon which the final product is built.

The midstream phase focuses on design, assembly, and quality assurance. This stage is critical for integrating complex software with delicate hardware components, ensuring seamless performance and compliance with stringent international safety and environmental regulations (e.g., CE, FCC, RoHS). Manufacturing often utilizes highly automated assembly lines to maintain precision and manage costs. Downstream activities involve market penetration, distribution, and post-sales support, where brand perception and consumer education become paramount. Distribution channels are bifurcated into direct sales (DTC via specialized e-commerce platforms) and indirect sales through traditional retail partners and specialized educational distributors, each requiring tailored logistics and inventory management strategies based on the product's price point and technological complexity, influencing the final margin structure.

The direct channel offers manufacturers greater control over branding and pricing, enabling immediate feedback loops for software refinement, which is crucial for AI-driven products. However, the indirect channel, particularly through global retailers, offers necessary scale and geographic reach. A robust service component, including continuous over-the-air software updates and responsive technical support, is essential in the downstream phase to manage the consumer experience, especially as the product relies heavily on evolving software functionality. Effective value chain management focuses on optimizing inventory carrying costs for high-value components and establishing geographically diverse manufacturing footprints to mitigate geopolitical supply chain risks, ensuring resilience against disruptive global events.

Potential customers for autonomous robot toys are highly diverse, spanning various age groups and motivational drivers, fundamentally segmented into individual end-users (children, teenagers, and adult hobbyists) and institutional buyers (educators and therapy providers). The largest and most volatile segment comprises parents seeking educational tools for children aged six to twelve, viewing these robots as a necessary investment to cultivate essential 21st-century skills such as coding, logical reasoning, and complex problem-solving. This segment is characterized by high spending power and an acute focus on verifiable educational outcomes and long-term utility, making them sensitive to third-party academic endorsements and reputable safety certifications, which are crucial conversion factors in this psychologically driven purchase decision.

A rapidly growing customer base includes adult hobbyists and collectors, particularly those interested in sophisticated robotics, programming, and pop culture franchises, who demand high-fidelity design, advanced technical specifications, and limited-edition releases. These buyers prioritize complexity, customization options, and the sheer technological novelty of the product, often engaging in strong community platforms where they share modifications and custom code, driving demand for developer-friendly hardware kits. The institutional segment, encompassing schools, universities, and specialized therapy centers, acts as a B2B buyer, purchasing in bulk for curriculum implementation or therapeutic interventions, prioritizing robust design, scalability of learning platforms, and comprehensive technical support infrastructure over individual aesthetic appeal.

Furthermore, the emerging market for companion robots targets older adults facing social isolation or individuals requiring cognitive engagement aids. While currently niche, this segment represents a significant future revenue opportunity, driving product development toward advanced emotional intelligence capabilities, simple user interfaces, and robust privacy features. Manufacturers must tailor their messaging and distribution strategies to address the distinct needs of each buyer group: educational efficacy for parents, technical sophistication for hobbyists, and institutional reliability for educators, ensuring that the marketing mix effectively communicates the unique value proposition relevant to the target demographic's specific underlying motivation and purchasing criteria.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 billion |

| Market Forecast in 2033 | USD 23.0 billion |

| Growth Rate | 19.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sphero Inc., LEGO Group (LEGO Education), UBTECH Robotics Corp., WowWee Group Ltd., Robosen Robotics Inc., Miko (Emotix), Vector (Digital Dream Labs), Hasbro Inc., Mattel Inc., Sony Corporation (Aibo), Blue Frog Robotics, DJI, Wonder Workshop, Rapiro (Conyac), Fable (Shape Robotics) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological core of the autonomous robot toys market resides in the seamless fusion of hardware miniaturization and sophisticated software intelligence, marking a departure from traditional electro-mechanical toys. Central to this landscape is the widespread adoption of customized System-on-Chip (SoC) solutions that integrate high-performance processing units capable of executing complex AI tasks locally (edge computing), minimizing latency and reliance on continuous cloud connectivity. These chips power real-time sensor data processing from arrays of inputs, including gyroscopes, accelerometers, ultrasonic sensors, and time-of-flight (ToF) cameras, which together form a comprehensive spatial awareness system, enabling advanced obstacle avoidance and precise localization within dynamic environments without external mapping assistance. Furthermore, advanced motor control systems utilizing high-resolution encoders are essential for achieving the smooth, fluid, and anthropomorphic movements necessary for realistic interaction and high-quality play experiences, driving the perception of high functional realism.

A secondary, yet equally critical, technological pillar is the advancement in deep learning and specialized AI frameworks tailored for consumer robotics. This includes the implementation of reinforcement learning techniques, allowing the robots to genuinely evolve their behavior through interaction and experience, moving beyond mere programmed responses. Manufacturers are heavily investing in Natural Language Understanding (NLU) technologies to facilitate more intuitive and contextually relevant verbal interactions, moving past simple keyword recognition to interpret nuanced language and intent. The necessity for these robots to be updated remotely requires robust, secure over-the-air (OTA) update frameworks, leveraging cryptographic security protocols to ensure the integrity of the downloaded software and protect against unauthorized firmware modification, addressing critical security vulnerabilities that plague connected consumer devices.

The peripheral technology landscape includes significant developments in flexible and modular component design, facilitating repairability and user customization, particularly important for the educational and hobbyist segments. Energy efficiency and power management systems are undergoing continuous refinement, utilizing advanced lithium polymer and solid-state battery chemistries coupled with intelligent power throttling algorithms to extend operational runtime, directly addressing one of the primary consumer pain points—limited battery life. The integration of augmented reality (AR) technologies, allowing the physical robot’s interaction to be overlaid with digital content through a companion smart device, is becoming a standard feature, dramatically enhancing the immersive quality of the play experience and blurring the lines between the digital and physical realms, thereby amplifying the perceived value proposition and ensuring sustained technological differentiation in a rapidly crowding market space.

The Autonomous Robot Toys Market is projected to exhibit a high growth trajectory, forecasting a Compound Annual Growth Rate (CAGR) of 19.5% between the years 2026 and 2033, driven largely by increasing demand for STEM educational tools and AI integration.

AI technology, including machine learning and computer vision, allows autonomous robot toys to perform real-time environmental analysis, personalize interactions, adapt their behavior over time, and provide sophisticated, non-repetitive play or learning experiences, significantly enhancing their functional utility and longevity.

Key restraints include the high initial cost of incorporating advanced components (sensors, processors), substantial parental concerns regarding data privacy and security protocols (especially COPPA/GDPR compliance), and ongoing technical challenges related to optimizing battery life for continuous operation.

The Educational Robotics application segment currently commands the largest market share, reflecting the widespread global emphasis among parents and institutions on equipping children with programming and robotics skills essential for future technological literacy and workforce readiness.

The Asia Pacific (APAC) region is expected to demonstrate the highest market growth rate during the forecast period, driven by rapidly increasing government investment in advanced STEM education infrastructure and the large, technologically receptive consumer base in major economies like China and South Korea.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.