ID : MRU_ 431467 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

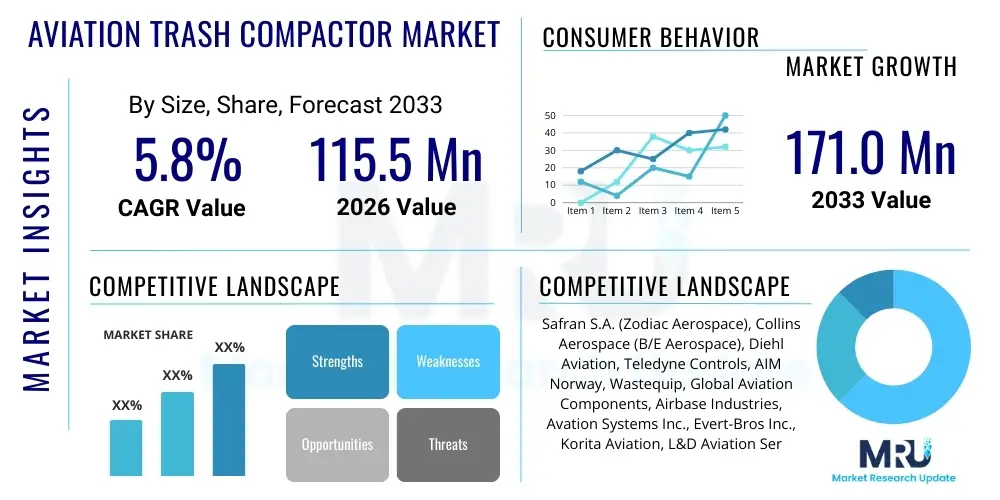

The Aviation Trash Compactor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 115.5 million in 2026 and is projected to reach USD 171.0 million by the end of the forecast period in 2033.

The Aviation Trash Compactor Market encompasses specialized equipment designed for efficient volume reduction of solid waste generated onboard commercial aircraft, private jets, and military transport vehicles. These compactors are essential components of the modern aircraft galley, serving the dual purpose of enhancing cabin hygiene and maximizing the limited storage space available for refuse during long-haul flights. The primary products include manual, semi-automatic, and fully automated electrically powered units, integrated within the galley structure or offered as movable carts.

Major applications of these systems revolve around minimizing the logistical burden of waste management, primarily dealing with catering leftovers, packaging materials, and general cabin refuse. Benefits include reduced waste volume (up to 80%), lower aircraft weight due to fewer required storage bins, and improved turnaround times on the ground. The market is driven by increasing global air passenger traffic, leading to higher volumes of onboard waste, coupled with stringent international regulations emphasizing sustainable waste management practices within the aviation sector.

Furthermore, advancements in materials science and compacting technology are driving innovation towards lighter, more energy-efficient, and quieter trash compactors. These systems contribute directly to operational efficiency and airline profitability by freeing up valuable galley real estate and reducing fuel consumption associated with carrying unnecessary bulk weight. The increasing focus on passenger experience also necessitates swift and discreet waste handling, bolstering the demand for high-capacity, automated compaction solutions.

The Aviation Trash Compactor Market is experiencing robust growth fueled by mandatory requirements for improved waste handling protocols and the expansion of long-haul international routes. Business trends indicate a shift towards fully integrated, intelligent compaction systems that offer real-time monitoring and predictive maintenance capabilities, appealing primarily to major international carriers seeking operational excellence. The competitive landscape is characterized by major aerospace component manufacturers dominating the supply chain, focusing on integrating compactors into comprehensive galley solutions during aircraft retrofit and original equipment manufacturing (OEM) phases.

Regional trends show North America and Europe retaining dominant market shares due to high domestic flight frequencies and the presence of major aircraft manufacturers and large commercial airlines committed to sustainability goals. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate, driven by significant investments in new aircraft procurement, booming middle-class travel, and the establishment of new low-cost carriers (LCCs) prioritizing optimized cabin logistics. Segment trends emphasize the growing adoption of fully automatic, electric-powered compactors over manual options, particularly in wide-body aircraft where waste generation volumes are substantial.

The market faces challenges related to the high cost of certifying new galley equipment and the restricted dimensions within existing aircraft designs. Nonetheless, strategic opportunities lie in developing ultra-lightweight compactors utilizing composite materials and integrating Internet of Things (IoT) capabilities for better inventory and waste tracking. The overarching theme remains efficiency—reducing volume, minimizing weight, and automating the disposal process to enhance overall flight sustainability and cost control.

Common user questions regarding AI's impact on the Aviation Trash Compactor Market often center on how automation can extend beyond simple mechanical compaction. Users inquire about the potential for AI to optimize waste sorting, predict waste generation volumes based on flight manifest and catering load, and enhance the maintenance predictability of the compactor unit itself. Key concerns revolve around the cost justification for implementing smart, AI-driven compactors versus traditional mechanical units, and how AI can be integrated without adding excessive weight or complexity to the already constrained galley infrastructure. The prevailing expectation is that AI will transform compactors from simple mechanical devices into intelligent waste management hubs, enabling proactive waste logistics planning both in the air and on the ground.

The integration of artificial intelligence and machine learning algorithms promises a paradigm shift in how aviation waste is handled, moving from reactive disposal to predictive management. AI systems, coupled with sensors embedded in compactor units, can analyze the composition and density of the compacted waste load. This analysis allows airlines to generate highly accurate reports on non-recyclable versus recyclable materials, which is crucial for meeting evolving international environmental reporting standards and optimizing ground handling services. For instance, an AI-powered compactor could detect an unusual volume of specific materials, flagging potential catering issues or unusual operational anomalies, thereby adding significant value beyond mere volume reduction.

Furthermore, machine learning facilitates predictive maintenance (PdM) for the compaction units. By analyzing operational data—such as motor stress levels, compaction cycle duration, and thermal signatures—AI can anticipate component failures before they occur, allowing maintenance crews to schedule replacements during routine layovers rather than causing unexpected equipment downtime mid-flight. This not only increases the reliability of the galley equipment but also minimizes the operational expenditure associated with emergency repairs or inefficient use of storage space due to malfunctioning compactors. These intelligent systems effectively contribute to a seamless and proactive maintenance environment, critical for minimizing aircraft ground time.

The Aviation Trash Compactor Market is significantly influenced by a blend of powerful drivers, stringent restraints, and substantial opportunities (DRO). A primary driver is the necessity for operational efficiency, where compactors directly translate into weight savings, thus reducing fuel costs and enhancing environmental performance. Simultaneously, strict international regulations from bodies like the International Civil Aviation Organization (ICAO) concerning aircraft waste segregation and disposal mandate the use of specialized equipment. Restraints largely center on the extremely high qualification and certification costs (e.g., FAA, EASA) required for new galley systems, coupled with the inherent challenge of integrating equipment into pre-existing, spatially limited aircraft designs. These forces combine to create an environment where innovation must balance technological advancement with rigorous safety and space constraints.

The immediate impact forces driving demand include the continuous increase in global air travel, especially long-haul routes where waste accumulation is maximal, necessitating robust compaction solutions. Furthermore, airlines are actively seeking solutions that improve passenger perceptions of cleanliness and sustainability, making advanced waste management a competitive differentiator. Conversely, the market’s reliance on the fluctuating cycle of aircraft production and refurbishment acts as an indirect dampening force. When airlines delay new aircraft orders or postpone cabin refurbishments due to economic instability, the demand for new compactor units can temporarily stagnate.

Opportunities for market expansion are concentrated in the development of lightweight composite compactors and the integration of IoT for remote diagnostics and waste volume reporting. These smart solutions attract forward-thinking carriers focused on digitalizing their operations. Moreover, the push towards standardized, modular galley components facilitates easier installation and maintenance across diverse fleets. Overall, the market dynamics are leaning towards sophisticated, high-efficiency compactors that address both the logistical challenges of space and weight, while simultaneously adhering to escalating global environmental compliance mandates.

The Aviation Trash Compactor Market is comprehensively segmented based on key operational and technical characteristics, allowing for targeted analysis of consumer preferences across the global aviation landscape. Primary segmentation criteria include the level of automation (Manual, Semi-Automatic, Fully Automatic), which dictates ease of use and capital expenditure; the volumetric capacity of the unit (Small, Medium, Large), tailored to specific aircraft size and flight duration; the type of aircraft utilizing the equipment (Narrow-body, Wide-body, Regional Jets), directly impacting dimensional constraints; and the final end-user (Commercial Airlines, Private/Business Aviation, Military Transport), reflecting different operational requirements and purchasing power. This structure provides a granular view of market penetration and growth potential across various aviation categories.

The segmentation by automation reveals a clear trend towards fully automatic compactors, especially among flag carriers operating wide-body aircraft, due to the substantial labor savings and enhanced sanitation they provide. However, cost-sensitive regional airlines and smaller private jets often rely on lighter, simpler semi-automatic or manual units where waste volumes are lower. Capacity segmentation is vital for matching the compactor to the flight mission; long-haul flights demand large capacity units to manage several meal services, while short-haul routes require compact, space-saving options.

Aircraft type segmentation is perhaps the most critical determinant, as galley space in narrow-body aircraft (like the Boeing 737 or Airbus A320 families) is severely restricted, favoring slim-line or custom-fit compactors. Wide-body aircraft (Boeing 777/787, Airbus A350/A380) can accommodate multiple, large, high-throughput compactors. The commercial airline segment dominates the end-user market, but the private aviation segment offers high-margin opportunities for bespoke, aesthetically integrated, and low-noise compactor solutions that cater to luxury cabin environments.

The value chain for the Aviation Trash Compactor Market begins with upstream suppliers providing specialized materials and high-precision components. This upstream segment is highly specialized, involving providers of lightweight, aerospace-grade alloys, high-efficiency electric motors, and sophisticated electronic control units necessary for automated systems. Key considerations at this stage include material certifications and strict adherence to weight reduction targets. Manufacturers often rely on long-term supplier partnerships to ensure consistency in component quality and compliance with stringent aviation safety standards (e.g., fire-proof casing materials).

The core manufacturing and assembly phase is characterized by intense design and engineering effort, particularly concerning size optimization and certification compliance. Original Equipment Manufacturers (OEMs) and major Tier 1 suppliers (focused on galley systems) are pivotal in this stage. Downstream activities involve distribution channels that are predominantly direct for large fleet orders (OEM installation or direct retrofit by Maintenance, Repair, and Overhaul – MRO facilities). Indirect channels are less common but include specialized aviation parts distributors catering to smaller MROs or private aviation needs.

The end of the value chain involves maintenance and aftermarket services, which represent a crucial revenue stream. Given the rigorous operational environment, compactors require frequent servicing and part replacements, managed either directly by the aircraft component manufacturers or through approved MRO service providers globally. The trend towards smart, IoT-enabled compactors is enhancing efficiency in this downstream segment, allowing manufacturers to offer proactive service contracts based on real-time usage data, thereby strengthening customer retention and maximizing equipment lifespan.

The primary consumers and end-users of aviation trash compactors are globally recognized commercial airline operators, spanning from large legacy carriers with extensive international fleets to regional and budget airlines. Legacy carriers, such as American Airlines, Lufthansa, Emirates, and Singapore Airlines, represent high-volume buyers, consistently investing in advanced, automated compactors for their wide-body, long-haul aircraft to manage substantial waste generated during transcontinental flights. Low-cost carriers (LCCs) like Ryanair or Southwest, while often prioritizing minimum weight, still represent significant potential, increasingly seeking compact, durable, and easily maintainable semi-automatic units to enhance cabin turnaround efficiency.

A second major segment comprises the burgeoning Private and Business Aviation sector. Buyers in this segment, including fractional ownership providers, charter operators, and ultra-high-net-worth individuals, demand highly customized, quiet, and aesthetically integrated compactors. For them, space saving must be achieved without compromising the luxury interior design or cabin tranquility, leading to demand for bespoke, high-cost solutions often embedded discreetly within cabinetry. This segment prioritizes low noise output and reliability over extreme high-volume throughput.

A third, specialized customer base includes Military and Government Aviation bodies. These customers utilize compactors, primarily in large transport aircraft (e.g., cargo or troop transports) and specialized mission aircraft, where extended flight durations necessitate self-contained waste management. Their purchasing criteria heavily emphasize ruggedness, durability, ease of field maintenance, and compliance with military specifications rather than pure cost optimization or luxury integration. The Maintenance, Repair, and Overhaul (MRO) facilities also serve as crucial indirect buyers, purchasing units and parts during major aircraft retrofit cycles on behalf of the end-user airlines.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 115.5 million |

| Market Forecast in 2033 | USD 171.0 million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Safran S.A. (Zodiac Aerospace), Collins Aerospace (B/E Aerospace), Diehl Aviation, Teledyne Controls, AIM Norway, Wastequip, Global Aviation Components, Airbase Industries, Avation Systems Inc., Evert-Bros Inc., Korita Aviation, L&D Aviation Services, TransDigm Group Incorporated, Turkish Aerospace Industries (TAI), Liebherr-Aerospace. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Aviation Trash Compactor Market is rapidly evolving, driven by the need for superior weight efficiency and enhanced operational intelligence. Traditional compactors relied on heavy hydraulic or robust mechanical linkages, often resulting in high energy consumption and substantial weight. The current technological focus is heavily centered on developing advanced electro-mechanical systems. These modern systems utilize highly efficient electric motors and specialized gear drives to generate sufficient compaction force while minimizing the overall unit weight. This shift is critical as every kilogram saved in galley equipment directly translates to reduced lifetime fuel consumption and lower operational costs for the airline.

A significant technological development is the incorporation of lightweight composite materials and aerospace-grade polymers in the casing and internal structures of compactors. Manufacturers are moving away from heavy stainless steel in non-critical structural components to drastically reduce mass without compromising fire safety regulations or durability requirements. Coupled with this material innovation is the integration of advanced sensor technology, enabling features such as volumetric sensors to measure the remaining compaction capacity and stress sensors to monitor the health of the internal mechanism. This sensor data forms the foundation for the emerging IoT capabilities.

Furthermore, the cutting-edge technology involves sophisticated control systems utilizing miniaturized Programmable Logic Controllers (PLCs) and microprocessors. These controllers manage variable compaction cycles, optimize energy usage based on waste density, and facilitate connectivity for data transmission. Noise reduction technology, including specialized damping mounts and acoustic insulation, is also a critical competitive factor, particularly for compactors placed near premium cabin sections, ensuring minimal disruption to the passenger experience. The convergence of lightweight design, smart electronics, and robust mechanical engineering defines the competitive technology space.

The global Aviation Trash Compactor Market exhibits diverse growth patterns across major geographical regions, influenced by fleet size, regulatory environment, and economic development in the aviation sector. These regional variations dictate procurement strategies and adoption rates for new technologies.

The primary function is to drastically reduce the volume of solid waste generated onboard, often achieving volume reduction ratios of 5:1 or higher. The economic benefit lies in reduced weight, leading to lower fuel consumption, and the freeing up of limited galley storage space, thereby improving operational logistics and cabin efficiency.

Certification requirements from agencies like the FAA and EASA are extremely stringent, requiring extensive testing for fire resistance, structural integrity, and electromagnetic compatibility. This high barrier to entry increases the R&D cost and time for new technologies, favoring established manufacturers with proven certification processes and discouraging rapid technology adoption.

Manual compactors require significant crew effort and are less common. Semi-automatic units use power for compaction but require manual bag insertion and removal. Fully automatic compactors handle the entire cycle, including automated sealing and disposal readiness, providing the highest efficiency and hygiene, often preferred for large, long-haul aircraft.

The Asia Pacific (APAC) region is projected to register the fastest growth rate. This is due to extensive investments in new aircraft procurement, the rapid expansion of domestic and international air travel, and the emergence of new low-cost carriers demanding optimized cabin equipment.

IoT integration enables smart compactors to transmit real-time data on waste volume, compaction cycles, and maintenance needs wirelessly. This data supports predictive maintenance planning for MROs and allows airlines to optimize ground handling logistics and accurately report environmental compliance metrics.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.