ID : MRU_ 431490 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

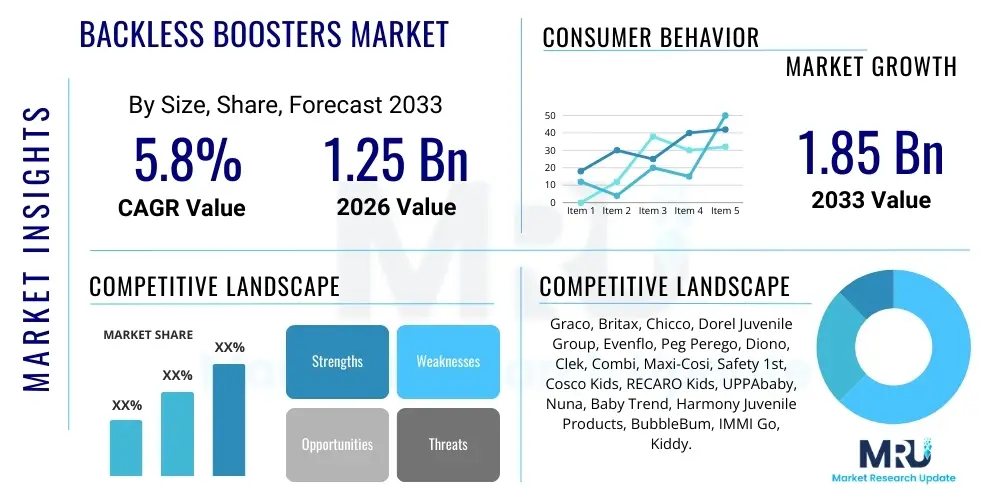

The Backless Boosters Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% (CAGR) between 2026 and 2033. This growth is driven by stringent governmental safety regulations regarding child passenger safety and increasing parental awareness across emerging economies. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 1.85 Billion by the end of the forecast period in 2033, reflecting consistent demand for cost-effective and portable child restraint solutions as children transition out of high-back booster seats.

The Backless Boosters Market encompasses the manufacturing, distribution, and sale of specialized child restraint systems designed for older children who have outgrown conventional car seats but are still too small for standard adult seat belts. These seats elevate the child to ensure the lap belt rests correctly across the strong hip bones and the shoulder belt crosses the center of the chest and shoulder, drastically reducing the risk of injury during a collision. Backless boosters primarily serve children typically ranging from 4 to 12 years old, or those weighing between 40 and 120 pounds, depending on regional safety standards like the U.S. Federal Motor Vehicle Safety Standard (FMVSS) 213 or the European ECE R44 and R129 regulations. The core function is to optimize seat belt fit, providing essential safety without the lateral or head support found in high-back counterparts, making them highly desirable for transport flexibility and ease of installation in secondary vehicles.

Major applications for backless boosters are overwhelmingly concentrated in private passenger vehicles, including sedans, SUVs, and minivans, where families prioritize flexibility and portability for child safety. The utility of backless boosters extends particularly well to carpooling scenarios, ride-sharing services, and vehicles with limited interior space where a full-sized car seat would be cumbersome. The underlying driving factors for market expansion include continuous regulatory updates globally mandating appropriate restraint usage for children up to higher ages or heights, robust public health initiatives emphasizing the importance of correctly fitted restraints, and sustained population growth in demographic segments relevant to the product. Furthermore, the affordability and longevity of use compared to infant or convertible car seats contribute significantly to their market adoption.

Key benefits derived from backless booster utilization involve enhanced crash protection by preventing "submarining" (sliding under the lap belt) and ensuring optimal energy distribution across the child’s body during impact. From a consumer perspective, the primary benefit is convenience: these boosters are lightweight, easy to transfer between cars, simple to clean, and often feature LATCH systems or specific seat belt guides to facilitate proper installation. The market structure is influenced heavily by materials science, focusing on durable, impact-absorbing foams (such as Expanded Polystyrene – EPS) and resilient polymer shells, balanced against consumer demand for slim designs that allow three seats across the back row of a vehicle.

The global Backless Boosters Market is characterized by steady growth underpinned by non-negotiable safety standards and evolving consumer preferences for minimalist, travel-friendly child safety solutions. Business trends indicate a strong focus on material innovation, specifically the use of sustainable and lightweight yet highly durable polymers, aimed at improving product safety ratings while simplifying installation. Regional trends show differential adoption rates: North America and Europe demonstrate high market maturity driven by strict enforcement and widespread public awareness, whereas Asia Pacific exhibits rapid expansion due to increasing disposable incomes, urbanization, and the adoption of Western-style safety protocols. Manufacturers are strategically targeting the mid-range price segment, balancing sophisticated features like integrated cup holders and ergonomic padding with cost efficiency to maximize market penetration.

Segment trends highlight the dominance of the Plastic and Polymer Construction segment due to manufacturing efficiency and superior impact absorption capabilities, although the Fabric and Foam segment, emphasizing portability and comfort, is experiencing steady uptake. In terms of distribution, e-commerce platforms are increasingly gaining prominence, offering consumers detailed product comparisons, user reviews, and accessibility to international brands, thereby challenging traditional brick-and-mortar retail dominance. Furthermore, the market is seeing consolidation among major players who are leveraging intellectual property related to belt-positioning technology and side-impact protection, even in backless models, to differentiate their offerings in a largely standardized product category.

The prevailing market dynamic is defined by the necessity for manufacturers to continually invest in testing and certification processes to meet stringent global standards (e.g., meeting both ECE R129 i-Size requirements for dimensional fit and weight classes, and U.S. regulatory standards). This environment necessitates deep supply chain integration, ensuring the sourcing of high-quality, non-toxic materials compliant with global chemical regulations (such as REACH or CPSIA). Future growth is highly dependent on manufacturers’ ability to effectively market the incremental safety benefits of their products—even the simple backless design—to safety-conscious parents who are often confused by the proliferation of different car seat types available.

Common user questions regarding AI's influence on the Backless Boosters Market revolve primarily around optimizing safety testing protocols, automating quality control in manufacturing, and enhancing personalized consumer recommendations. Users are keen to know if AI can predict material failure points, accelerate the lengthy crash-test simulation process, or if machine learning algorithms are being utilized to analyze real-world accident data to inform design improvements in belt routing and structural integrity. A significant concern also centers on AI-driven supply chain transparency and traceability, ensuring that materials used are genuine and compliant with safety standards. The overarching theme is the expectation that AI should lead to safer, more reliable products while also streamlining the complex regulatory compliance pathways that govern child restraints.

AI is expected to revolutionize the manufacturing and supply chain aspects of the Backless Boosters market rather than directly integrating into the passive product itself. AI-driven simulations, utilizing computational fluid dynamics (CFD) and Finite Element Analysis (FEA), allow design engineers to rapidly iterate on structural designs, optimizing energy absorption profiles without the need for extensive physical prototyping, thereby significantly reducing time-to-market and R&D costs. Furthermore, predictive maintenance algorithms applied to manufacturing equipment ensure minimal downtime, maintaining high output capacity, crucial for meeting stable consumer demand. AI-enabled visual inspection systems on assembly lines are far more effective than human inspectors at identifying subtle material defects or mold inconsistencies in plastic components, guaranteeing that every booster meets critical safety tolerances.

On the consumer front, AI algorithms deployed by retailers and manufacturers are refining targeting and inventory management. By analyzing purchasing behavior, geographic location, vehicle type, and child age data (when provided), AI ensures that specific booster models meeting regional regulations and vehicle compatibility requirements are efficiently stocked and recommended to the right consumers. This personalization, combined with AI-powered chatbot customer service that can instantly verify product registration and recall information, significantly enhances the post-purchase experience and builds brand trust, addressing the complex logistical and compliance concerns often associated with juvenile products.

The Backless Boosters Market is propelled by mandatory child passenger safety laws (Drivers), but faces resistance from potential consumer confusion between high-back and backless models (Restraints). Opportunities arise from developing ultra-slim designs for urban mobility and expanding penetration into untapped emerging markets, while the primary impact force remains the continuous and rigorous evolution of global safety certifications (R129, FMVSS 213). The interplay between regulation and consumer awareness dictates market momentum; stringent enforcement acts as a powerful driver, compelling purchases even as price sensitivity acts as a mitigating restraint. Manufacturers must navigate the delicate balance of offering cost-effective products while simultaneously meeting the highest, often expensive, safety testing requirements.

Key drivers include the transition phase for children aged 6 to 12, who require booster seats until they reach approximately 4 feet 9 inches in height, ensuring a consistently regenerating consumer base. Furthermore, the convenience factor—being easily transferable and stored—makes them essential for secondary vehicles, grandparents’ cars, and childcare providers. However, restraints persist due to increasing regulatory preference in some regions for high-back boosters over backless ones, as high-back models offer superior side-impact protection and better belt positioning, often confusing consumers about when a backless model is truly safe or appropriate. The inherent lack of a LATCH system connection in many basic backless models, leading to potential seat movement when unoccupied, also poses a perceived safety restraint for some highly cautious consumers.

Significant opportunities lie in innovative design focusing on enhanced ergonomics and sustainability. The demand for products made from recycled or bio-based polymers is increasing, aligning with broader consumer trends for environmental responsibility. Expanding market share in densely populated regions of Southeast Asia and Latin America, where rapid motorization is occurring alongside the introduction of foundational child safety legislation, presents substantial long-term growth potential. The impact forces are continually shaped by legislative updates, particularly the shift towards criteria based on height rather than weight (such as the ECE R129 i-Size regulation), compelling manufacturers to redesign products to fit a wider range of stature and age brackets, ensuring the market remains dynamic and responsive to evolving scientific understanding of crash biomechanics.

The Backless Boosters Market segmentation provides a granular view of product diversification and consumer purchasing patterns, primarily categorized by material, distribution channel, and weight capacity. Material segmentation, encompassing plastic, polymers, foam, and fabric, dictates the product’s weight, durability, and cost profile, heavily influencing manufacturing processes. Distribution channel analysis reveals a critical shift toward digital retail, although specialized juvenile product stores maintain importance due to the need for expert advice on installation and compatibility. Weight capacity segmentation addresses specific regulatory requirements across different jurisdictions, ensuring products are marketed appropriately based on local safety standards.

Segmentation by material is crucial, as the performance during an impact depends heavily on the chosen shell construction and energy-absorbing materials. High-density Polyethylene (HDPE) and Polypropylene (PP) polymers dominate, offering an optimal balance between cost-effectiveness and structural integrity. Meanwhile, the growing segment of advanced cushioning materials, such as dense memory foam or specialized EPS variants, caters to the premium market demanding enhanced comfort for extended trips. This dual focus allows manufacturers to capture both budget-conscious consumers (seeking basic compliance) and those prioritizing comfort and perceived safety enhancements.

The distribution landscape reflects evolving consumer behavior. While mass retailers (e.g., Walmart, Target) remain foundational due to volume sales, the e-commerce segment’s rapid growth is driven by its ability to offer extensive product specifications, direct shipping, and easier handling of bulky items. Specialized infant and child product retailers, though smaller in volume, provide crucial educational resources and fitting checks, which are essential for products where correct installation directly impacts safety outcomes. Understanding these segmented needs allows companies to tailor their marketing strategies, focusing on price and convenience through mass retail, and safety credentials and expert advice through specialized channels.

The value chain for the Backless Boosters Market begins with the upstream sourcing of raw materials, primarily specialized plastics (HDPE, PP), high-density foams (EPS, EPP), and non-flammable textile coverings. Upstream activities are characterized by rigorous material quality checks and certifications, ensuring compliance with global chemical and flammability standards, necessitating strong relationships with specialized polymer compounders. Component manufacturing, including the molding of the structural shell and the assembly of belt guides, forms the core operational stage. High precision in molding is paramount, as structural integrity is directly linked to performance in crash tests. This requires significant capital investment in advanced injection molding machinery and tooling.

The midstream involves final assembly, rigorous in-house quality assurance testing, and mandatory external certification by regulatory bodies (e.g., NHTSA, TUV Rheinland). This stage generates substantial value through intellectual property related to design efficiency and safety features, such as patented belt routing mechanisms. Logistics and distribution channels then manage the flow to the downstream market. Direct distribution often targets major mass retailers and large e-commerce hubs, minimizing intermediary costs and maximizing volume sales. Indirect distribution leverages specialized distributors and wholesalers who possess deep regional knowledge, particularly effective in fragmented markets or those requiring tailored customs compliance and local retail relationships.

Downstream activities focus on sales, marketing, and post-sale services. Marketing strategies heavily emphasize safety ratings, ease of use, and compatibility information, often utilizing AEO strategies to answer common parental queries regarding safe installation and transition timing. The ultimate downstream buyers are the end-users—parents and caregivers. The distribution channel choice is strategic: e-commerce offers geographic reach and convenience, capitalizing on detailed digital product listings and user reviews, while physical specialty stores provide vital hands-on demonstrations and installation guidance, crucial for consumers prioritizing personalized safety verification.

The primary potential customers and end-users of backless boosters are parents and legal guardians of children typically aged five to twelve who have outgrown a traditional convertible or high-back booster but still require belt positioning to achieve a safe fit with the vehicle’s three-point seat belt system. This demographic is characterized by high safety consciousness and often seeks economical solutions for their older children who are nearing the transition to adult seating. Secondary customer segments include grandparents, extended family members, and childcare providers who frequently transport children temporarily and require a portable, easily stored, and compliant safety device without the bulk of a full child safety seat. The purchasing decision is highly influenced by regulatory compliance, ease of transferability, and vehicle compatibility, particularly in households with multiple cars.

A significant, growing segment includes individuals utilizing ridesharing services or taxis in urban environments, particularly in jurisdictions where child restraint laws apply universally across commercial transportation. For these customers, the backless booster offers the lightest and most portable option available, easily carried or deployed upon entering the vehicle. Furthermore, institutions such as schools, summer camps, and rental car agencies represent bulk purchasers requiring durable, easy-to-clean booster seats for fleet use, where cost-per-unit and longevity are critical procurement factors. Market messaging must address the core needs of safety compliance, portability, and value, resonating with both individual family buyers and institutional fleet managers.

The profile of the safety-conscious parent remains the most influential customer. These consumers often utilize online resources and consumer safety publications to compare crash test ratings, installation complexity, and user-friendliness. Their purchasing journey is highly researched, driven by authoritative recommendations from bodies like the Insurance Institute for Highway Safety (IIHS) or national safety boards. Therefore, manufacturers must invest heavily in transparent testing data and clear communication regarding the product's limitations and proper use, optimizing their digital content for AEO to capture these highly motivated, research-intensive buyers at the point of inquiry.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 1.85 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Graco, Britax, Chicco, Dorel Juvenile Group, Evenflo, Peg Perego, Diono, Clek, Combi, Maxi-Cosi, Safety 1st, Cosco Kids, RECARO Kids, UPPAbaby, Nuna, Baby Trend, Harmony Juvenile Products, BubbleBum, IMMI Go, Kiddy. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for backless boosters, while seemingly simple, focuses intensely on material science, ergonomic design, and patented belt-positioning mechanisms to maximize safety performance within a minimal form factor. A primary technological focus involves the selection and formulation of lightweight, high-strength polymers (often variations of high-density polyethylene or proprietary blends) capable of absorbing significant crash forces without fragmentation. The geometry of the booster shell, often optimized through Computational Fluid Dynamics (CFD) and Finite Element Analysis (FEA) software, is designed to distribute impact loads evenly across the child's hip bones, ensuring that the structural integrity prevents deformation that could lead to injury. Furthermore, advanced foam technologies, such as injected Expanded Polystyrene (EPS) or Expanded Polypropylene (EPP), are layered within the seat structure to provide localized energy management, cushioning the child from sudden decelerations.

Another crucial technological element is the development of innovative, user-friendly belt-guide systems. Backless boosters rely entirely on the vehicle’s seat belt; thus, the ability of the booster to reliably position both the lap and shoulder belts correctly is critical. Manufacturers employ patented belt clip designs, color-coded guides, and enhanced friction materials on the base to prevent slippage during a collision or during normal use. While LATCH systems are less common in backless models due to their simplicity and portability focus, premium versions often incorporate simplified LATCH attachments (or rigid LATCH connectors) designed primarily to secure the unoccupied booster seat, preventing it from becoming a projectile in a crash, without necessarily enhancing the crash protection provided by the vehicle's belt.

The manufacturing technology itself, particularly precision injection molding, is key to maintaining tight tolerances required for safety certification. Furthermore, the integration of smart textiles that are breathable, stain-resistant, and inherently flame-retardant (meeting strict standards like FMVSS 302) represents a constant area of material innovation. Although backless boosters are passive safety devices, the technological edge lies in optimizing the interaction between the product, the child, and the vehicle seat belt, prioritizing simplicity and error reduction during daily use, which is critical for maximizing real-world safety adherence. Digital integration focuses on QR codes or embedded chips for seamless product registration and immediate recall notification rather than active safety features.

The transition typically occurs when a child outgrows the internal harness of a convertible seat, usually around age four or five, provided they meet the minimum weight (usually 40 lbs) and maturity requirements. However, pediatric safety experts highly recommend using a high-back booster until the child reaches 4 feet 9 inches (approximately 8-12 years old) to ensure optimal seat belt fit and safety, reserving the backless booster primarily for travel or secondary vehicles.

Backless boosters are safe and compliant with federal standards (like FMVSS 213) when used correctly, as their primary function is proper belt positioning. However, high-back boosters generally offer better head, neck, and side-impact protection, particularly if the vehicle lacks sufficient headrests. Backless models are preferred for portability and ease of fit in older or smaller vehicles, but they offer less protection against side intrusion impacts.

The majority of backless booster seats do not strictly require LATCH (Lower Anchors and Tethers for Children) installation for restraining the child, as the child and seat are secured directly by the vehicle’s seat belt. Some premium backless models include LATCH connectors, but these are primarily used to secure the booster when the child is not seated, preventing the seat from becoming a projectile in a collision.

Most backless booster seats have an expiration date ranging from 6 to 10 years from the date of manufacture. This expiration is necessary because materials, particularly plastics and foams, degrade over time due to temperature fluctuations, UV exposure, and wear, potentially compromising the seat's structural integrity and impact absorption capabilities. Always check the manufacturer's label for the specific date.

ECE R129 (i-Size) regulations have introduced stricter criteria, prioritizing height measurement and enhanced side-impact testing, although backless boosters are inherently restricted in their ability to provide superior side protection. R129 specifically influences backless design by setting minimum height requirements (often 125 cm or taller for new models) to ensure correct belt fit and by driving manufacturers to use higher quality, dimensionally stable materials to meet stringent testing protocols.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.