ID : MRU_ 436562 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

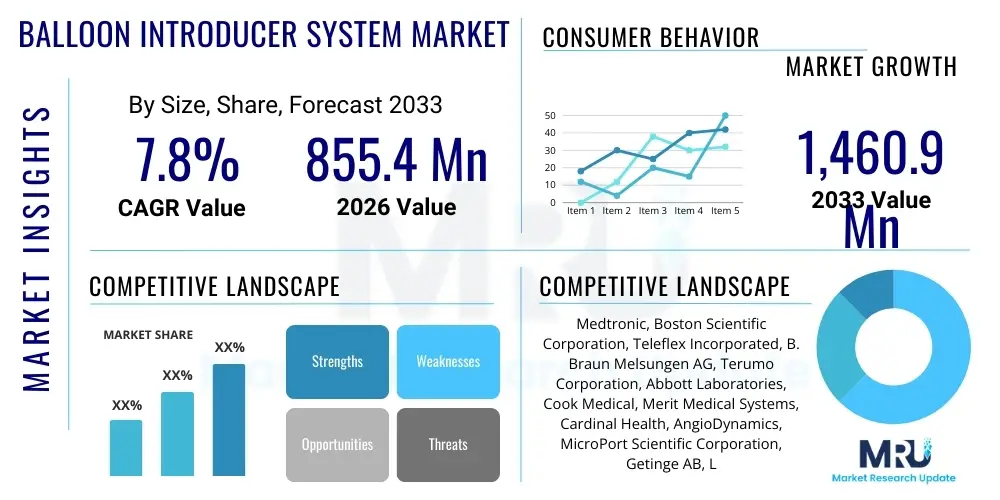

The Balloon Introducer System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 855.4 million in 2026 and is projected to reach USD 1,460.9 million by the end of the forecast period in 2033.

The Balloon Introducer System Market encompasses specialized medical devices designed to facilitate the safe and efficient introduction and guidance of catheters and other interventional instruments into the vasculature, primarily in minimally invasive procedures such as percutaneous coronary interventions (PCI) and peripheral vascular interventions (PVI). These systems typically consist of a sheath introducer, a dilator, and often incorporate hydrophilic coatings to minimize friction and prevent trauma to the vessel walls during insertion. Their design is crucial for procedures requiring large-bore access, such as transcatheter aortic valve replacement (TAVR) or endovascular aneurysm repair (EVAR), ensuring hemostasis control and reducing complications related to vascular access site management.

Major applications of balloon introducer systems span across cardiology, radiology, and vascular surgery, playing an indispensable role in diagnosing and treating complex cardiovascular and peripheral diseases. The primary benefits include enhanced maneuverability of interventional devices, reduced procedural time, and significant minimization of patient discomfort and recovery time compared to traditional open surgical approaches. Furthermore, the introduction of specialized systems, such as steerable or adjustable sheaths, allows clinicians greater precision in reaching difficult anatomical locations, thereby improving clinical outcomes and widening the scope of treatable conditions.

The market is predominantly driven by the surging global prevalence of chronic cardiovascular diseases, including coronary artery disease and peripheral arterial disease, which necessitate high volumes of interventional procedures. Concurrently, the increasing elderly population, a demographic highly susceptible to these conditions, fuels demand for less invasive treatment options. Technological advancements, such as the development of smaller profile systems and devices compatible with radial artery access, are further driving adoption. Favorable reimbursement policies in developed economies and increasing healthcare infrastructure investments in emerging markets also contribute significantly to the market's sustained growth trajectory.

The Balloon Introducer System market exhibits robust growth fueled by technological innovation focused on improving device profile, flexibility, and biocompatibility, addressing critical needs in complex interventional cardiology and structural heart procedures. Business trends indicate a strong focus on strategic mergers and acquisitions among key market players aiming to consolidate distribution networks and integrate specialized manufacturing capabilities, particularly for large-bore systems used in transcatheter therapies. Furthermore, manufacturers are heavily investing in clinical trials demonstrating the safety and efficacy of next-generation introducer systems that minimize vascular trauma and access site complications, positioning clinical evidence as a primary competitive differentiator in market penetration strategies. The shift toward Ambulatory Surgical Centers (ASCs) for routine procedures, driven by cost containment pressures, represents a significant structural change impacting direct sales channels and requiring optimized logistical supply chains.

Regional trends highlight North America and Europe as established revenue generators due to sophisticated healthcare infrastructure, high procedural volumes, and favorable regulatory environments supporting rapid adoption of advanced medical devices. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), driven by massive population density, rising incidence of lifestyle diseases, improving economic conditions leading to increased healthcare spending, and government initiatives aimed at modernizing healthcare facilities in countries like China, India, and Japan. This regional expansion necessitates localized product sizing and training protocols to accommodate diverse patient demographics and varying levels of clinical expertise across different geographical markets.

Segmentation analysis reveals that the large-bore introducer segment, specifically those utilized in TAVR and Mitral Valve Repair/Replacement (TMVR), is experiencing accelerated growth due to the expansion of structural heart interventions. By end-user, hospitals remain the dominant segment, although specialty cardiac clinics and ASCs are rapidly gaining traction, driven by patient preference for outpatient settings and lower procedural costs. Technological advancements in coatings, particularly the use of highly lubricious hydrophilic materials, continue to dominate the product type segment, enhancing procedural safety and success rates. The overall market is moving toward greater specialization, where systems are increasingly tailored not only to the application (e.g., coronary vs. peripheral) but also to the specific access site (radial vs. femoral).

User inquiries regarding AI's influence on the Balloon Introducer System Market frequently center on automation, procedural guidance, inventory management, and personalized device selection. Key themes emerging from these questions include whether AI can minimize human error during complex access procedures, how machine learning might optimize sheath sizing based on real-time vessel anatomy (CT angiography data), and the role of predictive analytics in reducing access site complications, which remain a major concern in interventional cardiology. Users are particularly interested in AI-driven integration within catheterization labs that could link diagnostic imaging with procedural tools, potentially guiding the exact placement and handling of the introducer system. Furthermore, there is significant curiosity regarding AI's application in streamlining the supply chain and predicting demand fluctuations for specific introducer sizes, thereby optimizing hospital procurement processes and reducing waste.

The application of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is poised to significantly enhance the precision and safety of procedures involving balloon introducer systems. AI-powered image analysis tools can process complex imaging data (e.g., fluoroscopy, IVUS, OCT) in real-time, providing interventionalists with highly accurate anatomical measurements, crucial for selecting the optimal introducer size and trajectory. This capability reduces the risk of vessel injury and improves procedural efficiency, especially in tortuous or calcified vasculature. Predictive models utilizing patient-specific data, including comorbidities and vessel morphology, can anticipate the likelihood of vascular complications post-procedure, allowing clinicians to select specialized introducer systems or implement proactive closure strategies.

Beyond clinical applications, AI is transforming the operational aspects of the market. Manufacturers are leveraging AI for advanced simulation and design iteration, optimizing the biomechanical performance and material selection of new introducer systems before extensive physical prototyping. On the demand side, hospitals are starting to employ AI-driven inventory management systems that accurately track usage patterns of different introducer types, sizes, and brands. These systems minimize stockouts of critical supplies and prevent overstocking, leading to significant cost savings and improved resource allocation within high-volume interventional centers. This integration of AI across the value chain, from R&D to procurement, establishes a foundation for more customized and reliable product delivery.

The Balloon Introducer System Market dynamics are governed by a complex interplay of increasing demand for minimally invasive procedures (Drivers), stringent regulatory pathways (Restraints), and the untapped potential of novel material science (Opportunities). The primary driving force remains the global shift from open surgery to interventional techniques, necessitated by the rising burden of cardiovascular diseases and the advantages associated with shorter hospital stays and quicker patient recovery inherent in these procedures. Conversely, the market faces constraints related to the high upfront capital investment required for high-quality introducer systems and the inherent technical challenges associated with procedures requiring extremely large-bore access (e.g., TAVR), which can still lead to significant vascular complications if not managed properly. This balance of accelerating demand against technical constraints defines the competitive landscape.

Restraints are further amplified by rigorous regulatory approval processes, particularly in major markets like the U.S. and E.U., where evidence of long-term biocompatibility and clinical efficacy is mandatory for specialized, high-risk devices. Product recalls related to material failure or compromised hemostasis function can significantly impact market confidence and operational costs for manufacturers. However, significant opportunities exist in developing bio-absorbable or drug-eluting introducer sheaths designed to minimize inflammation and infection at the access site, addressing current limitations. Furthermore, market expansion into previously underserved rural areas and low-to-middle-income countries through differentiated pricing strategies and targeted clinician training represents substantial growth potential.

The impact forces within the market structure are intense, driven by the immediate need for improved clinical outcomes and efficiency in high-volume settings. Technological innovation acts as a powerful accelerating force, pushing manufacturers to continually refine sheath profiles and introduce advanced coating technologies (e.g., active hemostatic coatings) that improve performance. Simultaneously, pricing pressure from Group Purchasing Organizations (GPOs) and public health systems acts as a strong restraining force, compelling companies to focus on cost-efficient manufacturing and demonstrating superior economic value through clinical data. Ultimately, the market trajectory is heavily influenced by the adoption rate of structural heart procedures, which require the most sophisticated and specialized introducer systems, thereby setting the technological benchmark for the entire industry.

The Balloon Introducer System market is segmented across multiple critical dimensions, including product type, application, sheath size, and end-user, enabling focused analysis of market trends and strategic opportunities. Product segmentation differentiates between standard introducer sheaths, integrated systems (sheath and dilator kits), and specialty devices such as valved introducers, which are essential for structural heart interventions to prevent blood backflow. Application segmentation highlights the dominance of interventional cardiology procedures, though peripheral interventions, electrophysiology, and neurovascular applications represent high-growth niches requiring unique device specifications, such as increased flexibility or specialized radiopaque markers.

Sheath size remains a fundamental segmentation criterion, dividing the market into small-bore (typically 4F-7F), medium-bore (8F-12F), and large-bore (>12F) systems. The shift toward smaller profiles (radial access) is driving growth in the small-bore segment for diagnostic and routine procedures, while the explosive growth of TAVR and EVAR has cemented the large-bore segment as the highest value contributor. End-user segmentation categorizes consumption among hospitals, which account for the largest share due to infrastructure requirements for complex procedures, and rapidly expanding specialty centers such as Ambulatory Surgical Centers (ASCs) and Cardiac Catheterization Laboratories that focus on increasing procedural throughput and operational efficiency.

The value chain for the Balloon Introducer System Market begins with the upstream segment, which involves the sourcing and processing of specialized raw materials, primarily high-grade polymers such as PTFE, Pebax, FEP, and specialized stainless steel components for guidewires and dilators. This phase is highly reliant on chemical and materials engineering firms that can consistently supply materials meeting stringent biocompatibility and mechanical strength standards. The manufacturing process involves sophisticated extrusion, molding, bonding, and coating techniques, often performed in controlled cleanroom environments, requiring significant investment in advanced robotics and quality control infrastructure. Upstream supplier consolidation and the procurement of customized hydrophilic coatings are critical factors influencing the final product cost and performance characteristics.

Moving downstream, the value chain encompasses the distribution, sales, and end-user phases. Distribution channels are complex, involving both direct sales forces, particularly for high-value, large-bore systems requiring intensive clinical support, and indirect channels through large medical device distributors and Group Purchasing Organizations (GPOs). GPOs play a pivotal role in negotiating contracts, driving significant volume sales at predetermined prices, thus exerting continuous pressure on manufacturers’ profit margins. The effectiveness of the sales force, focused on providing comprehensive procedural training and technical support to interventional cardiologists and radiologists, is crucial for market penetration and sustained growth, especially when launching technologically advanced or novel systems.

The distribution logistics must be highly efficient, ensuring sterile, temperature-controlled delivery to hospitals and specialty centers globally. Direct sales are often preferred for premium or technically demanding products, allowing manufacturers to maintain tight control over product information and customer relationships. In contrast, indirect distribution through third-party logistics (3PL) providers and local distributors is vital for reaching fragmented markets in developing regions. The final consumption point—the hospital or ASC—provides critical feedback loops regarding product performance, which feeds back into the research and development pipeline, ensuring continuous product iteration aligned with evolving clinical needs, particularly concerning ease of use, profile size, and access site hemostasis management.

The primary end-users and potential customers of the Balloon Introducer System Market are institutions performing complex diagnostic and therapeutic cardiovascular and peripheral interventional procedures. These customers are broadly categorized as large tertiary care hospitals, specialized cardiac and vascular centers, and increasingly, high-volume Ambulatory Surgical Centers (ASCs). Hospitals, particularly those with established catheterization labs and structural heart programs, represent the largest volume buyers, often requiring a wide array of introducer sizes and specialty systems for procedures ranging from routine angioplasty to complex TAVR and EVAR procedures. Their purchasing decisions are heavily influenced by clinical efficacy data, ease of integration with existing lab equipment, and institutional contracts negotiated through GPOs.

Specialty cardiac clinics and ASCs, while performing a smaller proportion of the highest complexity cases, are rapidly increasing their procedural volume for routine peripheral and coronary interventions. These centers prioritize operational efficiency, cost-effectiveness, and devices that contribute to quick patient turnover. For these customers, factors such as simplified packaging, standardized kits, and reliable performance that minimizes complication risk are paramount. Manufacturers often tailor their sales strategies to ASCs by offering bulk pricing and streamlined procurement processes, recognizing their growing importance as cost-efficient providers of specialized care.

The purchasing cycle for these potential customers involves multiple stakeholders, including interventional cardiologists (who specify the required features), materials management teams (who handle logistics and vendor relations), and hospital administrators (who control budgets and capital expenditures). Successful market penetration requires engaging all these groups by demonstrating not only superior clinical outcomes but also quantifiable economic benefits, such as reduced complication rates leading to lower overall treatment costs, improved inventory control, and reduced procedure setup time. Continuous education and training provided by the device manufacturer are essential components of maintaining and expanding the customer base in this technologically driven segment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 855.4 Million |

| Market Forecast in 2033 | USD 1,460.9 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Boston Scientific Corporation, Teleflex Incorporated, B. Braun Melsungen AG, Terumo Corporation, Abbott Laboratories, Cook Medical, Merit Medical Systems, Cardinal Health, AngioDynamics, MicroPort Scientific Corporation, Getinge AB, Lepu Medical Technology, R. Bard (BD), Biotronik, Transluminal Technologies, Shenzhen YHLO Biotech Co., Ltd., Advanced Vascular Dynamics, Vascular Solutions (Teleflex), ASAHI INTECC CO., LTD. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Balloon Introducer System Market is characterized by continuous advancements in material science, focusing primarily on enhancing biocompatibility, flexibility, and radial strength while reducing wall thickness to achieve the lowest possible profile. The use of advanced polymer combinations, such as blends of high-density polyethylene and PTFE (Polytetrafluoroethylene), allows manufacturers to create thin-walled sheaths capable of accommodating larger inner diameters without increasing the outer diameter, a critical factor for minimizing vascular injury during insertion. Furthermore, specialized manufacturing techniques, including laser welding and proprietary tip molding processes, are employed to ensure a smooth, atraumatic transition between the dilator and the sheath, significantly improving insertion performance and reducing the risk of vessel dissection or plaque disruption.

A major focus area is the development and application of sophisticated surface coatings, predominantly hydrophilic coatings, which are essential for reducing frictional drag as the introducer navigates the tortuous vasculature. These coatings react with bodily fluids to create a highly slick surface, easing insertion and manipulation, which is crucial for complex procedures utilizing radial access where smaller vessels are involved. Beyond standard hydrophilic layers, the market is beginning to explore bio-active coatings, such as those that might include anti-thrombotic agents or localized drug delivery elements, potentially addressing long-standing issues related to localized inflammation and thrombosis formation at the access site following prolonged sheath insertion, thereby enhancing patient safety and recovery protocols.

Innovation also extends to the design of valve technology integrated within the introducer hub. Advanced hemostasis valves are necessary to minimize blood loss and air embolism risk, particularly when multiple devices are rapidly exchanged. Manufacturers are adopting proprietary valve designs that maintain exceptional seal integrity even under high pressure and with varying sizes of inner catheters, addressing concerns related to backbleeding in critical procedures. The integration of visualization technology, such as radiopaque markers and compatibility with advanced imaging modalities (like fluoroscopy and intravascular ultrasound), allows interventionalists unprecedented real-time control over device placement, further cementing technology's role as the primary determinant of competitive advantage in this specialized medical device market.

Geographically, the Balloon Introducer System Market demonstrates diverse growth patterns influenced by regional healthcare spending, regulatory frameworks, and procedural volume concentrations. North America, particularly the United States, commands the largest market share due to the high prevalence of cardiovascular diseases, early adoption of advanced interventional techniques (especially structural heart procedures like TAVR), and the presence of leading medical device manufacturers. Europe follows closely, driven by sophisticated healthcare systems in countries like Germany, France, and the UK, though market expansion can be occasionally tempered by stringent price controls imposed by public health systems.

The Asia Pacific (APAC) region is poised for the most rapid growth, fueled by massive untapped patient populations, increasing disposable income allocated to healthcare, and governmental investments aimed at expanding cardiac care infrastructure in densely populated nations. Latin America and the Middle East & Africa (MEA) currently hold smaller market shares but are experiencing incremental growth driven by rising awareness of minimally invasive options and increasing accessibility to advanced catheterization lab technologies, though market uptake is constrained by economic volatility and slower regulatory harmonization.

The market is primarily driven by the increasing global incidence of chronic cardiovascular diseases, the growing elderly population seeking minimally invasive treatments, and continuous technological advancements resulting in lower-profile, high-performance introducer systems that improve procedural safety and efficiency.

The segmentation by sheath size is crucial, with the large-bore segment (>12F) generating the highest average revenue per unit due to its necessity in high-value structural heart interventions like TAVR and EVAR, while the small-bore segment (4F-7F) drives volume due to its use in standard diagnostic and radial access procedures.

Hydrophilic coatings are essential for reducing frictional resistance between the introducer system and the vessel wall. This minimizes trauma during insertion, eases device navigation through tortuous anatomy, and significantly reduces the risk of access site complications, thereby improving overall procedural success.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), fueled by expanding healthcare infrastructure, rising prevalence of lifestyle diseases, and increasing governmental focus on providing modern interventional cardiology services in major economies like China and India.

Key restraints include the high initial procurement cost associated with specialized, large-bore introducer systems, particularly for structural heart interventions, and the need to navigate stringent regulatory approval processes that often slow the commercialization of new, complex devices.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.