ID : MRU_ 435553 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

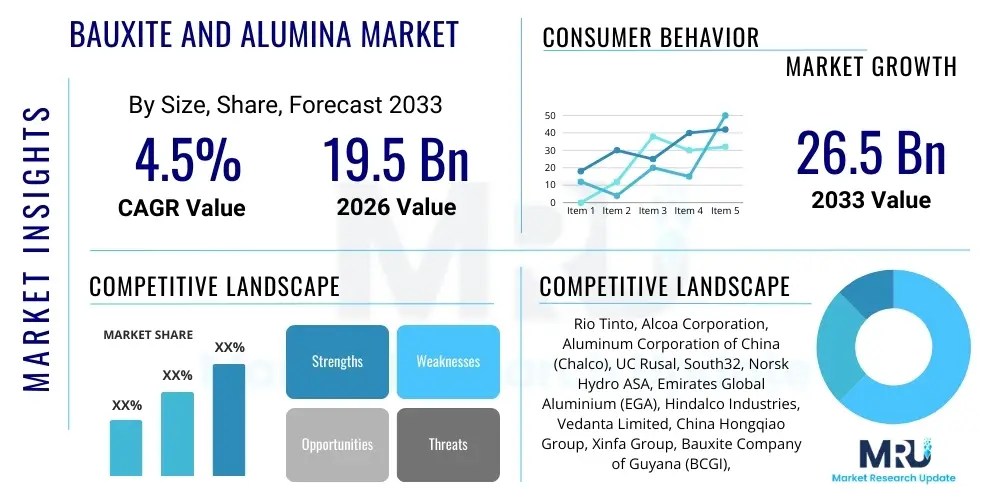

The Bauxite and Alumina Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2026 and 2033. The market is estimated at USD 19.5 Billion in 2026 and is projected to reach USD 26.5 Billion by the end of the forecast period in 2033.

The Bauxite and Alumina Market forms the fundamental upstream supply chain necessary for global aluminum production. Bauxite, a naturally occurring aluminum ore, is primarily refined through the energy-intensive Bayer process to produce alumina (aluminum oxide), which is subsequently smelted into primary aluminum using the Hall–Héroult process. This essential industrial commodity is characterized by its high volume, concentration of reserves in specific geopolitical regions, and intense dependency on energy costs for processing.

Alumina serves as the indispensable precursor for over 90% of the world's aluminum, a metal celebrated for its lightweight, strength, corrosion resistance, and recyclability. The market dynamics are inextricably linked to global economic health, particularly the expansion of infrastructure and manufacturing sectors. Major applications span structural components in the aerospace and automotive industries, efficient packaging solutions, and essential materials in the construction sector, driven by persistent urbanization trends and the push toward vehicle lightweighting to enhance fuel efficiency and facilitate electrification.

Key benefits derived from the use of alumina include superior thermal resistance, high hardness, and chemical stability, enabling its widespread use in non-metallurgical applications such as refractories, abrasives, and specialized ceramics. The market's primary driving factors currently revolve around robust demand from emerging economies for basic infrastructure development, accelerated technological advancements in low-carbon aluminum smelting, and increasing regulatory pressure promoting sustainable raw material sourcing and production efficiency across the value chain.

The Bauxite and Alumina market is currently navigating a period defined by fluctuating energy prices, heightened geopolitical risk impacting supply stability, and an aggressive industry shift toward decarbonization. Business trends show major mining and processing firms investing heavily in vertical integration and modernizing aging refineries to improve operational efficiency and reduce the environmental footprint, specifically tackling the challenge of red mud residue management. Furthermore, the global aluminum industry’s commitment to achieving net-zero emissions is catalyzing demand for green alumina derived from sustainable energy sources, influencing capital expenditure decisions and partnership formation across the supply chain.

Regional trends highlight the Asia Pacific (APAC) region, dominated by China and India, as the central engine of market growth, driven by massive domestic consumption in construction and electronics manufacturing, alongside established production capacity. While China remains the largest refiner of alumina, strict environmental enforcement and domestic power limitations are encouraging shifts in sourcing and refining operations toward resource-rich nations in Africa and South America. North America and Europe, while having lower production volumes, are focusing intensively on technological innovation, circular economy initiatives, and securing resilient, ethically sourced supply chains, often through long-term contracts with stable geopolitical partners.

Segmentation trends indicate metallurgical grade alumina will continue to dominate due to the overwhelming demand from the primary aluminum sector, though non-metallurgical grades are experiencing specialized growth, particularly in advanced ceramics and high-temperature refractory linings used in industrial furnaces. The focus within the technology segment is moving away from incremental efficiency gains toward transformative changes, such as utilizing renewable energy for the Bayer process and exploring technologies that minimize or eliminate the production of hazardous bauxite residue (red mud), ensuring the long-term viability and social license to operate for market participants.

Users frequently inquire about how Artificial Intelligence (AI) can mitigate the two major historical challenges in the Bauxite and Alumina sector: the high energy consumption of the refining process and the volatility of raw material sourcing. Common questions center on the application of predictive maintenance to prevent costly downtimes in high-pressure steam lines and kilns, the use of machine learning algorithms for optimizing the Bayer process parameters (such as temperature, concentration, and caustic consumption) in real time to maximize yield and minimize energy use, and the role of AI in complex geological surveying and resource modeling to locate high-grade, easily accessible bauxite deposits. The underlying expectation is that AI will be a primary tool for achieving both operational excellence and stringent sustainability targets, transforming the historically manual and energy-intensive industry into a data-driven, highly efficient sector.

The implementation of sophisticated AI models is also expected to significantly enhance supply chain resilience. By analyzing global shipping routes, political stability indices, and real-time commodity pricing data, AI systems can provide advanced forecasting for sourcing bauxite and distributing refined alumina, helping producers hedge against unforeseen risks and optimize inventory levels. This proactive approach minimizes exposure to price volatility and logistical bottlenecks, which have traditionally plagued the sector due to its reliance on long-distance maritime transport. Furthermore, AI is crucial in developing advanced sensor technology and interpreting the massive datasets generated by modern refineries, enabling the creation of 'digital twins' for simulation and optimizing future plant designs for improved thermal efficiency.

A further key area of interest is the use of AI in environmental management, particularly concerning the vast quantities of red mud generated. AI algorithms are being applied to classify, characterize, and potentially find high-value uses for this residue, moving beyond simple disposal toward valorization. By analyzing the complex chemical composition of red mud from different sources, AI can identify optimal leaching processes or specific industrial applications (like cement additives or rare earth metal extraction), turning a waste product into a potential revenue stream, thereby addressing significant environmental and regulatory concerns associated with bauxite refining.

The market for Bauxite and Alumina is propelled primarily by enduring global urbanization and industrialization trends, which solidify the foundational demand for aluminum in construction, automotive, and electrical transmission infrastructure. These foundational drivers are strongly complemented by the accelerating transition to electric vehicles (EVs), where aluminum's lightweighting properties are crucial for extending battery range and improving overall energy efficiency. However, the industry faces severe structural restraints, notably the immense energy intensity of the refining process, which exposes producers to volatile global energy markets and high carbon taxes. Additionally, stringent environmental regulations governing the management and storage of bauxite residue (red mud) impose substantial operational and capital expenditure burdens, particularly in jurisdictions with sensitive ecosystems.

Opportunities for growth are concentrated in technological breakthroughs and shifts toward sustainable practices. The development and commercial viability of green alumina production, utilizing renewable energy sources like solar or hydro power for the Bayer process, represent a significant avenue for market expansion and differentiation, attracting environmentally conscious buyers and commanding potential price premiums. Furthermore, the increasing global focus on resource security is opening new opportunities for bauxite mining in previously untapped regions of Africa and Southeast Asia, diversifying the supply base away from traditional concentrated sources and promoting regional economic development.

The impact forces currently reshaping the market center on ESG (Environmental, Social, and Governance) compliance and technological disruption. Geopolitical shifts, particularly trade tensions and resource nationalism, act as powerful external forces influencing sourcing strategies and investment decisions. Internally, the force of technological innovation, including the adoption of inert anode technology in aluminum smelting (which eliminates direct CO2 emissions from the reduction process) and advanced digital solutions for operational efficiency, necessitates rapid capital turnover and adaptation by market participants. These forces compel industry players to prioritize supply chain transparency, resource efficiency, and carbon footprint reduction to maintain competitiveness and regulatory adherence.

The Bauxite and Alumina market is comprehensively segmented based on the end product’s application, the grade of the material produced, and the ultimate end-use industry utilizing the aluminum or related compounds. The segmentation reflects the diverse demand characteristics ranging from high-volume commodity production necessary for metallurgy to niche, high-performance materials required for specialized industrial uses. Understanding these segments is crucial for producers to align their resource allocation and processing capabilities, especially considering the distinct quality requirements, impurity tolerances, and pricing structures associated with metallurgical versus non-metallurgical applications.

Metallurgical grade alumina overwhelmingly dominates the market volume, serving as the essential feedstock for the primary aluminum industry, driven by expansive demand from construction and transportation sectors. Conversely, non-metallurgical alumina, though smaller in volume, commands higher value due to its purity and specialized properties required for applications like refractory materials used in high-temperature environments, technical ceramics requiring exceptional hardness and dielectric properties, and chemical synthesis. The geographical distribution of demand further emphasizes segmentation, with Asia Pacific driving volume consumption, while North America and Europe focus on high-value, specialized segments requiring advanced non-metallurgical compounds.

The major industrial segments driving consumption remain closely tied to global infrastructure development. The packaging industry, particularly for beverages and flexible containers, exhibits stable, resilient demand. The automotive sector, experiencing a rapid evolution toward electric mobility, demands increasing quantities of high-strength, lightweight aluminum alloys, thus ensuring continuous robust demand for high-quality alumina. This complex interplay of volume-driven and value-driven demand across different applications necessitates highly flexible and quality-controlled production facilities throughout the global supply chain.

The Bauxite and Alumina value chain is typically characterized by high upstream concentration and significant downstream processing costs. Upstream activities involve bauxite mining and beneficiation, which are concentrated in geologically rich regions such as Australia, Guinea, Brazil, and China. Efficiency at this stage is dictated by the grade and mineralogy of the ore, as lower-grade bauxite requires more intense pre-treatment and caustic soda consumption in the subsequent refining phase. Integration between mining operations and refining facilities (alumina refineries) is a key strategic advantage, minimizing transport costs and optimizing raw material quality control, thus influencing the overall cost competitiveness of the refined product.

The midstream phase, dominated by the Bayer process to convert bauxite into alumina, is the most capital and energy-intensive step. Alumina refineries are strategically located near major bauxite reserves or close to abundant, cheap energy sources (e.g., hydro or coal power, depending on regional regulations) and typically require access to large caustic soda supplies. The distribution channel for refined alumina is highly globalized, relying heavily on specialized bulk carriers and port infrastructure to transport millions of tons annually to aluminum smelters located across different continents. Direct distribution models, where integrated companies transport alumina to their own smelters, are prevalent, though significant volumes are traded on open markets or through long-term contracts.

Downstream analysis focuses on the final use of alumina, primarily in the production of primary aluminum via the Hall–Héroult smelting process. This step requires massive electrical power and yields the final metallic product. Indirect channels involve the sale of non-metallurgical alumina to specialized manufacturers of refractories, ceramics, and chemical catalysts, often through specialized distributors who provide technical support and smaller, customized material batches. The structure of this value chain emphasizes vertical integration as a risk mitigation strategy against price volatility at both the mining and refining stages, with logistics efficiency being a paramount concern given the sheer volume of materials handled.

The primary customer base for Bauxite and Alumina is defined by the heavy industry sectors reliant on aluminum production and specialized high-performance materials. The largest segment of buyers consists of global aluminum smelting companies, which require high-purity metallurgical alumina as the sole input for their reduction plants. These major customers include multinational corporations involved in primary aluminum production, often characterized by high-volume, long-term procurement contracts necessary to sustain continuous, energy-intensive smelting operations. Their purchasing decisions are critically dependent on alumina quality, consistency, and the competitive cost per ton delivered, placing high importance on supplier reliability and logistical competence.

A secondary, high-value segment comprises manufacturers specializing in non-metallurgical products. These end-users, such as refractory lining manufacturers, technical ceramics producers for electronics and machinery, and specialty chemical companies, demand specific grades of non-metallurgical alumina (e.g., tabular, fused, or activated alumina). These customers are less sensitive to volume fluctuations but require materials with exact physical and chemical specifications, including precise particle size distributions and minimal impurity levels, leading to premium pricing for specialized grades. The shift towards electrification and high-performance manufacturing is increasing the relevance of these niche buyers, particularly those involved in advanced battery components and high-temperature industrial processes.

Furthermore, indirect buyers include large-scale construction and infrastructure development firms that drive overall aluminum demand, though they purchase the finished metal rather than the raw material. Government entities, particularly in countries with significant defense or aerospace sectors, also act as influential indirect customers, setting quality standards and driving demand for high-performance, lightweight alloys derived from premium alumina. The evolving regulatory environment, particularly mandates concerning environmental performance, means that potential customers are increasingly scrutinizing the sustainability credentials and carbon footprint associated with the source of their purchased alumina.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 19.5 Billion |

| Market Forecast in 2033 | USD 26.5 Billion |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Rio Tinto, Alcoa Corporation, Aluminum Corporation of China (Chalco), UC Rusal, South32, Norsk Hydro ASA, Emirates Global Aluminium (EGA), Hindalco Industries, Vedanta Limited, China Hongqiao Group, Xinfa Group, Bauxite Company of Guyana (BCGI), Jamalco, Alumina Limited, EGA Bauxite & Alumina. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The current technology landscape in the Bauxite and Alumina market is dominated by incremental refinements of the well-established Bayer process, alongside disruptive innovations aimed specifically at reducing carbon emissions and managing bauxite residue. Traditional technological focus centers on improving efficiency within the digester and precipitation stages, primarily through advanced process control systems, enhanced heat recovery exchangers, and optimization of the caustic soda regeneration circuit, all aimed at lowering the massive thermal energy input required. Digitalization, incorporating Industrial IoT sensors and integrated control software, is foundational to extracting maximum performance from existing refinery assets while maintaining stringent quality control over the refined alumina product.

However, the most impactful technological shifts are driven by environmental mandates. A key focus is the development of inert anode technology for the subsequent aluminum smelting phase. While inert anodes do not directly affect the Bayer process, their adoption fundamentally changes the demand structure for alumina purity, favoring lower silica and iron oxide content to prevent side reactions in the smelting cell. Furthermore, research into alternative bauxite processing methods, such as non-caustic leaching or high-pressure acid leaching for low-grade ores, seeks to bypass the complexities and high energy demand of the conventional Bayer method entirely, although these technologies are currently expensive and less commercially scalable for metallurgical volumes.

Crucially, technology related to Red Mud (Bauxite Residue) management is receiving unprecedented attention. Innovations range from dry stacking techniques to minimize water usage and land area, to complex chemical and physical processes aimed at valorization—extracting valuable components such as titanium, rare earth elements, or iron content, or utilizing the residue as an additive in cement or construction aggregates. The deployment of advanced computational modeling, including predictive geology and mineral processing simulation tools, is essential for identifying and exploiting new, economically viable bauxite deposits while simultaneously designing environmentally superior refinery operations from the ground up, ensuring the market meets its sustainability targets effectively.

Regional dynamics are critical in defining the global Bauxite and Alumina market structure, dictated by resource endowments, energy costs, and consumption patterns. The Asia Pacific (APAC) region stands as the undisputed center of both production and consumption. China, despite facing regulatory pressure to curb pollution and rationalizing its energy-intensive industry, remains the single largest global producer and consumer of refined alumina, sustaining demand through vast infrastructure projects and dominance in the global electronics supply chain. India is rapidly emerging as a major player, leveraging substantial bauxite reserves and expanding domestic refining capacity to serve its growing internal market, driven by urbanization and an expanding middle class.

North America and Europe, characterized by mature, high-cost energy environments and strict environmental compliance, are net importers of alumina but lead in technological innovation and high-value non-metallurgical applications. Their strategic focus is on securing diversified, low-carbon supply chains, increasing the demand for certified "green" alumina. These regions are investing heavily in recycling infrastructure to increase reliance on secondary aluminum, which indirectly places pressure on primary alumina producers to meet the highest ESG standards to remain competitive in securing long-term contracts.

The Middle East and Africa (MEA) and Latin America are increasingly vital as primary resource hubs. Guinea in West Africa possesses the world's largest high-grade bauxite reserves and is rapidly expanding its mining and export infrastructure, making it a critical strategic supplier to global refining centers, particularly China. Brazil and Jamaica in Latin America maintain significant bauxite mining and refining operations, often vertically integrated with major global aluminum producers. These regions benefit from lower operating costs and large reserves but face challenges related to political stability, infrastructure development, and establishing robust environmental governance frameworks, which influence overall market supply stability.

The primary driver is the accelerating global demand for lightweight aluminum, particularly driven by urbanization, infrastructure development in Asia Pacific, and the rapid adoption of electric vehicles (EVs) necessitating lighter automotive body structures.

Alumina refining via the Bayer process is extremely energy-intensive, meaning volatile fluctuations in natural gas or electricity prices directly and severely impact operational expenditure, significantly compressing profit margins for non-integrated or high-cost producers.

The key technological focus is the effective management and valorization of bauxite residue (red mud), seeking innovative processes for resource extraction or safe utilization in construction materials, alongside the development of green alumina production methods powered by renewable energy.

Australia historically holds significant market share, but Guinea (West Africa) is rapidly emerging as the dominant global supplier of seaborne bauxite, holding the largest reserves and expanding its production capacity dramatically to meet Chinese demand.

Non-metallurgical alumina, while smaller in volume, is critical for high-value applications such as refractories, advanced ceramics, and abrasives. Its value is driven by strict purity and performance specifications required for specialized industrial processes and high-tech manufacturing.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.