ID : MRU_ 432035 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

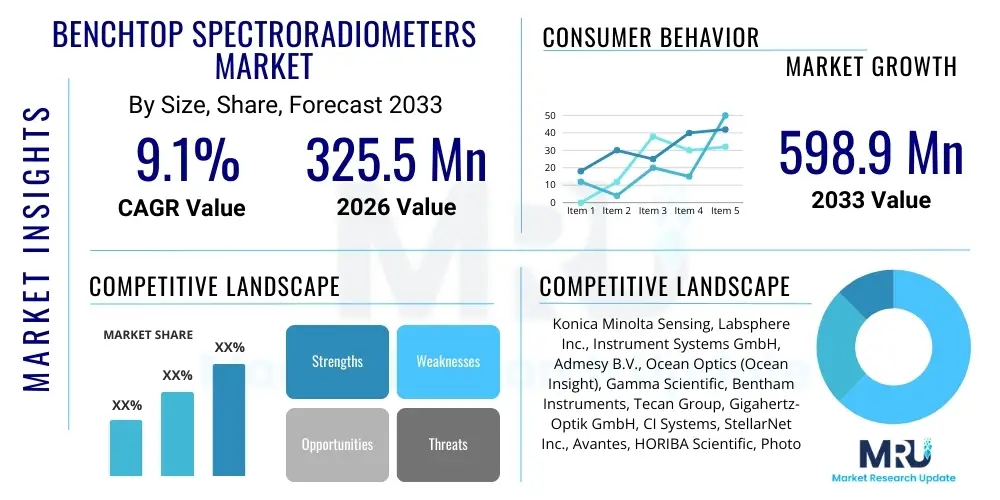

The Benchtop Spectroradiometers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.1% between 2026 and 2033. The market is estimated at $325.5 Million USD in 2026 and is projected to reach $598.9 Million USD by the end of the forecast period in 2033.

The Benchtop Spectroradiometers Market encompasses advanced optical instruments used for precise measurement of light parameters across the electromagnetic spectrum, typically from the ultraviolet (UV) through the visible (VIS) to the infrared (IR) regions. These high-precision devices are essential for determining spectral radiance, irradiance, luminance, and chromaticity, offering superior accuracy and resolution compared to handheld or portable alternatives. Benchtop units are distinguished by their robust design, complex internal components, and ability to handle highly demanding laboratory and manufacturing quality control environments where measurement integrity is paramount. They utilize technologies such as diffraction gratings and sophisticated detector arrays to analyze light sources, surfaces, and materials, making them indispensable tools in modern research and high-tech manufacturing sectors.

Major applications driving the demand for benchtop spectroradiometers include the quality assurance of modern display technologies, such as OLED and MicroLED, the optimization of solid-state lighting (SSL) products like LEDs, and critical tasks in remote sensing and solar energy research. In the display sector, these instruments ensure color consistency, uniformity, and luminance accuracy, meeting the stringent standards required for consumer electronics and professional monitors. Similarly, in the lighting industry, they are vital for characterizing luminous flux, correlated color temperature (CCT), and color rendering index (CRI) of LED products, which is crucial for energy efficiency and human health considerations (non-visual effects of light). The increasing complexity and performance demands of these end-user products necessitate the precision offered by benchtop systems.

The primary benefits derived from using benchtop spectroradiometers include unparalleled accuracy, high spectral resolution, stability over long measurement periods, and comprehensive software integration for complex data analysis. Key driving factors fueling market expansion are the global push toward energy-efficient lighting solutions, the rapid proliferation of advanced display technologies in automotive and consumer electronics, and increasing investment in photovoltaic research aimed at optimizing solar panel efficiency. Furthermore, the stringent regulatory requirements across various industries, particularly those involving human-machine interfaces and visual performance, mandate the adoption of certified, high-accuracy measurement equipment, thereby reinforcing the market's trajectory.

The global Benchtop Spectroradiometers Market is experiencing robust growth driven by accelerating technological advancements in photonics and display manufacturing, positioning the market for substantial expansion through 2033. Current business trends indicate a strong shift towards integrating these devices into automated quality control lines, moving beyond traditional laboratory use cases. This integration is facilitated by enhanced connectivity options and sophisticated data processing software that allows for real-time spectral analysis and feedback loops in high-volume production environments, such as those found in the Asian electronics supply chain. Manufacturers are prioritizing solutions that offer faster measurement cycles without compromising spectral fidelity, responding to the demand for efficient yet precise testing in industries facing increasing throughput pressures.

Regional trends highlight the Asia Pacific (APAC) region as the dominant market, primarily due to the concentration of major display panel manufacturers (South Korea, China, Taiwan) and global LED production hubs. North America and Europe maintain significant market shares, characterized by high investment in aerospace and defense research, advanced automotive lighting R&D, and pharmaceutical photostability studies, driving demand for the most sophisticated, high-end spectral measurement systems. Emerging economies in Latin America and the Middle East are showing accelerated adoption rates, fueled by infrastructure development projects requiring rigorous quality control for lighting systems and growing local electronics assembly capabilities, although these regions currently lag behind the established markets in terms of overall consumption volume.

Segment trends reveal that the Array-based Spectroradiometers segment holds the largest share, favored for its speed and suitability in production line quality control, allowing simultaneous measurement of multiple wavelengths. However, the Scanning Spectroradiometers segment, while slower, maintains its niche dominance in high-resolution scientific research and calibration laboratories where the utmost spectral precision is non-negotiable. Application-wise, Display Measurement remains the primary revenue driver, intrinsically linked to the continuous innovation cycles of consumer electronics. Furthermore, the burgeoning demand from the Solar Measurement segment, driven by global renewable energy initiatives and the need to characterize complex multi-junction solar cells, presents a significant high-growth opportunity for market stakeholders specializing in robust, field-deployable calibration standards and laboratory-grade instruments.

User queries regarding AI's role in the Benchtop Spectroradiometers Market frequently revolve around three core themes: enhanced data interpretation, automation capabilities, and predictive maintenance. Users are keenly interested in how Artificial Intelligence can move beyond mere data collection to provide actionable, real-time insights—specifically, automating the detection of subtle spectral anomalies indicative of material defects in displays or LEDs, which are often missed by traditional thresholds. Concerns also focus on integrating AI models for complex spectral classification, such as identifying trace impurities or classifying nuanced color shifts (metamerism) that require subjective human judgment. The expectation is that AI will drastically reduce measurement time and lower the barrier to complex analysis, making sophisticated spectral insights accessible outside dedicated spectroscopy labs, ultimately leading to higher production yields and faster failure analysis.

The integration of Artificial Intelligence is revolutionizing how benchtop spectroradiometers are utilized and maintained. AI algorithms are increasingly employed for advanced calibration drift correction, where machine learning models analyze historical performance data and environmental variables (temperature, humidity) to predict and preemptively compensate for minor instrument shifts, significantly improving long-term measurement stability and reducing the frequency of costly physical recalibrations. Furthermore, in high-throughput manufacturing settings, AI is used for rapid, automated spectral fingerprinting, allowing instantaneous comparison of thousands of measured spectra against ideal quality standards. This capability is critical in minimizing false positives and negatives, accelerating the quality control process in dynamic environments like OLED panel manufacturing where spectral consistency is a primary quality metric.

The market for Benchtop Spectroradiometers is fundamentally shaped by a dynamic interplay of Drivers, Restraints, and Opportunities, collectively forming the critical Impact Forces determining market expansion. Major drivers include the relentless technological push towards higher resolution and wider color gamut displays (e.g., 8K, HDR, MicroLED), which mandates increasingly stringent and accurate measurement tools to ensure viewer experience and regulatory compliance. Simultaneously, the global mandate for sustainable and efficient lighting has institutionalized the requirement for accurate spectral characterization of solid-state lighting (SSL), directly fueling the demand for high-end benchtop systems capable of meeting CIE standards. This technological dependency, coupled with the need for high-confidence data in mission-critical applications like aerospace optics calibration, sustains the market's upward momentum.

However, the market faces significant restraints, primarily centered around the substantial initial capital investment required for high-accuracy benchtop units, making them prohibitive for smaller laboratories, academic institutions with limited budgets, or medium-sized manufacturers. Furthermore, these instruments require highly specialized technical expertise for optimal operation, calibration, and data interpretation, contributing to operational overhead and limiting widespread adoption in regions with nascent technical talent pools. The increasing competitiveness and performance improvement of high-end portable and handheld spectroradiometers also pose a mild constraint, as these smaller, more versatile devices begin to meet the lower-to-mid-range accuracy requirements previously exclusive to benchtop systems, potentially eroding some entry-level market share.

Opportunities for growth are concentrated in the rapid commercialization of next-generation display technologies, particularly flexible OLEDs and augmented/virtual reality (AR/VR) head-mounted displays, which require novel spectral and photometric measurements due to complex near-eye optics and unique light output patterns. The expanding focus on environmental monitoring, including atmospheric and water quality assessment using spectral signature analysis, offers a substantial market adjacency. Additionally, the proliferation of Internet of Things (IoT) sensors and connected devices, which rely on precise light detection and color communication, presents a niche opportunity for developing spectroradiometers optimized for sensor characterization and calibration, moving beyond traditional light source measurement. Successfully navigating these opportunities requires continuous innovation in detector technology and robust software ecosystems that simplify complex measurement tasks.

Summary of DRO & Impact Forces:

The Benchtop Spectroradiometers Market is segmented primarily by Type, Application, and End-User, reflecting the diverse technical requirements and industrial deployment scenarios of these precision instruments. Analyzing the market through these lenses provides a clear understanding of where growth capital is concentrated and which technological advancements are most favored by specific industries. The segmentation by Type, specifically distinguishing between array-based and scanning systems, highlights the trade-off between speed (array) and precision (scanning), fundamentally dictating their suitability for production line versus laboratory environments. The breadth of applications, from display calibration to remote sensing, underscores the cross-sectoral importance of high-fidelity spectral measurement, which is vital for product success and scientific advancement across numerous fields.

In terms of end-users, the market exhibits a high degree of dependence on the Electronics and Semiconductor industry, which leverages spectroradiometers for critical quality control of every light-emitting component, from mobile phone screens to optical sensors. The distinction between commercial and research applications is also key; while commercial users prioritize throughput, repeatability, and robust factory integration, research institutes often seek the highest possible spectral resolution and sensitivity, influencing the purchasing decisions towards higher-end scanning models. This inherent segmentation ensures that manufacturers offer tailored product lines designed to address the specific pain points and regulatory compliance needs of each distinct segment, maximizing market penetration.

The trend towards miniaturization and enhanced connectivity is beginning to blur the lines between high-end portable devices and entry-level benchtop units, challenging traditional segmentation boundaries. However, the fundamental physical limitations regarding thermal management, detector size, and optics complexity ensure that benchtop instruments will retain their dominant position for applications requiring absolute NIST-traceable accuracy and stability. Future segmentation growth is expected to be highest in the solar and emerging display technology applications, given the intense research and rapid commercialization cycles anticipated in these areas through the forecast period.

The value chain for the Benchtop Spectroradiometers Market is complex, beginning with highly specialized upstream suppliers providing critical optical components and precision electronics. Upstream activities are dominated by specialized manufacturers of high-performance diffraction gratings, highly sensitive CCD/CMOS or InGaAs detector arrays, and custom-designed optical fibers. These components require specialized fabrication processes and are characterized by high barriers to entry, leading to strong reliance on a limited number of niche suppliers. The quality and performance of these foundational elements directly determine the ultimate accuracy and spectral range of the final benchtop unit, making robust supply chain management a critical competitive factor for system integrators.

Midstream activities involve the core instrument manufacturing, calibration, and software development. Leading spectroradiometer manufacturers focus heavily on integrating these high-end components into thermally stable, vibration-resistant enclosures, developing proprietary measurement firmware, and executing rigorous, NIST-traceable calibration procedures. The calibration process, which establishes the absolute accuracy of the instrument against certified standards, is arguably the most value-intensive step in the midstream. Simultaneously, the development of user-friendly yet powerful data analysis software—often incorporating AI features for automated analysis—adds significant intellectual property and value, transforming raw spectral data into actionable industrial insights.

Downstream activities include distribution, sales, technical support, and post-sales calibration services. Distribution channels are typically a mix of direct sales teams for major, specialized customers (e.g., large government labs or Tier 1 electronics manufacturers) and indirect distribution through value-added resellers (VARs) and specialized technical distributors who can provide local support and integration services. Post-sales support and periodic recalibration services are essential revenue streams and critical determinants of customer satisfaction, particularly given the sensitivity and high maintenance requirements of these precision instruments. The final end-users, ranging from automotive QA labs to photovoltaic researchers, demand comprehensive training and rapid technical assistance to maintain measurement uptime.

The primary potential customers for Benchtop Spectroradiometers are entities requiring extremely high precision in the measurement and characterization of light, color, or material spectral properties. End-users fall broadly into two categories: industrial manufacturing (for quality control and R&D) and institutional/scientific research. In the industrial sphere, major buyers include manufacturers of advanced displays (OLED, QLED, MicroLED), which use these systems to ensure uniformity, color fidelity, and white point calibration across panels. The automotive sector, specifically suppliers developing advanced Head-Up Displays (HUDs) and intricate LED matrix lighting systems, represents a growing customer base prioritizing instruments capable of handling complex photometric and spectral measurements under varying conditions.

In the institutional and scientific domain, potential customers include national metrology institutes (NMIs) responsible for maintaining primary light standards, university research laboratories focusing on materials science, chemistry, and physics, and government defense organizations utilizing advanced optical sensor technology. These groups often require the highest spectral resolution and widest dynamic range available, favoring high-end scanning spectroradiometers. Furthermore, companies involved in solar cell manufacturing and testing are key buyers, utilizing these instruments to determine the quantum efficiency and spectral response of photovoltaic materials under standardized test conditions, critical for maximizing energy conversion rates.

A rapidly emerging customer segment includes third-party calibration houses and independent testing laboratories that provide contract measurement services for smaller firms unable to invest in their own benchtop equipment. These service providers require multi-purpose, robust spectroradiometers that can be certified and handle diverse sample types, from small-scale LEDs to large-area screens. The decision-making process for these customers is heavily influenced by instrument specifications like measurement speed, long-term stability, software interface usability, and the manufacturer's global reputation for calibration and support services, reinforcing the market importance of technical differentiation and service infrastructure.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $325.5 Million USD |

| Market Forecast in 2033 | $598.9 Million USD |

| Growth Rate | 9.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Konica Minolta Sensing, Labsphere Inc., Instrument Systems GmbH, Admesy B.V., Ocean Optics (Ocean Insight), Gamma Scientific, Bentham Instruments, Tecan Group, Gigahertz-Optik GmbH, CI Systems, StellarNet Inc., Avantes, HORIBA Scientific, Photo Research, Spectrolight Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Benchtop Spectroradiometers Market is characterized by continuous innovation aimed at increasing measurement speed, expanding spectral range, enhancing resolution, and improving sensitivity, particularly in low-light conditions. A fundamental technological trend involves the transition from traditional cooled CCD (Charge-Coupled Device) arrays to high-performance, deep-cooled CMOS (Complementary Metal-Oxide-Semiconductor) arrays and specialized InGaAs (Indium Gallium Arsenide) detectors for accurate near-infrared (NIR) and short-wave infrared (SWIR) measurements. Advancements in diffraction grating fabrication, including holographic gratings, are critical for minimizing stray light and maximizing spectral purity, allowing for the precise measurement of complex or highly saturated colors and narrow-band light sources like lasers and specialized LEDs.

Another crucial technological area is the integration of advanced thermal management systems, such as Peltier cooling elements, which stabilize the detector temperature far below ambient levels. This thermal stability is essential for reducing noise (especially dark current) and ensuring long-term measurement consistency, which is mandatory for accreditation in primary calibration laboratories. Furthermore, manufacturers are heavily investing in developing proprietary, high-throughput optics, including specialized lens systems and integrating spheres, that efficiently collect and homogenize light input while minimizing geometric errors, which is paramount for measuring large-area displays or highly directional LED beams accurately according to industrial standards (e.g., CIE recommendations). These optical advancements are necessary to meet the increasingly complex measurement geometry requirements demanded by the automotive and aerospace industries.

The shift towards software-defined metrology is also reshaping the market. Modern benchtop spectroradiometers are now sophisticated systems where the hardware's performance is highly leveraged by sophisticated processing algorithms. Key technological features include the development of proprietary spectral calibration routines that automate wavelength and radiometric calibration, and the integration of advanced signal processing techniques (such as spectral binning and averaging) to enhance the signal-to-noise ratio without significantly sacrificing measurement speed. The incorporation of AI and machine learning into the software stack for predictive analytics and automated defect classification represents the cutting edge, turning the spectroradiometer from a passive measurement tool into an active, intelligent quality control station capable of complex decision-making.

The APAC region, spearheaded by countries like China, South Korea, Japan, and Taiwan, holds the largest market share and is projected to exhibit the highest growth rate globally. This dominance is directly attributable to the region being the global epicenter for the manufacturing of high-end consumer electronics, particularly advanced display panels (OLED, QD-OLED, MicroLED) and solid-state lighting components. The relentless competition among Asian giants to produce superior visual technologies drives continuous investment in high-accuracy benchtop spectroradiometers for critical R&D and automated factory quality assurance. Furthermore, substantial government investments in solar energy projects and associated photovoltaic research facilities in countries like India and China are accelerating the adoption of these instruments for solar spectral testing and calibration.

Market expansion in APAC is characterized by a strong preference for high-throughput, array-based spectroradiometers that can be integrated seamlessly into automated production lines running 24/7. However, the region also maintains a robust demand for scanning spectroradiometers within national metrology institutions (such as NMIJ in Japan and NIM in China) to maintain primary light and color standards, ensuring traceability across the vast electronics supply chain. The sheer scale of manufacturing output and the continuous technological refresh cycle in electronics manufacturing ensures APAC remains the foundational pillar of the global market.

North America maintains a strong position in the benchtop spectroradiometers market, driven primarily by high investment in advanced research and development across various high-tech sectors, including aerospace, defense optics, biomedical imaging, and cutting-edge automotive displays (e.g., advanced HUDs). The region's market is characterized by a demand for extremely precise, highly customized, and often large-format benchtop units capable of complex spectral measurements required for sensitive military and space-based applications. Major drivers include the presence of leading technology companies and prominent research universities that utilize spectroradiometers for fundamental materials research and developing next-generation light sources and sensors.

The North American market emphasizes instruments with the broadest spectral range and highest sensitivity, often necessitating specialized detectors and complex cooling systems. Regulatory compliance, particularly related to lighting standards (e.g., energy consumption and human factor considerations), also contributes significantly to sustained demand. The trend toward domestic semiconductor manufacturing and advanced optical component production further ensures a high-value customer base that requires rigorous calibration and quality control standards.

Europe represents a mature and technologically sophisticated market, with demand primarily fueled by the highly regulated automotive industry and the strong presence of international standards bodies and large industrial research clusters. European automotive manufacturers are leaders in advanced exterior and interior lighting design, including adaptive matrix LEDs and ambient color systems, requiring benchtop spectroradiometers for strict photometric and colorimetric quality assurance to meet European Union safety and quality directives. Additionally, the region hosts major optics and photonics companies that utilize these instruments for component testing and calibration services.

The market in Europe exhibits robust demand for spectroradiometers suitable for certifying compliance with international standards (CIE, ISO), placing a premium on traceability and robust calibration documentation. Germany, France, and the UK are key contributors, driven by precision engineering sectors and substantial academic research investment. While growth rates might be slightly lower than in APAC, the value of the market remains high due to the focus on premium, certified, and high-specification instrumentation.

LATAM and MEA currently represent smaller yet rapidly growing markets. Growth in these regions is primarily linked to infrastructure expansion, increased domestic manufacturing of consumer electronics components, and the development of solar energy farms. Countries such as Brazil, Mexico, and the UAE are investing heavily in establishing local research capabilities and adopting international quality standards for imported and domestically produced lighting and display components. The initial adoption wave is often driven by educational and government institutions setting up new metrology and quality testing centers.

The demand profile in these emerging regions often favors entry-to-mid-level benchtop spectroradiometers that offer a balance between affordability and acceptable accuracy, alongside comprehensive local technical support. As industrialization continues and regulatory environments mature, the transition to high-end, automated systems is expected to accelerate, presenting significant long-term growth opportunities for manufacturers capable of offering scalable solutions and strong regional service infrastructure.

Array-based spectroradiometers use a detector array (like CCD or CMOS) to measure all wavelengths simultaneously, prioritizing speed for high-volume quality control. Scanning spectroradiometers use a single detector and a moving grating to sequentially measure wavelengths, offering significantly higher spectral resolution and precision, making them ideal for critical research and calibration labs.

The highest market demand is driven by the Display Measurement application, specifically for quality control and characterization of advanced displays such as OLED, MicroLED, and HDR screens. Secondary drivers include the need for precise spectral characterization of high-efficiency LED lighting and research in photovoltaic solar energy efficiency.

AI technology enhances spectroradiometer utility by enabling predictive drift correction, automating complex spectral data analysis for defect detection, and optimizing measurement routines. This integration improves long-term accuracy, stability, and reduces the requirement for highly specialized manual data interpretation.

The high cost is attributed to the requirement for superior quality, specialized components, including high-end thermally stabilized detectors (often cooled), precision-machined optics, proprietary diffraction gratings to minimize stray light, and rigorous, traceable calibration procedures required for NIST/international standards compliance.

The Asia Pacific (APAC) region holds the largest market share, predominantly driven by the concentration of global manufacturing hubs for consumer electronics, display panels (South Korea, China), and LED components, necessitating high volumes of precise quality control instrumentation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.