ID : MRU_ 431816 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

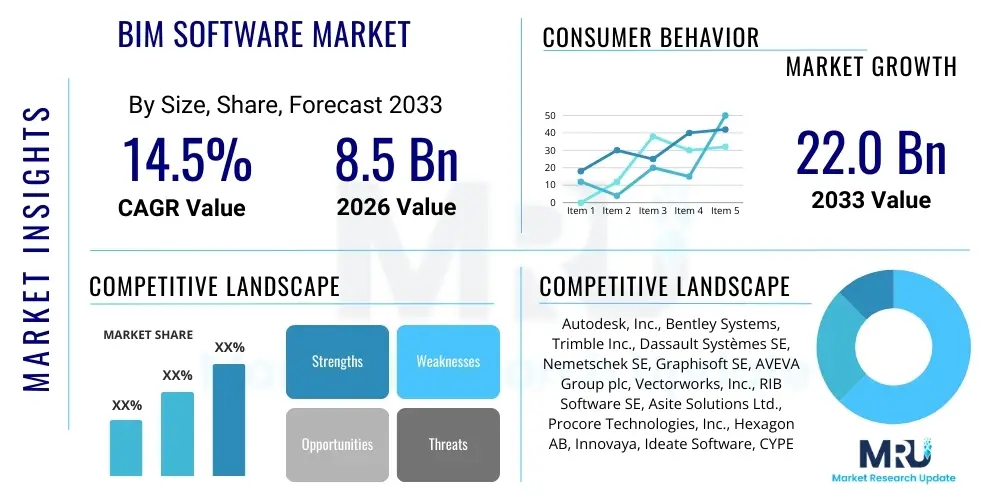

The BIM Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2026 and 2033. The market is estimated at USD 8.5 Billion in 2026 and is projected to reach USD 22.0 Billion by the end of the forecast period in 2033.

The Building Information Modeling (BIM) Software Market encompasses advanced digital tools and platforms that facilitate the creation and management of coordinated, consistent, and computable information about a construction project throughout its entire lifecycle, from design and documentation to construction and operation. BIM represents a fundamental shift from traditional 2D drafting to intelligent, 3D model-based processes, integrating geometric data, spatial relationships, geographical information, and quantities of components. This integrated approach allows all stakeholders—architects, engineers, contractors, and owners—to visualize, analyze, and simulate project performance and characteristics digitally before physical construction begins, significantly reducing errors, optimizing costs, and accelerating project delivery timelines. The core objective of BIM software is to enhance collaboration and decision-making by serving as a single source of truth for all project information.

Major applications of BIM software span across the entire Architecture, Engineering, and Construction (AEC) industry, including architectural design modeling, structural analysis, Mechanical, Electrical, and Plumbing (MEP) systems design, quantity takeoff, clash detection, facility management (FM), and energy performance analysis. The product range includes sophisticated desktop applications, increasingly shifting toward cloud-based collaborative platforms and specialized solutions catering to different phases of the construction process (e.g., 4D scheduling, 5D cost estimation, and 6D sustainability analysis). The adoption of BIM has been catalyzed by its demonstrated benefits, which include improved project quality, reduced rework, better risk management, and enhanced stakeholder communication, thereby contributing directly to higher productivity and profitability within the historically fragmented construction sector.

Driving factors for this market’s robust growth include increasingly stringent government mandates, particularly in developed regions like the UK, Germany, and Scandinavia, requiring the use of BIM Level 2 or higher for public sector projects. Furthermore, the global push toward sustainable construction and green building standards necessitates the detailed analysis capabilities provided by BIM tools, such as energy modeling and lifecycle assessment. The rapid digitalization of the global construction industry, driven by pressures to improve efficiency and manage complex urban infrastructure projects, coupled with advancements in computational power and software interoperability standards (like Industry Foundation Classes - IFC), continues to fuel the widespread deployment and integration of BIM solutions across diverse project scales and types, from residential buildings to complex industrial facilities.

The BIM Software Market is experiencing transformative growth, fundamentally driven by accelerating global construction digitalization and mandatory adoption policies imposed by various governmental bodies aiming for increased transparency and efficiency in public infrastructure spending. Current business trends indicate a significant shift from perpetual licensing models to subscription-based services and cloud deployment, which enhances accessibility, improves collaborative capabilities across geographically dispersed teams, and lowers the initial capital expenditure for smaller firms. Furthermore, there is intense focus on integrating BIM with other emerging technologies, such as Geographic Information Systems (GIS), Internet of Things (IoT) data for facility management, and Artificial Intelligence (AI) for generative design and automated clash detection. Key vendors are prioritizing the development of openBIM standards to improve data exchange and reduce dependency on proprietary file formats, thus fostering a more collaborative and competitive ecosystem.

Regionally, North America and Europe maintain market leadership, primarily due to high technological maturity, established regulatory frameworks promoting BIM adoption, and substantial investments in smart city infrastructure development. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period. This rapid expansion is attributable to massive urbanization projects, large-scale infrastructural initiatives in countries like China and India, and the growing recognition among local contractors and architectural firms of BIM's efficiency advantages in complex, time-sensitive projects. Latin America and the Middle East and Africa (MEA) are also showing promising acceleration, supported by large-scale oil and gas sector investments and diversification efforts aimed at establishing world-class construction standards and practices.

Segment trends reveal that the Architecture segment dominates the market in terms of revenue, driven by the foundational role of BIM in conceptual and detailed design phases. However, the Construction Management application segment is anticipated to witness the fastest growth, largely due to the increasing adoption of 4D (time) and 5D (cost) modeling capabilities that streamline on-site operations, logistics planning, and financial oversight. In terms of deployment, cloud-based BIM solutions are rapidly gaining traction over traditional on-premise installations, favored by their scalability, real-time collaboration features, and lower infrastructure maintenance requirements. This trend is particularly relevant for small and medium-sized enterprises (SMEs) seeking powerful tools without extensive IT overhead.

Common user inquiries regarding the impact of Artificial Intelligence (AI) on the BIM Software Market predominantly center on automation capabilities, efficiency gains, and the potential disruption to traditional design roles. Users frequently ask about AI's ability to automate repetitive tasks like drafting, component placement, and code compliance checking, seeking evidence of genuine productivity increases. Concerns often revolve around the security and proprietary nature of design data fed into AI models, the reliability of AI-generated designs, and the future necessity of human design expertise when generative AI tools mature. Expectations are high regarding AI’s potential in generative design, rapid optimization of structural and energy parameters, and enhanced predictive maintenance in the operational phase (6D BIM), moving the technology beyond mere modeling toward truly intelligent project management systems.

The integration of AI and machine learning (ML) within BIM platforms is fundamentally transforming the design and construction workflow by enabling computational capabilities far surpassing traditional deterministic algorithms. AI is being deployed for complex, data-intensive tasks such as optimizing building layouts based on regulatory constraints and performance metrics, performing instant clash detection across massive model sets, and predicting potential construction risks or cost overruns by analyzing historical project data. This shift allows architects and engineers to move away from mundane, iterative tasks, redirecting their expertise toward creative problem-solving and higher-value strategic planning. AI-driven solutions are thus democratizing advanced simulation and optimization techniques, making them accessible to a broader user base.

Furthermore, AI significantly enhances the lifecycle management aspects of BIM (6D and 7D). By analyzing sensor data collected from buildings post-occupancy (IoT data), ML algorithms can optimize energy usage, predict equipment failures before they occur, and automate maintenance scheduling, thereby increasing the operational longevity and efficiency of the built asset. This expansion into asset management validates BIM as a lifetime digital twin of a structure, dramatically increasing the value proposition of BIM software beyond the construction phase. However, standardization of training data and ensuring algorithmic transparency remain critical challenges for widespread AI adoption in highly regulated construction environments.

The BIM Software Market is characterized by robust growth drivers centered on regulatory support and efficiency demands, balanced by significant adoption restraints primarily related to high initial investment and the steep learning curve associated with complex software integration. Opportunities abound in the burgeoning fields of digital twin technology and modular construction, while the market's trajectory is profoundly influenced by the impact forces of technological advancements like AI and the standardization of open data protocols. The net impact of these forces is overwhelmingly positive, pushing the construction sector toward mandatory digital transformation, which inherently increases the demand for sophisticated BIM solutions capable of managing complex data flows and ensuring multi-party collaboration throughout the asset life cycle.

Key drivers fueling the market include mandatory BIM adoption policies across major global economies, which institutionalize the demand for compliant software. The inherent need for improved efficiency and waste reduction in the construction industry—known historically for low productivity—is a powerful economic driver, as BIM demonstrably reduces rework and shortens project timelines. Conversely, the market faces strong restraints, notably the high cost of implementation, including software licenses, specialized training, and necessary hardware upgrades, which particularly affects smaller and medium-sized enterprises (SMEs). A persistent lack of standardized, interoperable data exchange formats (despite advancements in IFC) and resistance to change among long-established industry professionals also slow the pace of complete market penetration.

Opportunities for exponential growth are concentrated in the integration of BIM with emerging technologies to create comprehensive digital twins for operations and maintenance (O&M), extending the software's utility far beyond the construction phase. The rise of industrialized construction methods, such as prefabrication and modular construction, also provides a fertile ground for BIM, which is essential for precise coordination and manufacturing tolerances. The primary impact forces defining the market landscape are continuous advancements in cloud computing, enabling real-time, global collaboration, and the aggressive integration of Artificial Intelligence for design automation and predictive analytics. These forces compel industry players to continually update their technological stack and adopt comprehensive, integrated project delivery methodologies.

The BIM Software Market is primarily segmented based on the component (Software and Services), deployment type (On-premise and Cloud-based), application (Architecture, Structural Engineering, MEP Engineering, Construction Management), and end-user (Architects, Engineers, Contractors, Owners). This detailed segmentation reflects the diversity of specialized tools and solutions required across the complex and multi-disciplinary construction value chain. The services segment, encompassing consulting, training, implementation, and maintenance, is growing rapidly as organizations require specialized support to fully transition their workflows and maximize the return on investment from their BIM technology stack, mitigating the steep learning curve associated with advanced modeling.

The application-based segmentation highlights which phase of the project lifecycle drives the highest software expenditure. While architectural design typically initiates the BIM process, subsequent applications such as structural analysis and especially construction management are demonstrating accelerated growth rates. The shift towards cloud-based deployment is the most significant observable trend, driven by the necessity for real-time collaboration among distributed project teams and the attractive flexibility of subscription licensing models, which offer lower barriers to entry compared to traditional heavy on-premise solutions requiring substantial local IT infrastructure and maintenance costs.

End-user segmentation clearly indicates that architects and engineers remain the foundational consumers, utilizing BIM for core design and documentation tasks. However, contractors and owners/developers are increasingly adopting BIM tools for operational benefits, leveraging 4D, 5D, and 6D capabilities for enhanced scheduling, cost control, and eventual facility management. This broadening user base signifies the market's maturation from a purely design tool to an essential platform for comprehensive project and asset lifecycle management across the entire AEC ecosystem, requiring vendors to develop specialized modules and user interfaces tailored to these diverse professional needs.

The value chain for the BIM Software Market begins with upstream activities dominated by core research and development, involving deep expertise in computational geometry, data management, and architectural/engineering standards. Software vendors invest heavily in developing sophisticated modeling kernels, ensuring interoperability (often via IFC standards), and integrating cutting-edge features like AI and cloud functionality. This stage requires high technical skills and significant intellectual property investment, leading to consolidation among a few major providers who own the most robust proprietary modeling technologies. The transition to cloud-native platforms has also introduced new upstream partners focused on robust, scalable hosting infrastructure and security protocols necessary for handling large, sensitive project models.

The core midstream activity involves software distribution and implementation. Distribution channels are varied, including direct sales from major vendors to large enterprise clients, specialized value-added resellers (VARs) who provide localized sales and technical support, and the burgeoning online subscription models. The implementation phase is crucial; services providers and consultants play an essential role in customizing the software to specific project delivery methods (like Integrated Project Delivery - IPD) and integrating BIM workflows with existing enterprise systems such as Enterprise Resource Planning (ERP) and project scheduling tools. Direct channels are increasingly preferred by large corporate clients for dedicated support and custom licensing agreements, while indirect channels through VARs remain vital for penetrating SME markets globally.

Downstream activities focus on the end-user application and continuous support. This includes training services to ensure user proficiency, technical support for model-specific issues, and continuous software updates driven by evolving industry regulations and technology standards. The ultimate consumers—the AEC professionals—utilize the software to deliver built assets. Furthermore, the downstream extends into the operational phase, where specialized facility management software utilizes the BIM data (6D and 7D) created during design and construction. This lifecycle approach generates long-term recurring revenue for vendors through maintenance contracts and specialized operational software licenses, cementing BIM's role as a strategic asset management tool rather than just a temporary construction aid.

The primary customers for BIM software are organizations and professionals operating within the global Architecture, Engineering, and Construction (AEC) industry who are committed to modernizing their project delivery methods and improving asset management efficiency. This includes large multinational construction conglomerates and specialized sub-contractors focused on specific trades (e.g., steel fabrication, HVAC installation). Architects and structural engineers form the initial and most consistent buyer segment, relying on BIM for conceptual design, detailed documentation, and sophisticated analysis required for permitting and fabrication. Their demand is centered on advanced modeling, visualization, and interoperability capabilities to seamlessly exchange data with other consultants.

A rapidly growing segment of potential customers includes large institutional owners and public sector bodies (e.g., government agencies managing public infrastructure, healthcare systems, university campuses). These owners are increasingly recognizing the long-term cost benefits of utilizing BIM data for facility management (FM), energy optimization, and capital renewal planning throughout the building's operational lifespan. Their purchasing decisions are often driven by the desire for lifecycle cost reduction (Total Cost of Ownership) and the need for a comprehensive digital record (Digital Twin) of their physical assets. Mandates for BIM usage on public projects are specifically aimed at driving adoption among these key owner groups, making compliance a strong purchasing driver.

Another crucial customer segment encompasses contractors and construction managers. Historically slower to adopt, this group now seeks BIM tools, specifically 4D (scheduling) and 5D (cost) applications, to enhance on-site execution, logistics planning, materials procurement, and progress monitoring. They are demanding mobile BIM solutions that can be used directly on the construction site for real-time model access and clash resolution. Furthermore, specialists involved in off-site construction, such as manufacturers of prefabricated components and modular building systems, are high-value customers, as their precision-driven workflows are entirely dependent on highly accurate and detailed BIM models to achieve manufacturing tolerances and efficient assembly.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 22.0 Billion |

| Growth Rate | 14.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Autodesk, Inc., Bentley Systems, Trimble Inc., Dassault Systèmes SE, Nemetschek SE, Graphisoft SE, AVEVA Group plc, Vectorworks, Inc., RIB Software SE, Asite Solutions Ltd., Procore Technologies, Inc., Hexagon AB, Innovaya, Ideate Software, CYPE Ingenieros, S.A., ESRI, Vianova Systems AS (now part of Trimble), FARO Technologies, Inc., ACCA software S.p.A., Tekla (now part of Trimble) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the BIM Software Market is rapidly evolving, moving beyond traditional desktop modeling towards highly integrated, data-centric, and cloud-native environments. A core technology shaping this evolution is the utilization of Common Data Environments (CDEs), which provide a central, standardized repository for all project information, ensuring that every stakeholder is working with the latest validated data and significantly improving workflow efficiency and reducing coordination errors. Furthermore, the reliance on open standards, particularly Industry Foundation Classes (IFC) and Building Collaboration Format (BCF), is paramount. These standards facilitate true interoperability, allowing diverse software solutions from different vendors to exchange model data seamlessly, addressing the long-standing challenge of proprietary data silos within the AEC industry.

Advanced reality capture technologies are becoming intrinsic to the BIM workflow, bridging the gap between the physical construction environment and the digital model. This includes the integration of high-definition laser scanning (Lidar), photogrammetry, and drone mapping, which rapidly generate accurate point clouds or mesh models of existing conditions or ongoing construction progress. These reality models are then directly imported into BIM software to create "as-built" models or to perform variance analysis against the "as-designed" model, supporting quality assurance and progress monitoring efforts. This integration underscores the market's focus on maintaining digital accuracy throughout the project lifecycle, ensuring the BIM model remains a reliable digital twin.

Beyond data capture and management, the incorporation of advanced computational tools like Generative Design and machine learning is defining the next generation of BIM software. Generative design uses algorithms to explore thousands of design solutions based on user-defined constraints (e.g., material cost, structural load, daylight penetration), allowing designers to find optimized solutions much faster than manual iteration. Furthermore, the adoption of web-based visualization engines (WebGL) allows for the viewing and manipulation of massive 3D and 4D models directly within standard web browsers and mobile devices, democratizing access to complex BIM data and facilitating real-time collaboration even on-site. These technological advancements emphasize mobility, computational power, and collaborative access as the core pillars of modern BIM tools.

The BIM Software Market exhibits distinct maturity levels and growth trajectories across different geographical regions, largely influenced by local governmental mandates, construction market size, and technological adoption rates. North America stands as a mature and leading market, driven by high technological literacy, extensive private sector adoption, and significant investment in large-scale commercial and infrastructure projects. The United States and Canada are pivotal, with widespread acceptance among large AEC firms and a strong focus on utilizing BIM for Integrated Project Delivery (IPD) and lifecycle asset management, often spurred by proprietary standards set by major institutional owners.

Europe represents another cornerstone of the global market, particularly characterized by strong governmental intervention. Countries such as the UK, Germany, and Scandinavian nations have implemented stringent, often mandatory, BIM requirements for public projects, which significantly accelerated market penetration and established advanced standards for information management (e.g., ISO 19650). This regulatory environment has fostered a mature ecosystem with a strong focus on openBIM standards and collaboration across the supply chain, positioning Europe as a key incubator for sustainable and standardized BIM practices.

The Asia Pacific (APAC) region is forecasted to be the fastest-growing market globally, buoyed by unprecedented urbanization and massive infrastructure investments, particularly in China, India, and Southeast Asia. While the region’s maturity in BIM adoption varies, the sheer scale of ongoing and planned projects necessitates efficiency gains only achievable through digital methodologies. Governments in APAC are increasingly recognizing the strategic importance of BIM for managing rapid, complex construction, leading to growing mandates and substantial foreign investment in local digitalization initiatives. The Middle East and Africa (MEA), especially the GCC states, are also witnessing accelerating growth, driven by ambitious mega-projects and smart city developments that inherently require advanced BIM and Digital Twin technologies from conception.

The BIM Software Market is projected to experience a robust Compound Annual Growth Rate (CAGR) of 14.5% during the forecast period from 2026 to 2033, driven primarily by mandatory digitalization across global construction sectors.

Cloud-based BIM solutions facilitate real-time, remote collaboration and utilize subscription models, reducing initial IT costs, whereas on-premise requires local infrastructure and capital expenditure. Cloud deployment is increasingly dominating due to enhanced scalability and ease of access for distributed project teams.

The Asia Pacific (APAC) region is anticipated to exhibit the fastest market growth rate, fueled by massive government investments in infrastructure, rapid urbanization, and growing adoption of digital construction methods in key markets like China and India.

AI's primary role is to automate high-complexity tasks, including generative design optimization, instantaneous clash detection, and predictive analytics for project scheduling (4D) and cost management (5D), significantly enhancing design efficiency and risk mitigation.

The most critical applications driving current demand are Construction Management (4D/5D modeling for scheduling and cost) and Facility Management (6D/7D BIM) for long-term asset operation, maintenance, and energy efficiency optimization.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.