ID : MRU_ 436726 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

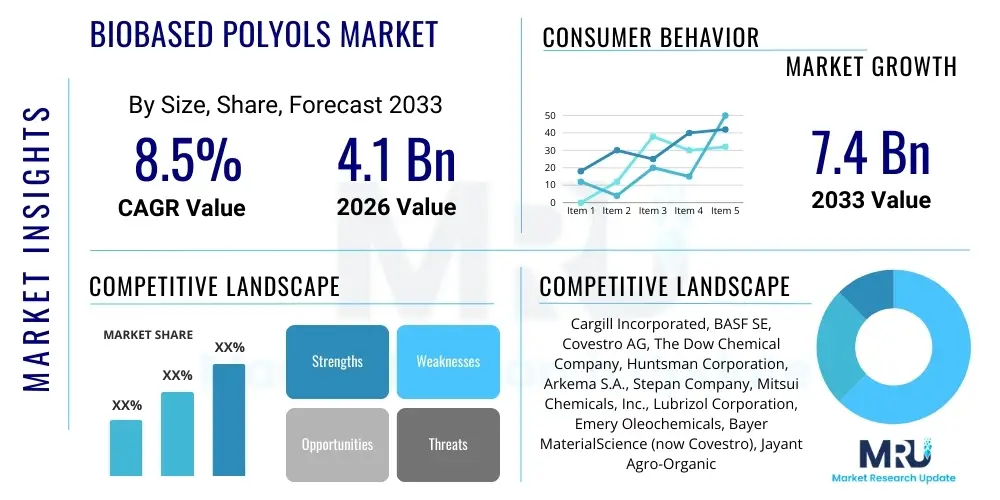

The Biobased Polyols Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.1 Billion in 2026 and is projected to reach USD 7.4 Billion by the end of the forecast period in 2033. This robust expansion is fundamentally driven by the escalating global demand for sustainable chemical solutions and the increasing regulatory pressure across developed economies to reduce reliance on petrochemical-derived materials. Biobased polyols offer a viable, environmentally conscious alternative, directly supporting corporate sustainability goals and circular economy initiatives across crucial downstream industries.

The valuation reflects significant investment in advanced manufacturing techniques and the diversification of feedstock sources beyond traditional vegetable oils (such as soy and castor). Emerging technologies, including microbial fermentation and enzymatic catalysis, are enhancing product performance parity with conventional polyols, thereby overcoming historical barriers related to application-specific properties like viscosity, functionality, and hydrolytic stability. This technological maturation is key to unlocking high-volume adoption in demanding segments such as automotive components, high-performance coatings, and rigid insulation foams.

Geographically, market expansion is particularly pronounced in regions implementing stringent environmental legislation, notably Western Europe and North America. However, the Asia Pacific region is rapidly gaining traction, propelled by massive industrialization and the establishment of large-scale production facilities catering to the burgeoning construction and packaging sectors. The inherent volatility in fossil fuel pricing further bolsters the economic competitiveness of biobased alternatives, providing a more stable raw material cost structure over the long term, which is crucial for market penetration and sustained growth across diverse industrial applications.

Biobased polyols are polymeric compounds derived wholly or partially from renewable biological resources, such as agricultural crops, algae, waste oils, and forestry residues, designed to replace traditional petroleum-based polyols. These sustainable alternatives typically function as key building blocks in the production of polyurethanes (PUs), which are essential components in foams, elastomers, coatings, adhesives, and sealants (CASE applications). The primary benefit of integrating biobased polyols lies in lowering the carbon footprint of the final products, contributing substantially to resource efficiency and biodegradability potential, aligning with global commitments to climate change mitigation.

The product description encompasses a wide chemical range, including polyether polyols, polyester polyols, and specialty polyols, all engineered to maintain or surpass the performance specifications required by high-performance applications. Major applications span several sectors: rigid foam for construction insulation and refrigeration, flexible foam for furniture and bedding, elastomers for automotive parts and footwear, and specialized coatings for marine and industrial protection. The versatility and customization potential of biobased polyols, driven by innovative chemical modification routes like epoxidation, ozonolysis, and transesterification, ensure their suitability across highly demanding environments.

Driving factors for this market are multifaceted, anchored primarily by environmental regulations—such as REACH in Europe and similar mandates globally—and increasing consumer preference for sustainable products. Furthermore, the push for material lightweighting in the automotive and aerospace industries, coupled with the superior insulation properties of biobased rigid foams, amplifies market adoption. The continuous development of cost-effective conversion technologies that utilize non-food competitive feedstocks, such as industrial waste streams and lignocellulosic biomass, is critical for scaling production and achieving price competitiveness against conventional petrochemical incumbents.

The Biobased Polyols Market is characterized by robust commercial growth fueled by synergistic factors, including stricter environmental mandates and accelerated material science innovations focused on renewable chemistry. Key business trends indicate a strong move toward strategic collaborations, vertical integration within the supply chain, and increased capacity expansion by large chemical producers who are aggressively diversifying their portfolios away from fossil fuels. The prevailing trend suggests that achieving functional equivalence or superiority in performance remains the core focus, particularly concerning thermal stability, mechanical strength, and fire resistance required in high-end applications like automotive interiors and wind turbine blades, driving significant R&D investment.

Regionally, Europe maintains its leadership position, propelled by comprehensive regulatory frameworks such as the European Green Deal and mandatory sustainability reporting, which create a definitive market advantage for biobased products. North America follows closely, driven by government incentives, bio-refinery investments, and the significant presence of major PU producers. Meanwhile, the Asia Pacific region, led by China and India, is emerging as the fastest-growing market, shifting from primarily consumption to large-scale production, leveraging vast agricultural resources and rapidly expanding construction and manufacturing sectors that require sustainable material inputs for mass production and export compliance.

Segment trends highlight the dominance of the Polyether Polyol segment due to its versatility and established use in flexible foams, while the Polyester Polyol segment is witnessing rapid growth, particularly in the coatings and adhesives sectors, valued for enhanced durability and chemical resistance. Feedstock segmentation shows that vegetable oil-based polyols, derived from soy, castor, and rapeseed, currently hold the largest share. However, polyols derived from non-edible biomass and algae are projected to demonstrate the highest growth trajectory, signaling a strategic shift toward second and third-generation feedstocks to mitigate food-versus-fuel debates and enhance overall sustainability credentials, thereby reinforcing long-term market viability.

User queries regarding the impact of Artificial Intelligence (AI) on the Biobased Polyols Market frequently center on themes of optimizing complex biochemical synthesis pathways, predicting feedstock quality and availability, and accelerating the discovery of novel enzyme catalysts. Users are keenly interested in how machine learning can shorten the R&D cycle for formulating biobased polyols with specific performance characteristics (e.g., tailored hydroxyl values or molecular weights) that currently require extensive, time-consuming lab experimentation. Furthermore, there is significant interest in leveraging predictive modeling for enhancing production efficiency, managing supply chain volatility associated with agricultural commodities, and ensuring consistent product quality across various batches and seasonal feedstock variations, thereby addressing key commercialization challenges. AI serves as a transformative tool that enhances efficiency, accelerates innovation, and minimizes waste in the transition toward bio-based chemical manufacturing.

The market dynamics of biobased polyols are powerfully shaped by a balance of strong environmental drivers, persistent economic challenges, and significant technological opportunities. The primary driver is the global mandate for sustainable chemistry, pushing corporations to replace petrochemicals to meet Scope 3 emission targets, simultaneously creating opportunities for innovation in non-food competitive feedstock utilization. However, the market faces restraints, chiefly the higher initial cost of production relative to established conventional polyols and the variability in the quality and supply of natural raw materials, requiring complex purification and standardization processes.

Impact forces acting upon the market include increasing governmental support through subsidies and tax incentives for bio-refineries, which substantially lower capital expenditure barriers. Conversely, the intense competition from large petrochemical conglomerates who are beginning to offer hybrid or partially bio-based solutions acts as a competitive restraint. Opportunities are vast in developing specialized, high-margin applications where performance requirements justify a price premium, such as aerospace composites and medical devices, alongside capitalizing on the immense market potential in developing nations seeking sustainable infrastructure solutions.

The market’s future trajectory is heavily dependent on achieving price parity through economies of scale and continuous technological improvements that streamline conversion efficiency. Successfully leveraging low-cost, second-generation feedstocks (like cellulosic materials) and employing advanced catalytic systems represent critical opportunities. Addressing the restraint of performance variability by implementing robust quality control standards and establishing globally harmonized certifications will be essential for securing widespread adoption in performance-critical industrial applications, thus minimizing perceived risk among major end-users.

The Biobased Polyols Market is extensively segmented across multiple dimensions, including product type, application, feedstock, and end-user industry, reflecting the diverse chemical compositions and end-use requirements of these sustainable materials. Understanding these segments is crucial for strategic market positioning, as each category presents unique growth rates, technological maturity, and competitive landscapes. Product type segmentation distinguishes between polyethers, polyesters, and specialty variants based on their chemical backbone and performance properties, while application segmentation reveals the primary areas of consumption, dominated by the polyurethane rigid and flexible foam industries, which are the largest volume users.

The value chain for the Biobased Polyols Market begins with the upstream sourcing and processing of renewable feedstocks, which involves agricultural production (soy, rapeseed), forestry operations, or specialized microbial cultivation (algae, bacteria). This upstream analysis necessitates robust logistics and purification steps to ensure feedstock quality and consistent supply to the bio-refining facilities. Key activities here include crop harvesting, oil extraction, and initial pre-treatment processes such as transesterification or epoxidation, which transform crude biological materials into suitable chemical intermediates, demonstrating the strong link between agricultural economics and chemical manufacturing.

The midstream phase involves the core chemical conversion of these intermediates into finished biobased polyols using various technological pathways, including high-pressure chemical modification, enzymatic reactions, or complex fermentation processes. This stage is characterized by high capital investment in processing plants and significant intellectual property related to proprietary catalysts and synthesis routes. Distribution channels for biobased polyols are critical, primarily relying on indirect sales through specialized chemical distributors who provide inventory management and technical support to numerous small and medium-sized manufacturers, though large volume transactions often occur directly to major polyurethane system houses.

The downstream analysis focuses on the integration of these polyols into final products, predominantly polyurethane systems, which are consumed by end-user industries such as construction (rigid insulation), automotive (seating and components), and consumer goods (footwear and bedding). Direct customers are the system house formulators and large manufacturers who blend the polyols with isocyanates and additives. The successful adoption at this stage is highly dependent on technical service, performance guarantees, and certifications confirming the material's bio-content and sustainable sourcing credentials, emphasizing the role of certification bodies in validating the final product's value proposition.

The primary consumers and end-users of biobased polyols are large-scale manufacturers and specialized system formulators operating within industries that heavily rely on polyurethane derivatives for their product composition and functional requirements. These customers are typically motivated by dual objectives: achieving competitive performance in their final products while meeting increasingly strict environmental, social, and governance (ESG) targets set by regulators and corporate stakeholders. Key end-users include multinational automotive manufacturers seeking to lightweight vehicles and incorporate sustainable interior components, major construction companies requiring high-efficiency, low-carbon footprint insulation materials, and large furniture and bedding producers focused on non-toxic, sustainable foams.

Specifically, polyurethane system houses represent a crucial segment of potential customers, as they act as intermediaries who formulate customized polyurethane systems (including polyol blends, isocyanates, and additives) tailored to the specific needs of their clientele, such as appliance manufacturers or coating applicators. Other significant buyers include producers of adhesives, sealants, and specialty elastomers (CASE), particularly those targeting regulated industries or specialized high-performance applications like flexible packaging and industrial flooring where bio-content provides a distinct market advantage. The purchase decision is often influenced not just by price and performance, but heavily by the verifiable sustainability certifications and guaranteed supply reliability of the biobased raw material supplier.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 7.4 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cargill Incorporated, BASF SE, Covestro AG, The Dow Chemical Company, Huntsman Corporation, Arkema S.A., Stepan Company, Mitsui Chemicals, Inc., Lubrizol Corporation, Emery Oleochemicals, Bayer MaterialScience (now Covestro), Jayant Agro-Organics, Global Bio-Chem Technology Group, PTT Global Chemical, Italmatch Chemicals, Bio-Pur Technology, Ecopol S.A., Allessa GmbH, Vertellus Holdings LLC, TCI Chemicals. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Biobased Polyols Market is highly dynamic, driven by the imperative to achieve cost-competitive and high-performance products from renewable sources. The primary established technologies revolve around chemical modification, such as the epoxidation and subsequent ring-opening of vegetable oils (e.g., soybean and castor oil), which is a mature and scalable process for producing foundational biobased polyols. However, significant R&D focus is now shifting toward optimizing catalyst systems, specifically employing enzymatic catalysis and novel heterogeneous catalysts that operate under milder conditions, reducing energy consumption and minimizing unwanted side product formation, thereby increasing sustainability and yield efficiency.

A burgeoning technological area involves the use of biotechnology, specifically microbial fermentation and metabolic engineering, to produce polyol precursors or even the final polyol structures using engineered microorganisms (e.g., yeast or bacteria) fed with simple sugars or lignocellulosic hydrolysates. This route, often termed 'white biotechnology,' holds immense promise for accessing novel, highly functionalized polyols that are difficult or impossible to synthesize through conventional petrochemical methods. Technologies like directed evolution and synthetic biology are being leveraged to optimize these biological pathways, enabling the use of inexpensive, non-food competitive feedstocks and offering unparalleled control over the molecular architecture of the resulting polymers.

Furthermore, technologies dedicated to utilizing waste streams, such as waste cooking oil (WCO) and used plastics (chemical recycling to monomers), are gaining traction, serving the circular economy model. Novel depolymerization and chemical recycling techniques allow for the recovery of bio-derived monomers, which are then repolymerized into polyols, effectively closing the loop on material use. The convergence of chemical engineering, advanced catalysis, and industrial biotechnology defines the competitive edge in this market, with companies investing heavily in continuous flow processes and modular manufacturing to achieve flexible, high-capacity, and economically viable production lines, critical for meeting mainstream industrial demand and ensuring rapid scalability.

Biobased polyols are derived from renewable biological resources such as vegetable oils or biomass, whereas petrochemical polyols are sourced from non-renewable crude oil derivatives. Biobased options offer a significantly reduced carbon footprint and enhanced sustainability profile, making them crucial for meeting green manufacturing targets.

While the initial cost of biobased polyols can be higher due to complex conversion processes and feedstock purification, economies of scale, technological advancements in catalysis, and stability in raw material costs relative to volatile fossil fuel markets are steadily closing the price gap, enhancing competitiveness over the long term.

The Construction and Infrastructure sector, particularly the demand for rigid polyurethane foam insulation, represents the highest volume application. This is driven by strict energy efficiency standards globally, mandating superior insulation properties that biobased rigid foams can efficiently provide while reducing the environmental impact of building materials.

Key technical challenges include ensuring performance parity—specifically maintaining hydrolytic stability, achieving necessary molecular functionality (hydroxyl value), and ensuring viscosity characteristics are compatible with high-speed manufacturing processes—and securing a consistent supply of standardized, high-quality, non-food competitive feedstock.

Regulatory policies, particularly in Europe (e.g., Green Deal, REACH) and North America (incentives for sustainable chemical production), are fundamentally accelerating market expansion by setting mandatory targets for bio-content, reducing hazardous substance use, and imposing carbon pricing, thereby creating a strong economic incentive for manufacturers to switch from fossil-based to biobased alternatives.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.