ID : MRU_ 439131 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

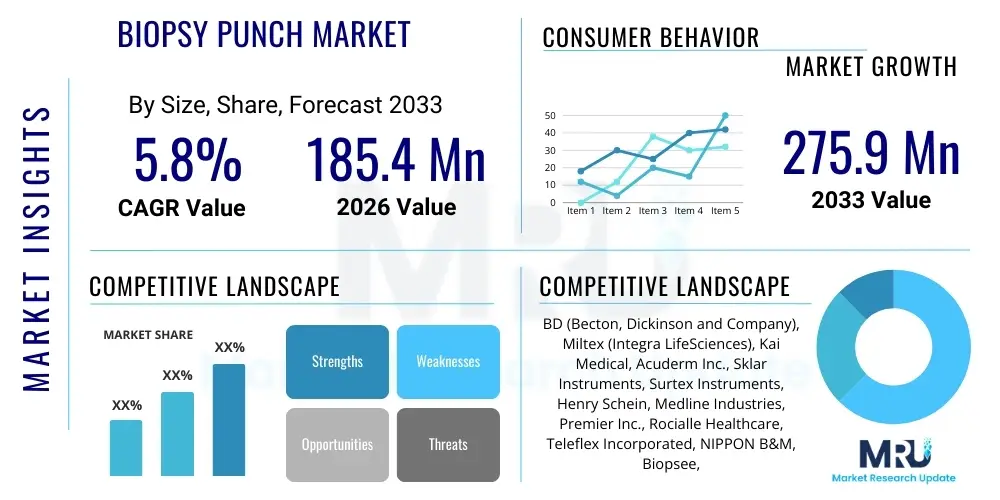

The Biopsy Punch Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 185.4 million in 2026 and is projected to reach USD 275.9 million by the end of the forecast period in 2033.

The Biopsy Punch Market encompasses the global trade and utilization of specialized medical devices designed to excise small, cylindrical tissue samples (biopsies) for diagnostic examination. These devices are critical tools in numerous medical disciplines, particularly dermatology, oncology, and forensic pathology, providing tissue specimens essential for accurate disease diagnosis, grading, and monitoring. Biopsy punches are typically characterized by a sharp, circular cutting tip attached to a handle, allowing for minimally invasive tissue acquisition. The market's growth trajectory is strongly influenced by the rising global incidence of skin cancers, infectious diseases requiring dermatological confirmation, and the increasing demand for precise, less painful diagnostic procedures.

Product variation within the market is substantial, catering to diverse medical requirements. Key product categories include disposable and reusable punches, available in a wide range of diameters (e.g., 1mm to 8mm), and specialized types like FUE (Follicular Unit Extraction) punches used extensively in hair transplantation procedures. The primary applications span diagnostic procedures for melanoma and basal cell carcinoma, sampling of autoimmune diseases, and research applications in cellular pathology. Technological advancements are focusing on enhancing ergonomic design, minimizing patient discomfort, and ensuring consistent sample quality through precision engineering and standardized sizing.

The market is primarily driven by demographic shifts, specifically the aging global population which experiences higher rates of skin malignancies, coupled with heightened awareness regarding early detection of dermatological and subcutaneous conditions. Furthermore, enhanced healthcare infrastructure in emerging economies and increased investment in diagnostic capabilities in both hospital and ambulatory settings are crucial factors bolstering market expansion. The inherent benefit of biopsy punches—their simplicity, cost-effectiveness, and speed in acquiring diagnostic samples—solidifies their indispensable role in modern clinical practice, contributing significantly to positive clinical outcomes through rapid diagnosis.

The Biopsy Punch Market is currently characterized by robust business trends emphasizing the shift towards high-quality disposable instruments to mitigate cross-contamination risks and streamline inventory management in high-volume settings. Key market players are concentrating on developing punches with integrated protective features, improved sharpness retention, and ergonomic handles to enhance user comfort and procedural accuracy. The primary competitive strategies involve strategic mergers, acquisitions, and collaborations focused on expanding geographic reach and integrating complementary diagnostic tools. Furthermore, sustainable manufacturing practices and biodegradable materials are gaining traction, driven by increasing regulatory scrutiny and institutional demands for environmentally conscious medical devices, representing a significant trend impacting product development and supply chain dynamics.

Regionally, North America maintains the largest market share, attributable to high healthcare expenditure, sophisticated diagnostic infrastructure, and a significantly high prevalence of skin cancer requiring regular biopsy procedures. However, the Asia Pacific (APAC) region is poised for the fastest growth, propelled by rapidly improving access to specialized medical care, significant government investment in public health systems, and a burgeoning medical tourism sector demanding high-standard diagnostic tools. European markets demonstrate steady growth, primarily focused on incorporating punches specialized for trichological and aesthetic applications, aligning with strong regional demands for cosmetic procedures.

In terms of segment trends, the disposable segment dominates the market due to stringent infection control protocols enforced globally. The Dermatology application segment commands the largest revenue share, reflecting the widespread use of punches in skin lesion assessment. Concurrently, the Ambulatory Surgical Centers (ASCs) end-user segment is exhibiting faster growth compared to traditional hospitals, driven by the increasing shift of minor surgical and diagnostic procedures to outpatient settings, which favor the quick, reliable sample acquisition offered by biopsy punches. The development of automated and motorized punches is a nascent segment trend, promising greater precision and reduced manual effort for high-throughput laboratory environments.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Biopsy Punch Market frequently revolve around two primary themes: the potential for AI to optimize the diagnostic workflow post-biopsy, and whether AI imaging could eventually reduce the necessity for physical biopsy sampling. Key concerns include the integration of digital pathology systems, where AI algorithms analyze the tissue sample obtained via the punch for accelerated diagnosis, potentially detecting subtle malignant features faster than human review. Users are highly interested in how AI-driven predictive analytics, based on clinical imaging, might triage patients more effectively, thereby optimizing the utilization of biopsy procedures rather than completely replacing the physical sampling step. While AI is unlikely to replace the need for the physical tissue sample acquired by the punch, it will dramatically transform the downstream analysis, enhancing efficiency, accuracy, and standardization of the pathology reports, thus increasing the value proposition of the well-executed biopsy procedure.

The Biopsy Punch Market is influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), shaping its market trajectory. The primary drivers include the escalating global prevalence of chronic dermatological conditions and various cancers (particularly melanoma), requiring definitive histological confirmation. Coupled with this is the continuous improvement in healthcare access globally, leading to higher rates of screening and diagnostic procedures. The ease of use, minimal invasiveness, and cost-effectiveness of biopsy punches compared to excisional surgeries solidify their position as the preferred diagnostic tool in primary and secondary care settings. These factors create strong upward pressure on market volume and revenue growth across developed and developing regions, fostering stable demand across clinical and research environments.

Restraints, conversely, include the risks associated with improper sample handling or insufficient tissue acquisition, which can lead to false negative results or the need for repeat procedures, thereby increasing healthcare costs and patient burden. Furthermore, the availability of alternative, non-invasive diagnostic techniques, while still limited in scope for definitive diagnosis, poses a potential long-term threat. Regulatory hurdles pertaining to single-use medical device disposal and environmental concerns also impose limitations on manufacturers, necessitating investment in compliant and sustainable materials, adding complexity to the production process and potentially increasing unit costs.

Opportunities for growth are predominantly centered around product innovation, specifically the development of specialized punches for niche applications such as hair restoration (FUE punches) and veterinary diagnostics. The expansion into developing economies, particularly in APAC and Latin America, represents a significant untapped market opportunity, driven by improving economic conditions and increased spending on healthcare infrastructure. Moreover, strategic partnerships aimed at integrating biopsy procedures with advanced diagnostic imaging and molecular testing services present substantial avenues for market expansion and value addition, ensuring the biopsy punch remains relevant in an increasingly sophisticated diagnostic landscape. The dominant impact force driving the market is the imperative for early and accurate disease diagnosis, which universally mandates tissue sampling.

The Biopsy Punch Market is comprehensively segmented based on Type, Material, Application, and End-User, providing granular insights into demand patterns and competitive landscapes. Segmentation by Type, including disposable and reusable punches, is crucial for understanding institutional purchasing preferences influenced by cost and infection control mandates. The disposable segment maintains dominance globally due to stringent hygienic requirements and ease of use. Analyzing the market through the lens of Application, particularly Dermatology and Oncology, reveals the primary revenue streams and areas necessitating targeted product innovation, such as specialized ergonomic designs for high-volume dermatological clinics.

Further segmentation by Material (e.g., stainless steel, plastic) helps identify trends in durability, cost, and disposal strategies, directly influencing manufacturing processes and supply chain choices. Stainless steel remains the standard for reusable and high-precision disposable punches due to its sharpness and rigidity, while plastic components contribute to the growing popularity of fully disposable, low-cost options. The End-User segmentation, focusing on Hospitals, Ambulatory Surgical Centers (ASCs), and Diagnostic Labs, highlights the shift in procedural venues. ASCs are rapidly increasing their share due to cost efficiency and patient convenience for minor diagnostic surgeries, demanding bulk quantities of high-quality, standardized disposable punches for immediate use.

The Value Chain for the Biopsy Punch Market starts with upstream analysis, focusing on raw material procurement, primarily high-grade stainless steel for the cutting tip and medical-grade polymers for the handles and protective sheaths. Key considerations at this stage include supplier selection based on quality consistency, cost efficiency, and adherence to ISO standards for medical device materials. Manufacturing involves precision engineering, sterile assembly, and stringent quality checks, particularly for ensuring the sharpness and structural integrity of the punch tips. Effective upstream management is critical as it directly influences the final product quality, which is paramount in obtaining optimal tissue samples free from artifacts.

Midstream activities include packaging, sterilization (often using ethylene oxide or gamma radiation), and inventory management. The distribution channel analysis is multifaceted, involving both direct and indirect sales strategies. Direct sales are typically preferred for large hospital groups or high-volume ASC chains, allowing manufacturers to maintain better control over pricing and customer relationship management. Indirect sales rely heavily on specialized medical device distributors and wholesalers who possess established networks within regional clinics and smaller diagnostic laboratories. These distributors provide essential services such as logistics, local regulatory adherence, and inventory maintenance, making them critical partners for market penetration, particularly in fragmented international markets.

Downstream analysis centers on the end-users—hospitals, clinics, and diagnostic labs—where the punches are utilized. Post-sales service is crucial, especially for reusable instruments requiring sharpening or repair, although the market trend leans heavily toward disposable products, shifting the focus to seamless supply and easy replenishment. Potential customers are heavily influenced by clinical efficacy, pricing, and the reputation of the manufacturer for reliable and sterile products. The efficiency of the distribution system, ensuring products are available just-in-time, directly impacts clinical operations and purchasing decisions, demonstrating the pivotal role of robust logistics in maintaining market share.

The primary end-users and buyers of biopsy punches are professional medical facilities and personnel who require definitive tissue diagnosis for patient care and research. Hospitals, encompassing large public facilities and private specialized institutions, represent the largest customer base. Within hospitals, dermatology departments, surgical oncology units, and pathology laboratories are the heaviest consumers, purchasing both standardized bulk quantities of disposable punches and specialized reusable sets. Purchasing decisions in this segment are often centralized and highly sensitive to regulatory compliance, bulk pricing, and demonstrable product reliability and sterility, driving strong demand for detailed product documentation and clinical validation.

Ambulatory Surgical Centers (ASCs) constitute a rapidly expanding customer segment. As increasing numbers of dermatological, minor cosmetic, and diagnostic procedures shift away from inpatient settings, ASCs require high-volume, cost-effective disposable punches for rapid patient throughput. Their purchasing behavior emphasizes convenience, sterile packaging, and minimized storage requirements. Furthermore, independent diagnostic laboratories and pathology centers are key buyers, as they process samples sent from various clinical settings. These customers focus on products that ensure high-quality sample integrity to minimize processing artifacts and enhance diagnostic accuracy, thereby favoring punches known for optimal sharpness and consistent sample depth.

Finally, the customer base extends to specialized research and academic institutions, including universities and pharmaceutical companies engaged in clinical trials or fundamental pathology research. This segment requires a diverse range of punch sizes and often demands specialized, high-precision products for microscopic analysis or niche tissue sampling. Veterinary clinics, particularly those specializing in advanced pet care and dermatopathology, also represent a significant, though smaller, niche customer segment. These diverse customer needs dictate that manufacturers offer a broad portfolio, ranging from high-precision motorized punches for research to mass-produced sterile disposable units for general clinical use.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 185.4 Million |

| Market Forecast in 2033 | USD 275.9 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BD (Becton, Dickinson and Company), Miltex (Integra LifeSciences), Kai Medical, Acuderm Inc., Sklar Instruments, Surtex Instruments, Henry Schein, Medline Industries, Premier Inc., Rocialle Healthcare, Teleflex Incorporated, NIPPON B&M, Biopsee, Robbins Instruments, Inc., ASSI (Accurate Surgical & Scientific Instruments), CooperSurgical, Inc., DermaPunch, Karl Storz SE & Co. KG. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Biopsy Punch Market, while seemingly simple in product concept, is undergoing continuous refinement centered on enhancing procedural precision, reducing patient trauma, and improving sample integrity for subsequent molecular analysis. The primary technological focus is on materials science, particularly the development of proprietary stainless steel alloys and specialized coatings that maintain edge sharpness over longer periods and minimize friction during tissue penetration. This results in cleaner excisions and less crush artifact, which is crucial for high-quality histological examination. Furthermore, advancements in handle ergonomics, incorporating non-slip grips and weight distribution optimized for physician comfort, contribute significantly to procedural consistency and reduced operator fatigue during high-volume use in dermatology clinics.

Another significant technological development involves the introduction of automated and spring-loaded biopsy systems. These devices are designed to standardize the depth and speed of tissue penetration, offering greater control than traditional manual punches. Automated punches often integrate visual indicators or locking mechanisms to ensure a consistent, measurable depth of sample acquisition, which is particularly useful for standardized clinical trials or when diagnosing conditions requiring precise dermal or subcutaneous sampling. While these motorized systems are currently a premium offering, their adoption is increasing in specialized oncology and research settings where sample standardization is a critical requirement for molecular diagnostics.

Furthermore, technology related to the disposable nature of the punches continues to evolve, focusing on integrated safety mechanisms and environmentally responsible materials. Many modern disposable punches feature retractable tips or protective sheaths designed to prevent accidental needle stick injuries post-procedure, aligning with global occupational safety standards. Future technological innovation is expected to merge physical sampling with digital capabilities, potentially incorporating micro-sensors or radio-frequency identification (RFID) tags onto the punch components for seamless integration into digital patient records and tracking systems, streamlining laboratory logistics and data management processes.

The disposable segment is predominantly driven by strict global infection control regulations (to prevent cross-contamination), the convenience of sterile, single-use items, and the high cost associated with the sterilization and maintenance of reusable instruments in modern clinical settings, especially high-volume Ambulatory Surgical Centers (ASCs).

Punch size is crucial for diagnostic accuracy. Larger punches (e.g., 4mm or 5mm) are often required for definitive diagnosis of panniculitis or certain inflammatory conditions to ensure sufficient subcutaneous tissue is acquired. Conversely, smaller sizes (1mm to 2mm) are preferred for cosmetic purposes or when minimal scarring is critical, such as for hair restoration (FUE).

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR). This growth is attributed to rising investments in healthcare infrastructure, increasing prevalence of skin conditions due to environmental and lifestyle factors, and expanding access to specialized diagnostic facilities across countries like China and India.

Automated or motorized punches are significant for enhancing procedural standardization and precision. They ensure consistent depth and speed of tissue acquisition, minimizing human variability and reducing crush artifacts, which is highly valuable for research protocols, clinical trials, and when obtaining tissue for sensitive molecular diagnostic testing.

No, while non-invasive imaging techniques (like advanced dermatoscopes and confocal microscopy) aid in triage and preliminary assessment, the physical tissue sample acquired by a biopsy punch remains the gold standard for definitive histological and molecular diagnosis of most serious conditions, including melanoma, as required by pathology standards worldwide.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.