ID : MRU_ 432028 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

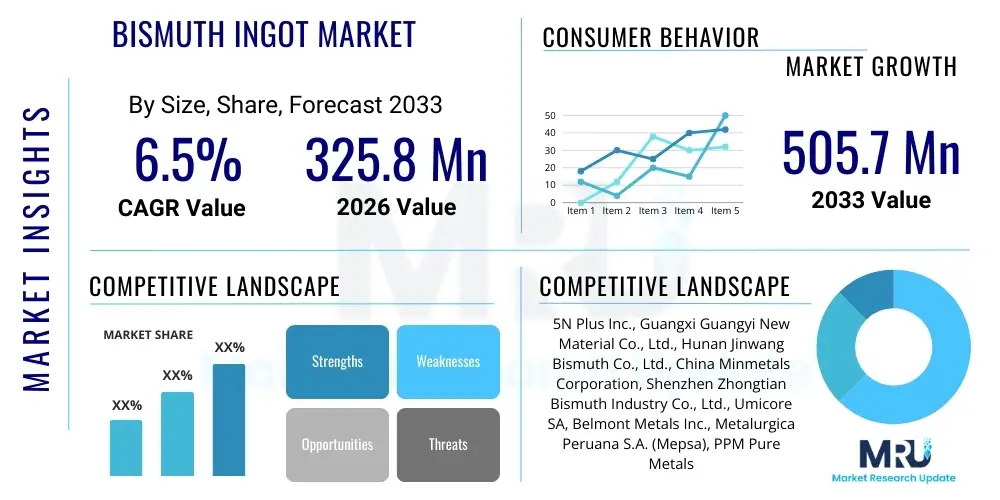

The Bismuth Ingot Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 325.8 Million in 2026 and is projected to reach USD 505.7 Million by the end of the forecast period in 2033.

The Bismuth Ingot Market encompasses the trade and utilization of refined bismuth metal, typically cast into ingot form for ease of handling and processing across various industrial applications. Bismuth (Bi) is a brittle, crystalline, white metal, recognized for its unusual property of being diamagnetic and having a low melting point, which makes it ideal for specialized low-temperature applications. Historically, bismuth served as a niche material, but its significance has surged due to its non-toxicity, making it a critical substitute for lead in plumbing, brass, solders, and ammunition, driven by stringent global environmental regulations, particularly in North America and Europe. The demand is heavily influenced by the construction and electronics sectors, which rely on lead-free solders and fusible alloys.

Bismuth ingots, often categorized by purity levels (e.g., 99.99% to 99.9999%), are the standard commercial form for downstream manufacturing. Key applications include the manufacturing of pharmaceutical compounds (such as bismuth subsalicylate for digestive aids), cosmetic pigments, and catalyst materials. Furthermore, the burgeoning field of thermoelectric materials, which utilizes bismuth telluride and similar compounds derived from high-purity ingots, is contributing substantially to market growth. The intrinsic benefits of bismuth, such as its corrosion resistance and expansion upon solidification, cement its necessity in precision casting and specialized tooling alloys.

Major driving factors include the global legislative push for lead substitution in industrial and consumer products, accelerated demand for specialty chemicals in the healthcare sector, and technological advancements in metallurgy requiring sophisticated low-melting-point alloys. The market’s trajectory is closely tied to the stability of primary production sources, as bismuth is primarily recovered as a byproduct of processing copper, lead, and tin ores. Ensuring a stable, high-purity supply chain remains paramount for continuous market expansion and meeting the stringent quality requirements of end-use industries like electronics and pharmaceuticals.

The Bismuth Ingot Market is characterized by steady growth underpinned by critical environmental shifts and technological demands, particularly the mandatory phasing out of lead in numerous applications across developed economies. Business trends indicate a focus on refining efficiency and establishing robust, transparent sourcing mechanisms, as geopolitical risks associated with byproduct metals necessitate supply chain diversification. Major manufacturers are investing in advanced refining technologies, such as electrolytic methods, to achieve ultra-high purity levels (5N to 6N) required for sensitive electronic and optical applications. Furthermore, consolidation among mid-tier refiners and strategic long-term contracts between miners and major downstream consumers are shaping the competitive landscape, aiming to mitigate price volatility often associated with byproduct commodity markets.

Regionally, Asia Pacific (APAC) dominates the consumption and production landscape, driven by massive electronics manufacturing hubs and rapid urbanization requiring extensive plumbing and construction infrastructure where lead-free materials are increasingly adopted. China remains the largest producer and consumer, although stricter environmental controls within the country are influencing production costs globally. North America and Europe, while having smaller production bases, exhibit high-value consumption due to stringent regulatory frameworks accelerating the transition to bismuth-based solders and alloys, particularly in automotive and defense industries. Latin America and MEA show nascent growth, primarily focusing on local pharmaceutical manufacturing and localized infrastructure projects.

Segmentation trends highlight the increasing importance of the high-purity segment (99.999% and above), which commands significant premiums due to its necessity in advanced thermoelectric devices, high-efficiency catalysts, and sophisticated metallurgical processes. Application-wise, the metallurgical segment (including lead-free solders and fusible alloys) remains the largest volume consumer, while the chemical and pharmaceutical segments drive demand for stability and guaranteed supply quality. The pharmaceutical sector, demanding adherence to Good Manufacturing Practices (GMP) and rigorous traceability, is witnessing specialized supply chain development focused exclusively on meeting industry-specific regulatory standards for bismuth salts and compounds.

Common user questions regarding AI's impact on the Bismuth Ingot Market frequently center on predictive pricing volatility, optimizing complex byproduct extraction processes, and enhancing the quality control of high-purity ingots. Users are particularly concerned about how AI and Machine Learning (ML) can stabilize the supply chain, given that bismuth production is inherently linked to the highly variable output of primary metals like lead and copper. The analysis reveals a strong user expectation that AI algorithms will transform demand forecasting for niche applications, providing refiners and consumers with more reliable strategic insights than traditional linear models. Furthermore, questions often relate to using AI for non-destructive testing and quality verification to meet the exacting purity standards required by the semiconductor and pharmaceutical industries, minimizing batch contamination and maximizing yield from complex refining operations.

AI’s initial impact is most visible in optimizing the complex flotation and refining circuits necessary to extract bismuth from primary ore concentrates, improving yields and reducing energy consumption by analyzing multivariate process parameters in real-time. Secondly, ML models are being deployed to integrate macro-economic indicators, primary metal output data, and regulatory changes to create highly accurate price forecasts for bismuth, crucial for long-term contract negotiations in a market prone to sudden price spikes. While direct application of AI in the physical casting of ingots is minimal, AI-driven sensor fusion and anomaly detection systems are being implemented to ensure dimensional consistency and detect internal flaws in high-value specialty ingots, ensuring that every batch meets the necessary quality specifications before shipment to downstream users.

The market dynamics for Bismuth Ingots are governed by a unique set of drivers, restraints, and opportunities, heavily influenced by global environmental policies and the inherent nature of Bismuth as a byproduct metal. The primary driver is the accelerating substitution of toxic lead across various sectors, creating significant mandated demand for lead-free alternatives, including bismuth-based solders, plumbing fittings, and ammunition. Simultaneously, the burgeoning development of advanced technologies, particularly in thermoelectric cooling and specialized pharmaceutical formulations, provides robust demand for ultra-high purity bismuth. These factors collectively push manufacturers towards technological upgrades and capacity expansion in refining.

However, the market faces significant restraints. The most prominent constraint is the supply dependency on primary metal mining (lead, copper), meaning Bismuth production cannot be independently scaled up to meet sudden surges in demand, leading to sharp price volatility and supply bottlenecks. Furthermore, the specialized and capital-intensive nature of ultra-high purity refining poses a high barrier to entry, limiting the number of viable global suppliers capable of meeting stringent industrial standards. Another restraint involves the potential instability of geopolitical factors affecting key producing regions, notably China, which could disrupt the global supply chain equilibrium and accessibility.

Opportunities for market expansion are significant, especially in the development of new intermetallic compounds and alloys leveraging bismuth's unique properties in energy storage and advanced battery technologies. The growth of the electric vehicle (EV) sector, requiring lightweight and efficient cooling systems (potentially utilizing thermoelectric modules), presents a long-term, high-growth avenue. Additionally, increased focus on metal recycling and urban mining techniques for recovering bismuth from electronic waste provides a strategic opportunity to reduce reliance on primary mineral extraction, enhance supply security, and meet sustainability goals. Strategic vertical integration by end-users to secure long-term supply remains a key opportunity in this supply-constrained market.

The Bismuth Ingot Market is comprehensively segmented based on purity level, which is the primary determinant of end-use application and pricing, and by end-use industry, reflecting diverse consumption patterns across industrial and specialty sectors. The purity segmentation is crucial because 99.99% (4N) bismuth serves large-volume industrial markets like metallurgy, while 99.999% (5N) and 99.9999% (6N) purity are reserved exclusively for high-tech, sensitive applications requiring minimal trace element contamination, such as semiconductors and high-end specialty chemicals. This delineation significantly impacts processing techniques, cost structures, and supplier base concentration within each segment.

Segmentation by end-use industry reveals that the Metallurgical sector, encompassing lead-free solders, fusible alloys, and free-machining brasses, constitutes the largest segment by volume, fueled by ongoing infrastructural developments and mandated safety standards. However, the Chemical and Pharmaceutical sector, driven by medical uses (e.g., treatments for H. pylori) and specialty pigment production, represents the most stable high-margin segment, demanding exacting regulatory compliance and quality assurance. These sectors require Bismuth salts derived from high-purity ingots, establishing a complex, regulated supply chain.

Further analysis includes segmentation by form factor, although the ingot remains the predominant commercial trading unit. Variations include shot, powder, and custom shapes, catering to specific manufacturing needs such as powder metallurgy or chemical synthesis processes. Regional segmentation remains vital for understanding regulatory divergence and local manufacturing capabilities, with Asia Pacific leading in both sheer volume consumption and production capacity, while Western markets prioritize high-value, specialized applications that demand ultra-high purity material specifications.

The Bismuth Ingot value chain begins with the Upstream Analysis, dominated by the mining and smelting of primary metals, chiefly lead, copper, and tin, as bismuth occurs almost entirely as a minor byproduct. Key upstream players are major global mining corporations that process polymetallic ores. The concentration and preliminary separation of bismuth-containing residues occur at this stage. Due to the complexity and low concentration of bismuth in these residues, the initial extraction process is highly sensitive to the economic viability of the primary metal operation. This dependency introduces significant external risk factors into the Bismuth Ingot supply chain, directly impacting raw material availability and pricing for refiners.

Midstream activities involve sophisticated secondary refining and purification processes, where raw bismuth metal is refined into commercial-grade ingots (4N to 6N purity). This stage is characterized by high technical expertise, utilizing methods such as electrolytic refining and zone melting to achieve ultra-high purity levels necessary for sensitive end-uses. Refiners act as the crucial link, transforming volatile raw materials into standardized, marketable products. Distribution channels are varied: direct sales are common for ultra-high-purity material to specialized high-tech firms (ensuring quality traceability), while indirect distribution through specialized global metal traders and distributors serves the broader metallurgical and chemical markets, providing inventory management and regional delivery support.

The Downstream Analysis involves the end-use industries, including manufacturers of lead-free solders, pharmaceutical companies processing bismuth into medicinal salts, and specialized chemical firms creating advanced catalysts or thermoelectric compounds. The value is added through complex formulation and integration into final products. Direct channels are preferred by pharmaceutical and aerospace buyers seeking stringent quality control, minimizing risk of contamination and ensuring regulatory compliance. Indirect channels facilitate small-to-mid-sized users requiring readily available volumes of standard commercial grade (4N) ingots. The chain concludes with the consumer or industrial application, where the non-toxic properties of bismuth provide essential functionality, driving continued demand back up the chain.

The primary purchasers and end-users of Bismuth Ingots span a diverse range of high-value and high-volume industrial sectors, characterized by a fundamental requirement for non-toxic, low-melting-point metallic components or specialized chemical precursors. A key segment includes electronics manufacturers, particularly those adhering to stringent environmental directives (like RoHS) that necessitate the use of lead-free solders in printed circuit boards and electronic assemblies for consumer goods, automotive systems, and telecommunications infrastructure. These buyers prioritize high-purity ingots (5N) to ensure conductivity and reliability in their complex soldering processes, typically engaging in long-term procurement contracts with verified global refiners to guarantee consistent supply and quality specifications.

Another crucial customer group consists of pharmaceutical and specialty chemical companies. These entities utilize high-grade bismuth ingots to synthesize specific bismuth compounds, such as bismuth subsalicylate or various catalysts. The pharmaceutical sector demands the highest levels of traceability and documentation, often requiring certifications demonstrating compliance with international pharmacopeia standards. Their purchasing decisions are heavily influenced not just by price, but by supplier reliability, purity assurance, and robust quality control systems, making them highly selective long-term partners for premium ingot providers. Growth in digestive health treatments globally continues to solidify this sector’s importance.

Furthermore, foundries and metallurgical manufacturers specializing in producing fusible alloys for safety devices (e.g., fire sprinkler systems), specialized tooling, and low-melting-point thermal management solutions represent consistent volume buyers of standard 4N bismuth ingots. As regulatory pressures increase the use of bismuth brass in plumbing and potable water systems to eliminate lead contamination, municipal infrastructure projects and commercial construction firms also emerge as significant indirect consumers, driving demand for intermediate alloy products derived from bismuth ingots.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 325.8 Million |

| Market Forecast in 2033 | USD 505.7 Million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | 5N Plus Inc., Guangxi Guangyi New Material Co., Ltd., Hunan Jinwang Bismuth Co., Ltd., China Minmetals Corporation, Shenzhen Zhongtian Bismuth Industry Co., Ltd., Umicore SA, Belmont Metals Inc., Metalurgica Peruana S.A. (Mepsa), PPM Pure Metals GmbH, Hunan Chenzhou Mining Group Co., Ltd., Western Mining Co., Ltd., Hudson Bay Minerals Inc., JX Nippon Mining & Metals Corporation, Teck Resources Limited, Yunnan Tin Co., Ltd., Rio Tinto Group, Xiamen Tungsten Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Bismuth Ingot market's technological landscape is heavily focused on refining and purification methods designed to achieve and maintain ultra-high purity levels required by modern high-tech applications, particularly 5N and 6N grades. The primary technology utilized is Zone Melting, a highly effective process for purification where a narrow melted zone is passed down a solid ingot, segregating impurities to one end due to differences in solubility. This technique is capital-intensive but crucial for producing material suitable for semiconductors, optical components, and thermoelectric modules, where trace element contamination is unacceptable. Continuous technological refinement focuses on automation and energy efficiency within zone refining to lower operational costs while maximizing purity yield.

Electrolytic Refining constitutes another foundational technology, used predominantly for initial high-volume purification of crude bismuth derived from primary smelting residues. This electrochemical process separates bismuth from common impurities like lead, copper, and silver, achieving purity levels typically around 4N to 5N. Innovation in this area involves optimizing electrolyte composition and electrode geometry to enhance current efficiency and reduce energy input. Advanced analytical techniques, such as Inductively Coupled Plasma Mass Spectrometry (ICP-MS), are integral to this process, providing real-time, highly sensitive measurement of trace elements, which is essential for quality control and certification.

Furthermore, specialized alloy formulation technology is critical downstream. Manufacturers are continually developing new low-melting-point alloys that combine bismuth with tin, indium, and cadmium (where permitted) to create customized solders and fusible materials with specific thermal and mechanical properties. This involves sophisticated vacuum melting and casting techniques to ensure homogeneity and prevent oxidation. The integration of advanced computational materials science is increasingly aiding in the design and testing of these new lead-free bismuth alloys, accelerating product development cycles for specialized industrial and medical device applications.

The primary drivers are global environmental regulations mandating the replacement of toxic lead in solders, brasses, and ammunition, coupled with rising demand from high-technology sectors like thermoelectric cooling, which requires ultra-high purity Bismuth for maximum efficiency.

As a byproduct primarily of lead and copper mining, Bismuth supply cannot be independently adjusted. Its production volume is intrinsically linked to the variable output of primary metals, leading to high price volatility and supply bottlenecks during periods of high demand or disruption in primary metal markets.

The electronics and semiconductor industries primarily demand ultra-high purity Bismuth Ingots, specifically 99.999% (5N) and 99.9999% (6N) grades. This stringent purity requirement ensures minimal contamination that could affect the performance and lifespan of sensitive components like lead-free solders and thermoelectric devices.

Asia Pacific (APAC), particularly China, dominates the global Bismuth Ingot market. This region accounts for the majority of global production capacity and is the largest consumer, driven by extensive electronics manufacturing hubs and rapid infrastructural adoption of lead-free materials.

Thermoelectric technology, particularly in the development of efficient Bismuth Telluride modules for cooling and power generation applications in the automotive (EV) and data center sectors, offers the greatest long-term growth opportunity, driving sustained demand for 5N and 6N purity ingots.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.