ID : MRU_ 433234 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

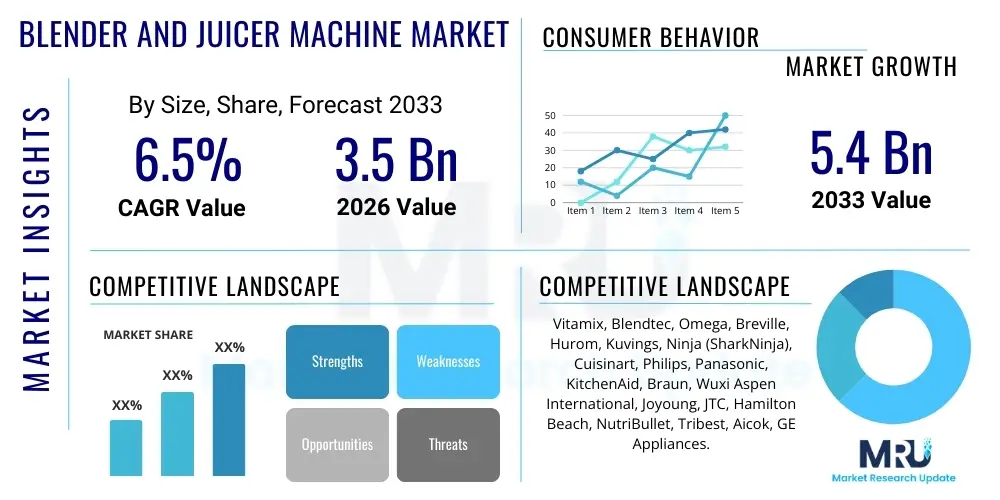

The Blender and Juicer Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 5.4 Billion by the end of the forecast period in 2033.

The Blender and Juicer Machine Market encompasses a wide range of kitchen appliances designed for processing fruits, vegetables, and other ingredients into beverages, purees, or mixes. Products within this market segment include traditional countertop blenders, immersion blenders, high-performance commercial blenders, centrifugal juicers, masticating (slow) juicers, and specialty personal blenders. These machines cater to both residential and commercial end-users, driven primarily by increasing health consciousness, busy modern lifestyles necessitating quick meal preparation, and the growing popularity of homemade smoothies and fresh juices as nutritional supplements. The versatility of modern appliances, capable of tasks ranging from crushing ice and blending nuts to extracting maximum nutrient yield from fibrous vegetables, significantly contributes to market expansion.

Major applications of blenders and juicers span across household kitchens, food service establishments (restaurants, cafes, smoothie bars), and healthcare facilities. In residential settings, they are indispensable for daily routines, enabling the creation of breakfast shakes, baby food, and complex culinary preparations. Commercially, heavy-duty blenders and juicers are critical components for high-volume beverage preparation, ensuring consistency and speed. The fundamental benefits these products offer include enhanced nutritional intake through preserved vitamins and enzymes, time savings in food preparation, and cost-effectiveness compared to purchasing pre-made beverages. Furthermore, technological integration, such as pre-set programs, vacuum blending capabilities, and smart connectivity, continues to elevate the user experience, making these appliances integral to contemporary healthy living trends.

The primary driving factors sustaining robust market growth include significant demographic shifts, particularly the rising middle-class disposable income in emerging economies, which encourages investment in modern kitchen appliances. Simultaneously, intense marketing efforts focusing on health and wellness, coupled with endorsements by fitness and nutrition influencers, amplify consumer demand. Manufacturers are continuously innovating to improve performance, reduce noise levels, and enhance ease of cleaning, addressing previous consumer friction points. Furthermore, the global shift toward plant-based diets and the emphasis on immunity-boosting foods post-pandemic have fundamentally solidified the blender and juicer machine’s position as a necessity rather than a luxury appliance.

The Blender and Juicer Machine market is characterized by fierce competition, rapid technological iteration, and a strong pivot toward premiumization and smart features. Key business trends include the consolidation of market share among major appliance manufacturers, aggressive expansion into high-growth APAC markets, and a significant emphasis on direct-to-consumer (D2C) channels to control brand narrative and pricing. The shift towards durable, powerful, and aesthetically pleasing designs is notable, transforming these kitchen tools into lifestyle products. Sustainability is becoming a critical business focus, with companies exploring recyclable materials, energy-efficient motors, and reduced packaging, driven by increasing consumer environmental awareness and regulatory pressures across North America and Europe.

Regional dynamics highlight Asia Pacific (APAC) as the fastest-growing market, primarily fueled by urbanization, increasing appliance penetration rates, and rising health expenditure in China, India, and Southeast Asian countries. North America and Europe, while mature, remain dominant in terms of revenue, specifically leading the adoption of high-end vertical juicers and advanced vacuum blending technology. In these developed regions, replacement cycles, coupled with demand for sophisticated integration into smart homes, maintain steady growth. Conversely, Latin America and the Middle East and Africa (MEA) present untapped potential, dependent on improving economic stability and targeted marketing efforts tailored to regional dietary habits and lower average household purchasing power.

Segmentation trends indicate a pronounced divergence in consumer preferences based on usage type and price point. The high-performance blender segment (used for heavy-duty commercial blending or specialized home tasks like nut butter making) is experiencing accelerated growth due to its versatility and durability. Concurrently, the slow (masticating) juicer segment is gaining traction over traditional centrifugal juicers, driven by scientific evidence suggesting better nutrient retention, appealing to health purists willing to pay a premium. The personal blender category continues to thrive, particularly among younger, urban populations seeking convenience and portability. Manufacturers are heavily investing in product variations tailored to these specific segment needs, ensuring comprehensive market coverage across the functional spectrum from basic utility to specialized culinary performance.

User queries regarding AI's influence on the Blender and Juicer Machine Market frequently revolve around concepts of personalized nutrition, automated usage based on dietary needs, predictive maintenance, and optimized blending/juicing cycles. Users express interest in how AI could analyze stored ingredient inventories, suggest recipes tailored to specific health goals (e.g., keto, high protein, low sugar), and then automatically adjust the speed, time, and pressure settings of the machine for optimal output and flavor consistency. Concerns often center on the security of personal health data shared with smart appliances and the potential cost increase associated with AI integration. The overarching expectation is that AI integration will transform these standalone appliances into integral components of a holistic, personalized smart kitchen ecosystem.

The practical application of Artificial Intelligence currently manifests in advanced sensor technology and proprietary algorithms that optimize machine performance. For blenders, AI can detect ingredient density and texture, automatically increasing or decreasing motor power to prevent stalling and achieve the perfect consistency, often termed ‘Smart Blending’ or ‘Self-Adjusting Technology.’ For juicers, AI can monitor the pulp extraction efficiency and recalibrate grinding speed to maximize yield based on the type and hardness of the fruit or vegetable inserted. This level of automated optimization improves both user satisfaction and the longevity of the appliance by preventing unnecessary wear and tear on the motor.

Looking ahead, the true disruptive impact of AI will be seen in its ability to connect appliance usage directly with health and inventory management platforms. For instance, a smart juicer connected to a consumer's wellness tracker could recommend specific nutrient-dense recipes if the user's activity levels spike or certain vitamin deficiencies are detected. Furthermore, AI-driven diagnostics will enable manufacturers to remotely monitor machine health, predict component failure before it occurs, and dispatch preemptive maintenance alerts, drastically enhancing after-sales service quality and reducing customer downtime. This technological evolution redefines the role of the appliance from a passive tool to an active participant in managing consumer well-being.

The Blender and Juicer Market is propelled by strong consumer demand for health-focused kitchen technology, driven by the global wellness movement and the convenience afforded by high-speed processing capabilities. Key restraints include the high initial cost associated with premium, performance-driven models (especially high-wattage blenders and slow masticating juicers) and market saturation in developed regions, leading to reliance on replacement cycles rather than new consumer adoption. Opportunities lie predominantly in technological advancements, such as integrating IoT capabilities for personalized nutrition guidance and developing specialized, affordable personal-sized units targeting mobile and budget-conscious demographics. The combination of these factors dictates market trajectory and competitive intensity.

Impact forces on the market are multifaceted. The accelerating pace of technological innovation acts as a significant positive force, with manufacturers constantly introducing vacuum blending, noise reduction features, and self-cleaning mechanisms, compelling consumers to upgrade. However, the presence of low-cost, unbranded appliances, especially through online marketplaces, exerts downward pressure on pricing and perceived value in the mass-market segment. Regulatory shifts concerning energy consumption standards (e.g., in the EU and North America) force manufacturers to invest heavily in motor efficiency, which can increase production costs but ultimately improves product sustainability, aligning with growing consumer preference for eco-friendly appliances.

Specifically, the primary driver remains the increasing global prevalence of chronic diseases linked to poor diet, prompting proactive consumer behavior regarding fresh food consumption. The market is restrained by the sheer volume of competitor offerings, leading to consumer confusion and decision paralysis when selecting the optimal appliance type (e.g., deciding between various juicing technologies). The largest opportunity involves penetrating commercial sectors beyond traditional foodservice, such as corporate offices, gyms, and specialty diet centers, which require robust, easy-to-use, and quick-serve options. Managing the balance between premium pricing (for specialized features) and mass accessibility (for core functionality) is central to navigating these complex impact forces effectively.

The Blender and Juicer Machine Market is fundamentally segmented based on product type, application, distribution channel, and motor power/performance level. Analyzing these segmentations is crucial for understanding specific consumer behaviors and allocating manufacturing resources effectively. The product type segmentation distinguishes between blenders (further categorized into conventional, high-performance, and personal) and juicers (centrifugal, masticating, and triturating). Performance segmentation often dictates pricing, with high-performance units (often exceeding 1000 watts) commanding significant premiums due to superior durability and ability to handle tough ingredients like frozen fruits and raw vegetables.

Application analysis highlights the dominant household use segment, which prioritizes ease of use, aesthetic design, and manageable size. Conversely, the commercial application segment demands industrial strength, continuous duty cycles, and large capacities suitable for high-volume environments like restaurant kitchens and juice bars. Distribution channels are rapidly shifting, with traditional retail stores losing ground to online platforms (e-commerce), which offer better price comparisons, detailed product reviews, and convenient direct delivery, thereby influencing purchasing behavior, especially among tech-savvy younger demographics who value instant access to product information and peer feedback.

The evolution within segmentation is driven by a focus on specialization. The rise of the personal blender segment, designed for single-serve convenience and portability, reflects the fast-paced nature of modern urban life. Similarly, within juicers, the masticating or slow juicer segment continues to grow rapidly as consumers prioritize the perceived health benefits of cold press technology over the speed of centrifugal models. Understanding the nuanced preferences across these segments—from the high-volume needs of commercial operators to the personalized nutrient focus of home users—is vital for sustained market penetration and product development strategy.

The value chain for the Blender and Juicer Machine Market begins with upstream activities, predominantly involving the sourcing of raw materials such as high-grade plastics (BPA-free Tritan), stainless steel components for blades and motors, and specialized electronic microprocessors. Successful upstream management requires robust supply chain logistics, particularly in managing fluctuations in commodity prices and ensuring the quality and safety certification of raw materials, which is crucial for consumer appliances. Key manufacturers often maintain long-term relationships with a limited number of specialized motor and blade suppliers to ensure performance consistency and protect proprietary design specifications, a vital component of brand reputation.

Manufacturing and assembly form the core of the midstream process, where major companies leverage automation and large-scale assembly lines, often located in Asia Pacific regions (China, Vietnam), to achieve economies of scale. Direct distribution is becoming increasingly favored by premium brands seeking tighter control over pricing and customer interaction, utilizing company-owned e-commerce platforms. Indirect distribution remains dominant for mass-market brands, relying on large national retailers, department stores, and hypermarkets to achieve broad geographic reach. The selection of distribution partners significantly impacts brand visibility, inventory management efficiency, and shelf-space negotiation, especially during peak retail seasons like holidays.

The downstream segment focuses heavily on marketing, sales, and post-sale services. Effective marketing strategies often utilize digital platforms and influencer partnerships to demonstrate product versatility and promote health benefits, directly appealing to the wellness demographic. Post-sales support, including extended warranties, accessible repair services, and readily available replacement parts (such as jars and blades), is a critical differentiator, especially for high-investment premium appliances. The overall efficiency of the value chain is determined by the seamless flow from material sourcing to end-user satisfaction, with continuous pressure to reduce lead times and optimize inventory levels to respond quickly to evolving consumer trends.

Potential customers for the Blender and Juicer Machine Market are broadly categorized into health-conscious individuals, busy urban professionals, culinary enthusiasts, and commercial food service operators. Health-conscious individuals represent a rapidly expanding demographic, purchasing these appliances primarily to facilitate dietary management, detoxification routines, and consistent consumption of whole fruits and vegetables. These customers often seek slow masticating juicers or powerful high-speed blenders capable of producing highly nutritious and smooth-textured beverages, prioritizing quality and nutrient retention over cost.

Busy urban professionals and younger consumers constitute the primary market for personal and compact blenders. This segment values convenience, speed, and portability, seeking appliances that allow for quick single-serve meal replacements, often consumed on the go. They are heavily influenced by digital marketing and social media trends, demanding sleek, aesthetically pleasing designs that fit small kitchen spaces. Price sensitivity is moderate in this group, balanced against the appliance's perceived contribution to a time-efficient and healthy lifestyle. The focus here is on ease of cleaning and minimal counter footprint.

The commercial segment, encompassing restaurants, juice bars, cafeterias, and institutional kitchens, represents a high-value customer base demanding appliances with industrial-grade durability, high throughput, and robust warranty coverage suitable for continuous use environments. These buyers prioritize features such as powerful motors (often air-cooled), sound enclosures for noise reduction, and modular designs that simplify maintenance and cleaning adherence to strict hygiene standards. For manufacturers, securing large contracts within the hotel and food service industries provides reliable, high-volume revenue streams, making direct sales and customized technical support crucial aspects of client relationship management.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.4 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Vitamix, Blendtec, Omega, Breville, Hurom, Kuvings, Ninja (SharkNinja), Cuisinart, Philips, Panasonic, KitchenAid, Braun, Wuxi Aspen International, Joyoung, JTC, Hamilton Beach, NutriBullet, Tribest, Aicok, GE Appliances. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Blender and Juicer Machine Market is defined by innovation aimed at improving motor efficiency, blade durability, noise reduction, and smart connectivity. A primary technological focus is on enhancing the motor's power output (often exceeding 1500 watts for premium blenders) while simultaneously integrating advanced thermal management systems to prevent overheating during prolonged, heavy-duty operation. For juicers, the shift from high-speed centrifugal technology to low-speed masticating technology, which minimizes heat exposure and oxidation, represents a significant technological leap focused on maximizing nutritional value retention. Furthermore, specialized blade designs (e.g., asymmetrical, aircraft-grade stainless steel) are critical for breaking down tough ingredients uniformly.

Noise mitigation technology is another vital area of innovation, particularly for high-powered blenders used in open-plan kitchens or commercial settings. Manufacturers are achieving substantial noise reduction through the use of fully enclosed sound dampening shields and sophisticated motor housing design. Simultaneously, the integration of Vacuum Blending technology has emerged as a high-growth segment. This process removes air from the blending jar before operation, significantly reducing oxidation, resulting in brighter colors, less foam, and better preservation of vitamins, directly appealing to health-conscious consumers willing to pay a premium for superior freshness and quality.

The future of the technology landscape is rooted in connectivity and user interface refinement. Smart blenders and juicers now feature built-in weight sensors, pre-programmed recipe cycles accessible via companion apps, and Bluetooth or Wi-Fi connectivity for remote monitoring and diagnostics. This integration allows for precise control over consistency, automated ingredient measurement, and firmware updates, effectively turning the appliance into a sophisticated culinary assistant. Key technologies such as sensor fusion, brushless DC motors for better efficiency, and Tritan plastic containers (BPA-free, highly durable) collectively define the modern standard of performance and safety in this market.

The global Blender and Juicer Machine Market exhibits distinct regional consumption patterns and growth dynamics. North America remains a highly mature and critical market, defined by strong consumer demand for high-performance blenders (such as those used for heavy-duty meal preparation) and premium, expensive juicing technologies. The US market is characterized by high replacement rates and a significant adoption of smart kitchen appliances. Consumers here are highly brand loyal but increasingly demand sophisticated features like vacuum blending, advanced warranties, and excellent after-sales support. This region serves as a benchmark for innovation and premium pricing strategies.

Europe mirrors North America in terms of maturity but shows a slightly higher propensity towards environmental considerations, influencing demand for energy-efficient motors and appliances made from sustainable or recyclable materials. Germany, the UK, and France are dominant contributors, with strong established local brands competing intensely with global players. The preference for compact design and integration into smaller European kitchens also drives the personal blender and stick blender segments. Regulatory alignment across the EU necessitates compliance with strict safety and energy standards, shaping product development priorities in this geography.

Asia Pacific (APAC) is unequivocally the engine of future market growth. Rapid urbanization, significant increases in disposable income, and a growing middle class in populous countries like China and India are transitioning from manual preparation methods to automated kitchen appliances. The demand in APAC is bifurcated: a large volume market exists for affordable, functional appliances, alongside a fast-growing niche for premium, imported appliances driven by aspirational consumer behavior. The unique focus on traditional ingredients and regional recipes also necessitates localized product customization (e.g., motors optimized for processing grains or regional spices), making it a key focus for global manufacturers seeking volume expansion.

The demand is primarily driven by the trend toward plant-based diets and complex home cooking, requiring high-wattage motors (1000W+) and durable blades capable of processing tough ingredients like raw vegetables, nuts, and frozen fruits into smooth, consistent textures quickly, often replacing multiple kitchen gadgets.

Centrifugal juicers operate at high speed, generating heat and aeration, which can degrade nutrients quickly. Masticating (slow) juicers press and grind ingredients slowly, minimizing heat and oxidation, thereby offering superior juice quality, enzyme preservation, and maximum yield, making them the preferred choice for maximizing nutritional benefits.

Asia Pacific (APAC), particularly emerging economies like China and India, holds the highest expansion potential. This growth is underpinned by rising disposable incomes, rapid urbanization, and an accelerating adoption of health-conscious lifestyles, leading to increased purchasing of automated kitchen appliances.

IoT integration allows for connectivity to companion apps, enabling features like personalized recipe suggestions based on dietary restrictions, automated blending programs based on ingredient detection (AI-assisted), remote diagnostics, and firmware updates, transforming the appliances into smart culinary assistants for enhanced convenience and precision.

Market saturation and the high average selling price (ASP) of premium models are the main restraints in developed markets like North America and Europe. Growth is heavily reliant on replacement cycles and the ability of manufacturers to introduce disruptive, compelling innovations (like vacuum technology or extreme power) that justify a consumer upgrade.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.