ID : MRU_ 438533 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

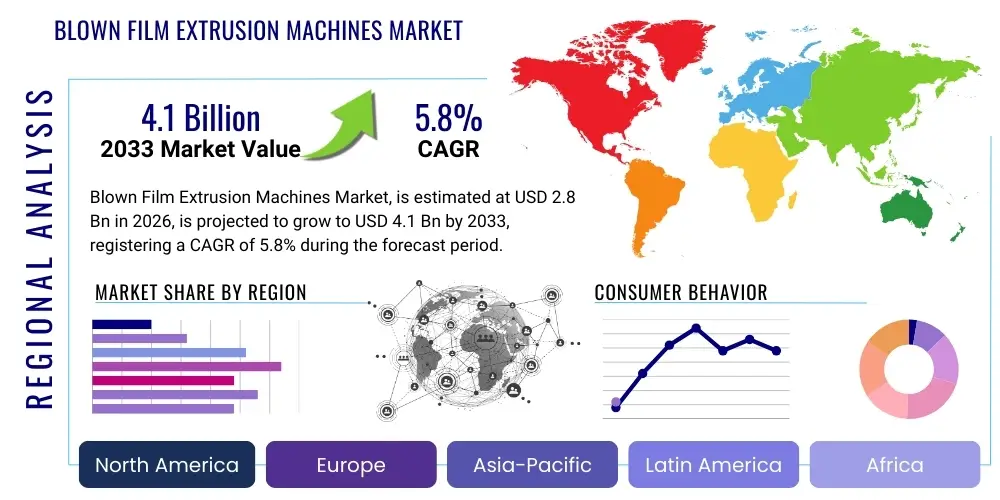

The Blown Film Extrusion Machines Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 2.8 Billion in 2026 and is projected to reach USD 4.1 Billion by the end of the forecast period in 2033.

The Blown Film Extrusion Machines Market encompasses the manufacturing, distribution, and utilization of specialized industrial equipment designed to produce thermoplastic films by extruding molten polymer through an annular die and inflating it with air. This process yields continuous tubing, which can be subsequently slit and treated for various flexible packaging and industrial applications. These machines are pivotal in transforming raw polymer resins, such as Low-Density Polyethylene (LDPE), High-Density Polyethylene (HDPE), and Linear Low-Density Polyethylene (LLDPE), into finished goods like shrink wrap, heavy-duty sacks, agricultural films, and multilayer barrier films essential for food preservation. The continuous demand from the thriving e-commerce sector and the sustained need for protective packaging across FMCG and pharmaceutical industries are primary growth pillars supporting market expansion globally.

Product sophistication within this domain has accelerated, driven by the need for enhanced film properties, including increased barrier protection, improved puncture resistance, and greater optical clarity. Modern blown film lines often incorporate multi-layer co-extrusion capabilities, enabling manufacturers to combine different polymers to achieve customized performance characteristics previously unattainable with mono-layer systems. The adoption of advanced components, such as automatic thickness control systems, gravimetric dosing units, and high-efficiency cooling rings, significantly enhances operational consistency, reduces material waste, and lowers energy consumption, making newer machines highly attractive investments for large-scale packaging converters aiming for superior productivity and sustainability compliance.

Major applications driving the demand for these machines include food packaging (pouches, wrappers), industrial packaging (stretch films, liners), consumer goods (shopping bags, protective coverings), and specialized applications like medical films and agricultural mulch films. The inherent benefits of films produced via blown extrusion, such as excellent heat seal strength, superior tensile properties, and the flexibility to adjust film width and gauge instantly, cement the machine’s foundational role in the flexible packaging supply chain. The overriding driving factors include rapid industrialization in developing economies, regulatory pressure favoring recyclable materials stimulating investment in specialized machine types, and the global shift toward flexible packaging solutions dueishing logistics efficiency and reducing overall material weight.

The Blown Film Extrusion Machines Market is characterized by robust business trends centered on automation, efficiency, and sustainability. Key business drivers involve fierce competition among machinery manufacturers focusing on integrating Industry 4.0 standards, including predictive maintenance capabilities and real-time operational diagnostics, to minimize downtime. Companies are strategically pivoting towards offering turnkey solutions and modular systems that allow converters flexibility in scaling production lines and quickly adapting to shifts in polymer trends, particularly the increasing reliance on bio-plastics and recycled content (PCR). Furthermore, mergers and acquisitions remain a consistent strategy among leading players to consolidate technological expertise, particularly in high-precision co-extrusion and large-format machine segments, thereby expanding geographic reach and enhancing competitive product portfolios.

Regionally, the Asia Pacific (APAC) market maintains undeniable leadership, primarily due to the expansive growth of the domestic manufacturing sector, rapidly escalating consumer demand for packaged goods, and significant governmental investment in infrastructure and industrial zones, particularly in China and India. While North America and Europe represent mature markets, growth here is dominated by stringent environmental regulations mandating the transition to machinery capable of handling sustainable and post-consumer recycled resins (PCR). This regulatory environment necessitates substantial capital expenditure for upgrading existing equipment or investing in sophisticated lines that meet circular economy objectives. Latin America and the Middle East and Africa (MEA) are emerging as high-potential markets, driven by favorable demographics, urbanization, and the nascent establishment of sophisticated local packaging industries, creating strong demand for mid-range and high-output machinery.

Segment trends indicate a pronounced shift towards multi-layer co-extrusion technology, specifically 5-layer and 7-layer systems, as converters prioritize barrier properties crucial for extending the shelf life of perishable goods. HDPE and LLDPE machine types are experiencing high volume sales, reflecting their utility in heavy-duty applications and stretch films, respectively. In terms of application, food and beverage packaging remains the most dominant segment, though specialty film production, including high-strength agricultural and medical films, is forecast to achieve the highest compounded annual growth rate. The market is also seeing polarization, with demand strong for both high-speed, high-output lines necessary for bulk packaging and compact, energy-efficient lines suitable for specialized, smaller volume production runs, underscoring the diversification of end-user needs.

User inquiries regarding AI's influence in the Blown Film Extrusion Machines Market primarily revolve around operational efficiency, material optimization, and predictive maintenance. Common questions include: "How can AI reduce material waste in the extrusion process?", "What role does machine learning play in optimizing film gauge uniformity?", and "Can AI predict equipment failure in complex multi-layer lines?" These themes reveal a strong market expectation for AI to solve persistent operational challenges related to throughput variability, quality control, and the costly downtime associated with unscheduled maintenance. Users are focused on leveraging AI for real-time prescriptive analytics, moving beyond mere descriptive monitoring to achieve genuine optimization of energy consumption and raw material usage, thereby enhancing competitiveness and sustainability credentials within a highly capitalized industry. The integration of sophisticated algorithms with existing industrial internet of things (IIoT) sensors is seen as the next frontier for achieving previously unattainable levels of precision in film production.

The market is predominantly influenced by robust drivers, counterbalanced by inherent operational restraints, while significant opportunities remain available for technologically agile firms, all of which are interconnected by fundamental impact forces defining market dynamics. The primary driver is the pervasive, sustained expansion of the global flexible packaging industry, fueled by evolving consumer lifestyles favoring convenience, portability, and single-serve packaging formats, which necessitates high-volume film production. Simultaneously, strict international and regional environmental regulations demanding circular economy practices are forcing manufacturers to invest in new extrusion technology capable of processing high percentages of recycled content (PCR) and bio-based plastics, effectively creating a replacement cycle for older, inefficient machinery. Furthermore, technological advancements in co-extrusion, allowing for production of films with superior barrier properties essential for sophisticated applications like medical and aseptic packaging, substantially push the demand envelope.

However, significant restraints temper the market’s growth trajectory. High initial capital investment required for state-of-the-art multi-layer extrusion lines poses a substantial barrier to entry for smaller and mid-sized enterprises, particularly in emerging markets, leading to market consolidation among well-capitalized players. Volatility in the price and supply of key raw materials, primarily crude oil derivatives such as polyethylene and polypropylene resins, creates instability in operational costs and profit margins for film producers, indirectly affecting machinery procurement cycles. Moreover, the increasing demand for sustainable packaging, while driving innovation, also introduces complexity in machine design and operational management, requiring specialized expertise and significant retooling efforts to achieve acceptable output quality with non-virgin materials.

Opportunities for expansion lie predominantly in developing customized machinery solutions tailored for highly specialized niche applications, such as high-strength agricultural silage films and technical films for construction. The rapid proliferation of e-commerce necessitates continuous innovation in protective and shipping films, offering a vast, untapped potential for high-speed stretch and shrink film lines. Furthermore, manufacturers who successfully integrate IIoT, AI, and comprehensive digital services into their machinery offerings, providing remote diagnostics and prescriptive maintenance solutions, stand to capture premium segments of the market. The impact forces acting upon this equilibrium are characterized by high substitution threat from alternative packaging forms (e.g., rigid plastics, glass) and strong bargaining power exerted by large film converters who dictate specifications and price points, requiring machine manufacturers to maintain relentless focus on cost reduction and technical superiority.

The Blown Film Extrusion Machines Market is meticulously segmented based on key structural and functional criteria, allowing for granular analysis of demand patterns and technological adoption across various end-user industries. The segmentation is primarily driven by the complexity of the film required (measured by the number of layers), the type of material processed, the output rate (size/capacity), and the ultimate application of the extruded film. The complexity of machinery ranges from simple mono-layer units used for commodity packaging to highly sophisticated nine-layer or ten-layer systems engineered for complex barrier films required in high-end food and pharmaceutical applications. Understanding these segments is crucial for strategic business planning, as it dictates the required investment level, the target customer base, and the regional suitability of the machinery offered.

The value chain for the Blown Film Extrusion Machines Market is complex, beginning with upstream analysis focused on the procurement of specialized components and raw materials necessary for machine construction. Upstream activities are dominated by specialized suppliers providing highly engineered components such as high-precision gearboxes, large-format screws and barrels made from specialized alloys, sophisticated annular dies, and advanced control systems (PLCs, motors, drives). The core competitive advantage for machine manufacturers often hinges on their ability to source these components reliably and integrate them efficiently. Price fluctuations in metals and sophisticated electronic components can significantly influence the final cost of the extrusion machine. Machine builders must manage complex supplier relationships to ensure component quality and availability, as a single component failure can render an entire production line inoperable.

Midstream activities involve the core manufacturing process, where leading machine builders focus on proprietary designs, precision machining, and rigorous assembly and testing protocols. Manufacturers differentiate themselves through technological innovation, such as developing specialized cooling systems (e.g., internal bubble cooling, high-efficiency air rings) and advanced automation features crucial for energy savings and operational consistency. The distribution channel is bifurcated into direct sales and indirect representation. Direct sales are typically favored for high-value, customized, multi-layer extrusion lines sold to large multinational packaging converters, ensuring close consultation and after-sales service. Indirect channels, utilizing specialized distributors or agents, are common for standard mono-layer or lower-capacity machines, particularly in regions where the manufacturer does not maintain a large local presence. These distributors provide essential local support, installation, and spare parts inventory.

Downstream analysis focuses on the end-users and the final applications of the produced film. The immediate downstream users are film converters and plastic packaging companies who utilize the machines to produce various primary and secondary packaging materials. These converters then sell their film products to diverse sectors, including Food & Beverage, Consumer Goods, and Agriculture. Direct sales ensure manufacturers maintain greater control over service quality and glean direct feedback for product improvement, which is critical in this high-technology market. Indirect channels broaden market access but require robust training and support for the channel partners to maintain the brand’s technical reputation. The success of the machine builder is intrinsically linked to the profitability and growth of these downstream film converters, necessitating partnerships that include technical training, financing solutions, and ongoing application support to optimize film formulation and production efficiency.

Potential customers in the Blown Film Extrusion Machines Market are primarily concentrated among companies involved in flexible packaging manufacturing and specialized polymer processing, forming a critical link between raw material suppliers and consumer goods companies. The dominant customer base includes multinational packaging corporations that operate numerous high-output production lines globally, such as Amcor, Berry Global, and Sealed Air. These large entities demand highly customized, multi-layer co-extrusion lines capable of high speeds, precise gauge control, and flexibility in handling complex resin blends, often prioritizing energy efficiency and sophisticated automation features to minimize labor costs and environmental impact across massive scales of operation. Their procurement decisions are driven by total cost of ownership (TCO) and long-term service agreements rather than just the initial capital expenditure.

A second substantial segment comprises medium-sized regional film converters who service local and national markets. These businesses typically seek robust, reliable three-layer or five-layer machines with moderate output capacities (200-500 kg/hr). Their purchasing criteria emphasize quick return on investment, ease of maintenance, and the versatility to switch between different film applications (e.g., from trash bags to agricultural film). In rapidly developing economies, this segment is characterized by high growth potential as industrialization accelerates, demanding cost-effective, durable machinery. Furthermore, niche potential customers include companies focused exclusively on specialized films, such as medical-grade sterile films or advanced photovoltaic encapsulation films, which require ultra-high precision extrusion systems and specialized cleanroom compatibility, representing a high-margin but low-volume sales opportunity.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 4.1 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | W&H (Windmöller & Hölscher), Reifenhäuser Group, Rajoo Engineers Ltd., Alpine (Hosokawa Alpine), Brampton Engineering Inc., Macro Engineering & Technology Inc., SML Group, KUHNE Anlagenbau GmbH, JC Times Technology Co., Ltd., Polystar Machinery Co., Ltd., Fong Kee Iron Works Co., Ltd., JINMING Machinery Co., Ltd., COLINES S.p.A., Carer Makina, BOCO Technologies Inc., and Atlas Converting Equipment Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Blown Film Extrusion Machines Market is undergoing continuous evolution, primarily focusing on enhancing co-extrusion capabilities, improving operational efficiency, and addressing sustainability requirements. Multi-layer co-extrusion technology is arguably the most critical advancement, enabling manufacturers to produce films containing up to 11 layers or more. This sophisticated layering allows for the strategic placement of different polymer resins (e.g., barrier resins like EVOH, adhesive layers, and structural resins) to achieve optimal performance characteristics, such as oxygen and moisture barrier protection crucial for shelf-stable food products. Modern lines incorporate highly advanced melt pumps and specialized feedblocks that ensure precise layer distribution and uniformity, which is vital for high-speed winding and subsequent converting operations. The drive towards high-output lines necessitates highly efficient cooling systems, including advanced Internal Bubble Cooling (IBC) systems and sophisticated air rings, which accelerate the cooling process to increase production speeds without compromising film clarity or mechanical strength.

A secondary, but rapidly accelerating, technological trend involves the integration of advanced process control and automation systems, moving towards the paradigm of smart manufacturing or Industry 4.0. Key components include gravimetric dosing systems that accurately measure and blend multiple raw materials in real-time, coupled with automated gauge control (AGC) systems using non-contact sensors (e.g., infrared or nuclear sources) to maintain tight film thickness tolerances across the entire width. These systems minimize material usage, which is the single largest cost component in film production. Furthermore, the incorporation of sophisticated Human-Machine Interfaces (HMIs) and connectivity tools allows operators to manage complex recipes, monitor energy consumption, and interface with centralized plant management software, thereby optimizing the entire factory floor performance and facilitating remote diagnostics and service support.

Finally, technology related to material handling and recycling is increasingly prominent. Machine designers are actively developing screws and barrels specifically optimized for processing resins derived from Post-Consumer Recycled (PCR) waste. Processing PCR is inherently challenging due to material heterogeneity and varying melt indexes, necessitating specialized venting and filtering systems (screen changers) to remove contaminants without disrupting the extrusion process. The development of extrusion lines that can seamlessly switch between virgin resins, PCR content, and biodegradable polymers demonstrates the market’s commitment to regulatory compliance and circular economy principles. This flexibility is essential for converters who must rapidly adapt their product mix to meet fluctuating customer demands and regulatory mandates regarding recyclable content.

The global Blown Film Extrusion Machines market exhibits significant disparity in growth rates and technological maturity across different geographic regions, heavily influenced by local economic growth, packaging regulations, and industrial production output.

The primary driver is the increasing regulatory and consumer demand for superior barrier packaging, particularly in the food and pharmaceutical sectors, which requires films with specific protection against oxygen and moisture to extend shelf life. Multi-layer co-extrusion allows converters to combine structural, adhesive, and barrier resins effectively to achieve these complex film properties, making them essential for high-end flexible packaging applications.

Sustainability mandates are significantly accelerating the investment cycle, forcing manufacturers to purchase or upgrade machinery capable of efficiently processing Post-Consumer Recycled (PCR) resins and bio-plastics. New machines must feature advanced filtration and specialized screw designs to handle variable quality recycled materials while maintaining high output and film quality, meeting brand owners' circular economy commitments.

Asia Pacific (APAC), particularly driven by China and India, holds the largest market share. This dominance is due to rapid industrialization, massive growth in the domestic consumer goods and flexible packaging industries, and the continuous expansion of the manufacturing base across the region, generating sustained high volume demand for both low-cost and technologically advanced extrusion lines.

Industry 4.0 technologies, including IIoT sensors and AI-driven control systems, are critical for achieving operational excellence. They enable predictive maintenance, real-time automated gauge control (AGC), precise material dosing, and energy usage optimization. This integration minimizes downtime, reduces material waste, and enhances the overall profitability of high-speed production lines.

Mono-layer machines produce films from a single type of polymer, suitable for commodity applications like trash bags or simple industrial liners. Co-extrusion machines use multiple extruders feeding a single die to merge several distinct layers of different polymers, essential for producing high-performance barrier films, stretch films, and customized food packaging requiring specific mechanical and protective attributes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.