ID : MRU_ 439172 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

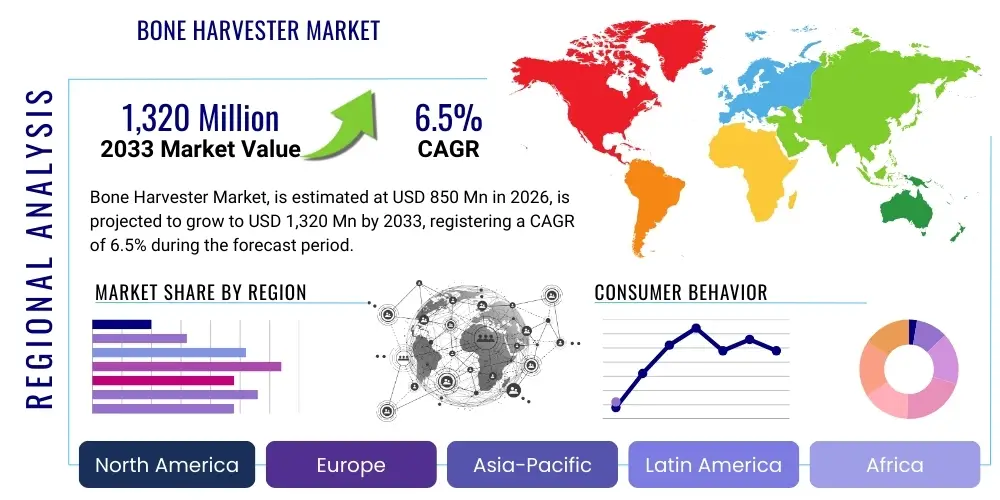

The Bone Harvester Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at $850 Million USD in 2026 and is projected to reach $1,320 Million USD by the end of the forecast period in 2033.

The Bone Harvester Market encompasses specialized medical devices designed for the precise and efficient collection of autogenous bone graft material from a patient’s own body. These devices are crucial in various surgical disciplines, including orthopedics, spinal fusion, trauma reconstruction, craniofacial surgery, and dentistry, where autograft bone remains the gold standard due to its superior osteoinductive, osteoconductive, and osteogenic properties. Modern bone harvesters range from traditional manual curettes and trephines to advanced motorized drills and minimally invasive systems, focusing on maximizing graft volume while minimizing donor site morbidity and operative time.

The core product offerings within this market include specialized aspiration systems, bone mills, manual bone scraping instruments, and sophisticated powered harvesters, such as ultrasonic or piezoelectric devices, which offer enhanced precision, particularly in dense cortical bone harvesting. The primary applications involve filling bone voids, promoting fusion in spinal and orthopedic procedures, and augmenting bone mass prior to dental implant placement. The evolution towards minimally invasive techniques and instruments that can harvest bone chips and slurry efficiently is a major trend driving product development and adoption globally.

Key benefits associated with the utilization of advanced bone harvesters include reduced surgical invasiveness, preservation of bone viability, lower risk of complication at the donor site (such as fracture or chronic pain), and improved patient recovery profiles. The market growth is fundamentally driven by an aging global population prone to degenerative joint and spinal conditions, the increasing incidence of complex trauma requiring bone reconstruction, and continuous technological advancements focused on ergonomic design and higher graft yield quality. These factors collectively underscore the critical role these devices play in modern reconstructive and regenerative surgical procedures.

The Bone Harvester Market is characterized by robust growth, primarily fueled by the increasing volume of spinal fusion procedures and the rising prevalence of orthopedic trauma worldwide. Business trends indicate a strong preference for motorized and piezoelectric bone harvesting systems over traditional manual instruments, driven by the desire for superior graft quality and reduced surgical complexity. Major market players are heavily investing in R&D to develop disposable, single-use harvesters and integration with navigation and robotics systems to enhance precision and sterility, reflecting a key strategy to address infection risks and improve surgical outcomes. The intense competitive landscape necessitates continuous innovation, particularly concerning instruments capable of simultaneously harvesting and preparing the graft material.

Regionally, North America maintains the dominant market share, attributed to established healthcare infrastructure, high reimbursement rates for complex orthopedic surgeries, and rapid adoption of advanced surgical technologies. However, the Asia Pacific (APAC) region is poised for the fastest growth, propelled by expanding medical tourism, improving access to specialized surgical care, and large unmet patient needs in populous countries like China and India. European growth remains steady, anchored by well-defined regulatory frameworks and a focus on cost-effectiveness and outcome-based surgical practices, driving demand for high-efficiency harvesting solutions.

Segment trends highlight the dominance of the orthopedic segment, particularly spinal applications, which require substantial volumes of high-quality autograft. Among device types, motorized systems currently hold a significant market share due to their speed and ability to procure large volumes, but the piezoelectric segment is gaining traction rapidly due to its precise cutting action, which minimizes thermal damage and preserves cell viability. End-user dynamics show hospitals continuing to be the largest revenue generator, although Ambulatory Surgical Centers (ASCs) are rapidly emerging as key growth drivers due to the shift towards outpatient elective procedures, demanding cost-effective and portable harvesting solutions.

User inquiries regarding AI's impact on the Bone Harvester Market predominantly revolve around three key areas: optimizing surgical planning, enhancing robotic precision during harvesting, and integrating data analytics for graft quality assurance. Users are keenly interested in how AI algorithms can analyze patient CT or MRI scans to precisely locate optimal, high-density donor sites (e.g., iliac crest, tibia) pre-operatively, minimizing the risk of insufficient graft yield or donor site complications. Furthermore, there is significant curiosity about the role of robotic arms guided by AI, which could execute the harvesting process with sub-millimeter precision, especially in delicate procedures like craniofacial reconstruction, far exceeding the consistency of manual techniques.

The integration of Artificial Intelligence and Machine Learning (ML) is expected to profoundly influence the workflow associated with autologous bone grafting. AI can analyze vast datasets concerning graft harvest location, patient demographics, and subsequent fusion rates, enabling surgeons to make data-driven decisions about the optimal quantity and quality of bone required for specific procedures. This predictive modeling capability reduces variability and improves the success rate of complex orthopedic and spinal fusions. Furthermore, smart imaging systems integrated with harvesters could use ML to provide real-time feedback on tissue density and viable cell count during the procedure, ensuring maximized graft integrity.

While the physical design of the bone harvesting instrument itself may remain largely mechanical or electromechanical, AI primarily serves as a powerful enabling technology, optimizing the entire surgical journey from pre-operative planning to post-operative quality assessment. This technological synergy promises not only enhanced surgical accuracy but also significant reductions in operative time and donor site morbidity, positioning AI as a crucial element for future innovation and differentiation in the high-precision surgical tools segment. The overall trajectory suggests AI will transition bone harvesting from an experience-based skill to a highly standardized, predictable procedure.

The Bone Harvester Market is actively shaped by strong driving forces, significant restraints, and clear avenues for growth, which together dictate market trajectory and investment priorities. Key drivers include the escalating global burden of orthopedic disorders, particularly spinal degeneration and arthritis, coupled with the proven clinical superiority of autogenous bone grafts over allografts or synthetic substitutes in terms of osteogenesis. Furthermore, ongoing improvements in minimally invasive surgical techniques necessitate the development of corresponding precise harvesting tools that reduce patient recovery time and decrease hospital stays, thereby aligning with modern healthcare economics.

Conversely, the market faces significant restraints, notably the relatively high initial capital investment required for advanced motorized and ultrasonic harvesting systems, which can limit adoption in budget-constrained healthcare environments, particularly in emerging economies. Regulatory hurdles, especially in regions like Europe and the US, demanding rigorous clinical validation for new device clearances, contribute to lengthy product development cycles. Another restraint is the persistent risk of donor site morbidity, even with advanced techniques, which encourages some surgeons to opt for synthetic or allograft alternatives when appropriate, thus capping the total addressable market for autograft harvesting devices.

Opportunities for expansion are prominent in the integration of specialized harvesters with computerized navigation systems, enhancing accuracy and safety during extraction, particularly in anatomically complex areas like the pelvis. The development of cost-effective, disposable versions that address sterility concerns and minimize cross-contamination risks presents a lucrative pathway. Furthermore, leveraging technology transfer from dental implantology, such as advanced piezoelectric bone cutting, into large-scale orthopedic applications represents a substantial opportunity for increasing the quality and viability of harvested graft material, appealing to high-volume surgical centers aiming for superior patient outcomes.

The Bone Harvester Market is comprehensively segmented based on Device Type, Application, and End-User, providing a granular view of demand patterns and technological preferences across various surgical disciplines. The segmentation by Device Type differentiates between manual instruments, which are basic and cost-effective, and powered/motorized systems, which offer speed and high efficiency, alongside the emerging category of piezoelectric and ultrasonic harvesters known for precision and reduced thermal trauma. Analysis across these segments reveals a trend favoring sophisticated, high-precision instruments that minimize patient impact while maximizing graft quality, leading to higher average selling prices (ASPs) in the powered segments.

The application segmentation is crucial, identifying Orthopedic Surgery (further broken down into Spinal Fusion, Joint Reconstruction, and Trauma Surgery) as the dominant revenue contributor, largely due to the high volume and complexity of these procedures requiring substantial bone grafting material. Dental and Maxillofacial applications, including sinus lifts and ridge augmentation, represent a rapidly growing niche, driven by the increasing demand for aesthetic dentistry and implant procedures. Understanding these application needs guides manufacturers in developing specialized instruments tailored for accessing specific donor sites like the ramus or mandibular symphysis.

End-User segmentation clarifies the consumption pattern, with Hospitals dominating the market due to their capacity for high-volume, complex surgeries and access to substantial capital for advanced equipment procurement. However, Ambulatory Surgical Centers (ASCs) are the fastest-growing end-user segment, driven by the shift of less complex procedures to outpatient settings where shorter recovery times and lower costs are paramount. This shift fuels the demand for portable, efficient, and often disposable bone harvesting kits that minimize setup and sterilization overhead.

The value chain for the Bone Harvester Market begins with upstream activities, primarily involving the sourcing of high-grade raw materials such as medical-grade stainless steel, titanium alloys, and specialized plastics required for instrument manufacturing. This initial stage demands rigorous quality control and adherence to ISO standards, given the instruments’ direct contact with human tissue and bone. Key activities in the upstream segment include precision machining, component assembly, and sterilization packaging, typically executed by specialized medical device contract manufacturers or large integrated market leaders. Maintaining intellectual property regarding unique blade designs, motor efficiency, and piezoelectric element integration is critical at this manufacturing stage.

Midstream activities focus on inventory management, centralized warehousing, and logistics, ensuring instruments are readily available for complex surgical scheduling. The distribution channel network forms the critical link between manufacturers and end-users. Direct distribution is common for high-value, complex powered systems, where manufacturers utilize dedicated sales forces to provide specialized training, technical support, and ongoing maintenance contracts to large hospital networks. This approach ensures high profit margins and closer customer relationships but requires substantial operational investment.

Downstream activities predominantly involve indirect distribution through third-party distributors, wholesalers, and specialized medical supply procurement organizations, particularly for manual instruments, disposable components, and lower-volume markets. These indirect channels help manufacturers achieve broader geographic reach, particularly in emerging markets, without incurring the high overhead of a fully localized sales team. The final stage involves the sale and utilization of the bone harvesters within hospitals and ASCs, where procurement decisions are highly influenced by clinical efficacy data, total cost of ownership, and adherence to surgical safety standards, completing the value flow from specialized raw materials to patient care.

The primary customer base for the Bone Harvester Market comprises institutions and highly specialized medical professionals who regularly perform reconstructive and fusion surgeries requiring autogenous bone grafting. These end-users prioritize instruments that offer reliability, high precision, and demonstrated efficacy in minimizing donor site morbidity while maximizing viable graft yield. Hospitals, specifically large university hospitals and Level I trauma centers, represent the largest segment due to their handling of complex orthopedic, neurosurgical, and craniofacial cases that necessitate substantial and high-quality bone graft material.

A rapidly expanding segment of potential customers includes Ambulatory Surgical Centers (ASCs) and specialized outpatient surgical clinics. As procedures like anterior cervical discectomy and fusion (ACDF) and certain dental implant procedures shift to outpatient settings, these centers require bone harvesting solutions that are cost-effective, easy to sterilize, and often disposable, streamlining workflow and reducing overhead. The decision-makers here often focus intensely on the efficiency gains and overall supply chain simplification offered by modern harvesting kits.

The specialized professionals driving demand include orthopedic surgeons (especially spine and trauma specialists), neurosurgeons, oral and maxillofacial surgeons (OMFS), and periodontists. These specialists require instruments tailored to specific anatomical access points—for instance, specialized drills for pedicle screw placement requiring local bone harvest, or fine-tuned piezoelectric tools for dental augmentation procedures. Targeting these key surgical disciplines with instrument customization and specialized training programs is crucial for penetrating specific high-value segments of the market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $850 Million USD |

| Market Forecast in 2033 | $1,320 Million USD |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Stryker Corporation, Zimmer Biomet Holdings Inc., Johnson & Johnson (DePuy Synthes), Arthrex Inc., Becton Dickinson (BD), Osteo Science, KLS Martin Group, Integra LifeSciences Corporation, Geistlich Pharma AG, Hu-Friedy Manufacturing Co., Blackwood Medical, R.O.C. Orthopedic Solutions, Cook Medical, Frios, Meisinger, Osseon, NovaBone. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Bone Harvester Market is currently undergoing a significant technological shift characterized by the move away from basic manual methods toward sophisticated energy-based and motorized systems designed for precision and tissue preservation. A cornerstone of this shift is the adoption of piezoelectric and ultrasonic technology. These devices use micro-vibrations to cut bone selectively, preserving surrounding soft tissues and neurovascular structures, which is highly advantageous in complex fields like spinal and craniofacial surgery. This technology is increasingly valued because it minimizes thermal necrosis, thereby improving the viability of the harvested bone cells, which is crucial for successful fusion outcomes.

Another major technological advancement involves the development of specialized, minimally invasive aspiration and harvesting systems. These systems utilize small diameter cannulas and negative pressure techniques to collect bone marrow and small bone chips simultaneously, often through the same incision used for the primary procedure (e.g., pedicle screw insertion). This reduces the need for a separate, often morbid, secondary donor site incision, aligning perfectly with the overarching trend toward reduced invasiveness in modern surgery. These systems often integrate disposable components to ensure optimal sterility and maintenance-free operation, appealing strongly to ASCs focused on rapid turnover.

Furthermore, digital integration and smart instrumentation are emerging as key differentiating factors. This includes instruments with embedded sensors that provide real-time feedback to the surgeon regarding cutting force, depth, and temperature. Such data integration is foundational for future AI-assisted surgical planning and execution. The competitive edge is increasingly held by manufacturers who can offer a complete system solution, combining precise harvesters with specialized bone preparation devices (e.g., bone mills or crushers) and tailored delivery systems for optimal graft placement, ensuring high consistency across all surgical procedures.

North America currently dominates the Bone Harvester Market, primarily driven by exceptionally high healthcare spending, widespread adoption of advanced surgical techniques, and the presence of leading medical device manufacturers. The region, particularly the United States, benefits from a high volume of spinal and orthopedic procedures resulting from high rates of degenerative disc disease and trauma. Furthermore, favorable reimbursement policies for complex reconstructive surgeries, coupled with a proactive approach to adopting technologically superior, albeit higher-cost, devices like ultrasonic harvesters, solidify its leading position in terms of revenue generation and early market entry for innovations.

Europe represents the second-largest market, characterized by mature healthcare systems and stringent regulatory controls (such as MDR). Growth in Europe is steady, supported by an aging population and increasing demand for joint and spine procedures. Key European countries like Germany, France, and the UK prioritize devices that demonstrate clear cost-effectiveness and improved patient outcomes. The trend here leans toward efficiency and standardization, driving demand for versatile, multi-use, and highly reliable harvesting instruments that meet rigorous clinical standards while managing costs within national healthcare systems.

The Asia Pacific (APAC) region is forecasted to exhibit the highest CAGR during the forecast period. This accelerated growth is primarily attributed to rapidly improving healthcare infrastructure, increasing access to advanced surgical care, and a huge population base with rising disposable incomes, leading to greater acceptance of elective procedures, especially in countries like China, India, and South Korea. While price sensitivity remains a factor, the massive unmet need, combined with growing medical tourism, makes APAC a critical strategic area for global market expansion and the target for manufacturers focusing on developing scaled, mid-range-priced powered harvesting solutions.

Piezoelectric and ultrasonic bone harvesters are highly effective for preserving graft viability. These advanced devices use precise, high-frequency micro-vibrations to cut bone, minimizing thermal damage and preserving osteocytes and surrounding soft tissue structures compared to traditional rotating drills or manual instruments.

The shift to ASCs increases demand for cost-effective, portable, and often disposable bone harvesting systems. ASCs prioritize efficiency and streamlined processes, favoring ready-to-use kits and instruments that require minimal setup and sterilization time, thus driving the disposable segment growth.

The main restraints include the high initial capital cost of purchasing advanced powered and robotic harvesting systems. Additionally, the persistent risk of donor site morbidity (pain, fracture, infection) associated with autograft procedures encourages the use of synthetic or allograft substitutes in certain clinical situations.

Orthopedic Surgery, specifically spinal fusion procedures, holds the largest market share. Spinal fusion requires substantial volumes of high-quality autograft material to ensure successful bony fusion, driving consistent demand for efficient and high-yield bone harvesting devices.

Yes, AI is being leveraged primarily in pre-operative planning to analyze patient imaging (CT/MRI) and precisely identify the optimal donor sites for maximal graft quality and volume, thereby enhancing surgical accuracy and minimizing exploration time.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.