ID : MRU_ 433901 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

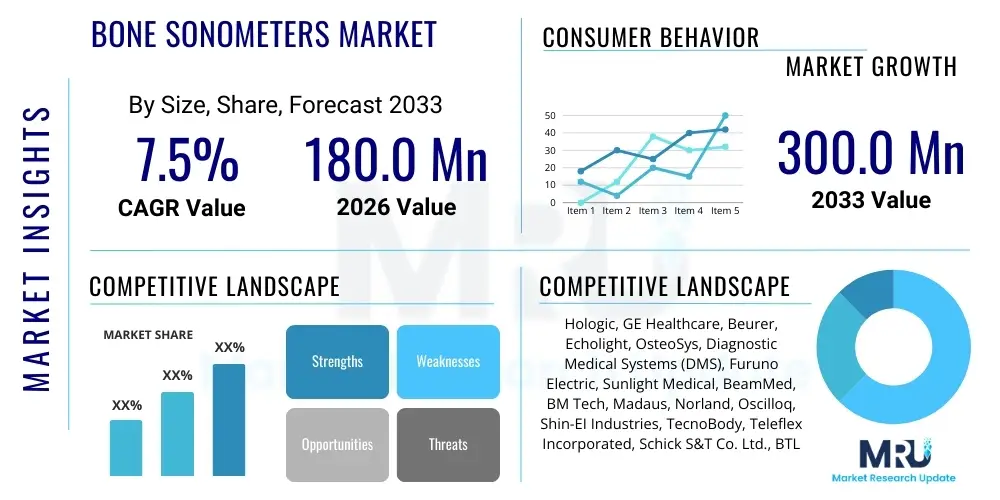

The Bone Sonometers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at $180.0 Million USD in 2026 and is projected to reach $300.0 Million USD by the end of the forecast period in 2033.

The Bone Sonometers Market encompasses the sales and distribution of devices utilizing quantitative ultrasound (QUS) technology for the non-invasive assessment of bone mineral density (BMD) and bone strength, primarily targeting the early diagnosis and management of osteoporosis and other bone health conditions. Bone sonometers measure parameters like broadband ultrasonic attenuation (BUA) and speed of sound (SOS) typically at peripheral skeletal sites such as the heel, tibia, or forearm. These devices offer a distinct advantage over traditional dual-energy X-ray absorptiometry (DXA) scanners due to their portability, lower cost, lack of ionizing radiation, and ease of use in primary care settings and remote areas.

The core product description centers on highly sophisticated yet user-friendly ultrasound devices designed specifically for skeletal assessment. These machines range from compact, handheld units ideal for screening large populations to more stationary, advanced models used in specialized clinics. Major applications include screening programs for postmenopausal women and elderly men at risk of fragility fractures, monitoring the effectiveness of anti-osteoporosis therapies, and evaluating pediatric bone development. The versatility of bone sonometers makes them indispensable tools in preventative medicine, shifting the paradigm from treating fractures to proactive risk stratification.

Key benefits driving market adoption include the accessibility of the technology, facilitating widespread preliminary bone health checks outside expensive hospital environments. Furthermore, the increasing prevalence of geriatric populations globally, coupled with rising awareness about osteoporosis, acts as a primary driving factor. Technological advancements focused on enhancing accuracy, integration with electronic health records (EHR), and miniaturization are continually improving the utility and penetration of these devices across various healthcare tiers, solidifying their role as essential instruments in modern musculoskeletal health diagnostics.

The Bone Sonometers Market demonstrates robust growth propelled by favorable demographics and technological convergence in portable medical diagnostics. Current business trends indicate a strong shift towards portable and handheld devices, which reduces capital expenditure for end-users and expands application scope into retail clinics and community outreach programs. Furthermore, strategic partnerships between device manufacturers and large healthcare systems are accelerating market penetration. Key players are investing heavily in software integration, aiming to provide predictive analytics derived from QUS data, thereby enhancing clinical decision support. The competitive landscape is characterized by moderate fragmentation, with established medical imaging giants competing alongside specialized QUS technology providers, focusing on regulatory approvals for standardized T-scores comparable to DXA measurements.

Regionally, North America and Europe currently dominate the market share, driven by high osteoporosis awareness, advanced healthcare infrastructure, and well-established reimbursement policies for bone density testing. However, the Asia Pacific (APAC) region is poised to exhibit the highest CAGR during the forecast period. This accelerated growth is attributed to massive untapped patient pools, increasing disposable incomes allocated to healthcare, rapid modernization of clinical facilities, and government initiatives aimed at preventative healthcare, particularly in rapidly aging nations like Japan, China, and India. Latin America and the Middle East & Africa (MEA) are also showing promising growth, primarily fueled by infrastructural improvements and rising incidence rates of lifestyle-related bone disorders.

In terms of segments, the Portability segment is undergoing the most significant transformation, with Portable/Handheld Bone Sonometers expected to capture a larger share due to their screening efficiency and logistical advantages. By End-user, Diagnostic Centers and Specialty Clinics are projected to remain the primary revenue generators, owing to their specialized focus on musculoskeletal disorders and high patient throughput. Trend analysis also highlights increasing demand for devices capable of providing multi-site assessments and automated reporting features, streamlining the diagnostic process and mitigating operator variability, which is crucial for achieving consistent clinical outcomes.

Users frequently inquire whether Artificial Intelligence (AI) can replace the need for physical bone density measurements or, conversely, how AI can enhance the accuracy and utility of existing QUS devices. Common concerns revolve around the potential for AI-driven risk models using electronic health record (EHR) data to bypass initial screening devices, and the expectations regarding AI's role in image analysis, calibration, and prediction modeling. The prevailing user theme centers on the integration of machine learning algorithms to reduce measurement variability, improve diagnostic specificity by distinguishing true osteoporosis from other causes of low bone density, and enhance prognostic capabilities, particularly for fracture risk assessment.

AI's primary influence is moving beyond simple data collection to sophisticated data interpretation. Machine learning models are being developed to process raw QUS signals and correlate them more accurately with gold-standard DXA data and actual fracture incidence, minimizing the historical disadvantage of QUS reproducibility. This AI-driven calibration allows for real-time quality control and automated identification of poor scan acquisitions, immediately alerting the technician. Such enhancements significantly elevate the reliability of bone sonometers, positioning them as powerful screening tools that yield actionable clinical intelligence rather than just raw metrics, thus broadening their acceptance among orthopedic specialists.

Furthermore, AI facilitates predictive maintenance and operational efficiency for healthcare providers. Algorithms can analyze device usage patterns, flag potential equipment malfunctions before they occur, and optimize scheduling based on expected patient load and technician availability. From a patient care perspective, AI systems can integrate QUS data with patient comorbidities, genetics, and lifestyle factors available in EHRs to generate personalized, multi-factorial fracture risk scores that are more comprehensive than traditional T-score evaluations alone. This integrated diagnostic power transforms the bone sonometer from a simple measurement tool into a critical element of an AI-powered bone health management system.

The Bone Sonometers Market is primarily driven by the escalating global prevalence of osteoporosis, particularly within aging populations worldwide, demanding accessible, cost-effective screening tools. The major restraints include the perception that QUS devices are less accurate than DXA in measuring central bone density (hip and spine), leading to hesitancy among certain specialist groups regarding their exclusive diagnostic use. Significant opportunities lie in expanding the application of QUS technology beyond basic screening into fields like space medicine, sports medicine, and military health, where portability is critical, and in developing next-generation devices capable of assessing bone microarchitecture. The market is influenced by the interconnected impact forces of technological innovation, regulatory environment, and public health awareness campaigns, all of which dictate the rate of adoption and clinical utility of sonometers.

A central driver is the global initiative to reduce healthcare expenditure by promoting early detection. Bone sonometers offer an attractive economic alternative for initial screening compared to expensive centralized DXA units, thereby increasing patient throughput and reducing the burden on specialized imaging centers. Additionally, strong governmental support and public health campaigns aimed at raising awareness about osteoporotic fracture prevention are fostering increased demand for routine testing, especially in regions previously underserved by advanced diagnostic equipment. The inherent safety of QUS (absence of ionizing radiation) further positions it favorably for serial monitoring of high-risk patients, including children or pregnant women, where DXA is typically avoided.

However, the market faces headwinds from ongoing debates regarding the standardization and interchangeability of QUS results across different device manufacturers and measurement sites. Until QUS measurements are universally recognized as equivalent to DXA T-scores for definitive diagnosis, their role might remain confined primarily to screening and monitoring. To overcome this, market players are pursuing technological breakthroughs, such as developing 3D QUS imaging capabilities and integrating advanced signal processing to improve measurement consistency. These advancements, combined with strategic marketing focusing on the clear benefits of portability and low maintenance, represent significant opportunities for market stakeholders to overcome the perceived limitations and broaden the clinical acceptance of bone sonometry.

The Bone Sonometers Market is primarily segmented based on Technology, Portability, and End-user, offering a comprehensive view of market dynamics across diverse application areas. The segmentation reflects the varied needs of healthcare systems globally, ranging from large centralized hospitals requiring highly accurate static devices to mobile health units demanding lightweight, battery-operated systems. Understanding these segments is crucial for strategic planning, as distinct market drivers and competitive landscapes exist within each category. For instance, the demand for portable units is primarily volume-driven (screening), whereas the demand for advanced desktop units is precision-driven (diagnostic support).

Technology segmentation is predominantly focused on Quantitative Ultrasound (QUS), often subdivided by the measurement site—calcaneal (heel) measurement being the most common due to its similarity in composition to trabecular bone structure and ease of access. Advances within QUS are focusing on improving the transducer design and incorporating sophisticated algorithms for better signal processing, moving towards technologies that can provide data related to bone elasticity and microarchitecture, not just density surrogates. These innovations are critical for distinguishing osteoporosis severity and predicting fracture risk more accurately than traditional QUS metrics.

The End-user segmentation reveals that hospitals and specialized diagnostic centers maintain the largest share, leveraging their existing infrastructure for diagnostics. However, the fastest growth is anticipated in the clinic and physician office setting, driven by the increased availability of cost-effective, user-friendly portable sonometers. This shift allows primary care physicians to integrate bone health assessments into routine physical examinations, significantly improving early detection rates and enabling timely intervention, which aligns with preventative healthcare goals worldwide. The increasing investment in research and academic institutions for clinical trials and large-scale epidemiological studies also contributes substantially to the End-user segment growth.

The value chain for the Bone Sonometers Market begins with the upstream activities centered on raw material procurement, specialized transducer manufacturing, and sophisticated sensor and software development, requiring high R&D investment. Critical components include ultrasonic crystals, signal processing microchips, and biocompatible materials for contact surfaces. Upstream complexity is high due to the necessity of meeting stringent medical device standards (ISO 13485, FDA/CE marking). Key success factors at this stage involve securing intellectual property for patented QUS technology and maintaining tight control over component quality to ensure measurement accuracy and device longevity, influencing the overall cost of goods.

Midstream activities involve the assembly, manufacturing, and calibration of the final sonometer systems. Manufacturers focus on lean production processes and effective integration of advanced software features, including user interfaces, patient databases, and connectivity solutions (EHR integration). Strict quality assurance protocols are mandatory, focusing on the reproducibility and reliability of the output measurements. Distribution channels form the crucial link to downstream customers. Direct sales forces are often used for high-value contracts with large hospital chains, providing personalized technical support and training. Conversely, indirect channels, relying on specialized medical equipment distributors and regional resellers, are essential for penetrating geographically dispersed markets, particularly clinics and smaller diagnostic centers.

Downstream analysis focuses on installation, training, maintenance, and post-sales support provided to end-users (Hospitals, Clinics). The effectiveness of the service network significantly influences customer satisfaction and loyalty. For portable devices, the service requirement is generally lower, but software updates and recalibration services are paramount. Potential customers (End-users/Buyers) prioritize ease of use, speed of measurement, and clinical acceptance (correlation with DXA). Successful market players ensure comprehensive training programs to mitigate operator error, which is a major factor in QUS measurement variability, thereby maximizing the clinical utility of the devices in real-world settings.

The primary potential customers for Bone Sonometers are institutions and practitioners dedicated to musculoskeletal health, preventative care, and geriatric medicine. These include large tertiary care hospitals that use sonometers as a high-throughput screening adjunct to their existing DXA services, and specialized diagnostic imaging centers that offer comprehensive bone health assessments. The strategic appeal to hospitals lies in the ability to decentralize initial bone density checks, reserving expensive DXA time for definitive diagnosis and treatment planning, thereby optimizing resource allocation and improving patient flow efficiency.

A rapidly expanding customer base includes private specialty clinics, such as endocrinology, rheumatology, and orthopedic offices, where practitioners seek convenient, immediate bone health insights for at-risk patients during routine consultations. The portability and low operational footprint of handheld sonometers make them highly attractive for these settings, allowing physicians to offer immediate screening without the need for patient referral to an imaging center. Furthermore, corporate wellness programs and senior living facilities represent emerging high-volume buyers, leveraging sonometers for proactive, on-site health evaluations and risk management within their resident or employee populations.

Finally, governmental and non-governmental public health organizations are significant purchasers, especially in developing economies or rural areas. These organizations utilize portable sonometers for community outreach and large-scale epidemiological studies aimed at quantifying bone health deficiencies and implementing preventative measures. The cost-effectiveness and mobility of the devices are ideal for these population-level screening initiatives, providing crucial data for national health planning and resource deployment targeted at reducing the societal burden of fragility fractures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $180.0 Million USD |

| Market Forecast in 2033 | $300.0 Million USD |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hologic, GE Healthcare, Beurer, Echolight, OsteoSys, Diagnostic Medical Systems (DMS), Furuno Electric, Sunlight Medical, BeamMed, BM Tech, Madaus, Norland, Oscilloq, Shin-EI Industries, TecnoBody, Teleflex Incorporated, Schick S&T Co. Ltd., BTL Industries, Meditech Equipment, Kono-Kizai Manufacturing. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Bone Sonometers Market is dominated by Quantitative Ultrasound (QUS) technology, which utilizes sound waves to characterize bone density and structure, typically focusing on the calcaneus (heel). The technology relies on two main parameters: the Speed of Sound (SOS), which measures bone elasticity and stiffness, and Broadband Ultrasound Attenuation (BUA), which assesses the frequency-dependent loss of ultrasonic energy as it passes through bone. Modern sonometers have drastically improved signal processing capabilities, moving from simple transmission methods to advanced algorithms that correct for soft tissue artifacts and improve the correlation between QUS indices and true bone mineral density measured by DXA, thereby enhancing clinical relevance and reliability.

Current technological advancements are concentrating on developing multi-site measurement capabilities, allowing clinicians to assess bone health at different peripheral sites (e.g., tibia, radius) simultaneously, providing a more holistic view of skeletal status. Furthermore, the push towards miniaturization and wireless connectivity is transforming device usability. Handheld devices are increasingly being designed with intuitive touchscreens, long battery life, and secure data transmission protocols, facilitating seamless integration into mobile medical units and primary care settings. This focus on portability ensures that the technology can reach underserved populations and be used effectively in point-of-care scenarios, reducing the logistical barriers associated with traditional centralized imaging systems.

The future technology landscape is moving towards integrating advanced features such as 3D Quantitative Ultrasound (3D-QUS) and techniques aimed at evaluating bone microarchitecture directly, mimicking the detailed insights provided by high-resolution peripheral quantitative computed tomography (HR-pQCT) but without the radiation exposure. This involves using sophisticated transducer arrays and advanced beamforming techniques to reconstruct 3D models of the bone structure. The integration of AI and deep learning into the device software is another critical trend, enabling automated image interpretation, enhanced diagnostic reporting (e.g., automatically calculating estimated T-scores and Z-scores), and real-time feedback on measurement quality, minimizing inter-operator variability and ensuring high standardization across diverse clinical environments.

Bone Sonometers use Quantitative Ultrasound (QUS) to measure bone stiffness and density surrogates non-invasively, primarily at the heel, without utilizing ionizing radiation. DXA (Dual-Energy X-ray Absorptiometry) is the gold standard, using low-dose X-rays to directly measure bone mineral density (BMD) at central sites like the hip and spine.

Bone Sonometers are highly reliable and effective for initial screening, identifying individuals at high risk of low BMD and subsequent fracture. While they provide valuable data, definitive diagnosis and treatment initiation often require confirmation via a central DXA scan, as per international clinical guidelines.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR), driven by large, aging populations, increasing healthcare accessibility, and government investments in preventative health screening programs in countries such as China and India.

Portability is a critical driver, allowing Bone Sonometers (handheld and portable units) to be used efficiently in primary care clinics, remote medical settings, community health fairs, and physician offices. This accessibility significantly lowers screening costs and expands patient reach beyond centralized hospital facilities.

AI integrates by enhancing diagnostic accuracy through machine learning algorithms that process raw QUS data for improved correlation with DXA standards. AI also enables automated quality control, generates predictive fracture risk scores, and streamlines clinical reporting, minimizing human variability in measurements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.