ID : MRU_ 435759 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

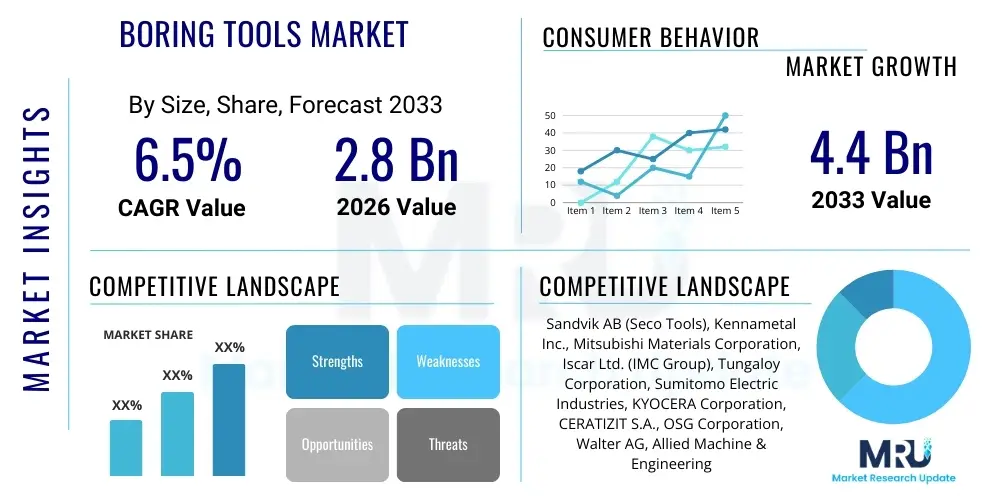

The Boring Tools Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 2.8 Billion in 2026 and is projected to reach USD 4.4 Billion by the end of the forecast period in 2033.

The Boring Tools Market encompasses specialized cutting instruments designed to enlarge, finish, or enhance the concentricity and straightness of existing holes in various workpieces, primarily within high-precision manufacturing environments. These tools are indispensable components of modern computer numerical control (CNC) machines, serving critical applications across diverse industries, including automotive, aerospace, heavy machinery, and energy. Product offerings range from basic fixed boring bars to sophisticated modular systems that allow for micro-adjustment and optimization for specific materials and surface finish requirements. The market is defined by continuous innovation in insert geometry, tool materials (carbides, ceramics, cermets), and advanced coating technologies (such as PVD and CVD) aimed at improving tool life, enhancing material removal rates, and achieving tighter dimensional tolerances.

Major applications of boring tools involve engine blocks, transmission cases, hydraulic components, landing gear structures, and turbine components where precise internal diameters are crucial for operational integrity and performance. The primary benefit derived from the use of advanced boring tools is the unparalleled accuracy they provide, often achieving tolerances in the micron range, which is critical for assembly efficiency and component longevity. Furthermore, the development of dampening systems integrated into boring bars helps mitigate vibration, enabling deeper cuts and improved surface finishes, particularly when dealing with difficult-to-machine materials like titanium alloys and high-nickel superalloys prevalent in demanding sectors like aerospace and medical device manufacturing.

Key driving factors accelerating the market growth include the global expansion of the manufacturing sector, particularly in emerging economies focusing on advanced industrial production and infrastructure projects. The increasing adoption of high-performance materials that necessitate specialized tooling, combined with the rising demand for lightweight and precision components in the automotive and aerospace industries, significantly boosts the need for advanced boring solutions. Furthermore, the ongoing digitalization of manufacturing, characterized by the integration of smart tooling and real-time monitoring capabilities, enhances the efficiency and productivity derived from high-end boring tools, thereby sustaining market momentum across all major geographical regions.

The Boring Tools Market exhibits robust business trends driven primarily by the global shift towards high-mix, low-volume manufacturing requiring extreme precision, coupled with the relentless pursuit of automation in machine shops worldwide. Key market players are heavily investing in modular tooling systems, digital connectivity features, and materials science breakthroughs to address the complexity introduced by advanced, difficult-to-machine alloys. Strategic mergers and acquisitions are shaping the competitive landscape, allowing major corporations to consolidate specialized expertise and expand their regional footprints, particularly in fast-growing industrial hubs in Asia Pacific. The necessity for reduced cycle times and improved tool utilization rates is propelling the demand for multi-functional tools that can handle roughing and finishing operations efficiently.

Regional trends indicate that Asia Pacific (APAC), led by manufacturing powerhouses like China, India, and Japan, represents the largest and fastest-growing segment, propelled by massive investments in automotive manufacturing, electronics production, and infrastructure development. North America and Europe maintain strong demand for premium, high-performance boring solutions, largely dictated by stringent quality standards in aerospace and medical device production, where highly sophisticated and customized tooling is preferred. Regulatory trends promoting energy efficiency and lightweight vehicle construction further reinforce the need for advanced tooling capable of processing intricate engine and chassis components effectively, thus maintaining consistent growth trajectory across mature markets.

Segmentation trends highlight the increasing dominance of modular boring systems, valued for their flexibility, quick change capabilities, and cost-effectiveness across varied batch sizes, offering a strong alternative to traditional solid tooling. Material-wise, carbide inserts remain the bedrock of the market due to their excellent wear resistance, though specialized materials like cermet and polycrystalline diamond (PCD) are seeing heightened demand in applications requiring exceptional surface finish or processing non-ferrous materials. Application-wise, the automotive sector retains the largest market share, though the aerospace and defense segments contribute significantly to the revenue generation of high-end, premium-priced product categories, emphasizing quality over volume.

User queries regarding the impact of Artificial Intelligence (AI) on the Boring Tools Market frequently revolve around predictive maintenance capabilities, optimization of cutting parameters, and the integration of smart tools within the Industry 4.0 framework. Users are concerned about how AI can maximize tool life, minimize unplanned downtime, and autonomously adjust feed rates and spindle speeds based on real-time feedback from sensors embedded in the machine or tool holder. Key themes include the implementation of machine learning algorithms to analyze acoustic emission, vibration data, and power consumption patterns to detect impending tool failure or surface finish degradation long before human operators can perceive issues. Furthermore, there is significant interest in how AI can streamline the tool selection and process planning phase, particularly for complex, multi-stage boring operations involving tight tolerances on exotic materials, leading to faster setup and greater consistency across production batches.

The dynamics of the Boring Tools Market are governed by a robust interaction between technological drivers and market constraints, creating significant opportunities for innovation. The primary drivers stem from the global manufacturing imperative for tighter tolerances and higher throughput, particularly in sectors demanding precision engineering, such as aerospace, medical implants, and high-performance automotive parts. The growing adoption of advanced CNC machining centers capable of utilizing sophisticated, high-speed tooling further necessitates corresponding advancements in boring tool design, specifically focusing on vibration dampening and thermal stability. These factors, combined with the industry-wide push for sustainability and resource efficiency, which favors tools with extended service life, exert substantial upward pressure on market growth.

Conversely, the market faces notable restraints, including the high initial investment required for premium modular boring systems and specialized tools, which can be prohibitive for small and medium-sized enterprises (SMEs). Furthermore, the complex expertise required to operate and maintain high-precision boring machinery and associated digital tooling represents a significant barrier to entry and requires continuous investment in skilled labor training. Economic volatility and disruptions in the global supply chain for crucial raw materials, such as tungsten carbide and cobalt, also pose risks, potentially leading to increased production costs and delays in tool availability, which affects overall market stability and pricing dynamics.

Opportunities for growth are concentrated in the development and commercialization of additive manufacturing techniques for producing specialized boring tool bodies and holders with intricate internal geometries for weight reduction and coolant delivery optimization. The expansion of emerging markets and the subsequent growth of their domestic manufacturing bases present substantial avenues for market penetration. The major impact forces shaping the competitive environment include the rapid obsolescence cycle of standard tooling due to continuous materials science breakthroughs, the increasing criticality of localized technical support and service provision, and the pressure from end-users demanding integrated solutions (tooling, software, and application support) rather than standalone products, shifting the market focus from mere product sales to comprehensive solution provision.

The Boring Tools Market is comprehensively segmented based on product type, material, application, and end-user industry, reflecting the diverse and specialized requirements of the precision manufacturing sector. The product type segmentation distinguishes between highly flexible modular systems and specialized fixed boring tools, with the former gaining significant traction due to its adaptability across various machining tasks. Material segmentation highlights the reliance on cemented carbide for general-purpose applications while emphasizing the strategic adoption of superhard materials like PCD and CBN for demanding applications involving abrasive or hardened materials. Understanding these segment dynamics is critical for market players aiming to tailor their product development strategies and focus their distribution efforts on high-growth niche areas within specific end-user verticals globally.

The value chain for the Boring Tools Market begins with the upstream suppliers responsible for sourcing and processing critical raw materials, predominantly tungsten, cobalt, and various synthetic diamond and nitride powders essential for producing high-quality inserts and tool bodies. This upstream segment is highly concentrated and crucial, as the quality and cost volatility of these inputs directly impact the final tool performance and pricing structure. Key activities here include powder metallurgy, coating application research, and the synthesis of superhard materials. Strong relationships with reliable raw material suppliers are vital for ensuring stable production, particularly in periods of commodity price fluctuations or geopolitical uncertainty affecting mineral supply chains, mandating strategic long-term sourcing agreements.

The midstream component involves the design, manufacturing, and assembly of the boring tools, where technological differentiation and intellectual property play a crucial role. Leading manufacturers invest heavily in R&D to develop advanced geometry inserts, modular coupling systems, and internal coolant delivery mechanisms. Manufacturing processes utilize highly specialized CNC grinding and balancing equipment to ensure the micron-level precision required for modern machining. The distribution channels form the crucial link to the downstream users, involving a combination of direct sales forces for large, strategic accounts and extensive networks of specialized industrial distributors and resellers. These distributors provide localized stock, technical application support, and rapid delivery services, particularly important for ensuring tool availability and minimizing customer downtime.

The downstream analysis focuses on the end-users, primarily machine shops, integrated manufacturers, and specialized component producers. Direct sales channels are typically preferred for high-volume users requiring custom or complex tooling solutions and ongoing technical consultation, particularly in aerospace or energy sectors where tooling performance is critical. Indirect distribution, leveraging local industrial supply houses, dominates the sale of standardized or replacement tooling to smaller machine shops and general manufacturing environments. The efficiency and quality of post-sale services, including regrinding, recoating, and application engineering support, significantly influence customer loyalty and repeat business throughout the entire value chain structure.

The primary consumers and end-users of boring tools are highly sophisticated manufacturing entities that require precise hole-making capabilities across a wide range of materials and dimensional specifications. The most significant customer base resides within the automotive industry, encompassing original equipment manufacturers (OEMs) and their extensive network of Tier 1 and Tier 2 suppliers, focused on mass production of engine blocks, cylinder heads, transmission housings, and brake components. These customers prioritize high-speed machining, tool reliability, and cost-per-part optimization, driving demand for automated and durable boring solutions tailored for high-volume output and demanding material processing specifications, often involving aluminum and cast iron alloys.

The second major cohort includes the aerospace and defense sectors, where the fabrication of complex structural components, turbine parts, and landing gear necessitates the highest level of accuracy and surface integrity, particularly when machining challenging materials like titanium, Inconel, and various superalloys. These customers are willing to invest in premium, application-specific tools, such as vibration-dampened boring bars and specialized CBN/PCD inserts, where tooling cost is secondary to component quality assurance and operational safety. This segment drives innovation towards high-performance materials and advanced monitoring systems, demanding comprehensive engineering support from tool suppliers.

Furthermore, heavy machinery manufacturers (e.g., construction equipment, agricultural machinery, mining equipment) and energy producers (e.g., oil and gas valve manufacturing, power generation turbine components) represent substantial market potential. These industries require large-diameter boring capabilities and tools engineered for robustness and endurance, often dealing with heavy components and tough materials under extreme conditions. Tooling solutions must accommodate large bore diameters while maintaining strict tolerances and surface requirements critical for the functionality and reliability of heavy-duty mechanical systems, such as large hydraulic cylinders, gearboxes, and oversized manifold blocks.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 4.4 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sandvik AB (Seco Tools), Kennametal Inc., Mitsubishi Materials Corporation, Iscar Ltd. (IMC Group), Tungaloy Corporation, Sumitomo Electric Industries, KYOCERA Corporation, CERATIZIT S.A., OSG Corporation, Walter AG, Allied Machine & Engineering, KOMET Group, BIG KAISER Precision Tooling, Mapal Dr. Kress KG, Star Cutter Company, Hanita Cutting Tools, NAREX R&D, Ingersoll Cutting Tools. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The contemporary technological landscape of the Boring Tools Market is defined by the synergistic evolution of materials science, digital integration, and mechanical design innovations aimed at maximizing precision and extending tool longevity under increasingly harsh operational conditions. A critical technological advancement is the widespread deployment of advanced PVD (Physical Vapor Deposition) and CVD (Chemical Vapor Deposition) coatings. These multi-layer coatings, often incorporating materials like titanium aluminum nitride (TiAlN) and diamond-like carbon (DLC), significantly enhance the thermal stability, wear resistance, and lubricity of carbide inserts, allowing for dramatically increased cutting speeds and feeds, particularly when dry machining or processing heat-resistant superalloys (HRSA). The continuous refinement of insert geometries, including chip breakers optimized for better chip evacuation and reduced cutting forces, is also central to improving performance.

Modular tooling systems represent a foundational shift in tool design, moving away from monolithic, fixed tools towards highly adaptable, quick-change systems utilizing robust connections like polygonal shank coupling (PSC) or proprietary taper interfaces. This modularity allows for rapid configuration adjustments, optimizing tool length and diameter combinations for specific bore specifications without the need to stock an excessive inventory of specialized, fixed tools. Furthermore, dynamic dampening technology, featuring internal elastomer or hydraulic systems, is increasingly integrated into long-reach boring bars. This technology actively counteracts vibration and chatter, enabling stable, high-quality deep-hole boring operations that were previously challenging or impossible to execute while maintaining required surface finishes and concentricity within acceptable limits for critical components.

The integration of Industry 4.0 elements is rapidly transforming the technology landscape. This includes the development of smart boring tools embedded with micro-sensors for real-time monitoring of temperature, vibration, and torque. Data collected from these sensors is transmitted wirelessly to the machine control unit and sophisticated monitoring software, often leveraging AI for analysis. This digital integration facilitates proactive adjustments to cutting conditions, provides accurate data for predictive maintenance scheduling, and enables comprehensive tool life management. Advanced simulation software and digital twin technologies are also being utilized extensively during the design phase, allowing manufacturers to simulate cutting dynamics and optimize tool performance before physical prototyping, significantly reducing development cycles and costs while enhancing precision capabilities.

Market growth is primarily driven by the increasing demand for high-precision components in critical sectors like automotive and aerospace, the global push towards automated and high-speed CNC machining processes, and continuous advancements in tool materials and coatings that enhance durability and cutting efficiency.

Modular boring systems utilize interchangeable components (heads, shanks, couplings) allowing for rapid adjustment of length and diameter, offering superior flexibility and inventory reduction compared to traditional fixed boring bars, which are monolithic and less adaptable to varying bore specifications.

The Automotive industry consistently holds the largest market share due to its massive scale of production requirements for engine blocks, cylinder heads, and transmission parts that necessitate continuous, high-volume, precision hole-making operations.

Advanced PVD and CVD coatings, such as TiAlN and AlCrN, are crucial for enhancing the performance of boring inserts by significantly increasing their surface hardness, wear resistance, and thermal stability, allowing tools to operate effectively at higher cutting speeds and feeds for extended periods.

Key constraints include the high capital expenditure required for adopting advanced CNC machines and modular tooling systems, volatility in the supply and pricing of essential raw materials (tungsten carbide), and the persistent shortage of highly skilled technical personnel capable of optimizing complex boring operations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.