ID : MRU_ 435694 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

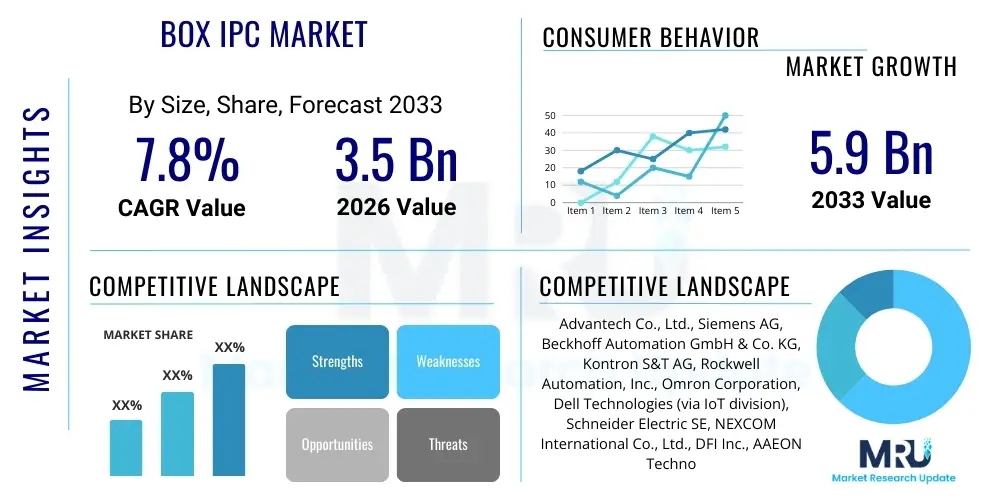

The Box IPC Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 5.9 Billion by the end of the forecast period in 2033.

The Box Industrial PC (IPC) market defines the segment of industrial computing characterized by compact, ruggedized, and often fanless enclosures, specifically engineered to operate reliably in highly challenging operational technology (OT) environments. These devices represent the backbone of modern industrial control systems, serving as powerful computing nodes for data acquisition, real-time control, edge processing, and gateway functions between sensors and enterprise cloud systems. Unlike standard commercial PCs, Box IPCs feature specialized componentry—including wide-temperature tolerance processors (such as Intel Atom, Core i, or specialized ARM SoCs), highly durable solid-state storage, and advanced thermal dissipation systems—ensuring high availability and minimal maintenance requirements across diverse applications ranging from deep sea monitoring to intense factory automation floors.

Box IPCs are fundamentally defined by their flexibility and resilience. They typically incorporate rich, highly customizable I/O interfaces, allowing them to communicate effectively across proprietary industrial protocols (like PROFINET, Modbus, EtherCAT) and modern standards (Gigabit Ethernet, 5G). This essential feature allows manufacturers to integrate new digital capabilities without completely dismantling entrenched legacy infrastructure. The robust design includes high levels of ingress protection (IP ratings), shielding against dust, moisture, vibration, and electromagnetic interference, attributes crucial for sectors like oil and gas, utilities, transportation, and heavy manufacturing. The inherent modularity, supporting quick integration of AI accelerators, specialized vision processing cards, or additional communication modules, positions the Box IPC as the critical pivot point in Industry 4.0 deployments.

The market trajectory is powerfully driven by the global imperative for digital transformation, specifically the migration toward decentralized processing architectures required by the Industrial Internet of Things (IIoT). Companies are moving data processing closer to the source (the edge) to minimize latency, a requirement that Box IPCs optimally satisfy. Key driving factors include the escalating demand for high-speed automated quality control leveraging machine vision, the necessity for sophisticated predictive maintenance solutions relying on localized AI inference, and global regulatory compliance demanding more accurate and auditable data logging from industrial processes. These drivers, combined with the inherent benefits of low power consumption and extended product lifecycles (often exceeding 10 years), ensure Box IPCs are indispensable for mission-critical industrial applications globally.

The Box IPC market is characterized by intense technological evolution and a competitive landscape dominated by established industrial automation conglomerates and specialized embedded computing firms. Current business trends emphasize the development of highly optimized software stacks integrated with hardware, focusing on containerization and virtualization capabilities to manage multiple workloads (control, visualization, AI) concurrently on a single Box IPC unit. Geopolitical factors, particularly trade tensions and supply chain risks, are accelerating regionalization of manufacturing and prompting end-users to prioritize vendors who offer robust supply continuity and component lifecycle assurances, favoring providers known for vertical integration or strong regional manufacturing bases. Moreover, market profitability is increasingly linked to offering comprehensive lifecycle services, including cloud-based device management and mandatory cybersecurity updating protocols.

From a geographical perspective, Asia Pacific maintains its lead in volume consumption, propelled by large-scale capital expenditure in new industrial capacity, especially across robotics, EV production, and semiconductor fabrication. This region's demand profile leans towards cost-competitive, high-performance systems. Contrastingly, North America and Western Europe focus on quality, complexity, and specialized certifications (e.g., ATEX for hazardous environments). These mature markets are driving innovation in specific high-margin niches, such as high-performance computing for advanced medical equipment and defense applications, prioritizing systems with superior cybersecurity resilience and adherence to strict functional safety standards (e.g., IEC 61508). Emerging markets, while smaller, offer rapid growth opportunities linked to infrastructure modernization in telecommunications and energy sectors.

Segment trends confirm the definitive shift toward fanless Box IPCs, which are now standard across most industrial environments due to maintenance and reliability benefits. Performance-wise, there is a clear segmentation emerging: low-power ARM-based systems for simple IIoT gateway functions, and high-performance x86 systems (utilizing Intel Core i7/i9 or similar high-TDP processors) augmented with dedicated accelerators to handle complex AI workloads. The most influential end-user segment growth is forecast in automotive (due to complex EV battery manufacturing demands) and the energy sector (driven by smart grid rollout and renewable energy plant automation). This structural evolution necessitates that manufacturers continually shrink form factors while simultaneously boosting computational density and thermal efficiency.

The primary architectural challenge users face when implementing AI in operational environments is bridging the gap between computational necessity and environmental robustness. Users frequently inquire about the feasibility of running large, sophisticated neural networks (like complex vision transformers or recurrent neural networks for time-series analysis) directly on a compact Box IPC, asking specifically about the trade-offs between utilizing general-purpose CPU cores, integrated GPUs, or dedicated hardware accelerators (such as FPGAs or custom ASICs). Key themes also revolve around model deployment and lifecycle management: how can models be securely updated and optimized over-the-air in vast fleets of geographically dispersed Box IPCs, and what is the required software overhead for deploying standardized AI frameworks (e.g., TensorFlow, PyTorch) within constrained industrial operating systems?

AI’s influence is moving Box IPCs beyond simple controllers into sophisticated decision-making engines. The market is seeing accelerated demand for systems capable of handling specific AI tasks: firstly, in industrial inspection, where high-resolution machine vision requires multi-gigabit camera inputs and rapid GPU-accelerated processing for flaw detection; and secondly, in predictive maintenance, where complex algorithms analyze vibration, temperature, and current draw data streams to forecast equipment wear. These applications demand Box IPCs equipped with high-throughput data buses (PCIe Gen4) and robust cooling to ensure sustained peak performance, especially crucial for continuous, high-speed production lines where a momentary processing lag can lead to significant quality control failures or catastrophic equipment breakdown. This shift mandates substantial investment in AI-ready hardware platforms by leading manufacturers.

Furthermore, the integration of AI directly impacts system complexity and, consequently, security. As Box IPCs become repositories for intellectual property (in the form of proprietary AI models) and controllers for critical infrastructure, they become prime targets for cyber threats. Manufacturers are responding by embedding advanced security features, including AI-specific protection layers, secure boot mechanisms, and comprehensive endpoint detection and response (EDR) capabilities directly into the industrial-grade operating system layer. The future success of AI in the Box IPC domain hinges on developing standardized, secure, and easily deployable software ecosystems that simplify the transition for industrial engineers accustomed to legacy programming environments like ladder logic and functional block diagrams. The complexity of model quantization and optimization for edge deployment remains a significant technical hurdle that market leaders are actively addressing through specialized SDKs.

The Box IPC market growth engine is driven primarily by the global strategic prioritization of industrial automation, underpinned by technological advancements in silicon design that allow greater processing power in smaller, more thermally efficient packages. Drivers include the increasing adoption of robotics, which requires powerful, low-latency control systems, and the strict requirement for data integrity and archival in highly regulated industries such as pharmaceuticals and energy. The inherent reliability and extended maintenance cycles offered by ruggedized Box IPCs provide a strong ROI justification compared to maintaining less durable commercial hardware in demanding environments, making them a default choice for greenfield industrial projects seeking optimal operational expenditure over time.

However, market expansion is significantly constrained by structural challenges, most notably the high initial acquisition cost, which is difficult for small and mid-sized enterprises (SMEs) to absorb, despite the long-term benefits. A persistent restraint is the skill gap within the industrial workforce; deploying and maintaining complex, AI-enabled IPCs requires specialized IT/OT convergence expertise that is often scarce, slowing down adoption rates, particularly in developing regions. Furthermore, the reliance on proprietary operating systems and vendor-specific configuration tools can create vendor lock-in, posing integration risks and flexibility issues for large corporations managing diverse industrial asset portfolios. The rapidly evolving cybersecurity threat landscape poses a perpetual restraint, as interconnected IPCs present new attack vectors into previously isolated industrial control networks, demanding constant and costly security updates.

The key opportunities lie in capitalizing on future infrastructure upgrades. The large-scale deployment of 5G across industrial campuses will unlock new use cases for wireless monitoring and mobile robotics, significantly broadening the operational scope of Box IPCs. The integration of Time-Sensitive Networking (TSN) is poised to standardize deterministic communication, allowing Box IPCs to replace numerous dedicated hardware controllers with fewer, more flexible, and software-defined units, optimizing system architecture and reducing hardware costs in the long run. Moreover, focusing on modular Box IPC designs that allow hot-swappable components and simple field upgrades offers vendors a competitive edge by lowering the total cost of ownership and extending system utility, particularly appealing to industries with very long equipment replacement cycles.

The Box IPC market is structurally segmented based on crucial technological and application criteria, including type, component, technology, end-user industry, and region. Analyzing these segments provides a granular view of market dynamics, revealing where investment and innovation are concentrated. Key segment drivers include the shift toward higher processing power components to support edge AI, the increasing preference for fanless and ultra-ruggedized designs in harsh environments, and the dominant adoption rates seen within the discrete and process manufacturing sectors. The market differentiation is increasingly defined by the ability of vendors to deliver highly customizable, modular, and cyber-secure solutions tailored precisely to specific industrial standards and regulatory compliance requirements.

The distinction between component segmentation, such as CPU architecture (e.g., x86 vs. ARM), is critical as end-users select processors based on the balance between power consumption, thermal efficiency, and raw computational demand. The fastest-growing segments are those facilitating advanced automation, particularly within automotive manufacturing (driven by the EV transition) and the semiconductor industry, which requires extreme precision and minimal operational variability. Geographic segmentation highlights the strategic importance of the APAC region as a manufacturing superpower, dictating global volume, while North America and Europe lead in terms of technological adoption of high-value, high-margin, specialized Box IPC deployments for highly regulated or safety-critical applications.

The Box IPC market value chain begins with upstream activities involving foundational component suppliers, predominantly semiconductor manufacturers (Intel, AMD, ARM), memory providers (Samsung, Micron), and specialized sensor manufacturers. This upstream segment is highly concentrated and dictates the pace of technological advancement, particularly concerning processing power and efficiency. Suppliers in this phase face intense R&D pressure to produce ruggedized, long-lifecycle components that meet industrial standards, requiring rigorous quality control and specialized industrial grade material selection, distinct from consumer electronics components.

Midstream activities involve the Box IPC manufacturers themselves (e.g., Advantech, Siemens, Beckhoff). These players are responsible for system integration, industrial design (focusing on heat dissipation and ingress protection, such as IP ratings), specialized BIOS/firmware development, and rigorous industrial testing and certification. This stage adds significant value through proprietary engineering, offering customizable configurations and ensuring the hardware integrates seamlessly with standard industrial operating systems (e.g., Windows IoT, real-time Linux distributions). Distribution channels are critical in delivering the final product. Direct sales channels are often used for major industrial accounts requiring extensive technical consultation and customized solutions. Indirect channels, involving specialized industrial distributors and system integrators (SIs), facilitate wider market penetration, particularly for smaller clients or standard product configurations, with SIs adding value through installation, software integration, and post-sales support.

Downstream activities include the deployment of Box IPCs by end-users (e.g., automotive factories, utility companies) and the subsequent service and maintenance phases. The downstream relies heavily on System Integrators (SIs) who tailor the hardware to specific application requirements, integrating it into complex OT networks, and developing application-specific software. Post-deployment services, including long-term technical support, warranty services, and lifecycle management (often extending beyond ten years), are vital, cementing the relationship between the manufacturer and the end-user. The overall value chain emphasizes robustness, customization, technical support, and extended product availability over pure cost minimization, reflecting the mission-critical nature of the applications.

Potential customers for Box IPCs are organizations operating within demanding, data-intensive industrial or harsh physical environments where standard commercial computers are unreliable or fail to meet necessary performance and durability metrics. The primary end-users are large multinational manufacturing corporations involved in discrete processes, such such as automotive assembly, electronics fabrication, and aerospace manufacturing, where high uptime and real-time control are paramount. These customers utilize Box IPCs as dedicated machine controllers, quality inspection systems running AI/vision algorithms, and secure data aggregation points for plant-wide monitoring.

Beyond traditional manufacturing, significant adoption comes from critical infrastructure sectors. Energy companies (power generation, smart grid operators) and utility providers (water treatment, distribution networks) require rugged IPCs for remote monitoring, substation automation, and SCADA system optimization in environments prone to electromagnetic interference and extreme weather. Similarly, the transportation sector, including rail, marine, and complex logistics hubs, uses Box IPCs for rolling stock control, trackside monitoring, and onboard telematics due to their vibration and shock resistance and ability to withstand wide temperature fluctuations typical of outdoor deployment locations.

A growing segment includes specialized technology integrators and OEMs (Original Equipment Manufacturers) who embed Box IPCs directly into their proprietary machinery, such as medical imaging devices, sophisticated robotics, and specialized telecommunications infrastructure. These customers prioritize long product lifecycles and guaranteed component availability to maintain the integrity and certification of their core products over many years. The core characteristic defining a potential customer is the need for industrial-grade reliability, extended operational temperature ranges, high computational performance at the network edge, and mandatory compliance with specific functional safety and environmental certifications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.9 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Advantech Co., Ltd., Siemens AG, Beckhoff Automation GmbH & Co. KG, Kontron S&T AG, Rockwell Automation, Inc., Omron Corporation, Dell Technologies (via IoT division), Schneider Electric SE, NEXCOM International Co., Ltd., DFI Inc., AAEON Technology Inc., Arbor Technology Corp., ADLINK Technology Inc., Lanner Electronics Inc., IEI Integration Corp., Phoenix Contact GmbH & Co. KG, Mitac International Corp., Avalue Technology Inc., B&R Industrial Automation GmbH, Fuji Electric Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technological evolution in the Box IPC market centers on improving compute density while maintaining or enhancing durability. A significant trend is the utilization of hardware-assisted virtualization technologies, such as hypervisors, enabling a single Box IPC to concurrently run multiple operating systems or real-time control applications alongside general-purpose HMI or data logging tasks. This consolidation reduces hardware footprint and simplifies network architecture, moving the industry towards software-defined control. Furthermore, standardizing interfaces, moving towards ubiquitous deployment of PCIe 4.0 and future PCIe 5.0 buses, ensures the necessary high-speed connectivity between the CPU, memory, and increasingly powerful peripheral accelerators like dedicated neural processing units (NPUs) or high-end GPUs tailored for edge AI processing.

Material science and specialized engineering are equally critical. The transition to advanced fanless thermal management relies on optimized chassis materials (often proprietary aluminum alloys) and sophisticated internal heat pipe configurations to efficiently dissipate heat generated by multi-core processors, maintaining performance stability without relying on moving parts that could introduce failures. The adherence to rigorous industry standards—such as IP67 ratings for complete dust and water immersion protection, MIL-STD-810G for shock and vibration resilience, and various regulatory certifications (e.g., CE, FCC, UL, ATEX/IECEx)—is mandatory, establishing a high technical barrier to entry for new competitors and underpinning customer confidence in reliability.

Connectivity remains paramount, demanding Box IPCs integrate both advanced wireless capabilities (Wi-Fi 6/6E, 5G NR modules) and high-speed, wired industrial communication protocols. The maturation of Time-Sensitive Networking (TSN) represents a fundamental technological shift, guaranteeing bandwidth and synchronization crucial for critical, distributed control applications. Additionally, the move toward open standards and interoperable platforms, supported by organizations like the Open Compute Project (OCP) and collaborative industrial foundations, is influencing design choices, promoting greater compatibility between different vendors' hardware and software components, thereby easing the burden of integration for large industrial end-users seeking flexible, multi-vendor solutions. Crucially, the embedded security suite utilizing hardware roots of trust and secure execution environments defines the technology barrier in highly sensitive industrial installations.

Geographical dynamics are essential to understanding the Box IPC market, reflecting the varying rates of technological adoption and industrial capacity across the globe. Each major region is driven by unique sectoral demands and regulatory requirements, influencing the specific Box IPC architectures purchased.

Fanless Box IPCs utilize passive cooling, eliminating mechanical failure points and reducing maintenance needs significantly. This design prevents dust and contaminants from entering the system, making them highly reliable and durable in harsh industrial environments with high ingress protection (IP) requirements, thereby ensuring extended mean time between failures (MTBF). They also operate silently and consume less power.

Industry 4.0 mandates the shift toward smart manufacturing, requiring Box IPCs to integrate enhanced edge computing capabilities, support real-time communication protocols like TSN, and incorporate AI/ML acceleration hardware (GPUs/VPUs) to process massive datasets locally for quality control and predictive analytics. This necessitates smaller, more powerful, and network-centric designs.

Asia Pacific (APAC), particularly driven by industrial modernization in China, India, and South Korea, shows the highest growth potential due to massive investments in smart factories, expanding electronics manufacturing, and government support for industrial automation initiatives across the region, leading to high volume demand.

TSN ensures deterministic, guaranteed latency for critical control loops, enabling real-time communication and synchronized machine control across the factory floor. Box IPCs equipped with TSN support are essential for advanced, multi-axis robotic systems and crucial centralized automation tasks where nanosecond precision is required, allowing IPCs to replace legacy fieldbus architectures.

Unlike commercial PCs, Box IPCs offer extended product lifecycles, typically guaranteeing component availability and support for 7 to 15 years. This longevity is critical for industrial customers who need to maintain system integrity, reduce re-certification costs, and avoid hardware obsolescence in long-term deployment scenarios, ensuring stable operations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.