ID : MRU_ 433765 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

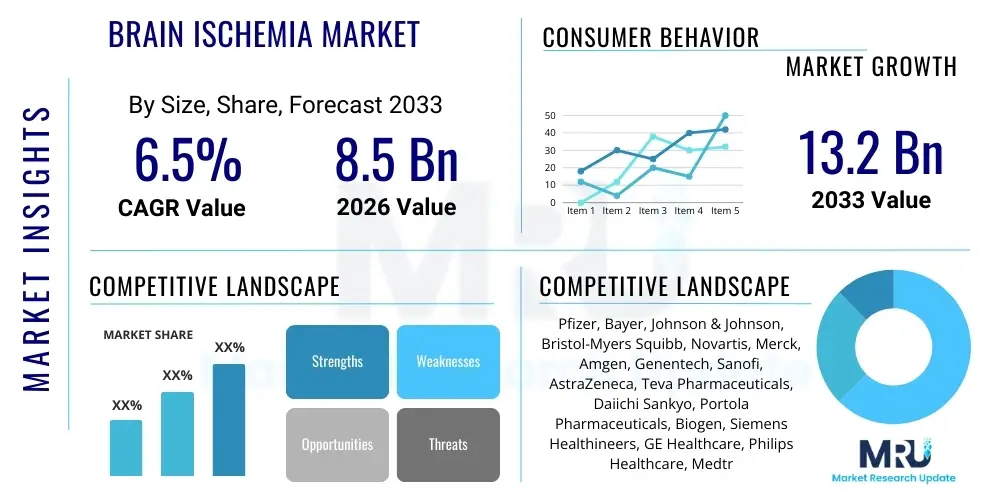

The Brain Ischemia Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at $8.5 Billion in 2026 and is projected to reach $13.2 Billion by the end of the forecast period in 2033.

The Brain Ischemia Market encompasses therapeutic, diagnostic, and preventative solutions aimed at managing conditions arising from inadequate blood flow to the brain, primarily ischemic stroke and transient ischemic attacks (TIAs). Brain ischemia results in cellular damage and neurological deficits, making timely intervention critical. The market includes pharmaceuticals such as thrombolytic agents, antiplatelet drugs, anticoagulants, and neuroprotective compounds, alongside advanced medical devices used for endovascular procedures and neuroimaging technologies vital for accurate diagnosis and patient stratification. The severe burden of ischemic stroke globally, driven by aging populations and rising prevalence of risk factors like hypertension and diabetes, establishes a strong baseline demand for market products.

Products within this domain are characterized by high regulatory scrutiny and significant research investment, particularly focusing on expanding the therapeutic window for acute stroke intervention. Major applications involve emergency room treatment for acute ischemic stroke (AIS), long-term secondary prevention, and rehabilitation. Novel delivery systems for neuroprotective agents and advanced multimodal imaging (CT perfusion, MRI diffusion-weighted imaging) are enhancing clinical outcomes. The market growth is inherently tied to technological advancements in neurocritical care and the implementation of organized stroke care systems in both developed and emerging economies.

The core benefits offered by market solutions include reduced mortality rates, minimization of long-term disability, and improved quality of life for survivors. Key driving factors include increasing awareness programs regarding stroke symptoms (Time is Brain), governmental initiatives promoting rapid access to specialized stroke units, and continuous innovation in minimally invasive thrombectomy devices, which have dramatically improved efficacy in treating large vessel occlusion strokes. The development of personalized medicine approaches, considering individual patient characteristics and stroke etiology, further catalyzes market expansion.

Global Brain Ischemia Market growth is dictated by shifting demographic profiles, particularly the rapid increase in the geriatric population worldwide, coupled with the persistent challenge of lifestyle-related chronic diseases that predispose individuals to cerebrovascular events. Business trends emphasize strategic collaborations between pharmaceutical companies and medical device manufacturers to offer integrated solutions, bridging the gap between drug therapy and interventional neurology. There is a notable trend towards outsourcing clinical trials and manufacturing to capitalize on cost efficiencies and access diverse patient pools in emerging markets, while established players focus on pipeline diversification into novel neuroprotective agents and advanced diagnostic AI tools.

Regionally, North America remains dominant due to sophisticated healthcare infrastructure, high awareness, and significant reimbursement policies for costly treatments like intravenous thrombolysis and mechanical thrombectomy. However, the Asia Pacific region is demonstrating the highest growth trajectory, fueled by rapid expansion of healthcare access, increasing disposable income, and governmental efforts to modernize stroke care protocols in densely populated nations like China and India. Europe exhibits stable growth, driven by stringent adherence to clinical guidelines and strong adoption of cutting-edge interventional technologies developed in the EU and US.

Segment trends reveal a significant surge in the Interventional Devices segment (catheters, stent retrievers) due to robust clinical evidence supporting mechanical thrombectomy as the standard of care for AIS with large vessel occlusions. Furthermore, within the pharmaceutical segment, the focus is gradually shifting toward developing drugs that extend the therapeutic window beyond the current 4.5 hours for thrombolytics, or neurorestorative therapies aimed at post-stroke recovery. The Hospital End-User segment maintains the largest market share, directly benefiting from the centralization of acute stroke care in specialized centers capable of 24/7 high-complexity interventions and diagnostics.

Common user questions regarding the impact of Artificial Intelligence (AI) in the Brain Ischemia Market primarily revolve around the speed and accuracy of diagnosis, optimization of treatment pathways, and the potential for predicting stroke risk in high-risk populations. Users are keenly interested in how AI algorithms can rapidly analyze complex neuroimaging data (CT, MRI) to identify large vessel occlusions (LVOs) and calculate the extent of salvageable brain tissue (penumbra), thereby dramatically reducing the "door-to-needle" and "door-to-groin" times, which are critical determinants of patient outcomes. Concerns often center on the regulatory approval process for AI diagnostic tools, data privacy, and the integration challenges within existing clinical workflows, especially in resource-limited settings.

The summarized key themes highlight AI's transformative role in acute care logistics and clinical decision support. Users anticipate that AI-powered solutions will democratize access to expert-level neuroimaging analysis, enabling quicker and more informed decisions, particularly in hospitals without immediate access to specialized neuroradiologists. The expectation is that AI will improve patient selection for high-risk interventions like thrombectomy and personalize secondary prevention strategies by identifying subtle patterns in patient data that precede stroke recurrence. Furthermore, AI is seen as an essential tool for accelerating drug discovery by identifying potential therapeutic targets and predicting drug efficacy and toxicity in preclinical stages for neuroprotective agents.

AI's adoption is expected to fundamentally reshape the value proposition of diagnostic imaging hardware and software providers, making integrated AI processing a standard feature rather than an optional add-on. The efficiency gains delivered by AI—reducing misdiagnosis rates and ensuring faster deployment of appropriate therapies—are projected to lower overall healthcare costs associated with long-term disability following a stroke, representing a major financial incentive for widespread implementation across global stroke networks.

The dynamics of the Brain Ischemia Market are governed by a complex interplay of Drivers (D), Restraints (R), Opportunities (O), and the resulting Impact Forces. The primary drivers include the escalating global incidence of ischemic stroke, driven by lifestyle changes, and the successful integration of advanced mechanical thrombectomy techniques into clinical practice, significantly expanding the eligible patient pool for high-value procedures. Restraints largely involve the narrow therapeutic window for effective acute treatments (especially thrombolytics), the high cost associated with interventional procedures and continuous monitoring devices, and lingering concerns regarding the risk of hemorrhagic transformation following reperfusion therapies. Opportunities are abundant in the development of remote monitoring systems (tele-stroke), personalized neuroprotective therapies, and the penetration of advanced stroke care infrastructure into underserved geographical regions, particularly those experiencing rapid demographic shifts.

Impact forces stemming from these factors manifest as high competition in the interventional device segment, pressure on pharmaceutical companies to develop safer and more effective neuroprotective agents, and increasing demand for cost-effective diagnostic screening tools. The strong positive impact of technological breakthroughs in endovascular treatment, evidenced by high success rates in recanalization and improved functional independence for patients, acts as a primary market accelerator. Conversely, the negative impact of regulatory hurdles and the inherent complexities of the brain, which make developing effective neuroprotective drugs challenging, restrain the pharmaceutical component of the market.

The market environment is further shaped by the pervasive influence of healthcare policy focused on quality metrics and outcome improvements. This necessitates continuous investment in stroke research and the standardization of care protocols globally. The drive to minimize long-term disability provides substantial momentum, pushing technology providers to innovate in rehabilitation and chronic management devices, ensuring the market trajectory remains robust throughout the forecast period, despite challenges related to market access and pricing negotiations across varied global health systems.

The Brain Ischemia Market is comprehensively segmented based on Type, Treatment, Diagnosis, and End-User, reflecting the diverse clinical landscape required for managing cerebrovascular events. Segmentation provides granular insights into specific high-growth areas and enables targeted strategic planning for stakeholders. The Type segment differentiates between Transient Ischemic Attacks (TIA) and Acute Ischemic Stroke (AIS), with AIS dominating the market share due to its severity and the immediate need for high-cost interventions. Analysis of the Treatment segment clearly shows the shift from relying solely on pharmacological interventions (thrombolytics) toward the synergistic use of pharmacotherapy with advanced mechanical intervention, signaling rapid growth in the devices category.

The Value Chain for the Brain Ischemia Market begins with the upstream activities centered on research and development (R&D) of novel drugs and advanced medical device technology. This phase is characterized by high capital expenditure, intellectual property creation, and rigorous preclinical and clinical trials required for regulatory approval. Key participants in the upstream segment include pharmaceutical research labs, academic institutions, specialized biotech firms focused on neuroprotection, and medical device innovators specializing in neurovascular access and retrieval systems. The successful navigation of clinical trial processes is paramount, setting the stage for subsequent manufacturing and commercialization stages.

Midstream activities involve the complex manufacturing and supply chain processes. For pharmaceuticals, this includes Active Pharmaceutical Ingredient (API) production, formulation, sterile filling, and quality assurance. For devices, it involves precision engineering of micro-catheters, stent retrievers, and imaging components, adhering to stringent quality control standards (ISO certification). The distribution channel structure is highly centralized for acute care products, relying heavily on specialized logistics providers capable of managing temperature-sensitive drugs and high-value medical devices. Direct sales models are often employed for capital equipment and interventional devices to provide specialized training and technical support to end-users (Hospitals), while indirect distribution through wholesalers and distributors is more common for standard pharmaceuticals.

Downstream activities focus on product deployment, utilization, and post-market surveillance. The primary end-users are specialized stroke centers and hospitals, requiring significant investment in capital equipment (advanced CT/MRI scanners, cath labs). Marketing strategies emphasize clinical evidence and peer-to-peer education due to the high medical complexity of the products. Effective post-market surveillance is crucial for monitoring device performance and drug safety, feeding back data into the upstream R&D cycle. The entire value chain is characterized by strong regulatory oversight from bodies like the FDA and EMA, ensuring product safety and efficacy throughout the lifecycle.

The primary consumers and end-users of Brain Ischemia Market products and services are institutions and practitioners involved in the entire continuum of stroke care, ranging from emergency diagnostics to long-term rehabilitation. Hospitals, particularly those designated as Comprehensive Stroke Centers (CSCs) or Primary Stroke Centers (PSCs), represent the most critical customer segment. These centers are the exclusive buyers of high-value interventional devices, advanced neuroimaging equipment, and acute thrombolytic drugs, given their mandate to provide time-sensitive, high-complexity care for acute ischemic stroke patients.

Secondary potential customers include specialized neurology clinics, rehabilitation centers, and independent diagnostic imaging facilities. Neurology clinics purchase antiplatelet and anticoagulant drugs for secondary prevention and long-term management of stroke risk factors. Rehabilitation centers are growing purchasers of technologically advanced recovery and monitoring devices. Furthermore, governmental health organizations and large integrated healthcare networks (IHNs) act as strategic customers, often dictating formulary inclusion and bulk purchasing agreements for pharmaceuticals and standardized imaging equipment across multiple facilities, influencing overall market access and pricing structures.

The purchasing decisions within this highly specialized market are typically driven by multidisciplinary teams comprising stroke neurologists, neurosurgeons, interventional radiologists, hospital administrators (for capital equipment), and pharmacy committees (for therapeutics). Efficacy, safety data, cost-effectiveness, and ease of integration into established stroke protocols are paramount considerations for these professional buyers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $8.5 Billion |

| Market Forecast in 2033 | $13.2 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Pfizer, Bayer, Johnson & Johnson, Bristol-Myers Squibb, Novartis, Merck, Amgen, Genentech, Sanofi, AstraZeneca, Teva Pharmaceuticals, Daiichi Sankyo, Portola Pharmaceuticals, Biogen, Siemens Healthineers, GE Healthcare, Philips Healthcare, Medtronic, Boston Scientific, Stryker. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Brain Ischemia Market is rapidly evolving, driven primarily by advances in neuroimaging, minimally invasive interventional techniques, and the digitalization of acute care processes. The foundational diagnostic technology revolves around rapid and high-fidelity Computed Tomography (CT) and Magnetic Resonance Imaging (MRI), with modern iterations focusing on perfusion imaging (CTP and MRP) to accurately map the ischemic penumbra (salvageable tissue) versus the core infarct. This precise anatomical and physiological mapping is critical for guiding acute reperfusion therapies, ensuring that only appropriate candidates receive high-risk interventions, thereby optimizing clinical outcomes and minimizing adverse events associated with unnecessary procedures.

In the therapeutic domain, mechanical thrombectomy devices represent the cutting edge of technology. Stent retrievers and aspiration catheters have significantly improved recanalization rates compared to older coil or wire techniques. Current innovations focus on making these devices smaller, more flexible, and capable of navigating increasingly tortuous neurovasculature, reducing procedure time, and increasing first-pass success rates. Furthermore, advanced neurocritical monitoring technology, including continuous EEG monitoring and devices tracking intracranial pressure and cerebral oxygenation, are becoming standard in specialized Intensive Care Units (ICUs) to prevent secondary brain injury following the initial ischemic event or reperfusion.

Future technological developments are concentrated on non-invasive monitoring and remote care solutions. Tele-stroke platforms utilize high-definition video conferencing and shared access to diagnostic images, enabling expert neurologists to consult and guide treatment in remote or rural hospitals instantly, effectively extending the reach of specialized stroke care. Alongside diagnostics, the pharmaceutical pipeline is heavily focused on developing genetically targeted therapies and novel delivery systems (e.g., nanocarriers) for neuroprotective agents that can maintain viability of the penumbra until reperfusion is successfully achieved, representing a long-term goal that, if realized, would fundamentally change the landscape of acute stroke management.

The primary factor driving market growth is the global demographic shift toward an aging population, which is highly susceptible to ischemic stroke, coupled with significant technological advancements in acute care treatments, notably mechanical thrombectomy devices.

AI significantly influences diagnosis by offering rapid, automated analysis of neuroimaging (CT/MRI) data, helping clinicians quickly identify large vessel occlusions and estimate the volume of salvageable brain tissue, thereby accelerating the critical decision-making process for reperfusion therapies.

Key restraints include the extremely narrow therapeutic time window (typically 4.5 hours) for effective thrombolytic treatment, the persistent challenge in developing effective neuroprotective drugs that maintain efficacy in human trials, and the potential risk of hemorrhagic transformation post-treatment.

The Asia Pacific (APAC) region is projected to exhibit the fastest Compound Annual Growth Rate (CAGR) due to rapid infrastructure development, increased healthcare spending, massive population density, and high incidence rates of risk factors like hypertension and diabetes across key economies.

The current standard of care for eligible patients presenting with acute LVO stroke involves rapid diagnostic imaging followed by immediate intervention, typically starting with intravenous thrombolysis (if within the time window) followed by mechanical thrombectomy using devices such as stent retrievers or aspiration systems.

Healthcare providers are addressing this challenge through the implementation of organized stroke systems, including tele-stroke networks, rapid transport protocols (EMS pre-notification), and AI-driven imaging platforms designed to minimize door-to-needle/groin times, effectively maximizing the number of patients treated within the critical therapeutic window.

Antiplatelet and anticoagulant agents play a crucial role in the secondary prevention segment of the market. They are essential for long-term management following an ischemic event to reduce the risk of stroke recurrence by preventing the formation of new clots or managing underlying cardiac conditions like atrial fibrillation.

Essential diagnostic imaging includes non-contrast CT (to rule out hemorrhage), CT angiography (CTA) to identify vessel occlusions, and CT perfusion (CTP) or MRI diffusion/perfusion sequences to assess the extent of irreversible damage and determine the amount of potentially salvageable brain tissue (penumbra).

The development of successful neuroprotective agents is highly significant as it represents an opportunity to extend the therapeutic window significantly beyond current limits, protecting neurons from secondary injury mechanisms that occur after ischemia and reperfusion, potentially mitigating long-term disability regardless of recanalization success.

The requirement for highly specialized stroke care centralizes demand among Comprehensive Stroke Centers (CSCs) and Primary Stroke Centers (PSCs). These centers become the dominant end-users, driving procurement decisions for high-cost, specialized diagnostic and interventional capital equipment, thereby shaping the market’s distribution strategy.

While mechanical thrombectomy has demonstrated high efficacy, ongoing concerns revolve around device-related complications, such as vessel perforation, embolization to new territories, and ensuring high operator competence. Continuous innovation focuses on improving device navigability and reducing these procedural risks.

Anticipated technological developments include gene therapies targeting stroke recovery, development of non-invasive brain monitoring systems for continuous cerebral blood flow assessment, and advanced robotics to assist in complex neurovascular procedures, further automating and refining acute care interventions.

Global health crises can temporarily disrupt the market by diverting healthcare resources and staffing away from stroke care, leading to delays in diagnosis and treatment. However, they can also accelerate the adoption of tele-stroke and remote monitoring solutions to maintain continuity of specialized care delivery.

Treatment for TIA (Transient Ischemic Attack) primarily focuses on aggressive secondary prevention (antiplatelets, risk factor modification) as there is no irreversible damage, whereas Acute Ischemic Stroke (AIS) requires immediate reperfusion therapy (thrombolysis or thrombectomy) to salvage brain tissue and minimize permanent neurological deficit.

Regulation imposes a significant barrier to entry, demanding extensive and costly clinical trials to demonstrate safety and efficacy, especially for novel neuroprotective agents and Class III medical devices (stent retrievers). This rigorous process often favors large, established market players with robust R&D capabilities.

The Interventional Procedures/Devices sub-segment, driven by high-cost mechanical thrombectomy devices, currently generates the largest revenue due to the high procedure cost, the necessity of specialized capital equipment (cath labs), and superior clinical outcomes demonstrated for LVO strokes.

Early-stage research investment is heavily focused on regenerative medicine, cell therapies aimed at neuronal repair post-stroke, and precision medicine approaches using genomics to identify individual patient response profiles to antiplatelet drugs and potential neuroprotective compounds.

Speed is critical because the brain loses approximately 1.9 million neurons per minute during an ischemic event. Faster diagnosis and initiation of reperfusion therapy directly correlate with reduced infarct size, better functional outcomes, and less long-term disability, emphasizing the "Time is Brain" principle.

Economic conditions significantly influence market penetration in developing regions, as low per capita healthcare spending limits the adoption of high-cost technologies like MRI and thrombectomy devices, often restricting available treatment to lower-cost generics and basic CT scanning capabilities.

Specialized training for neurologists, interventionalists, and emergency medical services (EMS) is paramount. Market growth for high-end devices is directly linked to the availability of skilled personnel who can safely and effectively deploy complex treatments, making professional education a key strategic component for manufacturers.

Ethical considerations include potential algorithmic bias leading to disparities in care based on demographic data, accountability for diagnostic errors made by AI systems, and maintaining patient confidentiality and data security in cloud-based imaging analysis platforms.

Manufacturers are utilizing advanced drug delivery technologies, such as utilizing nanoparticles, liposomes, or transiently opening the BBB using focused ultrasound, to safely and effectively transport neuroprotective or neurorestorative agents into the ischemic brain tissue where they are needed most.

The trend for non-invasive diagnostic tools, particularly Doppler ultrasound and high-resolution MRI techniques, is projected to increase, driven by their utility in screening high-risk patients (e.g., carotid stenosis) and avoiding the risks associated with invasive angiography procedures.

Preventative care solutions primarily target the pharmaceutical segment (antiplatelets, statins, antihypertensives) and the diagnostic segment (screening for atrial fibrillation and carotid artery disease), focusing on managing underlying risk factors to prevent the initial or recurrent ischemic event.

The competitive landscape for mechanical thrombectomy devices is highly intense, dominated by a few large players (Stryker, Medtronic, Boston Scientific) who constantly innovate on stent retriever design and aspiration technology, resulting in frequent product launches and fierce competition for market share in specialized centers.

Increased public awareness campaigns (e.g., FAST acronym) significantly influence the market by reducing pre-hospital delay times, leading to more patients arriving at hospitals within the critical therapeutic window, thereby increasing the utilization rates of acute treatments like thrombolysis and thrombectomy.

Long-term rehabilitation represents a substantial financial burden on healthcare systems and families. This drives the demand for cost-effective rehabilitation technologies, including robotics and virtual reality systems, aimed at improving functional recovery and reducing the need for chronic institutional care.

Key challenges in scaling tele-stroke services globally include poor internet connectivity in rural areas, regulatory barriers related to cross-state or cross-country medical licensing, and the initial capital investment required for high-definition video conferencing and secure data sharing infrastructure.

Key players are adapting by investing in biomarker discovery and pharmacogenomic research to understand individual responses to antiplatelet or thrombolytic drugs. This enables the development of diagnostic assays that predict treatment efficacy and potential adverse effects, leading to personalized secondary prevention strategies.

Biomarkers, particularly blood-based markers of neuronal injury or inflammation, are anticipated to play a crucial role by providing a rapid, easily accessible method to confirm stroke diagnosis, estimate time of onset, and potentially predict functional outcomes, complementing current reliance solely on imaging.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.