ID : MRU_ 431478 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

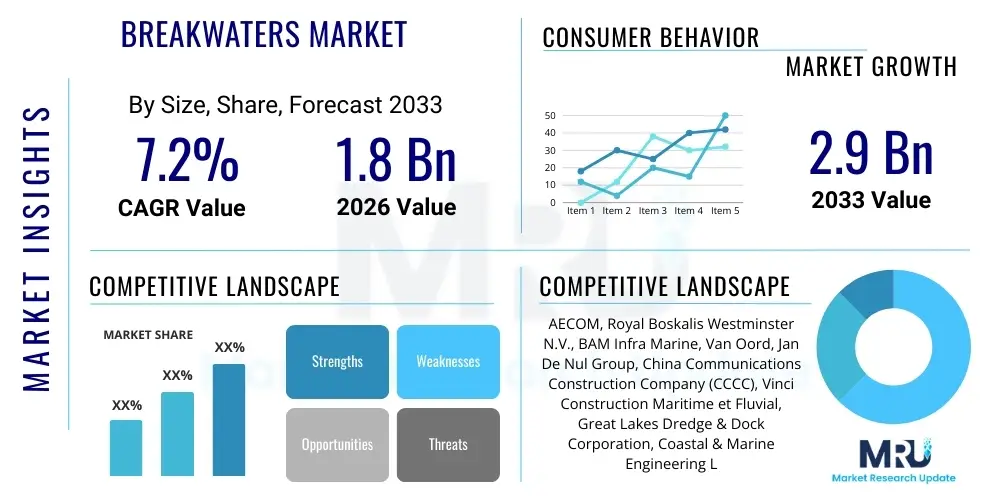

The Breakwaters Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 2.9 Billion by the end of the forecast period in 2033.

The Breakwaters Market encompasses the design, construction, and maintenance of structures built to protect coastlines, harbors, and marine infrastructure from the damaging effects of waves, tides, and storm surges. Breakwaters, fundamental components of coastal engineering, function primarily by dissipating wave energy and creating tranquil water zones necessary for safe navigation, port operations, and minimizing coastal erosion. These structures are critical assets in maritime nations, safeguarding vital economic hubs and ecologically sensitive regions.

Product categories within this market range significantly, including fixed structures such as rubble-mound breakwaters, composite breakwaters, and vertical wall structures, alongside innovative solutions like submerged and floating breakwaters. Major applications are concentrated in coastal defense initiatives aimed at mitigating the irreversible impacts of climate change, specifically sea-level rise and increasing storm intensity. Furthermore, the expansion of global trade necessitates continuous investment in modernizing and expanding port infrastructure, creating sustained demand for advanced breakwater solutions tailored to specific water depths and environmental conditions.

The driving factors for market expansion are multifaceted, including heightened awareness regarding the economic vulnerability of coastal assets, rapid urbanization in low-lying coastal areas, and large-scale government investments in maritime security and resilient infrastructure. The inherent benefits of breakwaters—providing stable conditions for cargo handling, recreational activities, and protecting valuable beachfront property—reinforce their indispensability. However, the market must navigate complex regulatory environments and high initial construction costs, often requiring novel approaches in material science and project execution to ensure long-term durability and ecological compatibility.

The global Breakwaters Market exhibits robust growth driven fundamentally by the escalating threat of climate change and the resultant need for resilient coastal protection infrastructure. Business trends indicate a shift toward sophisticated engineering methodologies, utilizing advanced computational fluid dynamics (CFD) for design optimization and greater integration of precast concrete units (PCU) to accelerate construction timelines and improve structural integrity. Key players are increasingly focusing on lifecycle assessment and sustainability, incorporating eco-friendly materials and designs, such as 'eco-revetments' and structures that promote marine habitat restoration, responding to stricter environmental regulations and corporate social responsibility mandates.

Regionally, the market dynamics are highly pronounced in Asia Pacific (APAC) due to extensive urbanization, massive port expansion projects, particularly in China and India, and the high susceptibility of regions like Southeast Asia to typhoons and tsunamis. North America and Europe, characterized by mature economies, are primarily focused on maintenance, repair, and upgrade (MR&U) projects, adopting modular and floating breakwater technologies to address environmental concerns and facilitate temporary or adaptable protection solutions. Latin America and the Middle East & Africa (MEA) represent emerging high-growth areas, fueled by investments in hydrocarbon export facilities and new strategic port development across critical maritime routes.

Segment trends demonstrate strong dominance by the Rubble Mound segment owing to its cost-effectiveness and flexibility across various seabed conditions, although the Vertical Wall and Composite structures are gaining prominence in deepwater port environments requiring vertical quay structures. The Application segment is dominated by Port & Harbor Development, closely followed by Coastal Protection, which is expected to accelerate significantly as government funding increasingly targets shoreline stabilization. Material innovation is crucial, with high-performance concrete (HPC) and specialized geosynthetics becoming pivotal in enhancing durability, reducing maintenance cycles, and ensuring the longevity of these massive structures against increasingly aggressive oceanic conditions.

Common user questions regarding AI's impact on the Breakwaters Market center primarily on how machine learning can optimize structural design against unpredictable wave patterns, enhance operational efficiency during construction, and predict maintenance needs to minimize catastrophic failure risks. Users seek clarity on the viability of using deep learning models for accurate forecasting of extreme weather events, which directly informs the required robustness of breakwater designs. Key themes revolve around AI's ability to reduce engineering margins, lower material consumption through precise simulation, and integrate real-time sensor data for proactive asset management, thereby moving the industry toward a predictive and highly optimized maintenance paradigm.

AI is transforming the preliminary stages of breakwater construction by dramatically improving hydrodynamics modeling and risk assessment. Traditional numerical simulations are time-consuming and computationally intensive, whereas AI algorithms, particularly neural networks trained on vast datasets of historical weather patterns, wave statistics, and material performance, can rapidly generate thousands of design iterations. This capability allows engineers to test the resilience of various structural configurations (e.g., armor unit placement, core geometry) against a broader range of extreme, low-probability events, ensuring designs are robust yet optimized in material use, translating directly into reduced capital expenditure and minimized environmental footprint.

Furthermore, during the operational lifespan of breakwaters, AI systems are instrumental in facilitating Predictive Maintenance (PdM). By analyzing continuous inputs from embedded sensors measuring strain, pore pressure, scour depth, and ambient wave energy, AI models can identify subtle structural degradation far earlier than conventional periodic inspections. This shifts the maintenance strategy from reactive repair to proactive intervention, significantly extending the service life of the breakwater and preventing major infrastructure failures. The integration of AI-powered monitoring systems enhances both safety and cost-efficiency, ensuring the sustained functionality of critical maritime assets against dynamic coastal environments.

The market is primarily driven by global imperatives for coastal resilience, specifically the urgent need to protect burgeoning coastal populations and infrastructure from escalating climate risks, coupled with sustained investment in international trade facilities. Restraints include the high capital investment required for construction, complex permitting processes tied to stringent environmental regulations, and the long project gestation periods characteristic of large marine civil engineering works. Opportunities arise from technological advancements in modular and eco-friendly breakwater designs, as well as significant governmental funding allocated globally for blue economy infrastructure development. These forces collectively shape the market's trajectory, mandating a balance between economic feasibility, environmental stewardship, and engineering resilience.

Drivers: The dominant driver is climate change mitigation, specifically the necessity to counteract rising sea levels and increased storm intensity, which render existing coastal defenses inadequate. Global trade expansion demands increased port capacity and operational efficiency, requiring stable water environments facilitated by new or upgraded breakwaters. Government mandates and international protocols focusing on coastal zone management, coupled with urbanization pressures on sensitive shorelines, also mandate proactive investment in protective infrastructure. Furthermore, the development of offshore energy infrastructure (wind, oil/gas) requires specialized breakwater solutions for asset protection and operational support bases.

Restraints: Significant restraints include the exceptionally high cost of marine construction, which involves specialized equipment, deepwater foundation work, and large volumes of durable materials. Environmental impact assessments (EIAs) often impose lengthy bureaucratic delays and strict design modifications to minimize damage to marine habitats, leading to protracted timelines. Technical complexity, particularly in seismic zones or areas with challenging seabed conditions, demands specialized engineering expertise that can limit the pool of viable contractors, thereby increasing project costs and complexity. Material scarcity or volatility in the pricing of raw materials like cement and rock aggregate also acts as a restraint.

Opportunities: The market opportunity lies in adopting modular construction techniques, particularly for floating breakwaters, which offer adaptability, lower deployment costs, and reduced environmental disturbance compared to traditional fixed structures. Innovation in material science, focusing on low-carbon concrete and durable composite materials, presents avenues for achieving greater sustainability and extended service life. Emerging markets in Africa and Southeast Asia are initiating new large-scale infrastructure projects that lack existing protection, representing greenfield growth. Moreover, the integration of breakwaters with renewable energy generation (e.g., wave energy converters integrated into the structure) offers a significant opportunity for multifunctional coastal infrastructure.

The Breakwaters Market segmentation provides a granular understanding of the structural preferences, application requirements, and material science trends driving specific sub-markets. The primary segmentation is categorized by Type, encompassing the structural form (Rubble Mound, Vertical Wall, Floating, etc.); by Material, reflecting the core components used (Concrete, Rock/Stone, Steel, Composites); and by Application, detailing the structure's primary function (Coastal Protection, Port & Harbor Development, Energy Infrastructure). This analysis is crucial for stakeholders to tailor their product offerings and strategic focus toward the most dynamic and profitable segments globally, optimizing R&D expenditure to meet specialized demands, such as those arising from deep-sea environments or environmentally protected zones.

The dominance of specific segments often correlates with geographical and economic characteristics. For instance, the Rubble Mound segment remains pervasive in areas where natural rock aggregate is readily available and water depths are moderate, offering a flexible and durable solution. Conversely, the Vertical Wall segment is critical for large, containerized ports requiring minimal footprint and deep berthing depths. Material evolution, particularly the increasing reliance on specialized precast concrete armor units (e.g., Tetrapods, Accropodes), reflects the industry's need for high-performance, predictable, and rapidly deployable solutions that can withstand severe hydraulic forces, demonstrating a clear trend toward standardization and optimization of complex geometries.

Analyzing the Application segmentation reveals distinct investment priorities. While Port & Harbor Development historically drives demand, the growing urgency of Coastal Protection projects—often government-funded and involving large-scale shoreline restoration or stabilization—is expected to be the fastest-growing application segment. Furthermore, the niche but highly specialized segment of Energy Infrastructure (protecting LNG terminals, offshore platforms, and coastal nuclear facilities) demands the highest standards of structural integrity and redundancy, often leading to the adoption of sophisticated composite breakwater designs and innovative materials capable of enduring extreme operational loads and minimizing seismic risk.

The value chain for the Breakwaters Market is characterized by highly specialized stages, beginning with upstream activities focused on geological surveying and material procurement. Upstream analysis involves detailed geotechnical investigations, hydrographic surveys, and the sourcing of bulk materials, primarily high-quality rock aggregate and cement. The quality and proximity of rock quarries significantly impact overall project costs and logistics. Furthermore, the design and engineering phase, involving specialized consulting firms and computational modeling experts, represents a critical value-add stage, ensuring the final structure is optimized for site-specific wave conditions and environmental constraints, utilizing proprietary software and advanced computational fluid dynamics (CFD) expertise.

Midstream activities encompass the actual construction and installation process, which is capital-intensive and requires specialized marine fleets, including dredging vessels, heavy-lift cranes, and customized placement machinery for armor units. Key contractors manage complex logistics, quality control, and adherence to strict safety and environmental standards. The transition towards precast concrete armor units (PCUs) has streamlined midstream operations by shifting much of the manufacturing process from the construction site to controlled fabrication yards, improving efficiency and consistency, and reducing weather-related delays inherent in open marine environments.

Downstream analysis focuses on the final asset owners—governments, port authorities, and private terminal operators—who are the direct buyers. Distribution channels are predominantly direct, involving competitive bidding and long-term contractual relationships between the asset owner and the lead engineering, procurement, and construction (EPC) contractor. Indirect influences include specialized consulting engineers who specify the design and material, and financial institutions that fund these massive infrastructure projects. The long-term maintenance, repair, and monitoring (MRM) services offered by specialized firms constitute a significant post-construction revenue stream, increasingly utilizing advanced inspection technologies like drones and robotic submersibles.

Potential customers in the Breakwaters Market are dominated by governmental and quasi-governmental organizations responsible for coastal zone management and maritime trade facilitation. This includes national and regional Port Authorities (e.g., major container terminals, bulk handling ports) whose primary interest lies in minimizing downtime and maximizing throughput through stable water conditions. Federal and State-level environmental or coastal protection agencies represent a burgeoning customer base, driving demand for ecological restoration and long-term coastal resilience projects, often involving soft defenses integrated with structural breakwaters.

Private sector buyers constitute a specialized, high-value segment, encompassing developers of recreational marinas, private industrial terminals (such as those for oil & gas, mining exports, and specialized manufacturing), and increasingly, operators of offshore energy facilities. These private entities prioritize return on investment, requiring durable, low-maintenance breakwaters that protect high-value assets. Furthermore, naval and defense establishments are consistent, high-specification customers, requiring structures that offer robust security, minimal wave reflection, and rapid deployment capabilities in strategic locations, often relying on proprietary and highly secure engineering standards.

The shift towards Public-Private Partnerships (PPPs) in infrastructure development is creating a new class of potential customers: consortiums that finance, build, and operate maritime assets over decades. These customers require breakwater solutions designed for maximum longevity and minimal lifecycle costs, pushing contractors toward innovative designs and robust warranties. Therefore, sales strategies must address not just the engineering needs of the project but also the long-term financial viability and risk mitigation concerns of the asset owner or concessionaire.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 2.9 Billion |

| Growth Rate | 7.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AECOM, Royal Boskalis Westminster N.V., BAM Infra Marine, Van Oord, Jan De Nul Group, China Communications Construction Company (CCCC), Vinci Construction Maritime et Fluvial, Great Lakes Dredge & Dock Corporation, Coastal & Marine Engineering Ltd., Shimizu Corporation, Penta Ocean Construction Co. Ltd., Bechtel Corporation, Hyundai Engineering & Construction Co., Ltd., Dredging International (DEME Group), J.F. Brennan Company, Inc., Weeks Marine, Inc., Dutra Group, Taylor Engineering, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Breakwaters Market is increasingly focused on resilience, sustainability, and efficiency, moving away from purely conventional construction methods. Key technological advancements center around high-performance material science, primarily the development of Ultra-High Performance Concrete (UHPC) and specialized precast armor units (e.g., Core-Loc, Xbloc, Accropode II). These materials offer superior durability, resistance to abrasion, and reduced environmental impact compared to standard concrete, allowing for smaller, lighter, yet stronger structures. Furthermore, the use of specialized geotechnical fabrics and geosynthetics for reinforcement and filtration within rubble mounds has improved long-term stability and reduced maintenance requirements.

Digitalization forms the second major technological pillar, profoundly impacting design and monitoring. Advanced Computational Fluid Dynamics (CFD) modeling, often integrated with Geographic Information Systems (GIS) and remote sensing data, enables engineers to create highly accurate digital twins of coastal areas. These simulations allow for precise prediction of wave-structure interaction, scour potential, and hydrodynamic performance under extreme conditions, significantly reducing the risks associated with traditional empirical design methods. Furthermore, the increasing use of Building Information Modeling (BIM) facilitates complex project management, minimizing clashes between infrastructure elements and improving logistical coordination across large, multi-year construction projects.

During the construction phase, technological progress is driven by automation and specialized marine equipment. GPS-guided placement systems are now standard, ensuring the precise positioning of core material and armor units, which is crucial for maximizing wave dissipation efficiency. The trend toward modular and floating breakwaters leverages composite materials and innovative mooring technologies, allowing for rapid deployment and adaptability. Finally, post-construction, structural health monitoring (SHM) systems, incorporating fiber optic sensors, accelerometers, and advanced data analytics, provide real-time insights into the structure’s performance and long-term degradation, ensuring proactive asset management and extended functional life.

The primary driver is the accelerating impact of climate change, specifically the combination of rising sea levels and the increased frequency and intensity of severe weather events (storms, hurricanes). This necessitates the construction of new, resilient coastal defense infrastructure and the massive upgrade of existing, outdated port and shoreline protection systems to safeguard economic assets and coastal populations.

Floating breakwaters are generally less effective than fixed rubble mound structures in dissipating very long-period, high-energy ocean waves, making them unsuitable for major commercial ports or primary coastal defense against severe storms. However, they are highly effective for mitigating shorter, wind-generated waves typical in marinas and lakes. They offer advantages in terms of lower cost in deep water, ease of deployment, minimal seabed disturbance, and suitability for locations with soft or unstable seabed foundations.

Digitalization, encompassing technologies like advanced Computational Fluid Dynamics (CFD), Building Information Modeling (BIM), and Structural Health Monitoring (SHM) systems, is crucial. It enables highly accurate predictive modeling during design to optimize structure performance and material use. Post-construction, sensor-based SHM systems use real-time data and AI analytics to conduct predictive maintenance, drastically extending the service life and reducing the risk of catastrophic failure by identifying structural anomalies early.

The Asia Pacific (APAC) region, specifically East and Southeast Asia, is projected to exhibit the highest growth rate. This is due to extensive urbanization along vulnerable coastlines, aggressive port expansion programs aimed at boosting global trade capacity (particularly in China, India, and ASEAN nations), and urgent governmental initiatives to build resilience against frequent and powerful typhoons and coastal flooding events.

Environmental considerations are increasingly stringent, driving demand for materials and designs that minimize ecological impact. This includes adopting low-carbon concrete formulations, utilizing locally sourced materials to reduce transport emissions, and implementing ‘Eco-Engineering’ principles. Modern breakwaters are often designed with enhanced surface textures (e.g., 'Biotopes') to promote the colonization and restoration of marine habitats and minimize turbidity and disruption to coastal sediment transport.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.