ID : MRU_ 432118 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

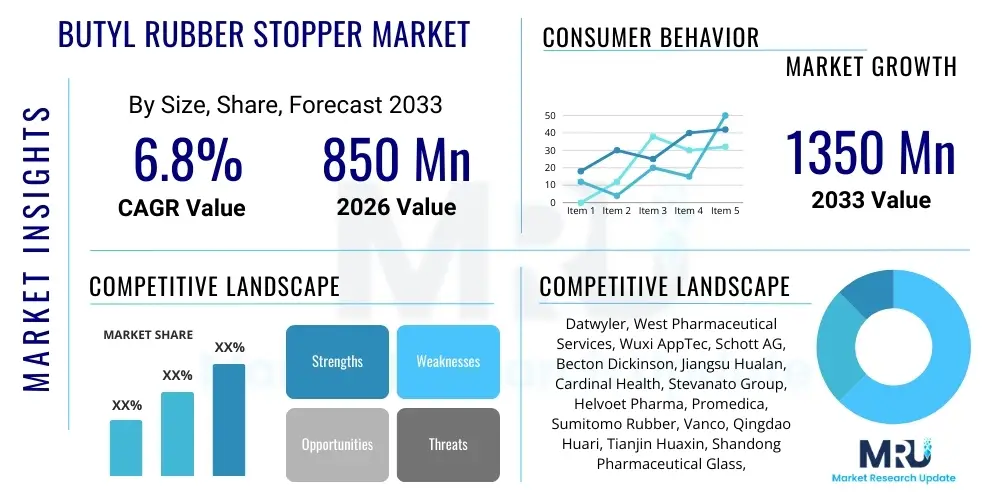

The Butyl Rubber Stopper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 850 Million in 2026 and is projected to reach USD 1350 Million by the end of the forecast period in 2033.

The Butyl Rubber Stopper Market is intrinsically linked to the global pharmaceutical and biotechnology industries, serving as a critical component in the primary packaging of injectable drugs, vaccines, and diagnostic reagents. Butyl rubber, known chemically as polyisobutylene-co-isoprene, is overwhelmingly preferred for stoppers due to its exceptional properties, notably its low permeability to gases and moisture, superior chemical inertness, and high sealing integrity. These characteristics are paramount for maintaining the sterility, shelf stability, and efficacy of parenteral formulations, especially sensitive biological products and complex vaccines. The primary function of these stoppers is to ensure a hermetic seal within vials and bottles, protecting the contents from environmental contaminants and preventing the leaching of harmful substances from the packaging material into the drug product.

The product landscape encompasses various specialized designs, including serum stoppers, lyophilization (freeze-drying) stoppers, and injection port stoppers, each engineered to meet specific drug delivery and processing requirements. For instance, lyophilization stoppers are designed with specialized collapse features to allow moisture sublimation during the freeze-drying cycle before being seated to seal the vial permanently. The manufacturing process demands stringent quality control, adherence to global pharmacopeial standards (such as USP and EP), and production within certified ISO Class cleanroom environments to mitigate particulate contamination. The increasing prevalence of chronic diseases requiring sophisticated injectable treatments, coupled with rapid advancements in biopharmaceuticals and personalized medicine, solidifies the foundational demand structure for high-quality butyl rubber stoppers globally.

Major driving factors include the massive global vaccination campaigns, the burgeoning demand for pre-filled syringes and cartridges which often utilize components derived from butyl rubber polymers, and the stringent regulatory environment that mandates the use of proven, low-extractable elastomer formulations. Furthermore, innovations in coating technologies, such as PTFE (Teflon) or Flurotec films, applied to the stoppers are extending the compatibility spectrum with highly aggressive or sensitive drug formulations by reducing friction during insertion and minimizing potential drug-packaging interactions, thereby enhancing drug safety and extending product shelf life. This ongoing technological refinement ensures the market remains dynamic and responsive to evolving pharmacological requirements.

The Butyl Rubber Stopper Market is experiencing sustained growth, fundamentally driven by the expansion of the global injectable drug pipeline, particularly in oncology, diabetes management, and cutting-edge gene and cell therapies. Key business trends indicate a definitive shift toward premiumization, characterized by heightened demand for ultra-high purity, low-extractable bromobutyl and chlorobutyl stoppers that ensure maximum drug stability. Leading manufacturers are heavily investing in advanced molding techniques and automated visual inspection systems to meet the Zero-Defect requirements imposed by major pharmaceutical clients and regulatory bodies like the FDA and EMA. Strategic mergers and acquisitions are shaping the competitive landscape, focused on securing raw material supply chain resilience and expanding geographical manufacturing footprints to serve burgeoning markets, particularly in Asia Pacific, where healthcare infrastructure investment is accelerating rapidly.

Regionally, North America and Europe currently dominate the market share owing to the presence of major pharmaceutical innovators, rigorous quality standards, and established regulatory pathways for drug approval. However, the Asia Pacific region, led by China and India, is projected to record the highest Compound Annual Growth Rate (CAGR) throughout the forecast period. This accelerated growth is primarily attributed to rising domestic drug manufacturing capacity, increasing accessibility to advanced healthcare, and substantial government initiatives aimed at vaccine production and public health infrastructure enhancement. Latin America and the Middle East & Africa are emerging as significant consumption centers, primarily reliant on imports but showing increasing local production capacities, particularly for generic injectable medicines and regional vaccine programs.

In terms of segment trends, the Application segment sees the Pharmaceutical sector retaining the largest market share, driven specifically by the requirement for stoppers in large-volume parenteral vials and specialty biologics. Within the material segmentation, Bromobutyl rubber is gaining dominance over Chlorobutyl variants due to its superior chemical resistance, improved curing characteristics, and lower moisture vapor transmission rate (MVTR), making it ideal for sensitive biologics. The Type segment is seeing significant traction in Lyophilization Stoppers, reflecting the growing trend of formulating unstable drug compounds into stable freeze-dried forms to extend their commercial viability and storage requirements. Furthermore, the rising adoption of ready-to-use (RTU) and ready-to-sterilize (RTS) components is streamlining the filling processes for Contract Manufacturing Organizations (CMOs), pushing manufacturers to provide specialized packaging formats.

Common user questions regarding AI’s impact on the Butyl Rubber Stopper Market revolve primarily around automating quality assurance, optimizing complex supply chain logistics, and accelerating new material R&D. Users frequently inquire if AI-driven vision systems can eliminate human error in detecting minute defects, thereby pushing quality standards beyond current limits. Furthermore, there is significant interest in how predictive maintenance algorithms can minimize machine downtime in high-volume, continuous manufacturing environments, ensuring consistent supply. Concerns also address the integration cost and the necessity of highly skilled personnel to manage and interpret large datasets generated during high-speed molding and finishing processes. Essentially, the market seeks assurance that AI can simultaneously enhance quality, reduce operational costs, and future-proof the supply chain against volatility.

The integration of Artificial Intelligence and Machine Learning (ML) platforms is fundamentally transforming the manufacturing and quality control paradigm for butyl rubber stoppers. AI-driven high-resolution camera systems are now employed on production lines to perform real-time, 100% inspection of stoppers, analyzing parameters such as dimensional accuracy, surface integrity, and particulate contamination at speeds and accuracies far exceeding human capability. These ML models are trained on massive datasets of acceptable and defective stoppers, allowing the system to learn and classify increasingly subtle defects, thus significantly lowering the Adjusted Quality Level (AQL) and reducing batch rejections. This stringent automated quality assurance is essential for products destined for highly regulated injectable applications.

Beyond quality control, AI is playing a crucial role in optimizing the upstream and downstream logistics. Predictive analytics are being utilized to forecast raw material (isobutylene/isoprene) pricing and availability, enabling manufacturers to execute optimal procurement strategies and mitigate supply chain risks associated with petrochemical fluctuations. Furthermore, AI algorithms are optimizing inventory management for both standard and specialized stoppers across various global warehousing locations, ensuring that critical pharmaceutical partners receive 'just-in-time' components, thereby minimizing client risk associated with packaging shortages. This comprehensive application of AI contributes directly to operational efficiency, cost management, and overall market reliability.

The dynamics of the Butyl Rubber Stopper Market are governed by a complex interplay of internal and external forces. The primary driver is the accelerating demand from the pharmaceutical sector, fueled by the massive research and development expenditures globally, particularly focused on high-value, injectable biological drugs, biosimilars, and advanced vaccine platforms. The inherently protective nature and regulatory acceptance of butyl rubber as a standard primary closure material provide a strong structural foundation for market growth. This driving force is strongly coupled with the opportunistic trend represented by novel drug delivery systems, such as dual-chamber systems and self-injection pens, which require highly specialized, precision-engineered elastomer components beyond standard vial stoppers.

However, the market faces significant restraints. The most prominent constraint is the increasingly stringent global regulatory framework, exemplified by pharmacopeial monographs and extractables/leachables testing requirements, which place immense pressure on manufacturers to minimize impurities and ensure long-term compatibility. Secondly, the market is highly sensitive to the volatility of petrochemical raw material prices, as key precursors like isobutylene and isoprene are derivatives of the oil and gas industry, leading to unpredictable fluctuations in manufacturing costs and challenging long-term pricing stability. These restraints necessitate continuous investment in analytical capabilities and process validation to maintain market access and competitiveness. Despite these hurdles, the demand for sterile, injectable medicine acts as a powerful counterbalance, sustaining market momentum.

The critical impact forces shaping the market trajectory include rapid technological adoption, particularly concerning surface treatment and coating technologies. The move towards Flurotec or equivalent coated stoppers is mitigating interaction risks for complex APIs (Active Pharmaceutical Ingredients), thereby establishing a new de facto quality standard for premium products. The opportunity arising from the COVID-19 pandemic response—which drastically accelerated vaccine production and supply chain decentralization—has instilled greater urgency in regional manufacturing capabilities, prompting investments in localized production hubs. Therefore, while regulatory stringency remains a challenge, it simultaneously drives innovation toward higher purity and better performance, ultimately benefiting end-users by ensuring safer and more stable drug products.

The Butyl Rubber Stopper Market is strategically segmented based on crucial parameters including Type, Material, and Application, reflecting the diverse needs of the life sciences industry. Segmentation by Type distinguishes between specialized functionalities such as Lyophilization Stoppers, which possess a specific design for freeze-drying cycles; Injection/Serum Stoppers, used for standard liquid formulations; and Diagnostic Stoppers, tailored for chemical and assay reagents. This categorization helps manufacturers address precise operational requirements of different drug processing environments. Lyophilization stoppers are expected to show accelerated growth due to the rising trend of stabilizing sensitive biological entities through freeze-drying.

The Material segmentation is critical, dividing the market primarily into Bromobutyl Rubber and Chlorobutyl Rubber. Both are halogenated butyl rubbers, offering excellent sealing properties, but bromobutyl is increasingly favored due to its lower extractable profile and greater chemical compatibility, making it the material of choice for advanced biological and high-cost small molecule drugs. While Chlorobutyl stoppers remain prevalent in generic and high-volume serum applications due to cost-effectiveness and proven track record, the overall market migration is towards premium, coated bromobutyl variants. The ongoing research into next-generation elastomers with even lower impurity levels suggests future segmentation may include proprietary polymer blends designed specifically for extreme pH or temperature conditions.

The Application segment highlights the dominance of the Pharmaceutical industry, which consumes the vast majority of the market volume for vials, cartridges, and pre-filled syringes. This segment is further subdivided into areas like vaccines, biologics, and small molecule injectables, each demanding different dimensional and chemical specifications for their corresponding stoppers. Following pharmaceuticals, the Diagnostics industry represents a stable application base, utilizing stoppers for specialized kits and blood collection tubes where barrier properties and sample preservation are paramount. This detailed segmentation allows stakeholders to accurately target investment and product development efforts toward the fastest-growing and highest-value niches within the life sciences ecosystem.

The value chain for the Butyl Rubber Stopper Market is highly integrated and begins with the upstream procurement of specialty raw materials, primarily petrochemical derivatives. The key raw material suppliers, often large chemical corporations, provide the base polymers: isobutylene and isoprene, which are then halogenated to produce Chlorobutyl or Bromobutyl rubber. This upstream segment is characterized by specialized expertise and capital intensity, as polymer quality directly dictates the performance and compliance of the final stopper. Price volatility and supply concentration at this stage represent significant risks that stopper manufacturers must actively manage through long-term supply agreements and strategic sourcing, thereby influencing the overall manufacturing cost structure.

The midstream process involves the complex transformation of the raw polymer into the final closure device. This involves compounding (mixing the polymer with fillers, curing agents, and stabilizers), precision molding (compression or injection molding), washing, siliconization or coating (e.g., Flurotec), and rigorous sterilization processes (autoclaving, gamma irradiation, or E-beam sterilization). Manufacturers in this segment, such as Datwyler and West Pharmaceutical Services, invest heavily in cleanroom technology (ISO Class 7 and 5) and advanced automated inspection systems to meet the Zero-Defect standards required by the pharmaceutical industry. The trend here is toward Ready-to-Sterilize (RTS) and Ready-to-Use (RTU) components, shifting validation burdens and processing steps away from the drug filler.

The downstream distribution channel involves connecting the manufacturer to the end-users. Direct distribution is common for large pharmaceutical companies and major Contract Development and Manufacturing Organizations (CDMOs) who require custom specifications and bulk volumes. Indirect distribution utilizes specialized packaging distributors who manage inventory, sterilization certificates, and smaller volume requirements for academic researchers, diagnostics labs, and smaller biotech startups. The dominant end-users are the companies performing aseptic filling of injectables. The efficiency and reliability of the distribution network, particularly concerning cold chain logistics for certain specialized products, is vital for maintaining the integrity and compliance of the sterilized stoppers until they reach the final filling line.

Potential customers for butyl rubber stoppers are concentrated overwhelmingly within the life science ecosystem, specifically those entities engaged in the formulation, manufacturing, and distribution of injectable therapeutic and diagnostic products. The primary segment comprises multinational Pharmaceutical Companies and large Biotechnology Firms (e.g., Pfizer, AstraZeneca, Roche, Genentech). These customers require vast quantities of high-specification, low-extractable stoppers for their proprietary drug pipelines, including critical vaccines, monoclonal antibodies, and advanced therapies. Their procurement decisions are driven by stringent regulatory compliance, validated performance data (leachables testing), and reliable global supply chain capacity, often favoring suppliers capable of providing technical support for complex drug-packaging compatibility studies and managing regulatory submissions.

A rapidly growing customer base includes Contract Development and Manufacturing Organizations (CDMOs) and Contract Research Organizations (CROs), which handle outsourcing services for smaller biotech companies and often manage the sterile filling operations. CDMOs, such as Catalent and Lonza, require a highly diversified portfolio of stoppers—from standard serum closures to specialized lyophilization types—to accommodate the varied needs of their numerous clients. Their purchasing criteria prioritize flexibility, guaranteed sterility (RTU components), rapid turnaround times, and robust quality documentation, positioning them as high-volume, dynamic purchasers critical to market growth, especially in the outsourcing of high-value biologics filling.

Secondary, yet significant, customer groups include Diagnostics Companies, focusing on reagents, specialized blood collection tubes, and in-vitro diagnostic kits; and Veterinary Pharmaceutical Companies, which use stoppers for animal vaccines and medicines. Academic and government research laboratories, including public health institutions responsible for national vaccination stockpiles, also constitute a stable customer segment. These customers often procure through indirect channels or specialized distributors, prioritizing consistency and cost-effectiveness for standard applications while maintaining strict adherence to regulatory standards applicable to their respective jurisdictions. The complexity of modern medicine means customers are increasingly seeking packaging partners, not just suppliers, demanding deeper collaboration on material science and closure integrity testing.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 Million |

| Market Forecast in 2033 | USD 1350 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Datwyler, West Pharmaceutical Services, Wuxi AppTec, Schott AG, Becton Dickinson, Jiangsu Hualan, Cardinal Health, Stevanato Group, Helvoet Pharma, Promedica, Sumitomo Rubber, Vanco, Qingdao Huari, Tianjin Huaxin, Shandong Pharmaceutical Glass, DWK Life Sciences, Gerresheimer, Nipro Corporation, AptarGroup, Shanghai Huaxin. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Butyl Rubber Stopper Market is defined by precision engineering, material science innovation, and advanced manufacturing protocols aimed at minimizing contamination and ensuring optimal barrier function. A core technology involves the use of high-precision injection and compression molding techniques that ensure strict dimensional adherence, which is critical for maintaining container closure integrity (CCI) across varied vial specifications. Furthermore, manufacturers are increasingly employing automated vacuum deflashing methods to remove excess material without compromising the stopper structure, contributing to superior product consistency and quality. The integration of Statistical Process Control (SPC) throughout the manufacturing workflow allows for continuous monitoring and adjustment of critical parameters, guaranteeing compliance with increasingly tight tolerances required by high-speed aseptic filling lines.

A major technological advancement driving market value is surface treatment, specifically the application of fluoropolymer coatings such as ethylene tetrafluoroethylene (ETFE) or polytetrafluoroethylene (PTFE) based technologies, marketed commercially as Flurotec or similar proprietary coatings. These coatings serve two vital purposes: they minimize the potential for extractables leaching from the rubber matrix into the drug product, and they reduce friction during the stopper insertion process, preventing particle generation and ensuring efficient closure. The adoption of these coated stoppers is becoming standard for sensitive biologics and high-cost small molecule injectables, necessitating significant investment by manufacturers in specialized coating and curing equipment. The development of robust, solvent-free coating application methods is a key area of R&D focus to further reduce the impurity profile.

Finally, cleanroom manufacturing and sterilization technologies are foundational to the industry. Stoppers must be processed in ISO Class 7 or higher environments to prevent biological and particulate contamination. Advanced sterilization methods, replacing traditional autoclaving, are gaining traction; particularly E-beam (Electron Beam) and Gamma irradiation, which offer superior validation reliability and allow manufacturers to supply Ready-to-Use (RTU) stoppers directly to end-users. These methods require complex material validation, as the rubber must maintain its physical and chemical properties post-sterilization. The technological shift towards RTU components is arguably the most impactful trend, significantly streamlining pharmaceutical manufacturing operations by eliminating the need for in-house washing and sterilization by the drug filler.

Regional dynamics in the Butyl Rubber Stopper Market reflect the global distribution of pharmaceutical manufacturing, regulatory maturity, and healthcare expenditure trends. North America, encompassing the United States and Canada, stands as the market leader in terms of revenue and demand for specialized, premium stoppers. This dominance is underpinned by the region's massive R&D spending, the presence of global pharmaceutical and biotechnology headquarters, and a high volume of new drug approvals, particularly complex biologics and personalized therapies. The stringent regulatory environment set by the U.S. FDA drives demand for the highest quality, low-extractable bromobutyl, and coated stoppers. Growth here is characterized by technological refinement and strategic capacity expansion to support rapidly growing segments like gene therapy packaging.

Europe represents the second-largest market, characterized by mature pharmaceutical production centers in Germany, France, Switzerland, and the UK. The European market is highly regulated by the European Medicines Agency (EMA), focusing intensely on sustainability and standardization (e.g., Ph. Eur. standards). Key growth drivers include the large generic injectable market and the robust vaccine manufacturing base. The demand trend in Europe mirrors North America’s move towards RTU components, driven by cost efficiency and reduced validation burden. Investment is focused on modernizing existing manufacturing facilities and establishing local supply chains to mitigate risks associated with long-distance transport and geopolitical instability, ensuring continuity of supply for critical medicines.

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally. This exponential growth is fueled by increasing government investment in healthcare infrastructure, the expansion of local drug manufacturing in countries like China, India, and South Korea, and the burgeoning prevalence of chronic diseases. APAC is becoming a major global manufacturing hub for both generic injectables and vaccines. While cost-sensitivity remains a factor, the rapidly professionalizing regulatory environment in key APAC nations is increasingly mandating the use of stoppers compliant with international pharmacopeial standards, leading to accelerating adoption of high-quality bromobutyl stoppers. This region represents the most significant opportunity for market expansion and capacity deployment throughout the forecast period.

The central factor is the continuous global growth of the injectable drug market, particularly the surge in complex biological therapeutics, advanced vaccines, and high-value oncology drugs, all of which require highly secure and chemically inert primary packaging closures.

Bromobutyl stoppers are generally preferred over Chlorobutyl variants due to their superior chemical resistance, lower propensity for leaching impurities (extractables), and enhanced barrier properties, making them the standard choice for sensitive, high-cost biological drug formulations.

Stringent regulatory bodies (FDA, EMA) mandate manufacturing within ISO Class cleanrooms, adherence to pharmacopeial monographs (USP, EP), and rigorous extractables/leachables testing. This drives manufacturers to adopt premium materials, advanced quality control, and certified Ready-to-Use (RTU) components.

The Asia Pacific (APAC) region is forecast to exhibit the highest CAGR, primarily due to expanding domestic pharmaceutical manufacturing capabilities in nations like China and India, coupled with significant increases in healthcare investment and rising demand for essential injectable medicines and vaccines.

Fluoropolymer coatings, such as Flurotec, are crucial for premium stoppers as they minimize the interaction between the rubber material and sensitive drug formulations, reduce friction during high-speed aseptic filling processes, and significantly lower the potential for extractable compounds.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.