ID : MRU_ 431628 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

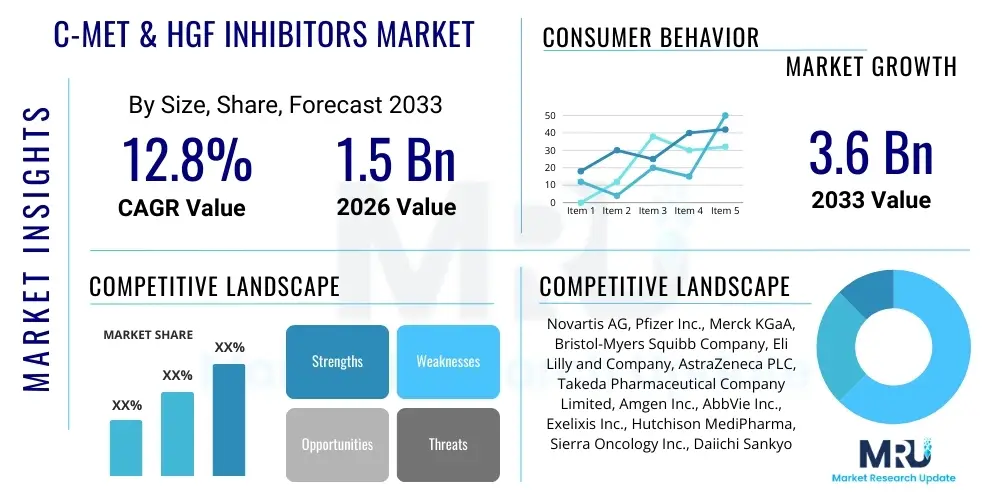

The C-MET & HGF Inhibitors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 3.6 Billion by the end of the forecast period in 2033. This substantial expansion is primarily fueled by the increasing prevalence of various solid tumors, particularly Non-Small Cell Lung Cancer (NSCLC) and gastric carcinoma, where C-MET overexpression or HGF signaling pathway deregulation is a key oncogenic driver. The shift towards personalized and targeted cancer therapies, which offer superior efficacy and reduced systemic toxicity compared to conventional chemotherapy, strongly contributes to this robust growth trajectory.

The C-MET & HGF Inhibitors Market encompasses specialized pharmaceutical agents designed to target and block the signaling pathways mediated by the C-MET receptor tyrosine kinase and its ligand, Hepatocyte Growth Factor (HGF). These inhibitors are central components of precision oncology, focusing on tumors that exhibit C-MET gene amplification, protein overexpression, or activating mutations, which are often correlated with aggressive disease progression, metastasis, and acquired resistance to standard treatments. The products available in the market span both small molecule tyrosine kinase inhibitors (TKIs) and monoclonal antibodies, each offering distinct mechanisms for neutralizing the oncogenic signaling cascade, thereby inhibiting cellular proliferation, survival, and motility across various cancer types.

Major applications for C-MET and HGF inhibitors currently focus on treating advanced malignancies, notably including NSCLC with MET exon 14 skipping mutations, papillary renal cell carcinoma, and hepatocellular carcinoma. Beyond oncology, research is also exploring their potential roles in fibrosis and autoimmune diseases, although oncology remains the dominant application segment driving immediate market growth. The principal benefits of these targeted agents include improved patient outcomes in biomarker-selected populations, often translating into significantly longer progression-free survival rates compared to non-targeted treatments. Furthermore, they play a crucial role in overcoming mechanisms of resistance developed against first and second-generation cancer therapies, offering vital salvage pathways for patients with limited treatment options.

Key driving factors underpinning the market expansion include continuous advancements in diagnostic capabilities, such as Next-Generation Sequencing (NGS) and sophisticated immunohistochemistry techniques, which enable accurate identification of C-MET-driven tumors. Increased investment in pharmaceutical R&D, coupled with regulatory approvals for novel inhibitors like capmatinib and tepotinib, accelerates market penetration. Moreover, the expanding geriatric population globally and the corresponding rise in cancer incidence ensure a sustained demand for effective, innovative therapeutic modalities that can selectively target tumor biology with enhanced specificity and reduced overall toxicity, establishing C-MET and HGF inhibitors as essential tools in modern cancer management protocols.

The C-MET & HGF Inhibitors Market is experiencing rapid commercial evolution, characterized by intense competition among biopharmaceutical giants and a substantial inflow of venture capital into early-stage research focused on next-generation inhibitors. Business trends indicate a strong move toward strategic alliances, co-development agreements, and exclusive licensing deals, particularly between large pharmaceutical companies seeking to diversify their oncology portfolios and smaller biotech firms possessing proprietary drug candidates. These collaborations are essential for navigating the complex and expensive process of clinical development and gaining rapid market access across key global geographies. A pivotal trend involves the increasing exploration of combination therapies, pairing C-MET inhibitors with immune checkpoint inhibitors (ICIs) or traditional chemotherapy, aiming to achieve synergistic therapeutic effects and mitigate acquired drug resistance, thereby reshaping standard treatment paradigms across multiple solid tumors.

Regional trends reveal that North America, particularly the United States, maintains market dominance, driven by superior healthcare infrastructure, high awareness of precision medicine, advanced diagnostic reimbursement policies, and the presence of major key market players and extensive clinical research activities. Conversely, the Asia Pacific (APAC) region is poised for the highest growth rate during the forecast period. This accelerated growth is attributed to the massive and expanding patient pool, increasing healthcare expenditure in emerging economies like China and India, and a rapid adoption of Western treatment guidelines. European markets demonstrate steady growth, supported by robust regulatory frameworks like the European Medicines Agency (EMA) and a strong history of academic research contributing to early clinical adoption.

Segment trends highlight the persistent dominance of small molecule tyrosine kinase inhibitors (TKIs) within the product type segment due to their established clinical efficacy, oral administration benefits, and relatively straightforward manufacturing processes. However, monoclonal antibodies targeting C-MET or HGF are rapidly gaining traction, particularly for intravenous administration in hospital settings, offering high specificity. Application-wise, NSCLC remains the most significant segment dueating to the high prevalence of MET exon 14 skipping mutations and the availability of specific targeted therapies. The market is also witnessing a strong trend towards personalized medicine models, with treatment decisions increasingly reliant on companion diagnostics to accurately stratify patient populations, enhancing therapeutic precision and overall cost-effectiveness.

User inquiries regarding the intersection of Artificial Intelligence (AI) and the C-MET & HGF Inhibitors Market predominantly center on how AI can accelerate the notoriously slow and expensive processes of target identification, lead optimization, and clinical trial design. Common questions focus on AI's ability to predict patient response to specific inhibitors, identify novel mechanisms of acquired resistance, and personalize dosage regimens. Users are keenly interested in predictive bioinformatics tools that utilize large genomic and proteomic datasets to precisely define patient populations most likely to benefit from C-MET targeted therapy, thus reducing the number of non-responders in clinical settings and improving drug development efficiency. The primary concern is the effective integration and validation of complex AI models within highly regulated pharmaceutical research environments and ensuring the interpretability of 'black box' predictions for clinical decision-making.

AI's influence is transformative, specifically in optimizing the chemical synthesis and structural modification of C-MET TKIs. Machine learning algorithms can analyze vast libraries of chemical compounds to predict binding affinities, toxicity profiles, and metabolic stability, significantly accelerating the pre-clinical phase. This allows researchers to prioritize only the most promising candidates, thereby shortening the time-to-market for novel inhibitors. Furthermore, deep learning techniques are being applied to analyze histopathological images and liquid biopsy data with unparalleled speed and accuracy, facilitating the early and precise detection of C-MET alterations, which is crucial for initiating targeted therapy immediately upon diagnosis. This data-driven precision substantially reduces R&D costs and enhances the probability of success for clinical assets.

In the clinical space, AI is revolutionizing trial management by selecting ideal sites, monitoring patient recruitment, and analyzing real-time safety and efficacy data. Predictive analytics can forecast patient drop-out rates or potential adverse events, allowing for proactive intervention. For existing C-MET inhibitors, AI algorithms are instrumental in developing sophisticated dosing strategies that adapt based on a patient's individual pharmacokinetic and pharmacodynamic profiles, minimizing toxicity while maximizing therapeutic exposure. This advanced personalization capability, driven by AI-integrated platforms, elevates the standard of care in targeted oncology, moving the C-MET & HGF inhibitor market toward true precision treatment delivery.

The C-MET & HGF Inhibitors Market is shaped by a confluence of impactful forces, where robust drivers often counter significant restraints, creating dynamic market opportunities. A major driver is the escalating global incidence of cancers, particularly NSCLC and gastric cancer, where C-MET pathway aberrations are frequent, necessitating highly specific treatment options. Concurrently, the increasing clinical acceptance and adoption of targeted therapies over traditional cytotoxic chemotherapy, owing to improved efficacy and reduced collateral damage, substantially boost demand. However, the market faces significant restraints, primarily stemming from the high cost associated with the research, development, and commercialization of complex targeted oncology drugs. Furthermore, the development of acquired resistance to C-MET inhibitors, which often occurs after an initial period of response, requires continuous innovation and poses a fundamental challenge to sustained efficacy and long-term market growth.

Opportunities within this market are concentrated around leveraging combination therapy approaches, such as pairing C-MET inhibitors with immunotherapy (PD-1/PD-L1 inhibitors) or VEGF inhibitors, to overcome resistance and achieve deeper, more durable responses. Another key opportunity lies in expanding the therapeutic scope beyond core indications like NSCLC into less common but C-MET-driven malignancies, including various sarcomas and glioblastomas, thereby expanding the addressable patient population. The development of advanced, highly sensitive companion diagnostics (CDx) that can accurately select patients eligible for therapy also presents a lucrative pathway, enhancing the commercial viability of these high-value drugs and ensuring regulatory compliance in precision medicine.

The impact forces driving market evolution are rooted in technological advancements, regulatory pressures, and socio-economic factors. Technological force is evident in the rapid evolution of next-generation inhibitors designed to address specific resistance mutations, alongside sophisticated biomarker identification tools. Regulatory forces, particularly streamlined approval pathways like Fast Track designation, accelerate the market entry of breakthrough inhibitors, particularly those addressing high unmet needs. Socio-economic factors, such as increased accessibility to advanced healthcare in emerging economies and favorable reimbursement policies for targeted oncology drugs in established markets, are crucial for converting clinical potential into commercial success, ensuring that the market trajectory remains upward despite development hurdles.

The C-MET & HGF Inhibitors Market is comprehensively segmented based on product type, therapeutic application, and distribution channel, providing granular insights into specific market dynamics and growth areas. The segmentation reflects the diverse pharmacological approaches used to target the C-MET signaling axis, ranging from oral small molecules to injectable biologics. Analysis across these segments is critical for understanding consumer adoption patterns, identifying high-growth indications, and enabling strategic planning for pharmaceutical companies looking to maximize penetration in specialized oncology markets. The dominance of small molecule inhibitors is contrasted by the rising potential of biologic agents, while therapeutic application segmentation highlights the continuing clinical priority of lung and gastric cancers globally.

The value chain for the C-MET & HGF Inhibitors Market is characterized by highly specialized, capital-intensive upstream activities, followed by stringent regulatory oversight during manufacturing, and a concentrated, specialized downstream distribution network. Upstream analysis focuses predominantly on R&D and drug discovery, involving extensive genomic and proteomic research to identify novel targets, screen compound libraries, and optimize lead candidates. This phase requires significant investment in specialized personnel, advanced laboratory infrastructure, and proprietary screening technologies like High-Throughput Screening (HTS) and advanced computational biology. The success rate in the upstream phase is low, making this segment the most critical determinant of long-term market leadership and requiring strong intellectual property protection for promising drug candidates.

The manufacturing stage involves the synthesis of small molecule inhibitors or the complex bioprocessing of monoclonal antibodies, both demanding adherence to Good Manufacturing Practices (GMP) and rigorous quality control. Due to the potency and specialized nature of these oncology drugs, manufacturing is often outsourced to highly qualified Contract Development and Manufacturing Organizations (CDMOs) specializing in high-potency active pharmaceutical ingredients (HPAPIs) or biologics production. Supply chain resilience is vital, particularly for ensuring the consistent availability of raw materials, which are often highly specialized chemical intermediates or cell culture media components essential for antibody production, necessitating robust supplier qualification processes.

Downstream activities center around distribution, marketing, and sales, involving specialized distribution channels due to the nature of targeted oncology treatments. Direct distribution predominantly occurs through specialized hospital pharmacies and oncology clinics, which are equipped to handle high-value, temperature-sensitive pharmaceuticals and manage complex patient support programs. Indirect distribution channels, including specialty retail pharmacies, play a smaller but growing role, often facilitating patient access for orally administered TKIs. Marketing efforts are heavily focused on educating oncologists and specialized healthcare providers on biomarker testing requirements and treatment protocols, relying heavily on medical science liaisons (MSLs) to disseminate complex clinical data and drive prescription behavior in highly segmented therapeutic areas.

The primary consumers and key decision-makers within the C-MET & HGF Inhibitors Market are highly specialized healthcare providers and institutional purchasers within the oncology ecosystem. These include specialized oncologists (particularly thoracic and gastrointestinal oncologists), hematologists, and interventional radiologists who prescribe and administer these targeted agents. Their prescribing behavior is fundamentally driven by companion diagnostic results, which confirm the presence of C-MET aberrations, making the adoption of these inhibitors highly dependent on the integration of precision diagnostics within cancer treatment protocols across major medical centers and academic research institutions.

Institutional customers, such as specialized cancer treatment centers, university hospitals, and regional cancer networks, represent the main volume buyers. These institutions procure C-MET inhibitors in bulk for inpatient and outpatient treatment settings, and their purchasing decisions are heavily influenced by formulary inclusion processes, health economic assessments, and comparative effectiveness studies. Procurement departments within these institutions focus intensely on minimizing treatment costs while maximizing patient outcomes, often negotiating contracts based on volume commitments and managed entry agreements, reflecting the high cost of these advanced targeted therapies.

Furthermore, third-party payers, including private insurance companies, government healthcare systems (like the NHS in the UK or CMS in the US), and national drug regulatory bodies, serve as critical indirect customers. While not the direct users, their reimbursement policies and coverage decisions ultimately determine patient access and utilization rates for C-MET and HGF inhibitors. Favorable decisions regarding coverage and pricing are essential for market uptake, requiring manufacturers to demonstrate significant clinical and economic value through rigorous pharmacoeconomic data submissions and engagement with health technology assessment (HTA) bodies globally.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 3.6 Billion |

| Growth Rate | 12.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Novartis AG, Pfizer Inc., Merck KGaA, Bristol-Myers Squibb Company, Eli Lilly and Company, AstraZeneca PLC, Takeda Pharmaceutical Company Limited, Amgen Inc., AbbVie Inc., Exelixis Inc., Hutchison MediPharma, Sierra Oncology Inc., Daiichi Sankyo Company Limited, Blueprint Medicines Corporation, Suzhou Connect Biopharmaceuticals Co., Ltd., ArQule, Inc. (acquired by Merck & Co.), Mirati Therapeutics, Inc., Eisai Co., Ltd., Roche Holding AG, GlaxoSmithKline PLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape driving the C-MET & HGF Inhibitors Market is primarily centered on sophisticated molecular biology, high-precision diagnostic platforms, and advanced drug design methodologies. A crucial technological dependency is on Next-Generation Sequencing (NGS) and Polymerase Chain Reaction (PCR) based assays, which are fundamental for accurately detecting C-MET gene amplification, MET exon 14 skipping mutations, and protein overexpression. These technologies serve as the backbone for companion diagnostics, ensuring that treatment is accurately delivered to the specific subset of patients who will respond, thereby maximizing therapeutic benefit and justifying the high cost of these therapies. Continuous refinement in liquid biopsy techniques is further revolutionizing the landscape, allowing for non-invasive and serial monitoring of C-MET alterations and resistance mechanisms during the course of treatment.

In the realm of drug development, computational chemistry and structural biology are paramount. Techniques such as X-ray crystallography and Cryo-electron Microscopy (Cryo-EM) are utilized to determine the three-dimensional structure of the C-MET receptor and HGF ligand interactions, allowing researchers to design highly selective small molecule inhibitors or high-affinity monoclonal antibodies. The development trajectory is increasingly focused on creating novel inhibitors that can specifically overcome known secondary resistance mutations within the C-MET kinase domain, often achieved through advanced medicinal chemistry that optimizes potency and reduces off-target effects, enhancing the drug safety profile compared to earlier generations of multi-kinase inhibitors.

Furthermore, the integration of bioinformatics and proprietary high-throughput screening (HTS) platforms significantly accelerates the initial discovery phase. HTS enables the rapid assessment of millions of compounds against the C-MET target, streamlining lead identification. Beyond discovery, advanced formulation and drug delivery technologies are vital for optimizing the bioavailability and patient compliance for orally administered TKIs. Specifically, sophisticated formulation techniques are employed to address solubility challenges and ensure consistent therapeutic concentrations are achieved and maintained in the plasma, which is a key factor in ensuring long-term efficacy and reducing the risk of treatment failure due to inadequate drug exposure.

The global C-MET & HGF Inhibitors Market exhibits distinct regional dynamics driven by variances in healthcare spending, regulatory environments, cancer incidence rates, and access to advanced oncology centers. North America, dominated by the United States, holds the largest market share. This dominance is attributed to the early adoption of precision oncology protocols, substantial expenditure on R&D, favorable reimbursement policies for targeted therapies and companion diagnostics, and the significant presence of globally leading pharmaceutical and biotechnology companies actively engaged in C-MET inhibition research. High disease awareness among clinicians and sophisticated infrastructure for complex clinical trials further cement North America's leadership position in innovation and commercialization.

Europe represents the second-largest market, characterized by steady growth supported by established regulatory pathways (EMA) and a strong public commitment to cancer research in key countries like Germany, France, and the UK. While pricing negotiations and health technology assessments (HTA) can impose constraints on market access compared to the US, the increasing prevalence of NSCLC and gastric cancers, coupled with robust healthcare systems that facilitate the delivery of high-cost targeted therapies, ensures sustained market expansion. Western European nations prioritize the integration of biomarker testing into standard oncology guidelines, driving the prescription of C-MET inhibitors in eligible patient populations.

Asia Pacific (APAC) is forecast to be the fastest-growing region during the projection period. This rapid acceleration is fueled by the immense, aging population base contributing to high cancer incidence, particularly in populous nations such as China, Japan, and India. Governments in these economies are increasingly investing in modernizing healthcare infrastructure and improving access to advanced oncology treatments. Furthermore, certain C-MET-driven cancers, such as gastric cancer, have a higher prevalence in parts of East Asia, creating a specialized and high-demand market for these targeted inhibitors. Localized R&D and manufacturing partnerships are also burgeoning, aimed at serving the large regional patient volume and mitigating importation costs.

C-MET and HGF inhibitors primarily function by blocking the signaling cascade initiated by the Hepatocyte Growth Factor (HGF) binding to the C-MET receptor tyrosine kinase. By disrupting this pathway, the drugs inhibit key oncogenic processes such as cell proliferation, migration, invasion, and angiogenesis, effectively slowing tumor growth and metastasis in targeted cancers.

The most common cancer type treated with C-MET inhibitors is Non-Small Cell Lung Cancer (NSCLC), particularly those patients harboring MET exon 14 skipping mutations. They are also approved and actively researched for use in treating gastric cancer, hepatocellular carcinoma (HCC), and papillary renal cell carcinoma (PRCC) that exhibit C-MET pathway aberrations.

Pharmaceutical companies address acquired resistance by developing next-generation inhibitors designed to target specific secondary resistance mutations (e.g., secondary site mutations in the kinase domain). Furthermore, strategic focus is placed on combination therapies, pairing C-MET inhibitors with immunotherapy agents or other targeted drugs to achieve synergistic efficacy and suppress resistance pathways.

Key growth drivers in the Asia Pacific market include the exceptionally high prevalence of specific C-MET-driven cancers, such as gastric carcinoma, coupled with increasing governmental and private investment in healthcare infrastructure, improved access to precision diagnostics, and a rapidly expanding patient base seeking advanced oncology treatments.

Small molecule Tyrosine Kinase Inhibitors (TKIs) currently dominate the market due to their established clinical efficacy, oral bioavailability, and ease of patient administration. However, monoclonal antibodies, offering high specificity and often utilized in hospital settings, are rapidly increasing their market share and clinical relevance in targeted C-MET inhibition.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.