ID : MRU_ 432418 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

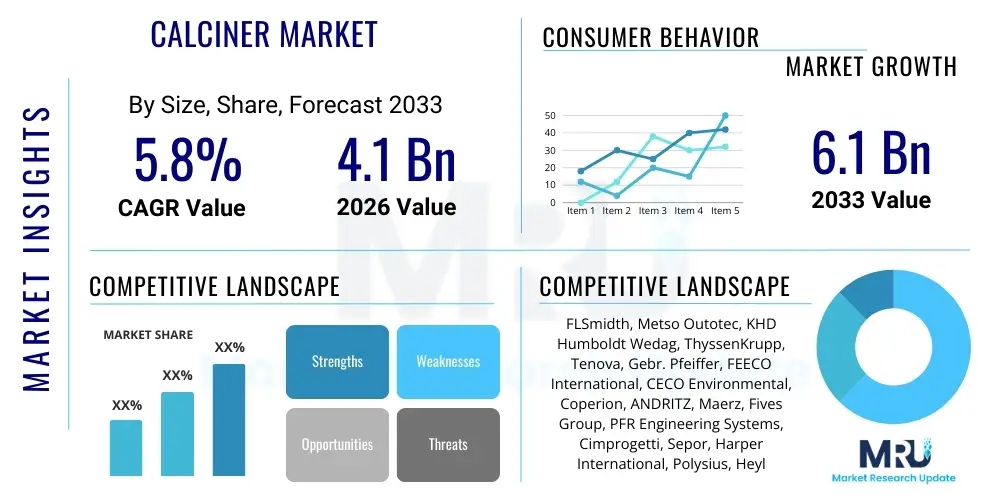

The Calciner Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 4.1 Billion in 2026 and is projected to reach USD 6.1 Billion by the end of the forecast period in 2033.

The Calciner Market encompasses the design, manufacturing, installation, and servicing of industrial furnaces used to heat materials to high temperatures, typically below the melting point, to induce thermal decomposition, phase transformation, or remove volatile substances. Calcination is a critical thermal treatment process essential across numerous heavy industries, primarily aimed at altering the physical and chemical properties of materials such as minerals, ores, and petroleum derivatives. Key products in this market include rotary kilns, fluidized bed calciners, and multiple hearth furnaces, each optimized for specific material characteristics and production scales, providing flexibility in handling diverse feedstock requirements ranging from fine powders to large lumps.

Major applications of calcination technology are concentrated in high-volume industrial sectors. The primary demand driver remains the alumina industry, where bauxite ore is calcined to produce activated or smelter-grade alumina, a fundamental component in aluminum production. Furthermore, calciners are indispensable in the processing of petroleum coke to create anode-grade carbon materials used in aluminum and steel electrolysis, ensuring material purity and specific electrical conductivity properties. The technology is also heavily utilized in cement and lime manufacturing, titanium dioxide pigment production, and various stages of mineral processing, including iron ore pellet hardening and magnesite production, illustrating the foundational role of calcination in the global supply chain of construction and metallurgical materials.

The market growth is primarily driven by global industrialization, particularly the continuous demand for aluminum, cement, and high-purity minerals in emerging economies. Benefits of advanced calcination systems include improved energy efficiency through optimized heat recovery systems and reduced fuel consumption, crucial for minimizing operational costs and meeting stringent carbon emission targets. Driving factors also include technological advancements focused on process automation, enhanced material throughput, and the increasing adoption of sustainable practices, such as utilizing alternative fuels (biomass, waste materials) in calciner operations to reduce reliance on fossil fuels and improve the overall environmental footprint of the process.

The Calciner Market is characterized by robust investment in large-scale industrial projects, primarily driven by sustained global demand for aluminum and infrastructure development materials. Current business trends indicate a strong emphasis on modernizing existing calcination plants to enhance efficiency and comply with environmental regulations, focusing heavily on upgrading older, less efficient rotary kilns with advanced control systems and superior refractory materials. There is a notable strategic shift towards modular and flexible calciner designs, particularly fluidized bed systems, which offer higher thermal efficiency, better temperature control, and easier integration into existing process lines, catering specifically to the rising demand for high-purity specialty materials like technical ceramics and specialized mineral fillers.

Regionally, the Asia Pacific (APAC) stands as the dominant market, fueled by massive infrastructural spending and high production volumes in China and India across the cement, alumina, and metallurgical industries. North America and Europe, while mature markets, are experiencing growth driven by stringent environmental compliance requirements, necessitating investment in specialized calcining technologies like circulating fluidized beds (CFBs) for efficient sulphur and nitrogen oxide capture, alongside the push for decarbonization solutions. Latin America and the Middle East & Africa (MEA) are emerging as high-growth regions, particularly due to increasing local exploitation and processing of mineral resources, requiring new installations of robust and reliable calcination equipment to meet export and domestic consumption needs.

Segment trends reveal that the Rotary Kiln Calciner segment maintains the largest market share due to its established reliability and capacity for high throughput in bulk material processing (like alumina and cement). However, the Fluidized Bed Calciner segment is registering the highest growth rate, propelled by its superior performance in processes requiring uniform temperature distribution and precision, such as petroleum coke calcination and specialty chemical production. Application-wise, the Alumina segment remains the largest consumer, but the Petroleum Coke segment is accelerating rapidly, reflecting the increasing global necessity for high-quality anode coke materials critical for the expanding electric vehicle and renewable energy sectors, which rely on lightweight, high-performance batteries.

User queries regarding the impact of Artificial Intelligence (AI) on the Calciner Market frequently center on themes of operational efficiency, predictive maintenance, and energy consumption optimization. Common questions include: "How can AI reduce fuel costs in rotary kilns?" and "Can machine learning algorithms predict refractory wear life?" The core concern is leveraging AI and machine learning (ML) to overcome the inherent challenges of thermal processes, such as managing temperature variability, reducing unplanned downtime, and ensuring consistent product quality in high-heat environments. Expectations are high regarding AI's ability to move beyond simple process control to achieve true predictive capabilities, enabling operators to make proactive adjustments based on real-time data integration across multiple plant systems, thereby maximizing throughput while minimizing emissions and energy wastage.

AI's influence is transforming calciner operation from reactive maintenance to prescriptive control. By analyzing vast datasets generated by temperature sensors, vibration monitors, gas analyzers, and product quality metrics, AI models can identify subtle patterns indicative of impending equipment failure (e.g., refractory lining thinning, burner degradation) long before conventional methods. This transition to predictive maintenance significantly boosts plant availability and reduces the high cost associated with emergency shutdowns. Furthermore, AI-driven process optimization algorithms are being deployed to dynamically adjust parameters like fuel flow, material feed rate, and rotational speed in real-time to maintain ideal calcination kinetics, ensuring homogenous heating, maximizing energy efficiency, and guaranteeing product specifications are met consistently, which is particularly vital for high-value applications like specialty ceramics and battery materials.

The Calciner Market is shaped by a confluence of powerful dynamics, encapsulated by Drivers, Restraints, and Opportunities (DRO), which collectively form the Impact Forces dictating market trajectory. Key drivers include unwavering global demand for raw materials such as primary aluminum and cement, essential for infrastructure growth, particularly in emerging markets. This is compounded by the regulatory push for cleaner industrial processes, compelling manufacturers to invest in high-efficiency, low-emission calcination technology. Conversely, the market faces significant restraints, notably the high capital expenditure required for new calciner installations and the volatile cost of primary fuels (natural gas, coal), which directly impacts operational margins. Opportunities arise from the transition to sustainable fuels, advanced digitalization for operational excellence, and the expansion into niche markets requiring highly specialized calcination, such as battery cathode materials and environmental waste treatment.

The primary driving force remains the growth in the end-use industries, particularly the metallurgical sector. The requirement for calcined petroleum coke (CPC) in the manufacturing of aluminum anodes is directly correlated with global aluminum production growth, driving continuous demand for high-capacity rotary kilns and fluidized bed calciners. Furthermore, rapid urbanization necessitates significant cement and lime production, demanding continuous investment in new or upgraded calciner capacity that adheres to modern emission standards. The regulatory environment acts as a strong impact force, where stricter emissions standards (e.g., relating to particulate matter and greenhouse gases) force operators to adopt technologies like low-NOx burners, sophisticated scrubbing systems, and more thermally efficient calciners, thereby stimulating innovation and market spending on retrofits.

Restraints are often linked to economic volatility and operational complexity. The extensive lead times and substantial initial investment required for sophisticated calciner systems present a significant barrier to entry, particularly for smaller market players. Moreover, the reliance on high-quality refractory materials that can withstand extreme thermal cycling and chemical attack introduces maintenance complexities and high replacement costs, impacting long-term viability. However, the market possesses a strong inherent opportunity through process diversification. The growing focus on processing industrial waste streams, converting biomass into advanced materials, and meeting the purity requirements for specialized minerals (like lithium and rare earths) offers new revenue streams and applications outside the traditional cement and alumina sectors, providing future resilience against fluctuations in bulk commodity markets.

The Calciner Market is highly segmented, allowing for precise technological matching with specific industrial requirements based on material type, production volume, and thermal profile complexity. Segmentation is primarily based on the calciner design (Type), the specific material being treated (Application), the mode of operation (Continuous vs. Batch), and the required operational heat levels (Temperature Range). This granular classification is essential for both manufacturers, who optimize equipment parameters, and end-users, who select the system that ensures maximal thermal efficiency, product quality consistency, and adherence to production economics. The diversity in segmentation reflects the broad scope of calcination—from massive, high-throughput rotary kilns in the alumina sector to highly controlled, specialized fluidized beds used for premium materials.

The value chain of the Calciner Market begins with upstream activities focused on raw material procurement, encompassing specialized materials such as high-grade refractory ceramics, steel alloys capable of withstanding extreme temperatures, and advanced control system components (PLCs, sensors, automation software). Key upstream challenges involve securing long-term supply agreements for specialized refractories, which directly influence the longevity and maintenance costs of the installed equipment. The subsequent stage involves core manufacturing, where original equipment manufacturers (OEMs) design, fabricate, and assemble the calciners, often requiring high-precision engineering and welding expertise. This manufacturing phase is crucial for integrating energy-efficient features, such as recuperators and waste heat recovery systems, which are key differentiators in the market.

The mid-stream segment involves distribution and installation. Due to the custom, heavy nature of calciner equipment, distribution channels are typically direct, involving specialized heavy transport logistics to site. Installation often requires extensive on-site construction, commissioning, and validation processes, requiring high-level engineering support from the OEM. Direct distribution channels dominate because the equipment is tailored to the end-user’s specific feedstock and capacity requirements, necessitating direct communication and customization throughout the sales cycle. Indirect channels might occasionally be used through local engineering procurement and construction (EPC) firms that manage the overall plant construction but rely on the OEM for core calciner technology and commissioning expertise.

Downstream analysis focuses on operation and maintenance (O&M) and end-use application. Maintenance services, including refractory replacement, routine inspections, and software upgrades, constitute a vital and profitable segment of the downstream value chain, often provided by the OEMs themselves or specialized third-party service providers. The ultimate end-users/buyers are large industrial operators in sectors like aluminum, petrochemicals, and construction. The value delivered downstream is the reliable production of high-quality intermediate materials (e.g., calcined alumina, CPC), which are critical inputs for multi-billion dollar industries, highlighting the strategic importance of calciner efficiency and uptime to the global supply chain.

The potential customer base for the Calciner Market is concentrated within the heavy industrial sectors that require high-temperature thermal processing for material transformation. These customers are typically large corporations or government-owned enterprises that operate continuously and require high throughput capacity and reliability. The predominant buyers are integrated aluminum producers, who require state-of-the-art calciners for bauxite processing into alumina, focusing on energy efficiency to manage vast production costs. Another significant customer group includes oil and gas refineries and specialized carbon manufacturers that require precision calcination of green petroleum coke into anode-grade coke, demanding tight control over volatile matter content and bulk density.

Furthermore, cement and lime producers constitute a massive customer segment, where rotary kilns are the central piece of processing equipment. These customers prioritize operational reliability, fuel flexibility (ability to burn alternative fuels), and stringent emissions compliance, particularly in developed regions. Beyond these bulk commodity processors, niche but high-value potential customers include specialized mineral processors dealing with titanium dioxide (TiO2) production, lithium compound processing for batteries, and iron ore pelletizing plants. These buyers often require smaller, highly customized calciners, such as fluidized beds or specialized rotary hearth systems, that can handle complex chemical reactions and require extremely tight temperature uniformity to meet high-purity specifications for advanced industrial applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 6.1 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | FLSmidth, Metso Outotec, KHD Humboldt Wedag, ThyssenKrupp, Tenova, Gebr. Pfeiffer, FEECO International, CECO Environmental, Coperion, ANDRITZ, Maerz, Fives Group, PFR Engineering Systems, Cimprogetti, Sepor, Harper International, Polysius, Heyl & Patterson, Claudius Peters, Kawasaki Heavy Industries |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Calciner Market is currently dominated by advancements focused on thermal efficiency, emissions reduction, and operational flexibility. Traditional technologies like the Rotary Kiln Calciner remain prevalent due to their robust design and capacity for high throughput of bulk materials, particularly in the cement and alumina industries. However, modern iterations of rotary kilns integrate sophisticated indirect heating mechanisms and advanced heat recuperation systems (such as satellite coolers and preheaters) to significantly reduce specific energy consumption and manage exhaust temperatures more effectively. These incremental improvements focus on extending refractory life and optimizing fuel switching capabilities, allowing operators to transition seamlessly between natural gas, coal, and alternative waste fuels, which is a major technological and economic advantage.

Fluidized Bed Calciners (FBCs), particularly the Circulating Fluidized Bed (CFB) variant, represent the cutting edge of thermal processing technology and are seeing rapid adoption in specific, high-value segments like petroleum coke and specialized chemical calcination. FBC technology provides superior temperature uniformity and precise control over the calcination atmosphere, minimizing product contamination and enabling high-efficiency heat transfer, which is crucial for achieving the strict quality metrics required for anode-grade carbon materials. Furthermore, FBCs are inherently superior for mitigating environmental impact, as their operational mechanism naturally facilitates in-situ desulfurization (SOx capture) when specific sorbents are introduced, making them critical for compliance in heavily regulated geographies like Europe and North America.

The integration of Industry 4.0 principles, including advanced sensors, IoT connectivity, and digital twinning, is fundamentally reshaping the market. Real-time monitoring of shell temperatures, vibration analysis of mechanical components, and continuous flue gas analysis are now standard features, moving towards a highly digitalized control environment. This technological convergence enables precise modeling of the calcination process, optimizing residence time and temperature profiles via automated control loops. Specialized technologies also include Multiple Hearth Calciners (MHCs) for processes requiring multiple distinct thermal zones and controlled atmosphere environments, and Flash Calciners, which are used for ultrafast thermal treatment of fine materials, enhancing overall processing speed and material yield in specialized mineral production.

The primary factor driving market growth is the consistent global demand for basic industrial materials, specifically calcined alumina for aluminum production and cement, fueled by ongoing urbanization and infrastructure development in emerging economies, alongside regulatory pressure for high-efficiency, lower-emission calcination technologies.

Environmental regulations significantly push end-users toward modern technologies, such as Fluidized Bed Calciners (FBCs) and advanced Rotary Kilns with preheaters, due to their superior ability to incorporate low-NOx burners, utilize waste heat, and facilitate effective capture of sulfur and particulate matter, ensuring regulatory compliance and reduced carbon footprint.

The Rotary Kiln Calciner segment maintains the largest market share globally due to its long history, proven reliability, ability to handle high throughput volumes of bulk materials like alumina and cement, and versatility in handling diverse feedstock characteristics across large-scale industrial operations.

AI and digitalization are crucial for enhancing operational efficiency by providing predictive maintenance capabilities, optimizing thermal parameters in real-time to conserve fuel, and ensuring consistent product quality through advanced process monitoring and dynamic control loops, leading to reduced operational expenditure and enhanced asset utilization.

The Asia Pacific (APAC) region, driven by continuous industrial expansion and large-scale manufacturing in countries such as China and India, offers the highest growth potential, characterized by both new plant construction and the modernization of existing facilities to meet surging domestic and international material demand.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.