ID : MRU_ 433872 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

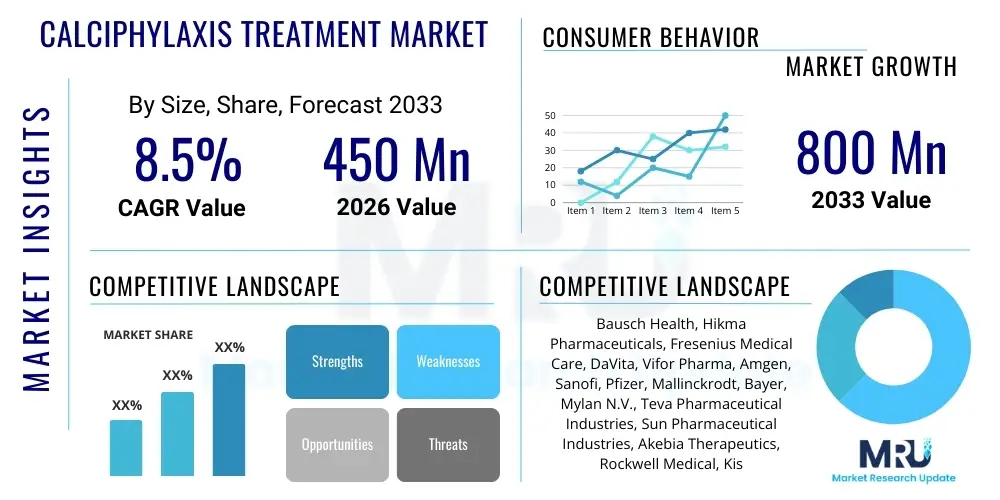

The Calciphylaxis Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $450 million in 2026 and is projected to reach $800 million by the end of the forecast period in 2033.

Calciphylaxis, also known as calcific uremic arteriolopathy (CUA), is a rare, severe, and life-threatening syndrome characterized by progressive calcification of the media layer of small- and medium-sized arteries, leading to painful skin lesions, necrosis, and subsequent systemic infection. This condition is overwhelmingly prevalent in patients with End-Stage Renal Disease (ESRD) undergoing hemodialysis, although non-uremic cases have also been documented. The market for calciphylaxis treatment encompasses a diverse range of therapeutic interventions aimed at managing symptoms, mitigating calcium deposition, preventing infection, and promoting wound healing, given that there is currently no single, universally effective, FDA-approved treatment.

The primary therapeutic products utilized in this market fall broadly into pharmacological and non-pharmacological categories. Pharmacological agents predominantly involve off-label medications such as intravenous Sodium Thiosulfate (STS), which serves as a chelating agent to dissolve calcium deposits. Other pharmacological strategies include calcimimetics like Cinacalcet to manage secondary hyperparathyroidism, and high-dose bisphosphonates to inhibit ectopic calcification. Major applications of these treatments are centered within acute care hospital settings, specialized dialysis centers, and wound care clinics. The ultimate objective is to reduce pain, minimize wound size, and significantly lower the extremely high mortality rates associated with this syndrome.

The market is fundamentally driven by the rising global incidence of predisposing factors, notably the growing prevalence of ESRD coupled with diabetes and obesity, alongside an expanding geriatric population reliant on maintenance dialysis. Benefits derived from effective treatment include enhanced patient quality of life, pain reduction, and improved survival outcomes, albeit the efficacy remains highly variable across the patient population. The driving factors are further strengthened by ongoing research into biomarkers for early diagnosis and the exploration of novel, targeted therapies aimed at the underlying molecular pathways of calcification, which promises to standardize treatment protocols and improve overall market performance.

The Calciphylaxis Treatment Market is characterized by robust expansion, primarily fueled by the increasing patient pool requiring specialized care for severe renal complications. Business trends indicate a strong focus on drug repurposing and securing Orphan Drug Designation for existing pharmacological agents, such as sodium thiosulfate, to formalize their use and stabilize supply chains. Furthermore, there is a distinct business drive towards integrated care models, where specialized dialysis providers partner with wound care management companies to offer comprehensive patient management, thereby capturing greater market share across the continuum of care. Strategic collaborations between pharmaceutical companies and academic research institutions are increasing to identify novel targets and expedite clinical trials for specific therapeutic compounds.

Regional trends highlight North America’s dominance, underpinned by its well-established reimbursement framework and high prevalence of ESRD, driving significant uptake of high-cost pharmacological and non-pharmacological modalities like Hyperbaric Oxygen Therapy (HBOT). Conversely, the Asia Pacific region is demonstrating the highest growth trajectory, propelled by surging healthcare infrastructure investments and an increasing awareness of specialized treatments among nephrology and dermatology professionals in countries like China and India. European markets maintain stable growth, prioritizing evidence-based integration of calcimimetics and intensive wound care protocols within national health systems. Competitive dynamics across all regions emphasize the importance of diagnostics and early intervention strategies to improve patient outcomes and reduce acute healthcare costs.

Segmentation trends reveal that the Pharmacological segment, particularly Sodium Thiosulfate, commands the largest revenue share, reflecting its status as the de facto standard of care despite its off-label use. However, the Non-Pharmacological segment, specifically advanced Wound Care and Hyperbaric Oxygen Therapy, is witnessing accelerated adoption due to their critical role in managing complex, non-healing necrotic wounds, thus positioning them as high-growth areas. Within end-users, Hospitals and Specialized Clinics remain the primary centers for treatment initiation and management, benefiting from the requirement for intensive monitoring and intravenous drug administration. Future growth is anticipated in segments related to novel small molecule inhibitors targeting matrix Gla protein or fetuin-A deficiency, pending clinical success.

User queries regarding the intersection of Artificial Intelligence (AI) and the Calciphylaxis Treatment Market predominantly focus on how AI can address the two critical limitations of the condition: diagnostic delay and treatment heterogeneity. Users frequently ask if machine learning can predict which high-risk dialysis patients will develop CUA, given the myriad of complex risk factors (e.g., mineral imbalance, inflammation markers, coagulation status, and medication history). Key themes revolve around leveraging AI to standardize diagnosis through image recognition of skin lesions, optimizing personalized treatment plans by predicting individual response to various combinations of off-label drugs (like STS and cinacalcet), and enhancing outcomes prediction to guide resource allocation in critical care settings. The prevailing expectation is that AI will move the diagnostic window significantly earlier, transforming calciphylaxis management from reactive wound treatment to proactive prevention.

The current lack of specific diagnostic biomarkers and standardized guidelines makes calciphylaxis a prime candidate for AI intervention. Machine learning models can process vast quantities of heterogeneous data—including electronic health records, dialysis session parameters, histological images, and genomic profiles—to identify subtle, non-linear correlations that precede clinical presentation. This predictive capability is crucial, as early intervention in calciphylaxis is intrinsically linked to improved survival rates. Furthermore, AI platforms can assist clinicians in differential diagnosis, distinguishing CUA lesions from other common skin conditions in ESRD patients, thereby eliminating diagnostic ambiguity and accelerating the commencement of appropriate therapy.

Finally, AI holds immense potential in driving drug development and optimizing clinical trial design within this rare disease domain. By simulating drug interactions and patient responses in silico, AI can expedite the identification of compounds that effectively target the underlying pathophysiology of vascular calcification without severe systemic side effects. This not only reduces the cost and time associated with traditional R&D but also helps pharmaceutical companies maximize the probability of success in securing regulatory approvals for specific calciphylaxis therapies, thereby potentially stabilizing the highly fragmented market supply of effective treatments.

The market for Calciphylaxis treatment is heavily influenced by a unique interplay of severe clinical necessity and significant therapeutic challenge, summarized by its Drivers, Restraints, and Opportunities (DRO). The primary drivers include the relentlessly increasing global prevalence of associated chronic conditions, particularly End-Stage Renal Disease (ESRD) and Type 2 Diabetes, which continuously expand the susceptible patient population. Simultaneously, greater clinician awareness and improved, though still complex, diagnostic protocols mean that more cases are being accurately identified and treated. Restraints, however, are substantial: the absence of a specific FDA-approved drug mandates the off-label use of expensive compounds like sodium thiosulfate, leading to high treatment costs and varying efficacy. Additionally, the devastatingly high mortality rate associated with the condition (often exceeding 50% within a year) frequently limits treatment duration and impacts market expenditure patterns.

Opportunities for market growth lie predominantly in the realm of advanced research and development focused on targeted, specific therapies. The push toward developing novel small molecule inhibitors that directly intervene in the calcification cascade—such as inhibitors of pyrophosphate degradation or activators of matrix Gla protein—represents a major area for investment and potential market disruption. Furthermore, enhancing non-pharmacological care, especially the refinement of specialized wound care products and the accessibility of advanced modalities like Hyperbaric Oxygen Therapy (HBOT), offers avenues for improved supportive care outcomes. The establishment of centralized, multidisciplinary centers dedicated to calciphylaxis management also provides a commercial opportunity by standardizing care and optimizing resource utilization.

The impact forces driving the market include regulatory pressures encouraging pharmaceutical companies to pursue Orphan Drug Designation (ODD) for rare diseases like calciphylaxis, providing incentives such as market exclusivity and tax credits. Clinical necessity acts as a high impact force, compelling healthcare systems to allocate resources for these expensive, life-saving treatments despite the economic burden. Conversely, high treatment failure rates and limited long-term efficacy serve as significant restraining forces, often leading to skepticism regarding return on investment for new entrants. Ultimately, the future trajectory of the market is contingent upon the successful transition from empirical, off-label management to evidence-based, targeted pharmacological interventions.

The Calciphylaxis Treatment Market is segmented across various critical dimensions, including Treatment Type, End-User, and Route of Administration, reflecting the heterogeneous nature of the therapeutic approach required for this complex condition. Analyzing these segments provides strategic insights into areas of highest expenditure and fastest growth. The segmentation by Treatment Type, encompassing both Pharmacological and Non-Pharmacological methods, highlights the current dominance of systemic drug therapies necessary to address the underlying pathophysiology, even while supportive wound management is paramount for patient survival and quality of life. The End-User segmentation, focusing on Hospitals, Specialty Clinics, and Ambulatory Surgical Centers, demonstrates the shift of intense wound care and maintenance therapy towards outpatient settings where feasible, although acute management remains centralized in hospitals.

The Pharmacological segment is further subdivided into agents such as Sodium Thiosulfate (STS), Bisphosphonates, Chelating Agents, and Calcimimetics. STS is currently the cornerstone of treatment, representing the largest sub-segment due to its ability to chelate calcium and promote vasodilation, despite regulatory challenges. Conversely, the Non-Pharmacological segment is crucial for immediate patient management, with advanced wound care products and surgical debridement driving revenue, necessitated by the severe nature of necrotic ulcers. The evolution of treatment protocols dictates that combined therapies are becoming the standard, ensuring that growth across both major segments remains interdependent.

Geographically, the market segmentation reveals disparities in access and adoption rates, with developed economies in North America and Europe holding larger market shares due to established dialysis infrastructure and higher rates of ESRD incidence. However, the rapidly expanding patient base and improving diagnostic capabilities in the Asia Pacific region are set to drive segment growth significantly over the forecast period. Understanding these segment dynamics is essential for stakeholders, as investments are increasingly targeting emerging economies for patient recruitment in clinical trials and commercial distribution of existing therapies.

The value chain for the Calciphylaxis Treatment Market begins with the Upstream Analysis, which focuses primarily on raw material sourcing and the synthesis of pharmacological agents, specifically Sodium Thiosulfate and various proprietary pharmaceutical compounds used off-label, such as calcimimetics and phosphate binders. Key activities at this stage involve sourcing high-purity chemical precursors and ensuring compliance with Good Manufacturing Practices (GMP). Given that many treatments are repurposed generic or specialty drugs, the manufacturing efficiency and quality control by primary producers are critical. For non-pharmacological treatments, the upstream phase involves the specialized production of complex medical devices, including advanced wound dressings, negative pressure wound therapy systems, and hyperbaric oxygen chambers, often necessitating specialized material science expertise and strict regulatory adherence.

The Midstream component of the value chain is dominated by clinical development, distribution, and logistics. Due to the rarity and severity of calciphylaxis, specialized clinical trials (often small, single-center studies) are necessary for novel drugs, involving collaborations between pharmaceutical companies, academic medical centers, and nephrology societies. Distribution channels are complex, involving both direct and indirect routes. Direct sales are often utilized for highly specialized medical devices or high-cost, proprietary drugs sold directly to major hospital systems and large dialysis organizations (like Fresenius and DaVita). Indirect channels rely on established pharmaceutical wholesalers and distributors to manage the supply of generic and off-label pharmacological agents to smaller specialty clinics and community hospitals, requiring careful inventory management due to the critical nature of the drugs.

The Downstream Analysis involves healthcare delivery and post-market activities. Treatment delivery is highly centralized, typically occurring in hospitals for acute management or specialized dialysis centers and dedicated wound care clinics for long-term maintenance. End-Users, which are primarily healthcare providers, require specialized training in drug administration (especially IV infusions like STS) and complex wound management. Post-market activities include rigorous pharmacovigilance for off-label drug use, ongoing data collection to improve treatment protocols, and continuous patient education. Potential customers or buyers are mainly institutional purchasers, including hospital formularies, integrated delivery networks (IDNs), and major dialysis service providers responsible for managing the chronic care needs of ESRD patients, who bear the primary responsibility for procuring and administering these critical therapies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $450 Million |

| Market Forecast in 2033 | $800 Million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bausch Health, Hikma Pharmaceuticals, Fresenius Medical Care, DaVita, Vifor Pharma, Amgen, Sanofi, Pfizer, Mallinckrodt, Bayer, Mylan N.V., Teva Pharmaceutical Industries, Sun Pharmaceutical Industries, Akebia Therapeutics, Rockwell Medical, Kissei Pharmaceutical, Takeda Pharmaceutical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The primary potential customers and end-users of calciphylaxis treatment products and services are large institutional buyers focused on managing chronic kidney disease and providing acute care. These include major hospital networks, particularly those with specialized nephrology, dermatology, and intensive care units capable of managing the systemic complications of CUA. Given that over 90% of calciphylaxis cases occur in patients with ESRD, large Dialysis Service Providers (DSPs) such as Fresenius Medical Care and DaVita are critical procurement decision-makers, as they integrate the administration of intravenous pharmacological agents (like STS) directly into the dialysis regimen and oversee chronic patient monitoring. These centers require consistent supply of high-volume pharmacological agents, advanced wound dressings, and pain management medications.

Specialty clinics, including dedicated wound care centers and multidisciplinary calciphylaxis clinics, represent another significant customer segment. These facilities focus on the non-pharmacological aspects of care, requiring advanced technologies such as Negative Pressure Wound Therapy (NPWT) devices and specialized surgical consumables for debridement procedures. Their purchasing decisions are often driven by efficacy data, ease of use for complex wound protocols, and overall patient compliance. Furthermore, government health programs and regional procurement agencies act as indirect customers, influencing market demand through national formulary listings and reimbursement decisions that determine which high-cost treatments are accessible to the broad patient population.

Finally, pharmaceutical wholesalers and distributors are essential customers within the procurement chain, managing the inventory and logistics for the wide array of off-label and supportive medications necessary for CUA management. As the treatment involves a cocktail of drugs—from anticoagulants and antibiotics to calcimimetics and chelation agents—distributors play a key role in ensuring the continuous and rapid supply of these crucial components to both hospital systems and outpatient clinics, underscoring their influence on market access and pricing stability.

The technology landscape for calciphylaxis treatment is primarily driven by advancements in drug delivery systems and diagnostic imaging, although the core therapeutic approach remains challenging due to the lack of specific FDA-approved drugs. Current technology focuses heavily on enhancing the efficacy and bioavailability of off-label pharmacological agents, particularly sodium thiosulfate (STS). Innovations are centered around developing stable, high-concentration formulations of STS for intravenous administration and exploring liposomal encapsulation techniques to improve drug targeting to the affected calcified tissue. Furthermore, sophisticated wound care technologies, including advanced hydrogels, antimicrobial dressings, and negative pressure wound therapy (NPWT) systems, form a crucial part of the treatment pathway, ensuring optimal management of the associated necrotic ulcers and preventing secondary infections which are major causes of mortality.

Beyond pharmacological innovation, diagnostic technologies are evolving to allow for earlier and more accurate identification of calciphylaxis, which is often misdiagnosed as cellulitis or vasculitis. High-resolution imaging technologies, such as improved computed tomography (CT) scans and magnetic resonance imaging (MRI) sequences designed to visualize early vascular calcification patterns, are being researched. Furthermore, minimally invasive diagnostic techniques, including advanced dermoscopy and specialized biopsy methods minimizing tissue damage, are critical for confirming diagnosis while reducing patient trauma. The integration of biomarker analysis, leveraging proteomics and metabolomics to identify patients at high risk before cutaneous lesions develop, represents a significant technological leap expected to improve prognostic outcomes.

The rise of personalized medicine approaches, supported by genomic sequencing and AI-driven data analysis, is beginning to influence treatment protocols. Technology platforms are being developed to monitor patient response to various therapeutic combinations—such as phosphate binders, calcimimetics, and bisphosphonates—in real-time. This allows clinicians to adjust dosages and combinations rapidly, moving away from generalized empirical treatments towards tailored interventions that address the underlying pathophysiology of individual patients, including their specific mineral metabolism profile. This integrated technological approach promises to mitigate the high morbidity and mortality rates associated with this rare but devastating condition.

The market is primarily driven by the escalating global incidence and prevalence of End-Stage Renal Disease (ESRD) and diabetes, the major risk factors associated with calciphylaxis. The necessity for effective, high-cost pharmacological and non-pharmacological treatments in this high-mortality patient group fuels demand.

Pharmacological treatments, particularly off-label use of intravenous sodium thiosulfate (STS), currently dominate the market due to its established role as the standard empirical intervention for minimizing calcium deposition. However, specialized wound care and surgical debridement segments contribute significantly to overall revenue.

Major restraints include the lack of specific FDA-approved drugs for calciphylaxis, resulting in reliance on expensive, off-label therapies with variable efficacy. Furthermore, the high mortality rate and complexities associated with definitive diagnosis often impede timely and optimized treatment initiation.

AI's primary influence will be in early diagnosis and personalized risk stratification. Machine learning algorithms can analyze complex patient data (dialysis parameters, lab results, imaging) to identify high-risk individuals earlier than conventional methods, leading to timely therapeutic intervention and improved prognosis.

North America maintains the largest market share, attributable to the high prevalence of ESRD, advanced healthcare infrastructure, significant R&D activity focusing on orphan drug designation, and robust reimbursement systems supporting the utilization of high-cost specialized treatments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.