ID : MRU_ 432130 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

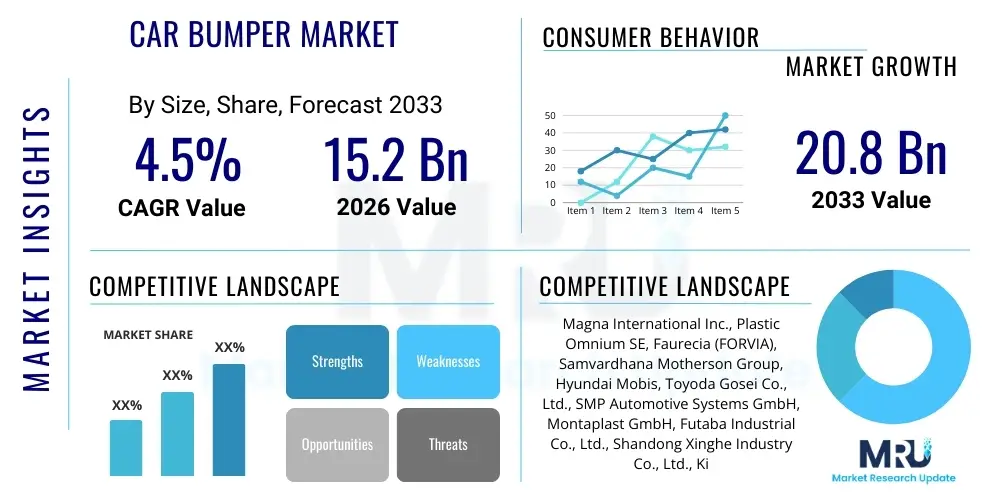

The Car Bumper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2026 and 2033. The market is estimated at USD 15.2 Billion in 2026 and is projected to reach USD 20.8 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global demand for passenger and commercial vehicles, especially across emerging economies in Asia Pacific, coupled with increasingly stringent government regulations pertaining to vehicle safety standards. The necessity for advanced energy absorption features and pedestrian protection systems is pushing Original Equipment Manufacturers (OEMs) to adopt sophisticated materials and design technologies in bumper systems, ensuring both compliance and improved consumer safety ratings. Furthermore, the growing trend of vehicle customization and aesthetic enhancement also contributes significantly to the aftermarket segment, where replacement and upgrade activities maintain a steady revenue stream.

The Car Bumper Market encompasses the manufacturing, supply, and distribution of vehicle protective structures designed primarily to absorb impact in low-speed collisions, thereby protecting the vehicle’s vital components and reducing injury risk to occupants and pedestrians. Bumpers, traditionally constructed from metals, have evolved significantly, now predominantly utilizing lightweight, high-strength plastics such as polypropylene (PP), polycarbonate (PC), and thermoplastic polyurethanes (TPU) to meet strict weight reduction and fuel efficiency mandates. Modern bumper systems are integral safety components, often incorporating advanced driver assistance system (ADAS) sensors, cameras, and aesthetic elements that define the vehicle’s brand identity, moving far beyond their original rudimentary function as simple protective beams. This technological integration transforms the bumper into a complex, multi-functional module essential for contemporary vehicle operation and safety ratings.

Major applications of car bumpers span the entire automotive ecosystem, including OEM installation in new vehicles (passenger cars, SUVs, trucks), and the robust aftermarket sector which caters to collision repair, replacement, and aesthetic modifications. The continuous global increase in vehicle production, driven by demographic expansion and rising disposable incomes in developing nations, serves as a primary driver for market growth. Moreover, mandatory safety certifications, such as those imposed by Euro NCAP and NHTSA, necessitate frequent redesigns and material innovation, keeping the primary market dynamic and technologically intensive. These regulations ensure that bumpers not only withstand minor impacts but also manage crash energy effectively to protect vulnerable road users, reinforcing their critical role in passive safety systems.

The key benefits associated with modern car bumpers include enhanced vehicle safety through impact energy dissipation, lower insurance costs due to minimized repair expenses in minor accidents, and crucial support for integrated ADAS features like parking assist sensors and radar systems. Driving factors for market acceleration include continuous material science advancements focusing on lightweighting without compromising strength, the rigorous imposition of global safety standards requiring sophisticated bumper designs (e.g., pedestrian protection mandates), and the rapid expansion of the electric vehicle (EV) segment. EVs, often demanding highly optimized aerodynamics and battery protection, necessitate specialized bumper designs, offering new avenues for market participants focusing on innovative composite materials and structural integration.

The Car Bumper Market is characterized by robust growth, primarily propelled by the convergence of tightening global automotive safety regulations and the sustained high volume of global vehicle manufacturing, particularly in the APAC region. Current business trends indicate a strong shift toward thermoplastic materials, replacing traditional metal bumpers to align with corporate average fuel economy (CAFE) standards and emission reduction targets. Furthermore, the integration of smart technologies, where the bumper serves as a vital housing unit for complex ADAS sensors (Lidar, Radar, Ultrasonic), is transforming the component's complexity and value proposition, driving increased R&D investment among Tier 1 suppliers. Strategic partnerships between material producers and OEMs focused on recyclable and sustainable composite materials are also emerging as a dominant theme, reflecting the industry's commitment to circular economy principles and environmental governance. The aftermarket segment remains critical, influenced heavily by collision rates and aging vehicle fleets, sustaining demand for repair and replacement parts.

Regional trends distinctly highlight Asia Pacific as the undeniable growth engine for the car bumper market, attributable to the massive manufacturing bases in China, India, and Japan, coupled with rapidly expanding vehicle ownership. North America and Europe, while being mature markets, exhibit demand stability driven by stringent regulatory frameworks concerning pedestrian safety and advanced integration of sensor technology required for L3 (Conditional Automation) and higher levels of autonomous driving capabilities. The European market, in particular, is witnessing intense focus on lightweighting and sustainable manufacturing processes, favoring suppliers who can offer advanced, injection-molded plastic solutions with high recyclability. Conversely, emerging markets in Latin America and the Middle East and Africa are seeing growth linked primarily to initial vehicle penetration rates and urbanization, often demanding durable, lower-cost bumper solutions adapted for varied road conditions.

Segmentation analysis reveals that the passenger vehicle category dominates the market share due to sheer volume, although the commercial vehicle segment is experiencing accelerated growth driven by increased logistics activities and infrastructure development. Material segmentation heavily favors plastic/polymer bumpers over metallic alternatives, owing to superior design flexibility, weight advantages, and cost-effectiveness in high-volume production. Within the technology landscape, standard bumpers are gradually being superseded by advanced, sensor-integrated bumper systems (Smart Bumpers). The OEM channel constitutes the largest revenue stream, but the Independent Aftermarket (IAM) maintains significant influence, especially for cost-conscious consumers and older vehicle models. The overall market trajectory emphasizes innovation in material composition, manufacturing efficiency (e.g., faster cycle times in injection molding), and functional integration to support the future generation of smart, connected, and autonomous vehicles.

User queries regarding AI's influence on the Car Bumper Market primarily revolve around how AI and Machine Learning (ML) optimize design and manufacturing processes, improve quality control, and integrate with autonomous driving sensors housed within the bumper structure. Common concerns include the complexity of integrating advanced sensor arrays (Lidar, Radar) which generate vast amounts of data requiring real-time AI processing for reliable autonomous functions, and how AI-driven predictive maintenance can affect bumper durability and replacement cycles. Users are also interested in the application of Generative Design algorithms to create lightweight yet structurally superior bumper geometries that meet stringent crash requirements more efficiently than traditional methods. The core expectation is that AI will enhance production efficiency, reduce material waste, and ensure the flawless function of safety-critical ADAS components embedded within the bumper system, leading to personalized and optimized crash energy management solutions.

The direct impact of AI is transforming the lifecycle of the bumper, from concept design to end-of-life recycling. In design, AI algorithms can simulate millions of impact scenarios instantly, optimizing material thickness, rib structure, and energy absorber geometry to achieve target safety ratings with minimum weight. This hyper-optimization is crucial for EVs where every kilogram matters. On the manufacturing floor, AI-powered computer vision systems are revolutionizing quality control, identifying micro-defects in molded plastics or paint finishes that are imperceptible to the human eye, ensuring zero-defect delivery of high-value components. This automation significantly reduces rejection rates and increases overall production throughput, addressing the stringent quality demands of OEMs, particularly regarding the flawless surface preparation needed for integrated sensors to function accurately.

Furthermore, the bumper’s role as the primary housing for ADAS sensors makes its function inherently linked to Artificial Intelligence, particularly in autonomous vehicles. AI algorithms process the data collected by bumper-mounted Lidar and radar systems to enable essential functions like adaptive cruise control, collision avoidance, and automated parking. The precise manufacturing tolerances and material choice of the bumper directly affect sensor calibration and performance, meaning AI-driven validation of the component’s structural integrity and placement accuracy is paramount. This deep integration means future bumper designs will not just be passive safety components but active, intelligent systems critical for the vehicle's operational autonomy, pushing manufacturers to invest heavily in smart production lines capable of handling these high-precision requirements, validated continuously by sophisticated AI modeling and simulation platforms.

The Car Bumper Market is heavily influenced by a critical balance of Drivers (D), Restraints (R), and Opportunities (O), which collectively shape the competitive and strategic landscape, constituting the Impact Forces. Key drivers include rigorous global safety regulations, especially those mandated for pedestrian protection (e.g., Euro NCAP requirements), and the accelerating global production of both ICE and electric vehicles, demanding high volumes of components. Restraints largely center around the volatility of raw material prices, particularly for petroleum-derived polymers like polypropylene, alongside the high initial investment required for sophisticated tooling and injection molding machinery capable of producing complex, high-tolerance bumper assemblies integrated with ADAS features. The significant opportunity lies in the burgeoning electric vehicle sector, which requires unique, lightweight, and aerodynamically optimized bumper systems, offering a premium segment for innovative material suppliers and component manufacturers.

The principal impact forces driving market evolution include technological advancements, where materials science pushes towards lighter, stronger, and more sustainable composites (e.g., natural fiber composites, recycled plastics). Safety compliance acts as a regulatory force, mandating continuous design evolution to meet evolving crash standards, forcing manufacturers to innovate or lose market share. Economic forces, such as the overall health of the automotive industry and consumer spending on new vehicles, directly influence OEM demand, while collision rates and insurance costs dictate the volume in the lucrative aftermarket. Furthermore, competitive intensity among Tier 1 suppliers is high, leading to continuous efforts to enhance manufacturing efficiency and offer value-added services, particularly in sensor integration and painted component delivery (just-in-time supply).

The interplay of these factors defines market direction. While mandatory safety standards (Driver) guarantee baseline demand and continuous technological upgrading, the simultaneous pressure for vehicle lightweighting (Opportunity) necessitates material innovation, which often runs counter to the cost pressures arising from polymer price fluctuations (Restraint). Companies that successfully navigate this complex environment by securing stable, long-term supply agreements for advanced materials and investing in highly automated production lines capable of precision ADAS sensor integration will gain a substantial competitive edge. The shift toward modular vehicle platforms further streamlines manufacturing but increases the need for highly precise, interchangeable bumper systems, making logistical efficiency and quality control paramount impact forces.

The Car Bumper Market is comprehensively segmented across several dimensions, allowing for precise targeting and strategic analysis of different demand pockets. The key segments include type (standard vs. designer), material (plastics/polymers, metals, composites), technology (conventional vs. smart/sensor-integrated), and end-use channel (OEM vs. Aftermarket). This structure reflects the diverse needs of the automotive industry, ranging from high-volume, cost-effective solutions for entry-level vehicles to technologically advanced, high-performance units for luxury and autonomous vehicles. The dominance of plastic materials in almost all segments underscores the industry's commitment to weight reduction and flexible design, whereas the rapid growth of sensor-integrated bumpers signifies the paradigm shift towards active safety components.

A deeper look into the End-Use segmentation reveals that the Original Equipment Manufacturer (OEM) segment accounts for the majority revenue share, directly correlating with global new vehicle production volumes. However, the Aftermarket segment (IAM – Independent Aftermarket) is crucial for profitability and stability, driven by collision damage repair, refurbishment, and vehicle personalization. Geographically, the segmentation confirms Asia Pacific's leadership in volume production, contrasting with the maturity and high technological demands of North American and European markets. Understanding these segment dynamics is essential for market participants, who must tailor their production capabilities and material portfolios to serve these distinct needs—for example, focusing on high-volume polypropylene injection molding for OEM contracts while maintaining quick turnaround capabilities for diverse, painted, and customized aftermarket requirements.

The value chain of the Car Bumper Market is extensive, starting from raw material procurement and extending through highly specialized manufacturing processes, complex logistics, and final installation or replacement. Upstream analysis involves major chemical and petrochemical companies supplying crucial raw materials such as polypropylene resins, painting materials, and specialized composite fibers. Price fluctuations in crude oil directly impact the cost of these polymers, making raw material sourcing and inventory management critical for margin stability. Suppliers often engage in long-term contracts with large Tier 1 component manufacturers to ensure a consistent supply chain, especially for specialized grades required for structural integrity and high-quality surface finish necessary for paint adhesion and sensor transparency.

The core manufacturing stage is dominated by Tier 1 suppliers who specialize in high-pressure injection molding, subsequent painting processes, and final assembly, often including the integration of lighting and ADAS sensors (Smart Bumpers). These manufacturers invest heavily in tooling and robotics to ensure high precision and repeatability, vital for meeting OEM standards and maintaining profitability in a volume-driven market. Downstream activities involve the distribution channel, which is bifurcated: Direct distribution to OEMs operates on a just-in-time (JIT) delivery model, requiring suppliers to locate facilities near automotive assembly plants. The indirect channel serves the aftermarket (IAM) through national distributors, wholesale auto parts stores, and independent repair shops, where speed, inventory breadth, and competitive pricing are the main determinants of success.

The complexity of modern bumpers—acting as structural components and sensor platforms—necessitates strong collaboration across the value chain. OEMs often dictate material specifications and design tolerances, forcing upstream suppliers to innovate in polymer composition (e.g., crash-optimized, high-impact strength PP). Distribution efficiency is critical for both channels; direct supply minimizes inventory costs for OEMs, while a robust indirect network ensures timely availability of replacement parts across vast geographical areas. Strategic management of this value chain, focusing on process automation, material recycling capabilities, and localized production hubs, offers competitive differentiation, optimizing both cost structure and responsiveness to rapid shifts in automotive design and consumer demand.

The primary customers for the Car Bumper Market are broadly categorized into two distinct segments: Original Equipment Manufacturers (OEMs) and the diverse components of the Automotive Aftermarket. OEMs, including global giants like Toyota, Volkswagen Group, and General Motors, represent the largest and most demanding customer segment, requiring high-volume, custom-designed bumpers that meet specific vehicle platform specifications, crash test standards, and aesthetic requirements. These customers prioritize quality assurance, consistency of supply (JIT delivery), and the ability of suppliers to integrate complex technologies like ADAS sensors seamlessly. Winning OEM contracts typically requires significant capital investment, validated quality management systems, and a strong track record of technological partnership and co-development with automotive design teams.

The Aftermarket segment constitutes the second major customer base, comprising independent repair shops, collision centers, body shops, specialized vehicle modifiers, and large-scale parts distributors. These customers seek replacement bumpers for repair following accidents or for vehicle customization. Unlike the OEM segment which values long-term partnership and innovation, the Aftermarket prioritizes speed of delivery, cost-effectiveness, and the availability of parts for a wide range of makes and models, including older vehicles. The market is segmented into OES (Original Equipment Supplier) parts, sold through authorized dealer networks, and IAM (Independent Aftermarket) parts, which are often non-OEM sourced but must comply with fit, form, and function standards. The increasing average age of vehicles globally ensures sustained demand from this resilient segment, particularly in emerging economies where collision rates and repair requirements are high.

A growing niche within the customer base includes vehicle customization companies and fleet operators. Customization companies require specialized, high-performance composite bumpers (e.g., carbon fiber) for aesthetic and aerodynamic enhancements, catering to the luxury and sports vehicle segments. Fleet operators (taxis, logistics companies) prioritize highly durable, easy-to-repair bumper systems that minimize vehicle downtime and long-term maintenance costs. The increasing complexity of ADAS integration means that collision centers are becoming increasingly sophisticated customers, requiring training and standardized processes to correctly replace and recalibrate smart bumpers, thus shifting customer focus from purely material cost to total repair quality and calibration service offerings.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 20.8 Billion |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Magna International Inc., Plastic Omnium SE, Faurecia (FORVIA), Samvardhana Motherson Group, Hyundai Mobis, Toyoda Gosei Co., Ltd., SMP Automotive Systems GmbH, Montaplast GmbH, Futaba Industrial Co., Ltd., Shandong Xinghe Industry Co., Ltd., Kirchhoff Automotive GmbH, Polytec Holding AG, Flex-N-Gate Corporation, Valeo S.A., Yanfeng Automotive Interiors, BASF SE (Material Supplier), LyondellBasell (Material Supplier), Trinseo S.A., Trelleborg AB, Dongfeng Motor Parts and Components Group Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Car Bumper Market is rapidly evolving beyond basic impact absorption, focusing heavily on lightweighting, functional integration, and sustainable manufacturing practices. The primary technology remains advanced injection molding, but modern applications utilize multi-shot molding and gas injection molding techniques to create complex geometries and integrated mountings with superior dimensional stability and reduced component weight. Materials science is critical, driving the adoption of specialized thermoplastic polyolefins (TPOs) and engineered plastics that offer high impact resistance, excellent surface quality for painting, and resistance to environmental stress, all while maximizing recyclability. Furthermore, the use of advanced simulation tools (FEA - Finite Element Analysis) is now standard practice, allowing engineers to predict crash performance and optimize energy absorber designs virtually, significantly reducing the timeline and cost associated with physical prototyping and testing, ensuring compliance with stringent safety standards like RCAR (Research Council for Automobile Repairs) guidelines.

A pivotal technological transformation is the advent of the "Smart Bumper," which acts as a crucial platform for Advanced Driver Assistance Systems (ADAS). This involves precision integration of high-value sensors such as radar, ultrasonic sensors, and Lidar units directly into the bumper fascia, often behind specialized, radar-transparent polymer covers. This integration demands ultra-precise manufacturing tolerances and materials that do not interfere with sensor signal transmission or reception, requiring sophisticated material coatings and mounting mechanisms that withstand vibration and environmental factors while maintaining calibration. This trend pushes component manufacturers into the electronics and systems integration sphere, requiring investment in specialized testing and calibration equipment to validate the complete assembly before delivery to the OEM line.

Sustainability technologies are also gaining prominence. Manufacturers are increasingly utilizing closed-loop recycling systems, incorporating post-consumer recycled (PCR) plastics back into bumper production without compromising structural integrity or aesthetic quality. This addresses both regulatory pressures for material stewardship and corporate sustainability goals. Furthermore, advanced surface treatment technologies, including low-VOC (Volatile Organic Compounds) painting systems and advanced clear coats, enhance durability and aesthetic appeal while minimizing environmental impact. The development of modular bumper systems that facilitate quicker repair and replacement of specific sections (rather than the whole assembly) also represents a functional technology improvement aimed at reducing repair costs and insurance claim severity, thereby adding value throughout the component lifecycle.

The shift is primarily driven by regulatory mandates for vehicle lightweighting (fuel efficiency and emission reduction) and improved design flexibility. Modern plastics (PP, TPO) offer excellent energy absorption, corrosion resistance, and are lighter and often cheaper than metallic counterparts, facilitating complex aerodynamic and aesthetic designs necessary for contemporary vehicles, especially EVs.

ADAS integration is significantly increasing the complexity and cost of bumpers. Bumpers must now function as high-precision housing units for expensive sensors (Radar, Lidar). This requires new materials that are radar-transparent, ultra-precise manufacturing tolerances, and specialized testing/calibration, transforming the bumper from a simple passive component into a critical active safety system.

Asia Pacific (APAC) holds the largest market share in car bumper production and consumption. This dominance is attributed to the presence of high-volume automotive manufacturing hubs, particularly in China and India, coupled with rapid urbanization and subsequent increases in new vehicle sales across the region.

The OEM segment focuses on high-volume, custom-designed, JIT supply for new vehicle assembly, prioritizing technological integration and quality. The Aftermarket (IAM) focuses on demand for replacement parts for collision repair and aesthetic upgrades, prioritizing speed of delivery, availability across vehicle models, and competitive pricing.

Sustainability is crucial, driving innovation in using Post-Consumer Recycled (PCR) plastics and bio-based composites. Manufacturers are adopting closed-loop recycling processes and low-VOC painting systems to reduce their environmental footprint, meeting rising consumer and regulatory demands for circular economy practices in automotive component production.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.